The "swiping" era of L2: When the expansion story is over, payment has become a lifeline

Surviving is more important than gazing at the stars.

Surviving is more important than gazing at the stars.Original Author: Eric, Foresight News

Recently, Solana made a joke about Starknet, mocking an L2 with only 8 daily active users and 10 transactions per day, yet having a FDV of $15 billion.

In hindsight, this salt-in-the-wound joke was intended to attract attention, leading to the announcement that the Starknet token STRK would be launched on Solana via NEAR Intents. However, Solana's criticism was not unfounded; the numerous L2s that have emerged in the past two years are indeed facing a traffic crisis.

The most compelling recent example is the Zero Network, an L2 network incubated by Web3 wallet company Zerion, which was reported to have stopped block production for over three weeks as of January 8, yet seemingly without any impact. The official response was even more subtle: Zero Network stopped producing blocks on December 19, 2025, but the official announcement to address the issue was made only on December 23, and the last original content posted on Zero Network's official Twitter was back in May of the same year.

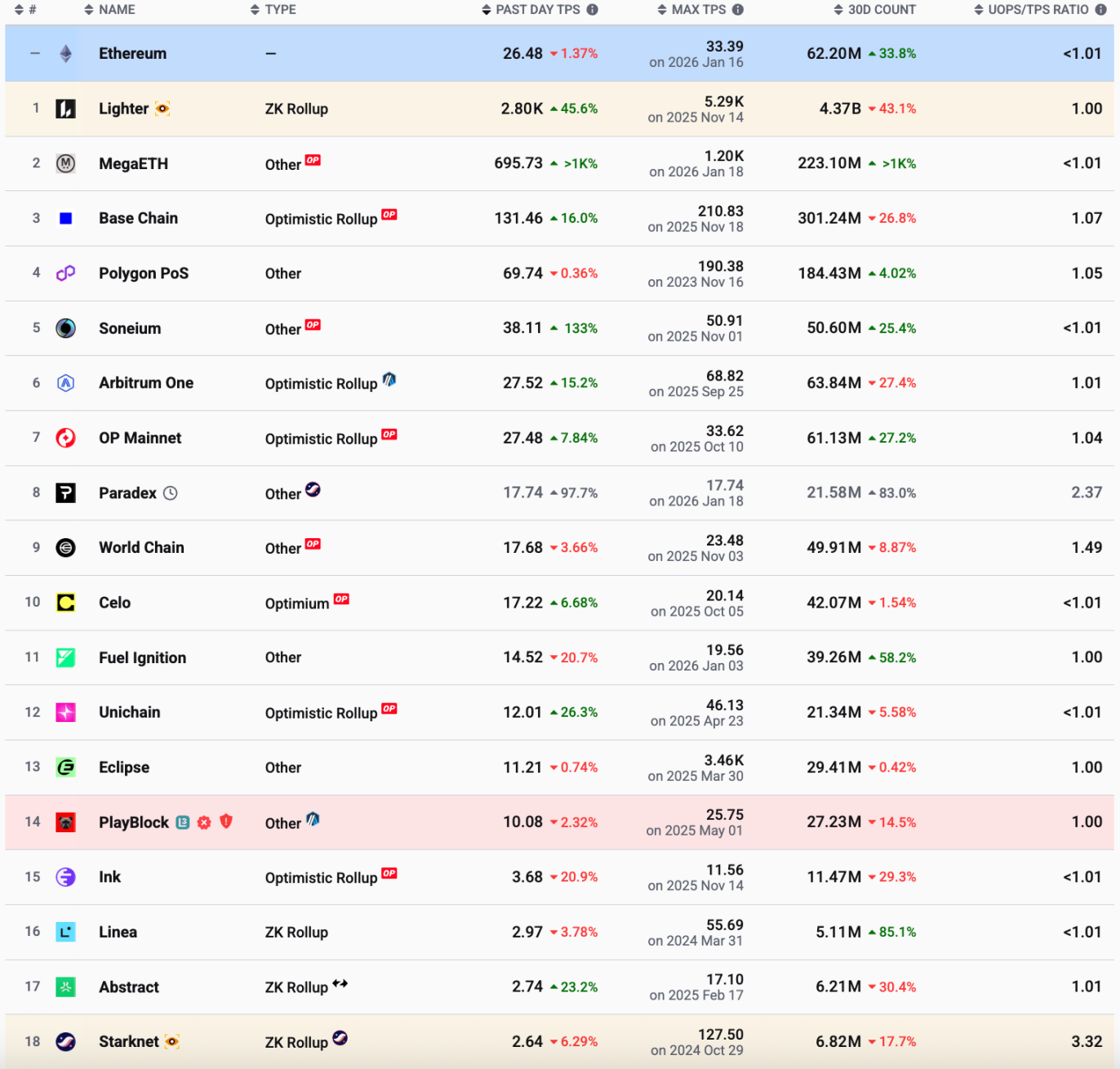

That said, the claim of only 8 users executing 10 transactions in a day is actually an exaggeration. According to data from L2BEAT, Starknet's TPS yesterday was 2.64, meaning there were over 200,000 transactions on the network in a day. However, this number is still absurdly low; even the Ethereum mainnet's daily transaction volume is ten times that of Starknet.

Data shows that among general L2s, besides Base and Polygon, even Arbitrum and OP Mainnet's TPS have not significantly exceeded that of Ethereum. Linea and Starknet's TPS is below 3, and the parts not captured in the screenshots include Scroll with a TPS slightly over 1, as well as ZKsync, Blast, and others with less than 1.

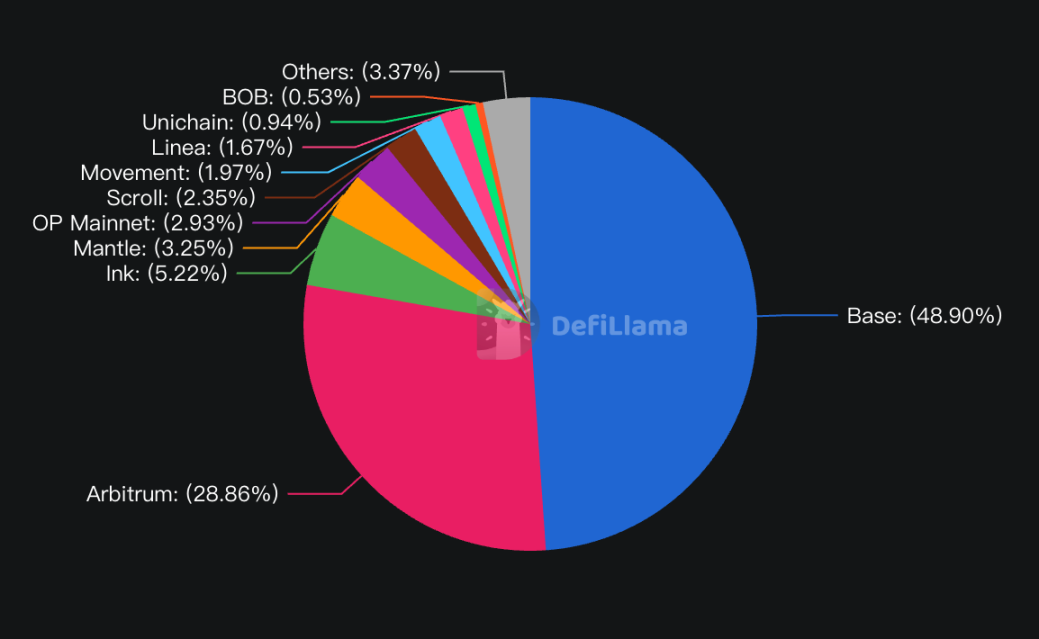

From the TVL data compiled by DefiLlama, Base and Arbitrum together account for nearly 80% of all L2 TVL, while the remaining L2s not categorized as Others have a combined valuation during private financing stages conservatively close to $10 billion, yet their total TVL adds up to less than $2 billion.

