Why should we pay attention to the Federal Reserve's interest rate hikes?

The news of interest rate hikes sometimes leads to declines and sometimes to increases. Who exactly is deciding the pace of interest rate hikes? What is their attitude towards interest rate increases?

The news of interest rate hikes sometimes leads to declines and sometimes to increases. Who exactly is deciding the pace of interest rate hikes? What is their attitude towards interest rate increases?Original Title: "Confused About the Fed's Rate Hikes While Being in Crypto?"

Original Author: Mabrary

Original Source: OKLink

This article will explore the impact of interest rate hikes and quantitative easing on Bitcoin prices, along with the current policymakers' attitudes towards rate hikes, hoping to provide insights and assistance in interpreting monetary policy.

1. Learning from History: Rate Hikes = Bad News?

Bitcoin is the pioneer of Crypto and also a barometer of the market. We will compare Bitcoin's market capitalization, halving cycles, internal Crypto indicators, and external indicators such as the Federal Reserve's interest rates and QE cycles to discover the patterns of Bitcoin prices in relation to these four sets of data from historical data.

Federal Reserve's real interest rate (orange) vs BTC price (log, blue) vs Bitcoin halving cycles (red) vs Federal Reserve's quantitative easing/tapering

Image Source: OKLink

Note: The green dashed line represents quantitative easing (QE), the red represents tapering (QT). The horizontal dashed line represents the monthly scale of bond purchases/tapering, and the shaded area represents the total scale of bond purchases/tapering during the period.

BTC Halving Dates: 2012.11.28 | 2016.7.9 | 2020.5.12 | 2024.5 (expected)

With Bitcoin's three halvings, the price of Bitcoin has seen increases of 580 times, 128 times, and 18 times during the three bull and bear cycles.

At the end of 2012, Bitcoin completed its first block reward halving, and after a slight correction in April 2013, it reached a peak of $1160 in November of that year, lasting 12 months.

Accompanied by low interest rates and the Federal Reserve's third QE (quantitative easing, 2012.9~2014.10), the BTC price increased 580 times from a low of $2, at which point Bitcoin's market capitalization was small ($13.9b), and trading mainly occurred in China, so the Federal Reserve's monetary policy had little actual impact on Bitcoin prices.

In July 2016, Bitcoin completed its second halving. Before this, BTC prices confirmed two bottoms: 2015.1 ($152)H and 2015.8 ($198). After that, the price rose steadily, reaching a peak of $19600 18 months after the halving (December 2017), an increase of 128 times from the previous low.

During this period, despite the absence of QE from the Federal Reserve and a significant rise in real interest rates, BTC rose against the trend, with a market capitalization of $320.2b, a 22-fold increase from the previous peak. It is worth noting that although rate hikes did not suppress Bitcoin's growth, the tapering that occurred in October 2017 had a clear cooling effect on the bull market.

Data Source: Federal Reserve Official Website

In May 2020, the third halving occurred, and after confirming a low of $3850 in March of the same year, it entered an upward channel. At the same time, the Federal Reserve initiated the fifth round of super QE in March to address the impact of the COVID-19 virus, and two months later, the Federal Reserve's interest rates fell to a near ten-year low. Due to domestic policy restrictions and BTC gradually gaining favor from U.S. capital, a significant feature of this bull market was its "stock market-like" behavior, meaning BTC prices showed a strong correlation with U.S. stocks (especially tech stocks).

The favorable monetary policy brought ample liquidity, combined with the increasing recognition of Crypto in traditional markets, led to the current price peak of $69000 in November (19 months after the halving), an increase of nearly 18 times from the previous bear market low, and a market capitalization increase of 2.94 times from the previous peak.

The growing relationship between Bitcoin and the U.S. has also drawn significant attention from the crypto community towards the Federal Reserve's monetary policy.

2. Who Decides Between Doves and Hawks?

The terms "dove" and "hawk" originally stem from media descriptions of political and diplomatic attitudes, especially regarding war tendencies. Hawks prefer to use strong measures to solve problems, while doves advocate for peace, sometimes taking a more gradual approach. In monetary policy, hawks are more sensitive to inflation and seek to control it through tightening monetary policy (such as rate hikes and tapering), while doves focus more on stimulating employment and maintaining economic growth, entering rate hike cycles later.

