BIS: Stablecoin and Safe Asset Prices

Dollar-backed stablecoins have experienced significant growth and are expected to reshape financial markets.

Dollar-backed stablecoins have experienced significant growth and are expected to reshape financial markets.Authors: Rashad Ahmed and Iñaki Aldasoro Compiled by: Institute of Financial Technology, Renmin University of China

Introduction

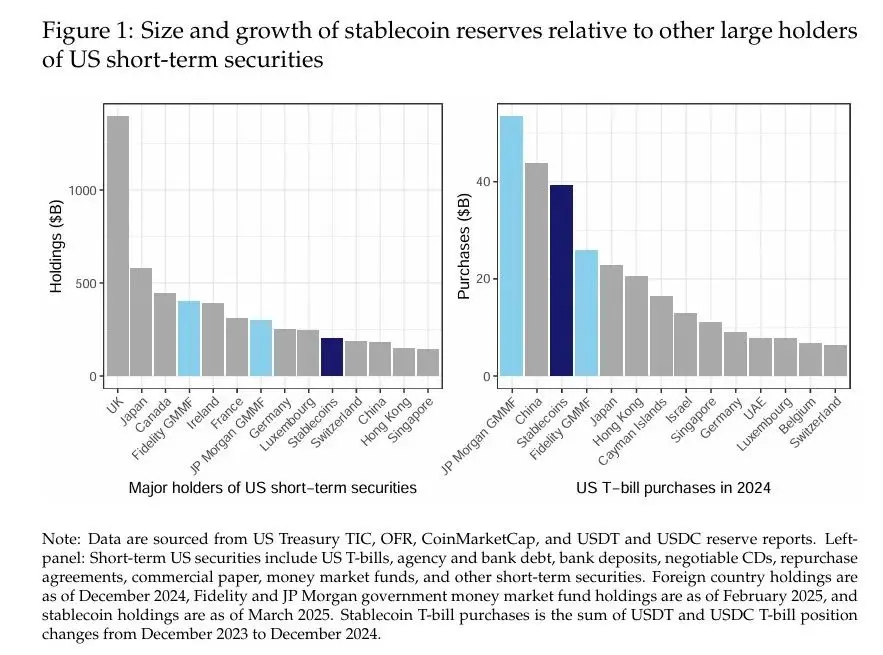

Dollar-backed stablecoins have experienced significant growth and are poised to reshape financial markets. As of March 2025, the total assets under management of cryptocurrencies backed by commitments to redeem at face value for dollars and dollar-denominated assets exceeded $200 billion, surpassing the short-term U.S. securities held by major foreign investors such as China (Figure 1, left). Stablecoin issuers, particularly Tether (USDT) and Circle (USDC), primarily support their tokens through U.S. Treasury bills (T-bills) and money market instruments, making them significant participants in the short-term debt market. In fact, in 2024, dollar-backed stablecoins purchased nearly $40 billion in U.S. short-term Treasury securities, comparable in scale to the largest government money market funds in the U.S. and exceeding the purchases of most foreign investors (Figure 1, right). While previous research has mainly focused on the role of stablecoins in cryptocurrency volatility (Griffin and Shams, 2020), their impact on the commercial paper market (Barthelemy et al., 2023), or their systemic risks (Bullmann et al., 2019), their interactions with traditional safe asset markets remain underexplored.

This paper investigates whether stablecoin flows exert measurable demand pressure on U.S. Treasury yields. We document two key findings. First, stablecoin flows depress short-term Treasury yields, with effects comparable to small-scale quantitative easing on long-term yields. In our most stringent specification, we overcome endogeneity issues by using a series of crypto shocks that affect stablecoin flows but do not directly impact Treasury yields. We find that a $3.5 billion inflow of stablecoins (i.e., 2 standard deviations) leads to a decline of about 2-2.5 basis points (bps) in the 3-month Treasury yield within 10 days. Second, we decompose the yield impact into issuer-specific contributions, finding that USDT has the largest contribution to the yield suppression, followed by USDC. We discuss the policy implications of these findings for monetary policy transmission, stablecoin reserve transparency, and financial stability.

Our empirical analysis is based on daily data from January 2021 to March 2025. To construct a measure of stablecoin flows, we collect market capitalization data for the six largest dollar-backed stablecoins and aggregate them into a single figure. We then use the 5-day change in total stablecoin market capitalization as a proxy for stablecoin inflows. We collect data on the U.S. Treasury yield curve and cryptocurrency prices (Bitcoin and Ethereum). We choose the 3-month Treasury yield as our outcome variable of interest, as the largest stablecoins have disclosed or publicly indicated this maturity as their preferred investment horizon.

A simple univariate local projection linking changes in the 3-month Treasury yield to 5-day stablecoin flows may be severely affected by endogeneity bias. In fact, estimates from this "naive" specification suggest that a $3.5 billion inflow of stablecoins is associated with a decline of up to 25 bps in the 3-month Treasury yield within 30 days. This magnitude of effect is incredible, as it suggests that a 2 standard deviation inflow of stablecoins has an impact on short-term rates similar to that of a Federal Reserve policy rate cut. We believe these large estimates can be explained by the presence of endogeneity, which biases the estimates downward (i.e., larger negative estimates relative to the true effect) due to omitted variable bias (as potential confounding factors are not controlled for) and simultaneity bias (as Treasury yields may influence stablecoin flows).