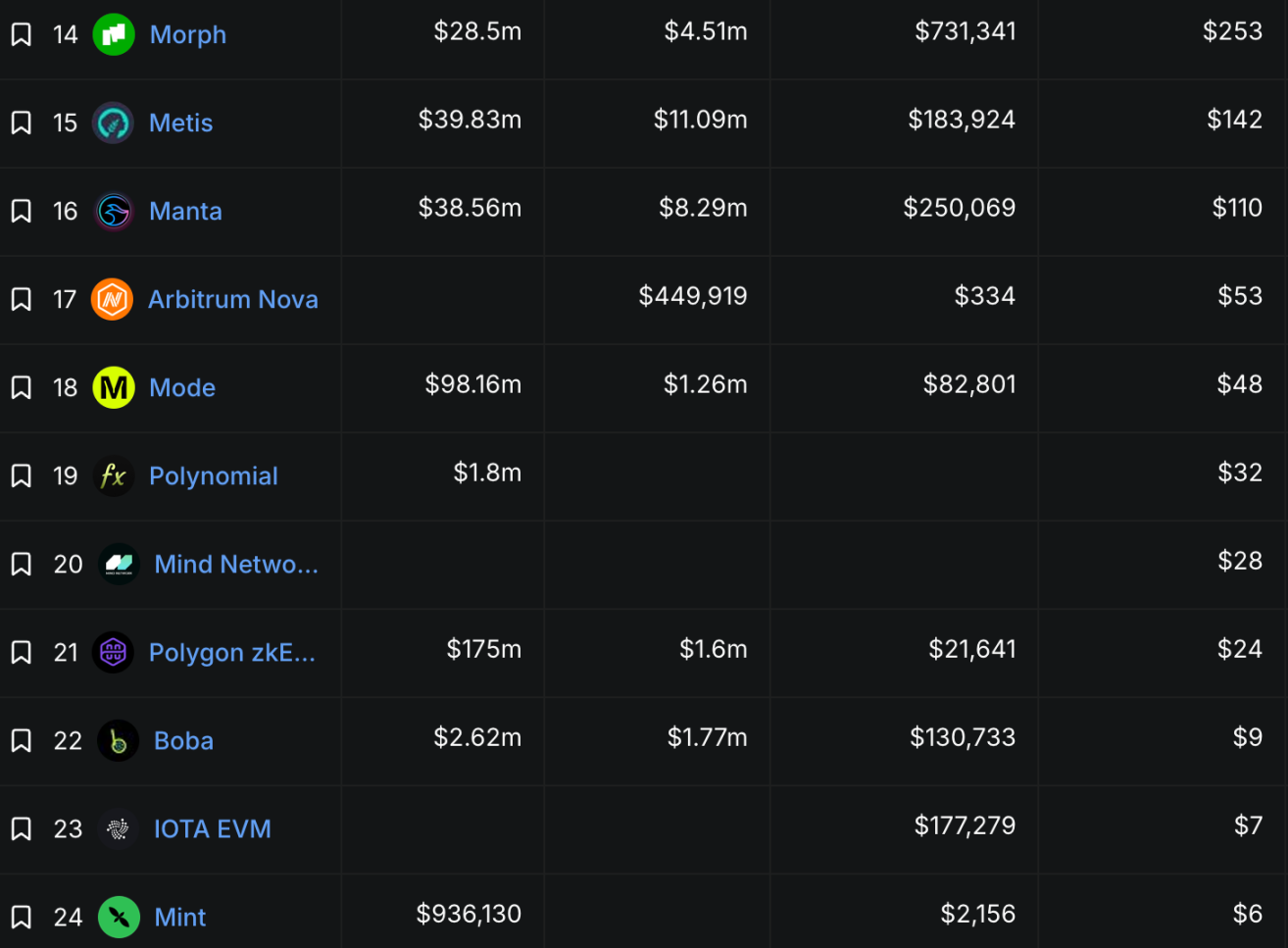

In terms of protocol revenue, only the top 7 protocols have generated over $1,000 in revenue in the past 24 hours, while those with daily revenues in the hundreds or even tens may not even match the interest earned by some large holders from their assets parked in exchanges.

