What is the driving force behind the surge in exchanges?

The emergence of various cryptocurrency exchanges is in full swing, and the temptation of huge profits is undoubtedly the fundamental reason. However, the existence and role of the main driving force behind it, namely the exchange system technology service providers, seem to be overlooked by most people.

The emergence of various cryptocurrency exchanges is in full swing, and the temptation of huge profits is undoubtedly the fundamental reason. However, the existence and role of the main driving force behind it, namely the exchange system technology service providers, seem to be overlooked by most people.This article was first published on March 20, 2020, on the Chain Catcher public account, authored by Hu Tao.

As trading platforms for various types of crypto assets, exchange systems involve many aspects such as trade matching, wallet storage, and liquidity. If a trading system with sufficient security and stability is to be developed from scratch, the developers would need to invest at least several million yuan and take 3-5 months. The technical and financial barriers are quite high, which is why the number of exchanges in the early stages of the industry was relatively limited.

However, the emergence of exchange system service providers has changed this situation. By providing a complete set of trading system solutions, they help any third party quickly and cost-effectively establish exchanges, greatly promoting the proliferation of various cryptocurrency exchanges. Currently, over 90% of the tens of thousands of exchanges worldwide are established through exchange system service providers, which have become increasingly important in the industry, representing an undeniable force in the blockchain sector.

At the same time, many changes are occurring within exchange system service providers and the industry, such as a gradual shift from private deployment models to SaaS models, and service providers moving from decentralization to centralization. These changes also reflect many trends and issues within the exchange industry.

1. Deployment Model: From Private to SaaS

The deployment model of exchange system service providers determines the system architecture of exchanges. It has evolved around characteristics such as flexibility, autonomy, and personalization, undergoing three stages of change from early days to the present.

In the early stage of the industry, from the second half of 2017 to the first half of 2018, the main deployment model of exchange system service providers was private deployment. This meant that service providers would deliver the front and back-end system code to clients, who could then further develop and upgrade it locally, particularly to create differentiated features and activities to attract users.

However, at that time, most exchange system service providers were small, informal teams, and the quality of their trading systems varied widely. Systems of average quality could cost only a few hundred thousand yuan, while those with better quality and continuous updates could charge three to five million yuan. For teams that were serious about establishing exchanges in the long term, only the latter, more expensive option could meet their needs, as system security is a lifeline for exchanges.

Although the former systems might attract more clients, exchanges that launched with them often sank without a trace, struggling to gain traction. Clients using the latter systems also found themselves in an awkward position, with only a few exchanges like Cointiger gaining notable recognition.

During that phase, the exchange market was almost entirely dominated by giants like Huobi and OKEx, while newly launched exchanges lacked significant differentiation and advantages in operations, making it difficult to attract large numbers of users. This was a problem that no technical architecture could remedy, and the subsequent operational and maintenance costs were also substantial, leading to a challenging survival situation. Additionally, these exchanges faced obstacles in maintaining and upgrading their systems due to a lack of independent development capabilities, which affected user experience.

It wasn't until June 2018 that exchanges like Huobi and OKEx, in response to the explosive popularity and competition from FCoin, launched various cloud exchange plans, marking the entry of the exchange system service provider industry into its second phase, similar to the white-label model in traditional finance.

In this phase, many exchanges opened their existing system architectures, allowing third-party clients to share their years of accumulated order matching systems, wallet systems, asset management, and clearing systems in the cloud, particularly in terms of depth and liquidity. Clients no longer needed to master development technology or deploy local services to set up exchanges, with representative cases being Huobi Cloud and OKEx Cloud.

The main advantages of these products lie in brand endorsement and reduced costs. On one hand, the endorsement of mainstream exchanges makes it easier for third-party exchanges to gain user trust; on the other hand, the primary purpose of mainstream exchanges launching this business is not to profit from selling systems, but rather to enhance their own platform's liquidity, making prices more affordable compared to those of vertical service providers.

