Rented Tracks: What is this wave of stablecoin FX hot money really paying for?

What is truly being repriced in the market is the layer between stablecoin issuers and the real economy - the transaction layer.

What is truly being repriced in the market is the layer between stablecoin issuers and the real economy - the transaction layer.Author: Cao Legong, The Adventures of a Financial Dog

Not long ago, I was chatting with an American investor, and he said something that left a deep impression on me: buying Circle's stock does not equate to gaining exposure to "stablecoins."

Upon reflection, this is indeed the case. CRCL is essentially a business that earns interest on reserves during a rate-cutting cycle, which has little to do with the trading volume of stablecoins, cross-border flows, or merchant networks that are truly being repriced.

What the market is really repricing is the layer between stablecoin issuers and the real economy - the transaction layer. And in this layer, capital has been pouring in quite aggressively over the past sixty days.

Major Moves in the Last Sixty Days

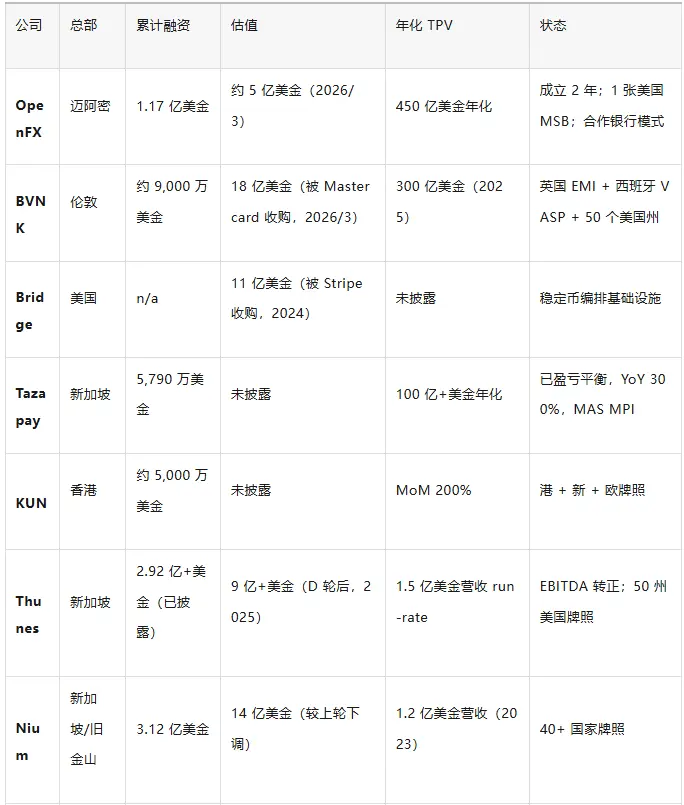

OpenFX secured $94 million in Series A funding, with a valuation of about $500 million.

Tether strategically invested in Axiym, aiming to embed USDT into global payment channels.

Mastercard acquired the stablecoin infrastructure unicorn BVNK for up to $1.8 billion.

Meanwhile, XTransfer, a cross-border payment company for small and medium enterprises, has submitted its prospectus to the Hong Kong Stock Exchange, with a pre-IPO valuation of about $3 billion. I mention XTransfer not because it belongs to this wave of stablecoin stories, but as a comparative anchor: to see how much the secondary market is willing to pay for a truly profitable, audited, and licensed cross-border FX company.

The story is real, the volume is real, and the regulatory tailwind is significant: especially with the U.S. GENIUS Act, which indeed provides institutional funds with a "reason to bet."

But to be honest, a considerable portion of the so-called "stablecoin-native" players in this wave are not doing anything entirely new. Essentially, they are still operating the same cross-border PSP business model from 2018, just replacing the settlement process with stablecoins. Innovation is real; however, the valuation being paid for is another matter - let's call it "the $500 million wrapping paper."

What Kind of Company is OpenFX?