These data vividly illustrate the current predicament of L2s: in a context of scarce application narratives, expecting a killer application that operates willingly on general L2s without being an application chain has become a luxury. In addressing the question of how to find an application scenario that can provide stable transaction data, L2s have found a common answer: cryptocurrency cards.

Pavel Paramonov, founder of the cryptocurrency research organization Hazeflow, has criticized that cryptocurrency cards are essentially not "cryptocurrency payments" but still fiat payments, and do not truly promote cryptocurrency. However, he also mentioned that many projects or public chains launch crypto cards out of necessity, with the sole purpose of keeping users within the ecosystem.

Currently, many cryptocurrency cards launched by exchanges are "custodial" cards, where users' assets are held in exchange or institutional custody accounts, and settlements are conducted by exchanges, off-ramp companies, and card issuers during consumption. The settlement chains for such cards are usually Tron or Solana, or even the slightly more expensive Ethereum; on one hand, the stablecoin asset supply on these chains is sufficiently large, and on the other hand, some cards reduce costs through batch settlements rather than per-transaction settlements. For institutions, liquidity and stability may be more important than the low costs of L2s.

The cryptocurrency cards that L2s are focusing on are various forms of "non-custodial cards," where assets are held in the user's own wallet before using such cards for payment, with each payment settled individually, effectively increasing on-chain activity. Typical examples include Scroll (settlement chain for Etherfi cards), Gnosis, and Linea (settlement chain for MetaMask cards).

In September 2024, Etherfi announced that its payment card would use Scroll as the settlement layer, allowing Scroll to help Etherfi achieve "gasless transactions" and provide a higher cashback rate through the SCR token. In addition to the traditional direct consumption of assets on Scroll, Etherfi cards also feature a special mechanism: users can use interest-bearing assets on Scroll as collateral to borrow fiat for payments, with supported assets including eETH, weETH, wETH, eBTC, and others.

Gnosis, a sidechain that has long lacked presence, has successfully made a comeback with its Gnosis Pay card, primarily operating in Europe. Users can connect non-custodial wallets like MetaMask and Gnosis Safe in the Gnosis Pay App, and during consumption, Gnosis Pay converts the supported assets in the user's wallet (some euro, pound, and dollar stablecoins) into the euro stablecoin EURe issued by Monerium, which is then converted 1:1 into euros for payment.

The cryptocurrency card issued by MetaMask uses ConsenSys's L2 Linea as its primary settlement network, and also supports Solana and Base. Before making a payment, users need to deposit supported assets (various dollar or euro stablecoins) into their MetaMask wallet, and during payment, the user's assets are transferred to the off-ramp service provider, converted into fiat, and then paid to the merchant.