U.S. monetary policy is set by the Federal Reserve (Federal Reserve System), and the so-called Fed rate hikes and cuts involve adjusting the federal funds rate, either keeping it unchanged or adjusting it by at least 25 basis points. For example, raising from 2.25%-2.50% by 25 basis points would change it to 2.5%-2.75%. The decision is announced through Federal Open Market Committee (FOMC) meetings.

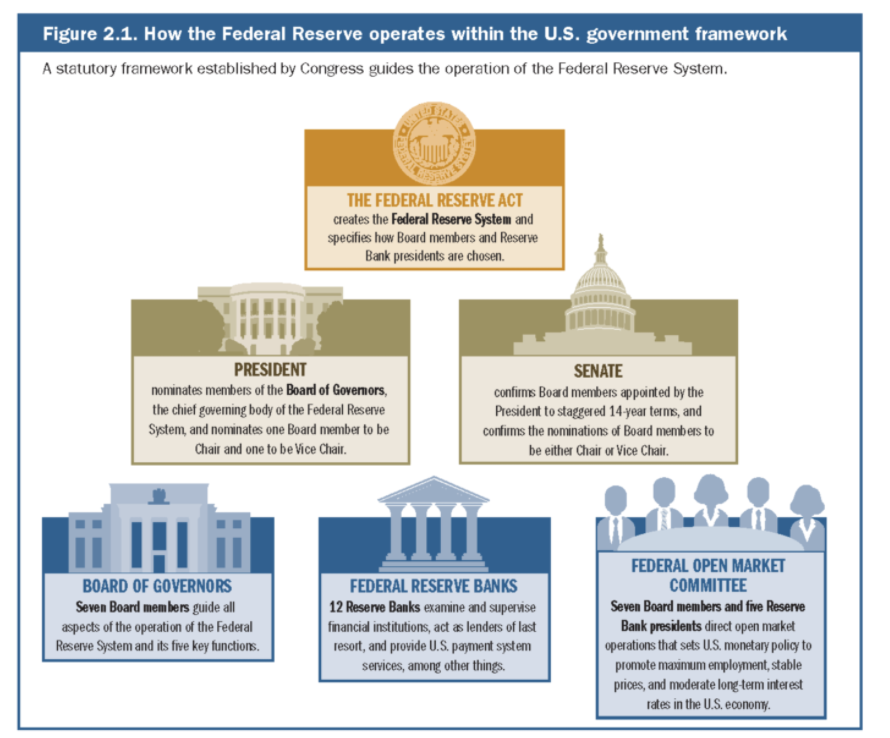

Federal Reserve & U.S. Government Cooperation Framework

Due to the voting system, the decision to raise or lower rates is not solely determined by the Fed Chair but is the result of a vote by a committee of 12 Fed members.

Next, let's briefly understand the composition of the Federal Reserve. The Federal Reserve consists of three key entities: the Board of Governors, Reserve Banks, and the Federal Open Market Committee (FOMC).

The Board of Governors, located in Washington D.C., is the governing body of the Federal Reserve System. The governors are nominated by the U.S. President and confirmed by the Senate. The board is composed of 7 members, but as of now (February 2022), only 4 are in office: Fed Chair Jerome H. Powell, Vice Chair nominee Lael Brainard, Governor Michelle W. Bowman, and Governor Christopher J. Waller.

The remaining three have been nominated by President Biden in January, including Sarah Bloom Raskin (left), who previously served as Deputy Secretary of the Treasury, for regulatory oversight, and two economists, Philip Jefferson (middle) and Lisa Cook (right).

