The trend of hyper-gambling series, is collectible card game RWA a good business?

This article explores the seemingly "on-chain" nature of the TCG (trading card game) RWA market, revealing its true growth engine behind it—"Hypergamblification."

This article explores the seemingly "on-chain" nature of the TCG (trading card game) RWA market, revealing its true growth engine behind it—"Hypergamblification."Original author: Bonna

TLDR: Everything can be wrapped in the shell of "entertainment + financialization," where gambling is no longer an accessory but becomes the core of emotional consumption. This provides a new narrative for IP/NFT: value does not necessarily have to extend to financial markets like lending and derivatives, but can instead be built directly through "entertainment + finance" to create independent and sustainable consumption scenarios. The financialized/gambling experience in games can itself be the endpoint. --- This logic has been validated by Pop Mart and is now being reaffirmed in card blind boxes, and will likely be replayed in more scenarios in the future.

Recently, the trading market for card chains has seen a surge in activity, revenue, and market value.

Many people subconsciously adopt the narrative: "Traditional card trading is inefficient, while on-chain solves the problem." However, if you delve into the TCG market, you will find that the reality is not so.

1. The TCG Secondary Market Has Been Standardized in the Internet Era

The secondary market for collectible trading cards has long been very mature in Europe and America, with a closed loop of "grading --- vaulting --- trading --- supporting."

1) Grading Provides Authentication and Condition Assessment, Along with a Rating.

Unlike the authentication in the second-hand luxury goods/used market, which is more about "can sell/cannot sell + general condition" and serves as a price reference with noticeable price arbitrage across different regions; TCG grading is almost an absolute price anchor, with clear price tiers between different grades.

Main participants include:

- @PSAcard the largest grading agency globally

- @beckettcollect known for its more detailed grading system

- @CGCCards started with comic book grading, fast and cheap

2) Vaulting Provides Card Storage, Avoiding Risks from Cross-Border Transport.

These vaulting services are often deeply integrated with trading markets, with most vault service providers having their own auction platforms or directly connecting with trading markets. Users can achieve "one-click consignment" after completing vaulting, a model akin to traditional art auction houses (like Christie's and Sotheby's) that come with storage vaults and seamlessly integrate with auction services. Main participants include:

- @FanaticsCollect has its own auction house and high-end card inventory

- @GoldinCo under PSA, high-end card auctions + vaulting

- @eBay connects trading and vaulting, with the highest coverage

3) Marketplaces Are the Main Places for Price Discovery and Liquidity Aggregation of Cards.

The TCG trading market is divided into two categories: one is direct trading markets, where both buyers and sellers can place orders, and buyers can also choose to buy directly according to sellers' listings, which is essentially no different from the NFT trading market experience, with the distinction being that card market pricing is anchored and referenced by grading, making it more orderly. The other category is auction markets, where transactions are made through bidding, with high-end cards often going through auctions to establish pricing, which is then transmitted to the entire market. Main participants include:

- @eBay the largest globally, with massive transaction data

- @TCGplayer in North America, aggregating offline store inventory

- @CardmarketMagic the largest card market in Europe

- @GoldinCo the auction house for high-end cards under PSA

- @FanaticsCollect high-end collectibles auctions and direct sales

4) Supporting (Data, Insurance, Logistics) Are Service Trading Supporting Links and Infrastructure.

Main participants include:

- Data platforms: PokémonPrice, eBay, etc.

- Insurance: Collectors Insurance Service, etc.

- Logistics: FedEx, DHL, and other carriers

2. The Real Growth Source of TCG RWA: Blind Boxes

In a trading market that heavily relies on network effects and liquidity scale, it is extremely difficult to compete for pricing power and price discovery on-chain when most card users are already accustomed to traditional channels like eBay.

If you actually open the Marketplace pages of these TCG RWA platforms, you will find that transaction activity is generally very low, which further indicates that replacing traditional trading markets on-chain is not so easy, especially in categories like RWA that heavily depend on offline infrastructure (grading, vaulting, logistics, insurance).

Moreover, most core players in the TCG industry chain often span multiple links (grading + vault + integrated auction/trading), which means that simply creating an "on-chain trading market" will not provide a competitive moat. So where does the rapid growth of these platforms come from? The answer is: Blind Boxes (Hypergamblification)

They are not providing a card trading market but are selling financial blind boxes that have been repackaged. This offers a quasi-gambling unpacking experience, allowing users to pay for uncertainty and sensory stimulation. For example:

- @Courtyard_io is closer to "on-chain unpacking," digitizing physical card packs, allowing users to directly open packs after purchase;