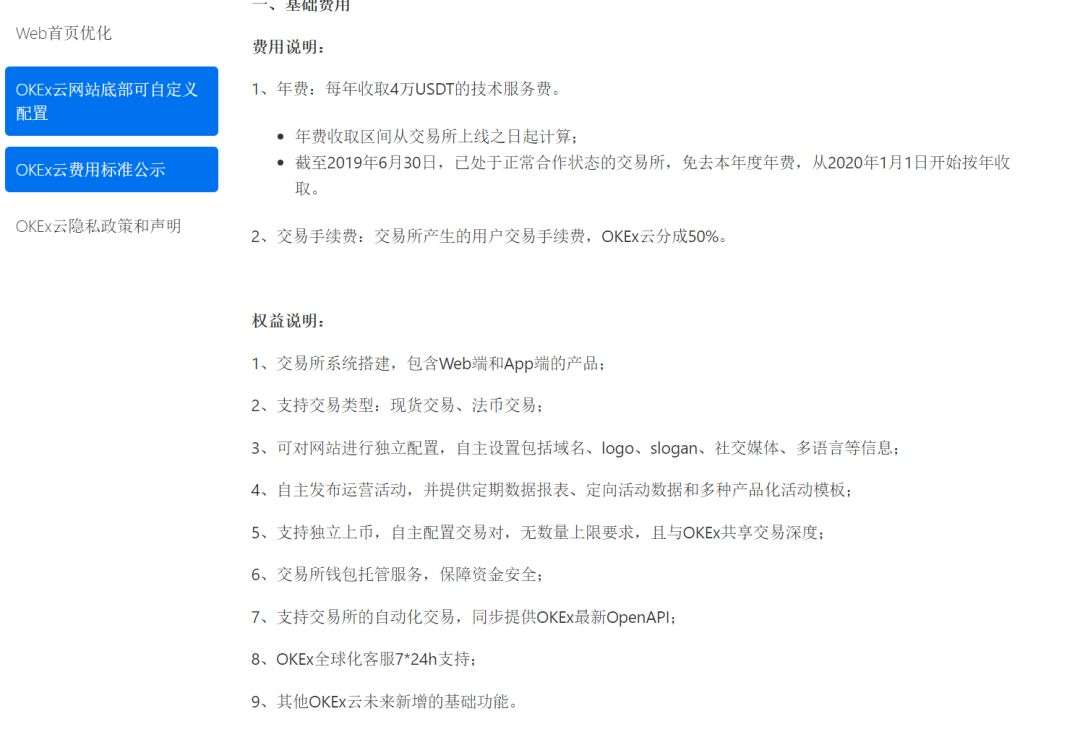

Compared to the previous private deployment model, this model significantly reduces the cost of setting up exchanges for third-party clients. According to Chain Catcher, the early charging situation for Huobi Cloud and OKEx Cloud was roughly 20,000 to 50,000 USDT per year (with OKEx waiving the first year's fee for early clients), along with a 50% share of transaction fee income, and additional fees for launching non-ERC20 tokens or issuing platform tokens.

OKEx Cloud's announcement explaining the cooperation model

This pricing is undoubtedly competitive compared to the private model. When Huobi Cloud and OKEx Cloud were launched, they received thousands of cooperation applications and became extremely popular. According to various statistics from Chain Catcher, approximately 250-350 cloud exchanges emerged from July 2018 to the end of 2019.

However, the drawbacks of cloud exchanges are also very apparent, as third-party exchanges have lower autonomy and controllability. User information and assets are all on the platform, and they cannot conduct secondary deep development to increase system functionality. Additionally, the front-end webpages appear uniform, which places extremely high demands on the operational and traffic-driving capabilities of exchange teams. Some industry insiders even believe that this is akin to third-party exchanges "working for" mainstream exchanges, leading to a difficult existence for most cloud exchanges.

"To be frank, it is impossible for cloud exchanges to grow strong because the current exchanges have competitiveness due to differentiation, but cloud exchanges are all the same model, so how can they grow?" said Adi, a founder of a cloud exchange.

The third phase is the SaaS model, which has rapidly become the main model adopted by new exchanges in China since early 2019. Many exchange system service providers are transitioning to this model, driving a new wave of exchange births.