Members of the Federal Reserve Board of Governors

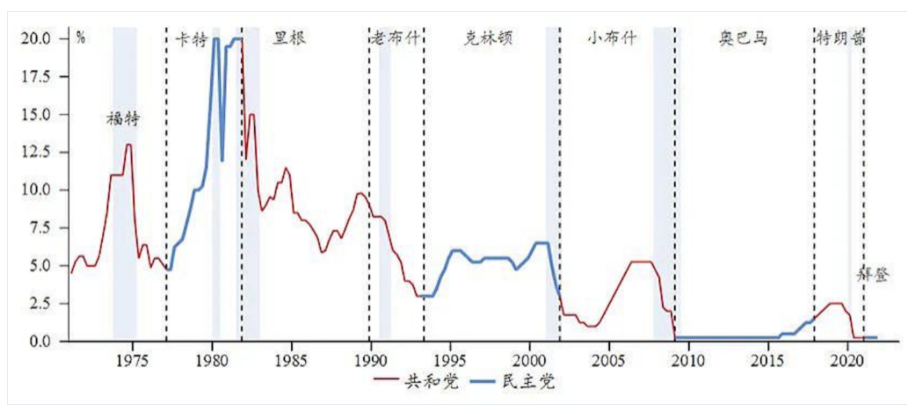

Since 7 out of 12 committee members are nominated by the President, we must consider the historical attitudes of the President and their party towards interest rates. Although the regional Fed presidents are not directly appointed by the President, the President can still indirectly influence the selection of regional Fed chairs through the nominated governors. Historically, the Federal Reserve under Democratic presidents has appeared to be more hawkish, and it is worth noting whether Biden will reshape a more "hawkish" Federal Reserve.

Federal Funds Rate vs President (Party Affiliation)

The primary monetary policy tool of the Federal Reserve is open market operations, which involve buying and selling government bonds and MBS. The FOMC is the decision-making body for U.S. monetary policy, where the 12 committee members vote on which monetary policy tools to use and how to use them.

All 7 members of the Board mentioned above serve on the FOMC, along with New York Fed President John C. Williams, making these 8 the permanent members of the FOMC. The remaining 4 members are rotated among the 11 regional Federal Reserve Bank presidents. Since January 2021, the presidents of the Boston Fed, Cleveland Fed, Kansas City Fed, and St. Louis Fed have served.

Based on the public statements of regional Fed presidents, we summarize their tendencies towards monetary policy. It can be seen that hawks dominate.

It is important to note that since rate hikes have become a foregone conclusion, the focus of the market should now be on how much and when to raise rates.

3. Expected Views

In the previous two halving cycles, although overall, the two major monetary policies of rate hikes and quantitative easing did not play a decisive role, the halving cycles and monetary policies alternately influenced prices. However, as BTC has become mainstream, the performance of this risk asset has gradually become correlated with the Federal Reserve's stance, impacting market expectations in the short term.

In the recent Bitcoin market, we can observe a short-term pattern where BTC prices experience slight rebounds when the Federal Reserve's hawkish statements align with expectations; however, if they exceed expectations, prices tend to fluctuate.

In addition to this short-term sentiment, the timing of when tapering will begin during this rate hike cycle is also worth noting. Looking back at the process from April 2017 when the Federal Reserve signaled tapering to October when it began, the expectations were sufficiently priced in, and the impact of tapering on asset prices was relatively limited, being more dominated by growth factors.

After tapering began in October 2017, U.S. Treasury yields rose in the first three quarters of 2018, and U.S. stocks also rose. The market's ability to continue rising was due not only to fully priced-in expectations but also to the underlying earnings fundamentals, which were driven by the tax reform passed at the end of 2017, resisting the pressures of monetary tightening and rising rates.

In contrast, during this rate hike cycle, since the federal funds target rate remains the Fed's primary monetary policy tool, the market is generally focused on the pace of rate hikes, which may lead to insufficient digestion of tapering expectations. The minutes from the January FOMC meeting indicated that participating Fed policymakers expected to begin raising rates soon, but did not mention the timing or scale of tapering.

However, most participants believed that if inflation did not decline as expected, it might be appropriate to tighten monetary policy more quickly, with tapering potentially occurring in May. Compared to the 6-month digestion time and favorable policies of 2017, if tapering indeed begins in May as the market expects, it could have a certain impact on the market.

Although the Federal Reserve Committee appears more hawkish, I speculate that the Fed will not abruptly raise rates immediately after the March taper ends to retain more policy flexibility. A moderate rate hike may wait for inflation and employment to respond, allowing for an increase in the pace of rate hikes or even tapering, while maintaining a balance between economic growth and stability and controlling inflation.

However, if unexpected hawkish statements or actions occur, those holding risk assets like Crypto need to be prepared for risk prevention and hedging.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles