The FCoin model is overdrawn on the future of exchanges

So, why was FCoin able to stand out and ignite the market in a short period of time?

So, why was FCoin able to stand out and ignite the market in a short period of time?Author: Gong Quanyu

Editor: Li Zhao

Recently, Chain Catcher interviewed several senior figures in the exchange ecosystem, uncovering numerous hidden insights and attempting to trace the impact of the FCoin model on the entire exchange industry.

At the same time, we attempt to describe the FCoin trading mining profit model and ecological operation system in this article, and propose many fresh viewpoints, hoping to discuss and exchange ideas with readers.

The trading mining model has been around for more than half a year, and the key to FCoin igniting this model in the industry lies in not setting a hard cap on mining rewards.

Not setting a hard cap on rewards means that FCoin will concentrate long-term development dividends into the short term, leading to trading teams becoming the main group on the platform and deteriorating the platform's ecosystem, effectively overdrawing the future of the exchange.

The key to maintaining the FCoin model lies in whether new funds can continuously flow in.

……

I. The Biggest Dark Horse of This Year So Far

The emergence of FCoin may be the most talked-about topic in the exchange industry in recent months.

On one hand, the price of its platform token FT skyrocketed from around 0.09 yuan at launch to 7 yuan, an increase of more than 70 times; on the other hand, FCoin's official website showed that its total transaction fees on June 17 amounted to 66,014 ETH, with a fee rate of 0.1%, which implies a total trading volume exceeding 200 billion yuan that day, surpassing the total trading volume of all exchanges within 24 hours as recorded by Non-Small Number.

It is difficult to determine how much of this data is generated by platform volume manipulation, but it is a fact that many institutions and individuals have entered the market to engage in volume manipulation. In a Telegram group called "FCoin API Support," hundreds of people discuss quantitative trading strategies daily, and some even sell software for volume manipulation targeting FCoin, claiming that with this software, one can repeatedly generate over 1 million in trading volume in just 10 minutes and achieve a daily return of 20% through FT rewards. The seller revealed that by noon on the 15th, over 80 sets of this software had been sold.

On the evening of June 18, FCoin's official website even temporarily stopped access due to excessive traffic and announced an emergency expansion.

The image shows the daily transaction fees announced by FCoin over the past month, which can be used to infer the total daily trading volume.

The greater impact is on the exchange industry. In mid-June, exchanges such as OCX and BTEX successively announced trading mining plans, and their platform token prices also surged nearly 10 times. Even exchanges that originally planned to launch soon delayed their launches to modify code to catch this wave of hype.

So, why was FCoin able to stand out and ignite the market in such a short time?

Current public opinion mostly believes that FCoin's biggest highlight lies in proposing the trading-as-mining model, significantly returning the benefits originally belonging to the exchange back to users, thereby attracting a large number of users and funds. However, the answer is far from simple.

II. The Trading Mining Model Without a Hard Cap

The trading-as-mining model is not originally created by FCoin; DragonEx launched a trading mining model as early as the end of November last year, followed by exchanges like DigiFinex and CEO imitating it, but none generated a response similar to FCoin. Moreover, the fee-sharing model has long been popular among second- and third-tier exchanges.

If we analyze the mining models of these exchanges in detail, we can easily find a significant difference between the trading-as-mining model proposed by FCoin and those of several previous exchanges.

In the mining models of exchanges like DragonEx, there is a hard cap on the number of platform tokens used for trading mining each day (i.e., a fixed quantity limit), and users receive platform token rewards based on a certain ratio. The more the total trading volume on the platform, the less platform token rewards individuals can receive, and the value of the returned platform tokens may be much less than the actual trading fees.

In contrast, under the trading mining model proposed by FCoin, there is no limit on the number of platform tokens used for mining each day. Users can receive platform token rewards equivalent to the trading fees they pay, regardless of the total trading volume on the platform. Meanwhile, FCoin also launched a referral reward program, where referrers can earn 20% of all fees generated by the referred users within 90 days.

By this calculation, if a user registers two accounts simultaneously, filling in the invitation code of account B when registering account A, and then trades using account A, the trading fees of account A will be 100% returned to account A through FT, while account B can receive 20% of account A's trading fees as FT rewards. The total rewards for both accounts would be 120% of the trading fees, which is 1.2% of the principal, while the cost is 0.1% of each trading principal.