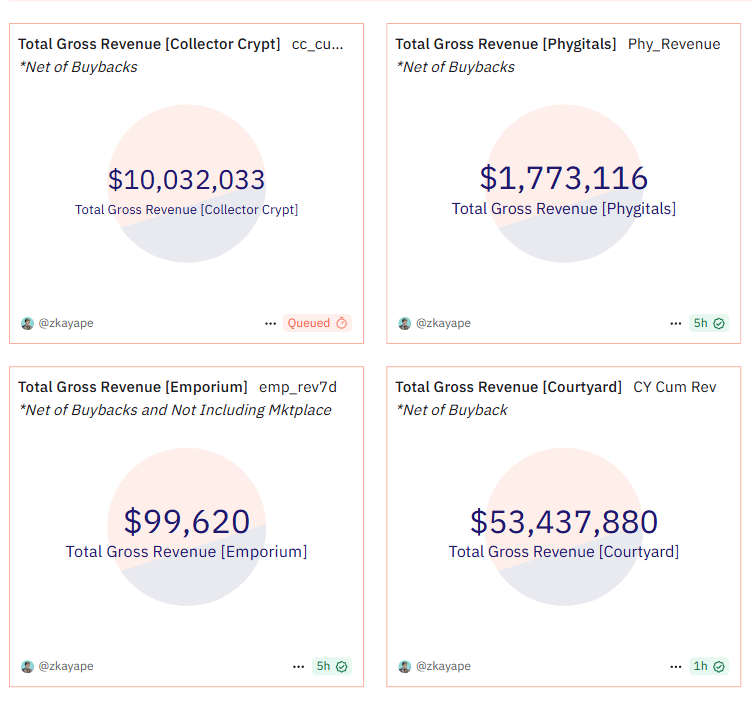

- @CollectorCrypt, @Phygitals, and @TCGEmporium directly introduce the capsule toy/vending machine mechanism from Japan, where users spend money to "insert coins" and randomly draw cards.

So where do the cards in these blind boxes come from? Some come from platform inventory (pre-purchased graded cards), and some come from user consignment (the platform offers a guaranteed selling price).

Additionally, since these platforms only sell graded cards with clear scores, price references, and liquidity, they often provide buyback/resale guarantees: if users are not satisfied with the cards they draw, they can sell them back to the platform at a pre-set price, and the platform can repackage that card into a new blind box for the next user to continue the lottery, creating a cycle. Thus, once opened, it becomes an endless loop, and one cannot stop.