Compared to previous deployment models, clients using the SaaS model can enjoy a series of cloud exchange software system services provided by service providers while also having an independent user account system and relatively flexible secondary development capabilities. This significantly enhances the operational autonomy of exchange clients and the ownership of user asset information. "One special benefit of the SaaS system is that clients can customize personalized services using the front-end source code and API," said Ju Jianhua, founder of CoinCore Technology.

To some extent, the SaaS model can be seen as a "fusion" of the private and cloud exchange models, balancing the advantages of the first two models, with pricing positioned between them. Therefore, since 2019, most clients intending to purchase exchange systems have chosen this deployment model.

It is worth noting that regardless of the service provider or system model, the pricing of their systems is somewhat flexible. "If some clients have particularly great potential, such as good traffic and abundant resources, strategic support can be provided because the transaction fees they can bring in can generate significant income," Ju Jianhua told Chain Catcher. Additionally, some exchange system service providers may also choose to provide services in the form of equity investment.

2. Service Providers: From Decentralization to Centralization

In the vast market for exchange system services, many well-known service providers have emerged in recent years, such as CoinCore Cloud, ChainUP, Gangsheng Technology, Huobi Cloud, and KuCoin Cloud. They are the main drivers and leaders of the aforementioned changes in deployment models.

The earliest exchange system service providers are hard to trace, but among the current major players, ChainUP, founded in September 2017 by serial entrepreneur Zhong Geng and Huobi co-founder Du Jun, is the earliest. Leveraging Du Jun's reputation and first-mover advantage, it quickly established a leading position in the exchange system service field. In the following months, other service providers like MasterDAX and Alicms entered the market.

However, from an overall market perspective, most exchange service providers at that time were small and decentralized, often operating as workshops, and there were many issues regarding technical reliability and pricing standards. Due to the lack of strong brand and technical capabilities among exchange system service providers, these lesser-known providers still occupied a significant market share.

By mid-2018, competition among exchange service providers reached a peak, with OKEx Cloud and Huobi Cloud both announcing their launch in June 2018. Additionally, exchanges like Binance and BitZ announced similar plans, while system service providers like CoinCore Cloud and Gangsheng Technology began to enter the market. Today, all major players in the exchange system service industry have emerged. Of course, there are also well-known overseas service providers like AlphaPoint, SHIFT MARKET, and B2BROKER rapidly developing, but they are not within the scope of this article.

In this phase, a multi-faceted competitive landscape formed among exchange system service providers, with several providers possessing sufficient strength to conduct in-depth research and market expansion. Specifically, ChainUP, due to its early entry and strong marketing capabilities, has a technical team of over a hundred people, leading in terms of functionality and service systems, having served over 300 exchange system clients, with representative cases including Cointiger and BiKi.

Huobi Cloud and OKEx Cloud benefit from endorsements at the exchange level, with their technical architecture and security having been tested in the market for years, allowing for liquidity and depth sharing. Among them, OKEx Cloud established a unified APP called "OKNodes" for its cloud exchanges, where users can log in and trade on specific cloud exchanges, and assets can be transferred directly through internal transfer channels from the OKEx platform, making it unique among service providers.

CoinCore Cloud, initiated by CoinCore Technology, has its founder Ju Jianhua as the former CTO of Huobi. The entire team has a solid technical foundation and experience, having proposed the exchange SaaS model early in the industry, particularly focusing on personalized customization and decentralized custody concepts. Since 2019, it has acquired nearly 200 exchange system clients.

The team at Gangsheng Technology mainly comes from traditional IT system service giant Hang Seng Electronics, possessing rich experience in financial system construction and promoting the concept of digital asset brokerage business on a large scale, winning numerous clients.

From the second half of 2018 to the first half of 2019, these exchange system service providers fiercely competed for the market. During this process, many service providers significantly changed their development strategies, and the industry's competitive landscape became increasingly clear, with some players' market competitiveness visibly declining.

Chain Catcher discovered that Huobi Cloud held a trading king competition for its partners in December 2018. According to the data, LOCKCOIN, BTC100, and BACCPro ranked in the top three. However, recent checks on the official websites of these exchanges revealed that one has announced the cessation of operations, another has long displayed zero trading volume, and one has abandoned the Huobi Cloud trading system in favor of another service provider. Additionally, Huobi Cloud previously listed many cloud exchange websites that are now inaccessible or have suspended operations, with only a few exchanges like XOXOEX remaining active.