To overcome endogeneity issues, we first extend the local projection specification to control for the U.S. Treasury yield curve and cryptocurrency prices. These control variables are divided into two groups. The first group includes forward changes in U.S. Treasury yields at maturities other than 3 months (from t to t+h). We control for the evolution of the forward yield curve to isolate the conditional effect of stablecoin flows on the 3-month yield based on changes in nearby maturity yields within the same local projection horizon. The second group of control variables includes the 5-day changes (from t-5 to t) in Treasury yields and cryptocurrency prices to control for various financial and macroeconomic conditions that may be related to stablecoin flows. After introducing these control variables, local projection estimates indicate that after a $3.5 billion inflow of stablecoins, Treasury yields decline by 2.5 to 5 bps. These estimates are statistically significant but nearly an order of magnitude smaller than the "naive" estimates. The attenuation of the estimates is consistent with our expectations regarding the sign of endogeneity bias.

In a third specification, we further strengthen identification through an instrumental variable (IV) strategy. Following the approach of Aldasoro et al. (2025), we instrument the 5-day stablecoin flows with a series of crypto shocks based on the unpredictable components of the Bloomberg Galaxy Crypto Index. We use the cumulative sum of the crypto shock series as an instrumental variable to capture the specific but persistent nature of crypto market booms and busts. The first-stage regression of 5-day stablecoin flows on the cumulative crypto shocks satisfies the relevance condition and shows that stablecoins tend to experience significant inflows during crypto market booms. We believe that the exclusion restriction is satisfied, as the specific crypto boom is sufficiently isolated and does not have a meaningful impact on Treasury market pricing—unless issuers use these funds to purchase Treasuries through stablecoin inflows.

Our IV estimates indicate that a $3.5 billion inflow of stablecoins would lead to a decline of 2-2.5 bps in the 3-month Treasury yield. These results are robust to changing the set of control variables by focusing on maturities that are less correlated with the 3-month yield—if anything, the results are slightly stronger in magnitude. In additional analyses, we find no spillover effects of stablecoin purchases on longer maturities such as the 2-year and 5-year, although we do observe limited spillover effects at the 10-year maturity. In principle, the effects of inflows and outflows may be asymmetric, as the former allows issuers some discretion in timing purchases, while such flexibility is absent under tight market conditions. When we allow the estimates to differ under inflow and outflow conditions, we indeed find that outflows have a quantitatively larger impact on yields than inflows (approximately +6-8 bps versus -3 bps, respectively). Finally, based on our IV strategy and baseline specifications, we also decompose the estimated yield impact of stablecoin flows into issuer-specific contributions. We find that the average contribution of USDT flows is the largest, at about 70%, while USDC flows contribute approximately 19% to the estimated yield impact. Other stablecoin issuers contribute the remaining portion (about 11%). These contributions are qualitatively proportional to the size of the issuers.

Our findings have important policy implications, especially if the stablecoin market continues to grow. Regarding monetary policy, our yield impact estimates suggest that if the stablecoin industry continues to expand rapidly, it may ultimately affect the transmission of monetary policy to Treasury yields. The growing influence of stablecoins in the Treasury market may also lead to a scarcity of safe assets for non-bank financial institutions, potentially affecting liquidity premiums. Regarding stablecoin regulation, our results highlight the importance of transparent reserve disclosures to effectively monitor concentrated stablecoin reserve portfolios.

As stablecoins become large investors in the Treasury market, potential financial stability implications may arise. On one hand, it exposes the market to the risk of sell-offs that could occur during a run on major stablecoins. In fact, our estimates suggest that this asymmetric effect is already measurable. The magnitude of our estimates may be a lower bound for potential sell-off effects, as they are based on a sample primarily from a growing market, thus potentially underestimating the potential for nonlinear effects under severe stress. Furthermore, stablecoins themselves may promote arbitrage strategies, such as Treasury basis trading, through investments supported by Treasury collateralized reverse repos, which is a primary concern for regulators. Equity and liquidity buffers may mitigate some of these financial stability risks.

Data and Methodology

Our analysis is based on daily data from January 2021 to March 2025. First, we collected market capitalization data for six dollar-backed stablecoins from CoinMarketCap: USDT, USDC, TUSD, BUSD, FDUSD, and PYUSD. We aggregated the data for these stablecoins to obtain a measure of total stablecoin market capitalization, and then calculated its 5-day change. We collected daily prices for Bitcoin and Ethereum, the two largest cryptocurrencies, from Yahoo Finance. We obtained daily series of the U.S. Treasury yield curve from FRED. We considered the following maturities: 1 month, 3 months, 6 months, 1 year, 2 years, and 10 years.

As part of our identification strategy, we also used a daily version of the crypto shock series proposed by Aldasoro et al. (2025). Crypto shocks are calculated as the unpredictable components of the Bloomberg Galaxy Crypto Index (BGCI), which captures broad dynamics in the crypto market (we will provide more details about crypto shocks below).