OpenFX tells a very compelling story: using stablecoins as an intermediary settlement layer between fiat currencies, eliminating the need for pre-deposits in nostro accounts, compressing T+2 settlements to under 60 minutes. Within twelve months, its annualized trading volume grew from $4 billion to $45 billion. CEO Prabhakar Reddy is a co-founder of FalconX, and the backing investors are top-tier.

But one thing must be clarified: OpenFX is not a multi-licensed financial institution.

Aside from a U.S. MSB license, it primarily relies on partner banks for operations in other markets - SEPA in Europe, FPS in the UK, and NPP in Australia, all through local partners. Compliance in each market is outsourced to "licensed and regulated institutions." Naming virtual accounts is still on the roadmap.

Reddy himself has been quite candid:

"The time required to obtain licenses globally is three times what you expect. Even those banks that publicly claim to be 'stablecoin-friendly' find it much more complex to establish cooperative relationships than what is stated in press releases. Last-mile liquidity is achieved corridor by corridor."

This statement almost perfectly describes the path Airwallex took from 2015 to 2020: first collaborating with local banks to capture FX spreads from multinational banks, then gradually obtaining licenses market by market. Airwallex took ten years and burned $1.57 billion to build the licensing moat behind its current $8 billion valuation.

OpenFX has only been established for two years. From this perspective, the $94 million Series A round is more of an entry ticket than a medal in this licensing marathon. This is not a criticism, but merely clarifying what investors are actually paying for.

However, there is another, more forgiving interpretation.

OpenFX may simply be following a "first build volume, then fill in licenses" script - and this script has indeed produced some of the most successful infrastructure companies in the crypto industry.

Ondo Finance achieved a 58% market share in tokenized stocks and about $2 billion in TVL for tokenized U.S. Treasuries while under SEC investigation; the investigation will conclude in November 2025, after which Ondo acquired Oasis Pro, bringing in broker-dealer, ATS, and transfer-agent licenses all at once. GSR, a crypto market maker, just secured its first round of external strategic investment from Standard Chartered SC Ventures last month, and after twelve years, achieving $287 million in revenue and $71 million in net profit, finally welcomed a regulated bank into its shareholder list.

The pattern is quite consistent: in markets where the regulatory framework is still being written, players who first build scale often end up defining "what compliance means," rather than rushing to fit themselves into a non-existent template.

Can OpenFX replicate this script in the cross-border payment space? That is an open question. Cross-border payments are much more fragmented than equity tokenization or crypto market making: regulation is divided by country, licenses by channel, and banking relationships by locality. Capital is priced based on the assumption of "what can be made to work."

Western Investors vs. Asian Players

Stablecoins as a settlement layer for cross-border FX is indeed a real innovation. It compresses the pre-deposit, the most hidden and largest cost in cross-border payments. A few hundred basis points of capital efficiency improvement, multiplied by the trillions of dollars in annual cross-border flow, is enough to constitute a significant repricing event.

But aside from that, there is nothing new. Collaborating with local banks, multi-currency virtual accounts, mid-market FX quotes, API-first access methods - these are standard practices that Asian and European cross-border PSPs have been using for years. Many of them are already profitable, and the vast majority are actively adopting stablecoins.

Three things in this table are particularly noteworthy.

First, Asian players demonstrate significantly higher capital efficiency. Tazapay achieved a growth curve similar to OpenFX with about half the funding and is already at breakeven. KUN raised about half of what OpenFX did, yet its month-on-month growth reached 200%. The Asian approach is to secure licenses first and then gradually burn cash; the Western stablecoin approach is to secure large first-round financing and deal with licenses later.

Second, the same stablecoin issuers and large financial institutions are backing both sides, but the prices are completely different. Tether invested in Axiym. Circle Ventures and Ripple invested in Tazapay. Visa and Citi Ventures invested in BVNK. Stripe bought Bridge for $1.1 billion; Mastercard acquired BVNK for $1.8 billion.