These phenomena indicate that Huobi Cloud's development status seems to lag behind other major service providers. Industry insider He Jiahao (a pseudonym) told Chain Catcher that he believes this is related to Huobi Cloud's early requirement that cloud exchanges must accumulate a pledge of 500,000 HT to gain the right to list tokens. Based on the HT price of 23 yuan, this would require 11.5 million yuan, such a high price not only reduces Huobi Cloud's competitive advantage but also cuts off the main revenue source for cloud exchanges, leading to developmental difficulties.

Chain Catcher learned from public reports that Huobi Cloud has now shifted its development focus to compliance and joint operations, seeking deep cooperation with institutions that have government resources in countries like Thailand and Argentina to jointly operate local exchanges in the form of cloud exchanges.

It is evident that Huobi Cloud has largely become an important tool for Huobi Group to expand its influence overseas, utilizing its years of refined trading system to gain access to overseas market channels, traffic resources, and relationship pathways, while third-party clients have become less of a focus.

At the same time, ChainUP has also shifted its market expansion focus overseas. In the first half of 2019 alone, ChainUP held multiple blockchain events in over 20 countries to promote its systems and services. "Although the costs are relatively high, we can earn it back by selling systems," said Jade Chen, ChainUP's Global Market Director.

At the end of July last year, CoinCore Technology and Gangsheng Technology reached a strategic cooperation to jointly develop the BOMS trading system and bring it to market. This cooperation also indicates that the service provider market has entered a stage of consolidation, where collaboration helps enhance competitiveness, while the market competitiveness of existing players is accelerating in differentiation.

In February of this year, Binance and KuCoin also entered the exchange system service market, attempting to leverage their influence over project parties, communities, and users to promote their trading systems. This also reflects that there is still considerable growth potential in the exchange market. "Since Huobi Cloud and OKEx Cloud launched two years ago, although there have been some successful cases, they are still far from the initial goals, and the products and services do not meet market demands, requiring new blood to come in," said Johnny Lyu, co-founder of KuCoin, to Chain Catcher.

Overall, as more and more "regular troops" enter the field, the "workshop" style service providers that previously occupied a major share of the exchange system market have almost disappeared, with the main market share increasingly concentrated in a few service providers. The current domestic trading service provider market has entered a "two super, many strong" pattern, with ChainUP and CoinCore Technology leading in terms of client numbers and market recognition, followed closely by the cloud systems of exchanges like OKEx and Huobi.

3. Exchanges: From Frenzied Entry to Difficult Survival

The various transformations and developments of service providers are closely related to the situation and demands of the exchange industry, reflecting the craziness and changes within the exchange sector.

As is well known, exchanges serve as the infrastructure of the blockchain industry, possessing clear profit models and important strategic positions, and are the largest intersection of blockchain and wealth. The emergence of exchange service providers has greatly lowered the technical and financial barriers to establishing exchanges, precisely meeting the needs of exchange entrepreneurs for IT systems, triggering wave after wave of exchange fever.

Among them, 2018 was arguably the most explosive year for exchanges, with nearly ten thousand new exchanges launching globally, as various teams attempted to enter this lucrative market. Jade Chen stated that during the industry's peak last year, ChainUP delivered a new exchange system almost every day.

Amidst the exchange frenzy, opportunists frequently appeared. "Once, a client approached me for cooperation and directly said, let's not waste time; I'll give you 100,000 yuan. After signing the contract, you don't need to spend another week on deployment; you don't even need to do anything. I asked why, and they said that with this contract, I can get money from investors," said Zhang Zhen (a pseudonym), a former executive at an exchange system service provider, to Chain Catcher.

This case reveals one aspect of the craziness in the exchange industry. However, returning to the exchanges themselves, is it really as easy to make money as most people think? What is the true survival status of these newly launched exchanges?

According to industry norms, transaction fees and listing fees are the largest sources of income for exchanges, determining their survival status. "If an exchange can achieve an average daily trading volume of 500 bitcoins, it might be able to survive quite comfortably." Li Zhen calculated for us, assuming an exchange has 1,000 daily active users, with each person trading an average of 0.5 bitcoins per day, resulting in a total daily trading volume of 500 bitcoins. The exchange charges a fee on both sides, calculated at 0.1% or 0.05%, yielding a pure income of half to one bitcoin per day.