3. Opportunities Under Cultural Differences and Regulatory Gaps

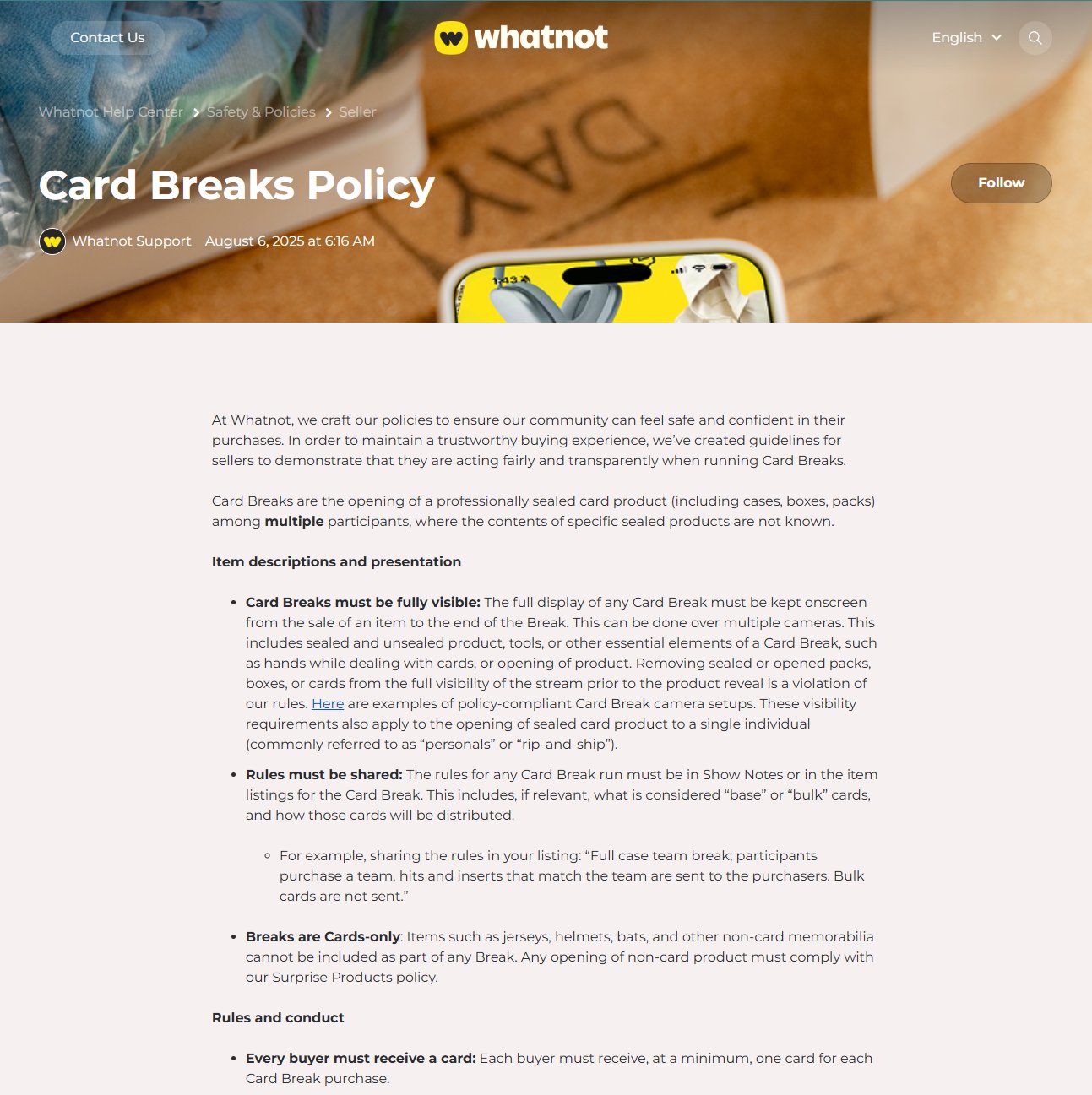

However, can web2 internet not do card blind boxes? Of course, it can, but with significant limitations, especially in Europe and America. In the live e-commerce platform @Whatnot, although there are hosts doing card breaks, there are very strict guidelines that explicitly prohibit any gambling-related "repackaging" probability games.

As for large platforms like eBay, they emphasize transparency and compliance, prohibiting the sale of "mystery blind boxes" or "guaranteed packs," only allowing standardized transactions. In other words, in the European and American markets, any gameplay involving probability + monetary exchange will quickly touch the regulatory red line for gambling.

In contrast, the situation in East Asia is completely different:

- Japan has a completely different scenario. The culture of lucky bags and capsule toys has deeply ingrained itself in people's minds, becoming part of the entertainment industry, and there are local online blind box card platforms like Clove, where the card drawing gameplay is almost part of the user mindset.

- China has had card games in the past, followed by Pop Mart, and platforms like Xianyu dominate the second-hand circulation market. Such gameplay is often categorized as consumer goods rather than financial products. Searching "card unpacking" on Douyin will yield a plethora of live streaming rooms dedicated to card unpacking, running 24/7. Some even offer "betting packs" (like guaranteeing a premium card after unpacking several packs), and some hosts provide resale options. Under the continuous embellishment and atmosphere created by attractive hosts, there are many who spend lavishly just to get a rare card.

4. Hypergamblification Has Become a Trend

What TCG RWA is doing is essentially helping the traditional card market with distribution and traffic through financialization.

After users draw cards, if they do not resell them back to the blind box platform, they will likely return to Web2 platforms like eBay or TCGplayer to cash out. However, their momentum confirms a trend: hypergamblification. That is, everything can be wrapped in the shell of "entertainment and financialization," packaged as a new product.

Gambling is no longer an accessory but has become the core. This provides a new narrative for the monetization of IP: it is not just about "physicalization," but rather the overlap of "finance-entertainment." It is not just about "consumer goods," but rather "financial experience goods."

If in the past we tended to think that NFTization and going on-chain were ultimately for DeFi, such as being used as collateral for loans, which was the "destination of use cases," then now and in the future, we can fully consider that adding "financialized gaming experience" can itself be the endpoint.

The value of NFTs does not necessarily have to extend to lending or derivatives markets, but can directly form an independent and sustainable consumption scenario through "entertainment + finance," as evidenced by Pop Mart and blind box unpacking. In the context of crypto-native environments, the impact of this trend is enormous:

IP Companies Greatly Enhance the Profitability of Native Crypto IP.

For example, it will greatly inspire the card series @vibes_tcg issued by the penguin ecosystem project @pudgypenguins and set a model for the subsequent commercialization of the acquired NFT series @moonbirds.

NFT Infrastructure A large amount of on-chain and issuance will directly drive demand for upstream NFT protocols and tools.

For example, @metaplex for Solana, which is not only the NFT issuance standard but also a full-stack tool for minting and circulation.

Gamblification Technology Stack

With the rise of gamblification, Gamblification itself needs to establish a set of abstract layer designs covering probability mechanisms, incentive distribution, etc., known as the "hypergamblification engine." @multiplierfun is a representative project focused on this area. Currently, it is only experimenting with fungible tokens, but its mechanisms can be horizontally transferred to NFT, cards, collectibles, etc., becoming a universal gamblification underlying module.

Risk warning

Risk warning Risk warning

Risk warning