Global Payment Fold: What is Web3 Doing Beyond the Mainstream Narrative from Tokyo to Nigeria?

In the cryptocurrency industry, we often shout "disrupt banking," but in reality, the fastest way to start over is actually through compatibility.

In the cryptocurrency industry, we often shout "disrupt banking," but in reality, the fastest way to start over is actually through compatibility.Written by: Web3 Farmer Frank

"Financial equality" is something that can often only be truly understood through personal experience.

Recently, while I was in Japan, as someone who is already accustomed to QR codes being ubiquitous, I felt that there was too much cash, card usage was cumbersome, and activating a Suica card was a bit of a hassle (the pain of using an Android device). However, at least, there is always Alipay and Visa/Mastercard as a safety net, so payment is never difficult to manage.

But when we shift the map slightly south to countries in Africa, Southeast Asia, and Latin America, the situation is completely different. In many of these countries, payment is not just a tool but a "survival skill":

The penetration rate of bank cards is extremely low, with many people not even having an account. The fees for small interbank transfers are high, the arrival times are unstable, and there may not even be cross-border services from commonly used banks. Even if they exist, the costs for cross-border payments are often astonishingly high.

In these places, "payment itself" is no longer a basic infrastructure like water and electricity, but has become a privilege.

1. The World is Folded: From Tokyo to Lagos

Living in East Asia (like China and Japan) or in Europe and America, our perception of payment is often one of "overabundance."

The smoothness of WeChat Pay, the omnipotence of Alipay, and even the one-touch experience of Suica in Japan make us feel that the flow of funds should be this way.

But the world is not flat, and the financial experiences of different people are also folded.

Just like the three physically separated spaces in the sci-fi novel "Beijing Folding," there are insurmountable gaps in global finance. For example, people in the first space are already discussing where to enjoy double-digit DeFi annual returns, while those in the third space are still worrying about how to safely bring their hard-earned money home every day.

Interestingly, it is also in this context that a "counterintuitive" truth in the data is often overlooked—although the overall stereotype of Africa is often "backward," if you shift your gaze to emerging markets like Nigeria, you will find that they are not averse to digital payments; rather, they are trapped by infrastructure:

According to the latest data from the Central Bank of Nigeria (CBN), Internet Transfers account for an astonishing 51.91% of the market share (by transaction count), while POS transactions account for 28.53%. Together, they make up over 80%, while cash withdrawals (ATM), which we think should occupy the highest proportion, only account for 2.21%.

This means that Nigerians actually rely heavily on digital payments, especially direct bank transfers. In simple terms, this is also because physical payment infrastructures like bank branches are, in fact, more costly and harder to realize compared to seemingly advanced options like electronic banking.

Therefore, in places like Nigeria, you do not need to consider teaching someone what an "e-wallet" is or how to use it, because under the pressure of real-world factors, they have already become accustomed to using their phones to complete almost all transfers, which is similar to how Axie Infinity became popular in Southeast Asia.

The only pain point lies in "connectivity." After all, for a freelancer in Lagos, Nigeria, or a worker abroad who needs to remit money back home, an average waiting time of 15 minutes or even longer, along with exploitative exchange rates, remains a huge black box.

They rely heavily on digital payments, but they lack stable, low-cost, globally connected payment infrastructures. It is against this backdrop that Web3 has truly shown people a new path that does not depend on the banking system for the first time.

2. Web3 Payments Should "Surround the City from the Countryside"

This is also why I have always felt that the revolutionary significance and immense potential of Web3 and stablecoins in marginal regions like Africa and Latin America, through a "rural surrounds urban" approach, have been largely overlooked by mainstream narratives for a long time.

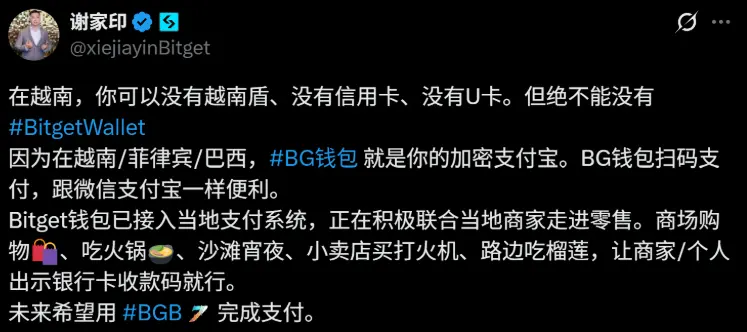

Recently, a video of Xie Jiayin using stablecoins for payment in Vietnam sparked quite a discussion. To be honest, it was quite impactful for me at the time.

The key point is that the payment was completed directly through a cryptocurrency wallet transfer, without needing to go through a U card as an intermediary.

Although completing transfers via QR codes is commonplace in China, it is built on highly mature and closed electronic payment channels like Alipay and WeChat—that is a unique national condition of China and the accumulation of twenty years of internet development, which is hard to replicate.

The model shown in the video is completely different: in Vietnam, using Bitget Wallet to scan the VietQR QR code, the front-end experience is very similar to Alipay, but behind it, cryptocurrency transfers are completed through the Solana network, and then instantly converted into fiat currency to enter the merchant's account via an intermediary protocol.