Chain Catcher also contacted a well-known service provider's exchange client, which belongs to the category of exchanges that are doing relatively well. The founder of this exchange, Adi, told Chain Catcher that he was once a bitcoin miner and decided to enter the exchange industry in 2018 as the market worsened. Now, he has over 20 operational staff. "At the beginning of the year, our daily transaction fees were over ten thousand yuan, with a listing fee of 3 bitcoins. During good market conditions, we would list about two projects a week, and issuing platform tokens for market cap management would also generate income."

More specifically, listing various altcoins is almost the core source of income for these small exchanges, as it is one of the few areas where differentiation can be formed. Only if the listed projects have a sufficiently large community can they bring considerable user volume and trading volume to the exchange.

This is especially true for OKEx Cloud, as the ease of fund transfers and trading processes makes it convenient for investors to use. Many altcoins and "air coins" choose to list on cloud exchanges cooperating with OKEx Cloud, leading to numerous dramatic price fluctuations, such as the well-known "hundred-fold coin" CPYT that launched on OKEx's open platform "Ideal Country" last year.

However, for most exchanges, the aforementioned income situation still appears overly idealistic. With the influx of tens of thousands of exchanges, on one hand, the scale and ecological effects of mainstream exchanges like Huobi have captured a large number of users, while on the other hand, these cloud exchanges have also encroached on the smaller retail market, making it difficult for the vast majority of cloud exchanges to achieve thousands of daily active users.

In this context, the survival of clients using various exchange system service providers is also not optimistic, with few well-known exchanges adopting third-party deployments. However, objectively speaking, this harsh reality is not directly related to the systems provided by service providers like ChainUP; no service provider can avoid such a situation. "The survival status of exchanges is unrelated to the deployment model; it is merely a cost issue. The team's operational capabilities and resource integration capabilities are the real decisive factors." Zhang Zhen believes.

From another perspective, exchange system service providers mainly play the role of technical and operational support in the exchange industry. The saturation of the exchange industry's development and its potential space determine the development prospects of service providers. Although most exchange system service providers express optimism about the future of the exchange industry, in reality, the development space for newly established exchanges will become increasingly narrow, which means that service providers will also face increasingly severe challenges.

In October last year, the state officially launched a blockchain strategy, clearly encouraging technology while maintaining a distance from cryptocurrencies. Subsequently, many exchanges faced accusations from the police and state media, which would also cause many potential entrants to adopt a wait-and-see attitude.

As a result, many exchange system service providers are seeking strategic transformations. ChainUP, for instance, began attempting to transition from an exchange system service provider to a comprehensive blockchain technology service provider last year due to concerns in this area. They have also launched chain reform solutions and risk control solutions to mitigate potential business decline risks.

The previously mentioned overseas expansion strategy is also an important direction. The cryptocurrency trading markets in some financially underdeveloped countries still have considerable growth potential. If exchange system service providers like Huobi Cloud, ChainUP, and CoinCore Technology can achieve breakthroughs in localization overseas, they may welcome a significant incremental market.

"The economic development levels and regulatory policies of countries around the world vary greatly, making it difficult for any exchange to perfectly meet the needs of users in every region. By collaborating with local partners, cloud services for exchanges can help quickly build trading platforms that best meet local user needs and comply with local regulations," Johnny Lyu stated. "If regional compliance can be achieved and operational transparency becomes the norm, it will greatly enhance the survival space for cloud exchanges."

Before major economies around the world announce clear regulatory policies for exchanges, there will always be a potential important window period in the exchange market, which is a key opportunity that most exchange system service providers value. However, this also places higher demands on the strength and resources of exchange system service providers, especially as they face issues such as cultural differences and competition from overseas service providers.

However, with the development of the industry, is there still a need for a continuous influx of numerous new exchanges? Will existing mainstream exchanges dominate most of the market share in the future? It is time for current exchange system service providers to carefully consider these questions.

Risk warning

Risk warning Risk warning

Risk warning