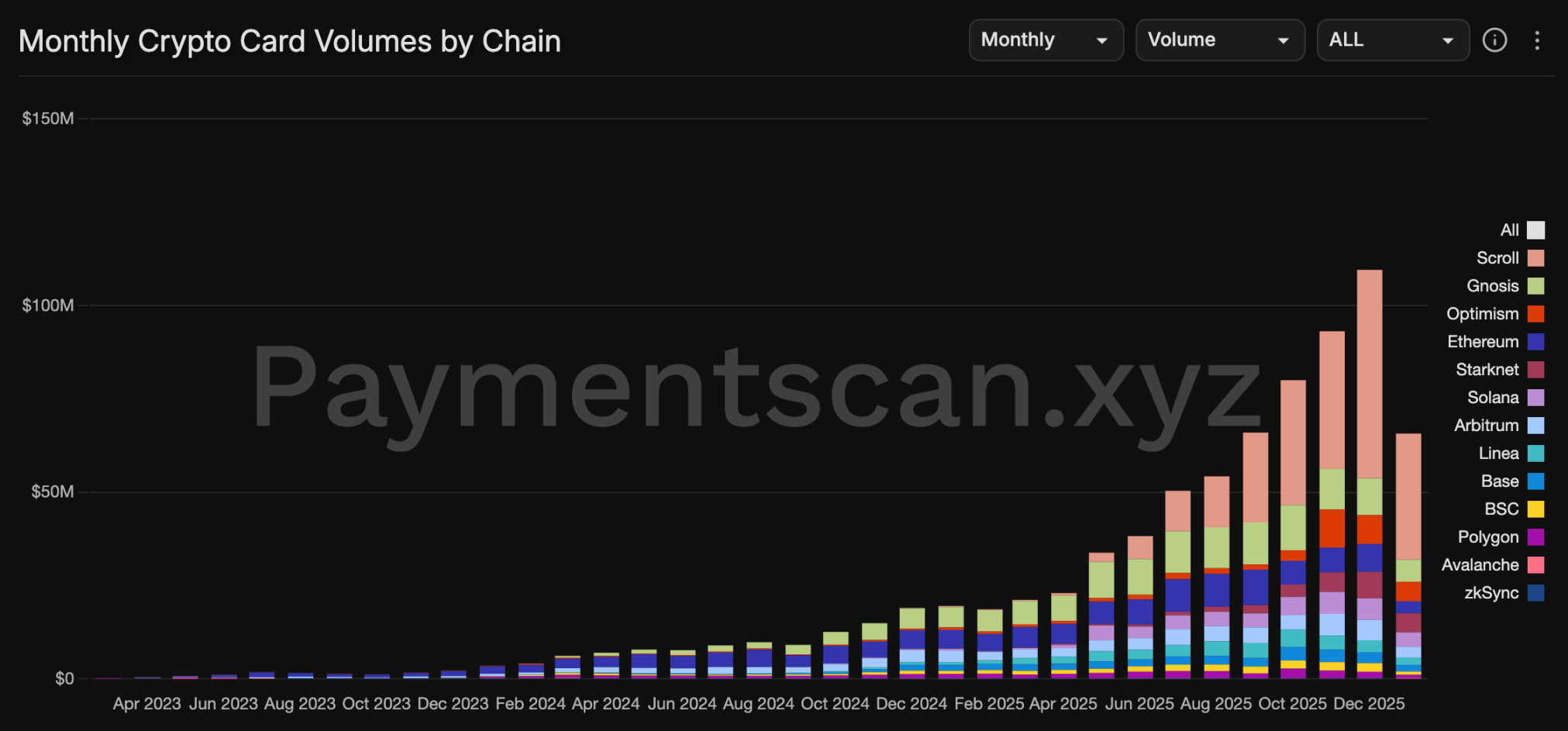

Due to the per-transaction settlement nature of non-custodial cards, each consumer transaction corresponds to an activation contract to verify the remaining asset quantity and the asset transfer on-chain. Thus, L2s can rely on payments, a highly frequent and sustainable scenario, to ensure a certain level of on-chain activity. According to Paymentscan data, Scroll has captured a significant market share in card payments through its collaboration with Etherfi and SCR subsidies. However, this data may not be entirely accurate, as many cards may not have conducted on-chain transfers during payments but settled internally within institutions. Nevertheless, it is an undeniable fact that L2s have found practical application scenarios through payments.

Not only are emerging L2s anxious, but Polygon, which cannot be strictly classified as an L2, has also shifted its strategic focus to payments recently. By the end of 2025, the non-USD stablecoin transfer volume on Polygon exceeded $11.1 billion, with the new stablecoin XSGD reaching a trading volume of $2.24 billion and the Australian dollar stablecoin AUDF reaching $2.46 billion. Additionally, Polygon has become one of the main chains used for stablecoin payments by Stripe; its announcement on January 13 of acquiring cryptocurrency payment infrastructure Coinme and blockchain development platform Sequence for $250 million further emphasizes its "all in on payments" strategy.

After experiencing a barrage of various concepts, L2s have come to terms with reality. While still hoping for novel applications, the urgent task is to survive by leveraging their low-cost and high-efficiency characteristics through payments.

Recommended Reading:

RootData 2025 Web3 Industry Annual Report

The Power Shift of Binance: The Dilemma of a 300 Million User Empire

Risk warning

Risk warning Risk warning

Risk warning