Figure 2 shows the market capitalization of dollar-backed stablecoins and U.S. Treasury yields during the sample period. Since the second half of 2023, the market capitalization of stablecoins has been rising, with significant growth at the beginning and end of 2024. The industry is highly concentrated, with the two largest stablecoins (USDT and USDC) accounting for over 95% of the outstanding amount. The Treasury yields in our sample cover both the tightening cycle and the pause and subsequent easing cycle that began around mid-2024. The sample period also includes a period of notable yield curve inversion, most prominently illustrated by the deep blue line moving from the bottom to the top of the yield curve.

Conclusion and Implications

Magnitude. The estimated yield impact of 2 to 2.5 bps from a $3.5 billion (or 2 standard deviations) inflow of stablecoins suggests that by the end of 2024, the industry could be around $200 billion in size. With the continued growth of the stablecoin industry, it is not unreasonable to expect its footprint in the Treasury market to increase. Assuming the stablecoin industry grows tenfold to $2 trillion by 2028, the 5-day flow differences would scale proportionally. Then, a 2 standard deviation flow would reach approximately $11 billion, with an estimated impact on Treasury yields of -6.28 to -7.85 bps. These estimates indicate that the growing stablecoin industry could ultimately suppress short-term yields, thereby fully affecting the transmission of Federal Reserve monetary policy to market yields.

Mechanisms. Stablecoins can influence Treasury market pricing through at least three channels. The first is through direct demand, as purchases of stablecoins reduce the supply of available cash, provided that the funds flowing into stablecoins do not flow into Treasuries. The second channel is indirect, as demand for U.S. Treasuries from stablecoins may alleviate dealers' balance sheet constraints. This, in turn, would affect asset prices, as it would reduce the amount of Treasuries that dealers need to absorb. The third channel is through signaling effects, as large inflows may signal institutional risk appetite or lack thereof, which investors then incorporate into the market.

Policy Implications. Policies surrounding reserve transparency will interact with the growing footprint of stablecoins in the Treasury market. For example, the granular reserve disclosures of USDC enhance market predictability, while the opacity of USDT complicates analysis. Regulatory requirements for standardized reporting could mitigate systemic risks associated with concentrated ownership of Treasuries by making some of these flows more transparent and predictable. Although the stablecoin market remains relatively small, stablecoin issuers have already become significant participants in the Treasury market, and our findings suggest that yields have already been affected to some extent at this early stage.

Monetary policy will also interact with the role of stablecoins as investors in the Treasury market. For instance, in a scenario where stablecoins become very large, yield compression driven by stablecoins could weaken the Federal Reserve's control over short-term rates, potentially necessitating coordination among regulators on monetary policy to effectively influence financial conditions. This perspective is not merely theoretical— for example, the "green dilemma" of the early 21st century arose from the Federal Reserve's monetary policy not having the expected impact on long-term Treasury yields. At that time, this was primarily due to the enormous demand from foreign investors for U.S. Treasuries affecting the pricing in the U.S. Treasury market.

Finally, the emergence of stablecoins as investors in the Treasury market has clear implications for financial stability. As discussed in the literature on stablecoins, they can still operate, with their balance sheets affected by liquidity and interest rate risks, as well as some credit risks. Therefore, if a major stablecoin faces severe redemption pressure, particularly considering the lack of access to discount windows or a lender of last resort, concentrated positions in Treasuries could expose the market to sell-offs, especially for those Treasuries that do not mature immediately. The evidence we provide regarding asymmetric effects suggests that the impact of stablecoins on the Treasury market may be greater in environments characterized by large-scale and abrupt outflows. In this regard, the magnitudes suggested by our estimates may be a lower bound, as they are based on a sample that primarily includes a growing market. As the stablecoin industry grows, this situation may change, heightening concerns about the stability of the Treasury market.

Limitations. Our analysis provides some preliminary evidence of the emerging footprint of stablecoins in the Treasury market. However, our results should be interpreted with caution. First, we face data constraints in our analysis due to incomplete disclosures of the maturity dates of USDT's reserve portfolio, complicating identification. Therefore, we must assume which Treasury maturities are most likely to be affected by stablecoin flows. Second, we control for financial market volatility by including returns on Bitcoin and Ethereum, as well as changes in yields across various Treasury maturities. However, these variables may not fully capture the risk sentiment and macroeconomic conditions that jointly influence stablecoin flows and Treasury yields. We attempt to address this issue through an instrumental variable strategy, but we recognize that our instruments may themselves be limited, including mis-specifications in our local project model. Additionally, due to data limitations and the high concentration in the stablecoin industry, our estimates rely almost entirely on time series variation, as the cross-section is too limited to be utilized in any meaningful way.

In summary, stablecoins have become significant participants in the Treasury market, exerting measurable and substantial impacts on short-term yields. Their growth blurs the lines between cryptocurrencies and traditional finance, necessitating regulatory attention to reserve practices, potential impacts on monetary policy transmission, and financial stability risks. Future research could explore cross-border spillover effects and interactions with money market funds, particularly during liquidity crises.

Risk warning

Risk warning Risk warning

Risk warning