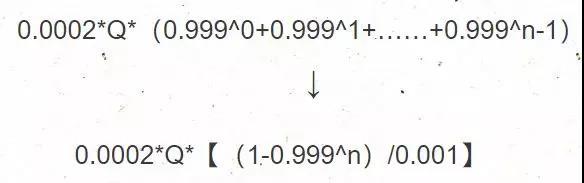

By this calculation, the user can earn a pure profit of 0.02% of the principal with each trade, and the number of trades determines the user's total earnings for the day. Under the condition that the FT price is relatively stable and there are no fluctuations, if a user has tokens worth 100,000 yuan and uses accounts A and B to trade back and forth every 4 minutes for 12 hours, considering that the principal decreases by 0.1% (the fee) after each trade, the total trading volume for that user can be recorded as 8.23 million yuan, with a pure profit of 3,296 yuan, resulting in a daily return rate of 3.29%. The specific calculation formula is as follows.

The image shows the theoretical profit model for volume manipulation, where Q is the principal and n is the number of trades.

If the user attempts to perform a certain number of swing trades during the back-and-forth trading process between the two accounts, the profit situation will be even more considerable.

For users accessing the Fcoink API, their trading capital can be even larger, with trading speeds reaching up to one order per second. With appropriate quantitative trading strategies (ensuring self-buying and selling while preventing order interception), achieving a daily return rate of 10-20% is also very possible. Especially considering the overall weak cryptocurrency market, such a return rate is undoubtedly enticing.

On June 6, after the FCoin referral reward mechanism was first implemented, the mining volume began to surge.

During the volume manipulation process, users face two main types of risks: the first risk is the price volatility of the traded tokens, so volume manipulators tend to choose tokens with relatively stable prices for trading, rather than FT; the second risk is the significant drop in the price of FT mined by the exchange. Since FT rewards are distributed daily, if the price of FT drops significantly the next day compared to the previous day, users' losses may exceed their volume manipulation profits. Therefore, most volume manipulators also prefer to sell FT quickly and reinvest the capital into trading.

In the previously mentioned trading mining model with a hard cap, even if there is a referral reward mechanism, it is very likely that the more one manipulates, the more one loses, as relying solely on platform rewards cannot compensate for the deducted fees, making it impossible to attract volume manipulation institutions.

At the same time, the insane increase in FCoin's trading volume has also driven up the dividend value for FT holders. A senior executive from a top 10 global exchange, Sandy, told Chain Catcher that the comprehensive dividend return rate for FT holders over the past 10 days reached 20%. For retail investors who do not have the energy and ability to engage in volume manipulation, this return rate is also highly attractive. "When many tokens do not have practical value in the short term, users have strong expectations for the appreciation potential of exchange platform tokens, after all, this is a tangible application." said David, the head of a newly established exchange.

Thus, under the stimulation of unlimited FT rewards and generous fee-sharing, a large number of institutions and individuals flocked to FCoin, leading to its explosive popularity, even surpassing the trading volume data of all exchanges.

III. Overdrawing the Future?

The new question this raises is whether this model is overdrawing the future of exchanges. The FT white paper shows that out of a total issuance of 10 billion FT, 5.1 billion FT are used for trading mining. Based on FCoin's average daily issuance of 31.33 million FT from June 12 to 17, this 5.1 billion FT will be fully issued in 162 days, and the remaining 4.9 billion FT will also be unlocked proportionally.

As a platform token, if FT is fully issued and unlocked in less than a year, it would likely set a record in the cryptocurrency space. In fact, whether it is mainstream exchanges like Huobi or earlier adopters of the trading mining model like DragonEx, their platform tokens generally take 4-10 years to unlock completely.

In these 162 days, will FCoin be able to improve its ecosystem and occupy the minds of existing users, becoming their primary trading platform? This may relate to FCoin's future security, coin quality, and operational capabilities, but the biggest problem is that users driven by benefits are also more likely to leave due to benefits. After all, a large number of exchanges similar to FCoin have already emerged, and once the habit of profiting from volume manipulation is formed, it is not easily abandoned.

Perhaps considering this factor, FCoin officially announced on June 17 that the referral rewards (officially named the Mining Income Doubling Plan, details shown in the image below) will be adjusted when the circulating supply of FT reaches 1.5 billion, 3 billion, and 4.5 billion, and whether the referral reward plan will continue after the total circulating supply of FT reaches 6 billion is still uncertain.

The decrease in the referral reward return ratio means that the FT rewards that volume manipulators can obtain will also decrease in stages, with the yield from a single trade being only 0.01% and 0.005% respectively, and it is expected that each adjustment will lead to multiple volume manipulation teams withdrawing, while the time for FT to be fully issued will also be significantly extended.

However, this does not resolve the fundamental issues of the FCoin model.

Sandy told Chain Catcher, FCoin needs a net inflow of funds every day to absorb the miners' sell-offs for this model to work. "In the entire FCoin ecosystem, miners will sell the FT they mined daily to achieve higher returns and prevent the risk of FT price drops, while FT holders are responsible for absorbing the miners' sell-offs daily, allowing miners to cash out their newly mined FT rewards. Therefore, the key to maintaining the entire system is whether new funds can continuously flow in."