The strategic logic is essentially the same, and it's worth pointing out: stablecoin issuers themselves do not have PSP or MSB licenses, do not conduct KYC for end merchants, and cannot single-handedly deploy USDT or USDC across 140 jurisdictions. They must find partners with last-mile compliance capabilities. Therefore, these "investments" are essentially distribution agreements disguised as equity, purchasing access. The core logic of the Axiym deal and the Tazapay deal is no different; the only difference lies in the final amounts paid.

Third, the reference prices given by the public market are quite rational. XTransfer - again, to emphasize, this is not a stablecoin company - submitted its prospectus to the Hong Kong Stock Exchange with a pre-IPO valuation of about $3 billion, backed by $248 million in revenue, $47.7 million in adjusted net profit, over 90% gross margin, 800,000+ SME clients, and an annualized trading volume of over $60 billion. In other words, a profitable, audited, fully licensed cross-border FX company currently has a market valuation of about 12 times revenue, supported by real operational data.

OpenFX is valued at $500 million, with trading volume roughly comparable, but lacks revenue, profit, and a supporting licensing framework. The money the market pays for "stablecoin premium" is real, but the underlying operational differences are also substantial. Western capital is pricing the regulatory options under the GENIUS Act; Asian PSPs are pricing based on realized P&L. In plain terms, the funds on both sides are almost not competing in the same pool.

Footnote on Brazil

On April 30, 2026, the Central Bank of Brazil issued Resolution BCB No. 561. Starting October 1, 2026, all eFX (electronic foreign exchange) service providers are prohibited from using stablecoins or any virtual assets for cross-border payment settlements.

For reference, stablecoins previously accounted for about 90% of Brazil's monthly $6-8 billion in crypto-related cross-border flow. This regulation does not prohibit individuals from holding stablecoins, but it draws a hard line around regulated FX channels, telling fintech companies: either remove the stablecoin segment or place it within a truly compliant channel.

This is the future, not an exception. Several other major jurisdictions are also tightening regulations on stablecoins and cross-border payments. Relying solely on a U.S. MSB license and partner banks to support a global stablecoin payment infrastructure window is gradually closing corridor by corridor.

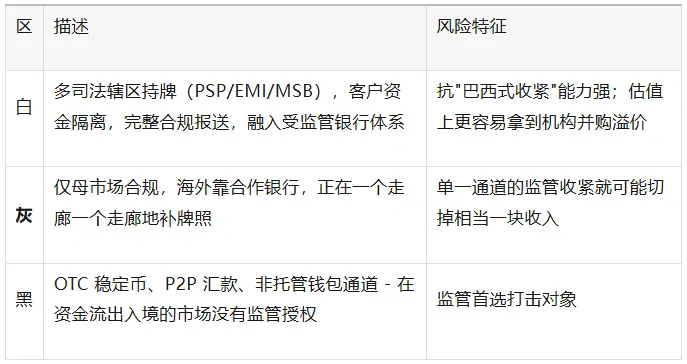

Players in this space can generally be divided into three regulatory categories:

Where the boundaries between these three zones tighten and to what extent will influence the landscape of this space over the next 24 months - and the ways of influence are not entirely clear at this moment.

The current strategic investments by stablecoin issuers - Tether's investment in Axiym, Circle and Ripple's investment in Tazapay, and other similar transactions - share a common point: each recipient has prominently placed "compliance" and "multi-jurisdiction readiness" in their product narratives.

However, whether the compliance posture is truly a moat or whether growth speed and product depth are more critical factors - this question has not yet been settled by the market. Different answers are being bet on at very different prices.

In Conclusion

The infrastructure for cross-border payments is indeed being repriced by stablecoins, making it a track worth taking seriously.

However, the valuations of the current wave of transactions in the West are not pricing the operational business itself, but rather an option - which includes clarity on regulatory direction, execution speed, and which channels will remain open or close.

This option could yield very substantial returns. It could also be repriced after the market gathers more data on "who is truly establishing sustainable businesses."

For those looking to find exposure to stablecoins outside of Circle, a more pressing question than "who is running fast today" might be: what will each player have left in their hands after the next wave of regulation lands in 24 months?

Risk warning

Risk warning