In simple terms, the difference lies in "replicability"—this model in Vietnam can theoretically be replicated in any country with a local instant payment network.

Especially in underdeveloped regions like Africa and Latin America, where smartphones and e-wallets have a certain level of penetration, but traditional financial infrastructures are lacking.

This also reveals a core demand: users do not care about what ERC-20 is or what Gas Fees are; they only care about "whether they can pay like scanning a code."

If we look back at the evolution of stablecoins in the dimension of Web3 payments, we have roughly gone through three stages:

- Pure On-chain Transfers: A geek's toy, almost impossible to use in real life except for buying NFTs and DeFi;

- The "U Card" Era: Using card issuers to load cryptocurrency onto Visa/Mastercard, which is convenient but has a high threshold (complicated KYC, expensive card fees, high transaction fees), and essentially still works for traditional card organizations;

- Direct-to-Bank: Attempting to connect on-chain accounts, stablecoin assets, and merchant payment endpoints, bypassing card issuers and card organizations in traditional payment chains, which is currently the most exciting exploration;

In this direction, payment giants have already begun to vote.

From Circle launching programmable wallets and CCTP (cross-chain USDC settlement) to global payment giant Stripe investing $1.1 billion last year to acquire stablecoin API service provider Bridge, all are efforts towards the third stage.

Including the recent launch of the bank transfer function on Bitget Wallet in Nigeria, which is supported by Aeon Pay's underlying technology, creating a "third choice" beyond large banks and P2P:

- Decentralized and No KYC: Unlike traditional exchanges that require cumbersome identity verification, it retains the anti-censorship properties of Web3 wallets;

- Fast Experience: Compared to the 10-15 minutes of P2P markets, this direct transfer can be completed in 5-10 seconds;

- Low-risk Channel: Funds no longer pass through unfamiliar individual merchants (P2P Merchants) but enter the banking system directly through compliant payment gateways, greatly reducing the risk of card freezing;

This also means that Web3 wallets are no longer just asset browsers but are beginning to directly connect to the central bank payment systems of various countries (such as Nigeria's NIBSS Instant Payment) through APIs.

From this perspective, the U card, which previously and still occupies mainstream visibility, is destined to be replaced in the future—traditional financial institutions will more actively embed Web3 payment paths and use cases, ensuring compliance while directly completing the full-link connection of user wallets, merchant collections, and asset inflows and outflows through bank accounts, payment channels, and clearing systems.

3. The Ultimate Form of PayFi: When Wallets Become "Invisible Banks"

This also leads to an extremely practical landing issue: Web3 at this stage does not need to reinvent a physical payment network but rather to let wallets "penetrate" the existing payment networks.

I have always believed that the ultimate form of PayFi may be a purely on-chain payment network that completely breaks away from Visa/Mastercard and even no longer relies on SWIFT:

- Merchant side: Directly accept stablecoin payments without mandatory conversion to fiat;

- User side: Directly initiate transactions from non-custodial wallets, with self-custody of funds, and instant on-chain settlement;

- Backend: Supported by compliant stablecoin issuers and on-chain clearing and settlement networks, without the need for Visa/Mastercard or SWIFT channels, completely eliminating the "toll fees" of traditional card organizations;

But this is an ideal state. Before the payment system undergoes a complete transformation, the most stable, realistic, and sustainable path remains to directly connect local bank networks through stablecoin payment gateways.

After all, TradFi excels in compliance regulation, account architecture, and risk control systems, while Crypto has natural advantages in asset openness, global liquidity, and trustless execution. The combination of the two is the optimal solution for "compliance" and "flexibility" at present.

In fact, this trend is already happening.

As mentioned earlier, the practice of Bitget Wallet in Nigeria, if stripped of the "Crypto" technical shell, is essentially disguising itself as an "offshore banking app with global liquidity":

Imagine, for an ordinary user in Lagos, when he opens Bitget Wallet, he receives not just an on-chain asset management tool but a super Alipay that can store dollars (stablecoins) and can instantly transfer money to the neighboring grocery store owner (local bank account).

This is perhaps the embryonic form of PayFi's killer application scenario in emerging markets.

Objectively speaking, when Web3 wallets can seamlessly connect to real-time payment systems in various countries (such as Nigeria's NIBSS, Brazil's PIX, India's UPI) through compliant channels, this system is likely to truly bypass the high costs and low efficiency bottlenecks of the traditional SWIFT system.

In the near future, products like Bitget Wallet may even surpass existing cross-border payment solutions like Airwallex and Wise in terms of cost and experience.

In Conclusion

Payment is the starting point for stablecoins, and "global payment" is their larger future towards global financial infrastructure.

The QR payment access in Vietnam and the bank transfer landing in Nigeria actually show that the greater role of stablecoins may not be to replace banks but to fill in the gaps that the banking system cannot address.

I also hope that in the future, there will be more wallets and more Web3 projects willing to continue experimenting and delving into these complex local scenarios.

Only in this way can "global payment" become not just a narrative but a tangible reality.

Risk warning Risk warning

Risk warning Risk warning