In other words, to break through in the short term, FCoin concentrated the long-term development dividends into the short term and released them almost without limits, which led to volume manipulation institutions and individuals becoming the main trading group and primary beneficiaries of FCoin, relying on a large influx of new users and funds to maintain ecological stability. However, funds certainly have limits.

"Once the new funds are less than the miners' sell-offs, the coin price will be unsustainable, leading to a decline in coin price and a decrease in miners' trading volume, which will then cause the dividends for FT holders to decline, further dropping the coin price, and the entire platform ecosystem will enter a negative feedback loop." Sandy added.

Although FCoin has announced that it will gradually adjust the referral reward ratios in the future, changing the previously potentially sharp decline in trading volume to a gradual decline, and allowing investors to have psychological expectations in advance, the decline in the dividends that FT holders can obtain from trading fees remains an inevitable trend with the decrease in trading volume and net outflow of funds, and the FT price will also significantly drop. The biggest victims of these declines will be the FT holders who buy from miners later, i.e., the so-called retail investors.

Although the trading-as-mining model itself has significant innovation and allows users to enjoy more of the platform's growth dividends, once the door to unlimited rewards is opened, the vast majority of platform tokens will be taken by volume manipulation teams, making it difficult for the price of platform tokens to escape manipulation by these teams, and most ordinary investors may find it hard to avoid being harvested.

"There is an eternal trend in the financial field, which is that large capital eats small capital. If small capital makes money temporarily, it should take the profit, otherwise, it is difficult to escape the fate of being eaten." said May, a partner at a Token Fund.

FCoin founder Zhang Jian once stated that FCoin would become a leader in the development of token economies, becoming the greatest innovation after Bitcoin.

But evidently, the existing mechanism of FCoin is difficult to support its long-term stable development, let alone realize the aforementioned vision. After its bubble bursts, it may ultimately just be a second- or third-tier exchange. However, if it adjusts its existing mechanism, it will touch the interests of volume manipulation players, who are the main players on the platform, and it will inevitably provoke their resistance.

Perhaps FCoin's fate was determined when it launched this model. If it wants to change its fate, it may only have to "cut the bone to heal the wound."

IV. Needs Improvement

"Friends who got in early have made money, but now most people have already exited to avoid being caught at the peak; they are already using the money earned from FT to bottom out on other platforms," revealed Candy, a vice president of an exchange.

Currently, there are already more than five exchanges that have clearly launched trading mining models without a hard cap, and some even have web designs that are significantly similar to FCoin. They will continue to siphon off FCoin's users and attract a large number of users who missed the FT opportunity but have strong investment intentions. At this stage, the trading volume of these exchanges still appears weak compared to FCoin, with several orders of magnitude difference. For example, BTEX saw trading volumes of 460 million and 170 million yuan on the 16th and 17th, respectively, after the coin price surged nearly 10 times.

Even so, a daily trading volume of 170 million can still rank within the top 50 among all exchanges, which is not an easy feat for any new exchange, especially for one that has just launched a few days ago.

Therefore, although the previously mentioned trading mining model has obvious problems and limited growth potential, it still serves as a marketing strategy worth referencing. "For small and new exchanges, the trading mining model provides a new cold-start method that can successfully attract a batch of users, institutions, and media, quickly aggregating users and establishing a brand." said Alex, the founder of an exchange infrastructure service provider.

However, how much this strategy can positively impact the platform in the long term remains to be seen. Taking the two trading mining models mentioned earlier as examples, the model without a hard cap is actually not conducive to the long-term stable development of exchanges, while the model with a hard cap can attract some initial traffic, but its effectiveness is limited under the current prevalence of the first model, as users seeking more fee rewards will undoubtedly prefer the former model. Therefore, both models are currently in a somewhat awkward situation.

Taking DragonEx, the first exchange to adopt the trading mining model, as an example, its platform token surged nearly 10 times within a week of its launch last November, but within days it plummeted and has been fluctuating around the opening price ever since.

"How to better distribute and utilize platform tokens, and how to allow users to achieve lower trading costs, these are the reflections FCoin brings us, but simply copying is the least technical and valuable approach." David told Chain Catcher.

Therefore, how to improve the existing trading mining model without affecting the long-term development ecology of the platform, aligning the long-term and short-term interests of the platform, will be something more exchanges need to explore.

In essence, the trading mining model, as a profit-sharing method, is a competitive strategy for exchanges to engage with the existing user base in the market when there is no significant influx of new users, and it does not fundamentally change the way exchanges operate.

After all, the core issues for exchanges remain security, coin quality, and quantity, and all other strategies serve these fundamental issues.

Note: The names David, Candy, Sandy, May, and others in the text are pseudonyms.

Risk warning

Risk warning Risk warning

Risk warning