Pantera Capital letter to investors: The next big trading era has begun, and the crypto market will decouple from traditional markets and follow an independent trend

"To avoid panic, the central bank should provide loans to solvent companies early and freely (i.e., without restrictions), rather than requiring good collateral and high interest rates."

"To avoid panic, the central bank should provide loans to solvent companies early and freely (i.e., without restrictions), rather than requiring good collateral and high interest rates."Author: Pantera Capital

Compiled by: DeFi Dao

I will not comment on the decisions made by the Federal Reserve during the economic panic two years ago. However, what they are doing today is clearly a mistake. They are still actively inflating bubbles in bonds, stocks, real estate, and other areas, which will require a massive policy reversal to stop it. The ultimate result of this cleansing will be chaos in the normal asset markets. Later, I will argue that the best place to avoid the consequences of this policy failure is in blockchain assets.

Crucially, the Federal Reserve has overlooked the "high interest rates" aspect. Their manipulation of U.S. Treasuries and mortgage bonds—seemingly still driven by some disconnection from reality—has pushed interest rates to historic lows.

There has never been a time in history where the annual inflation rate was 7.5% while the federal funds rate was zero. (And if you exclude "owner's equivalent rent," 7.5% would turn into 8.6%, which is well known to be slow to update.) This policy combination is clearly wrong. There is much debate about whether to raise rates five weeks from now. They should have raised rates five months ago or today. When I started as a bond trader, the Federal Reserve acted in real-time. There was no such drama of "forward guidance."

The real interest rate—interest rates after inflation—is negative 5.52%, the lowest in 50 years. No economically rational investor would buy something that loses so much money every year.

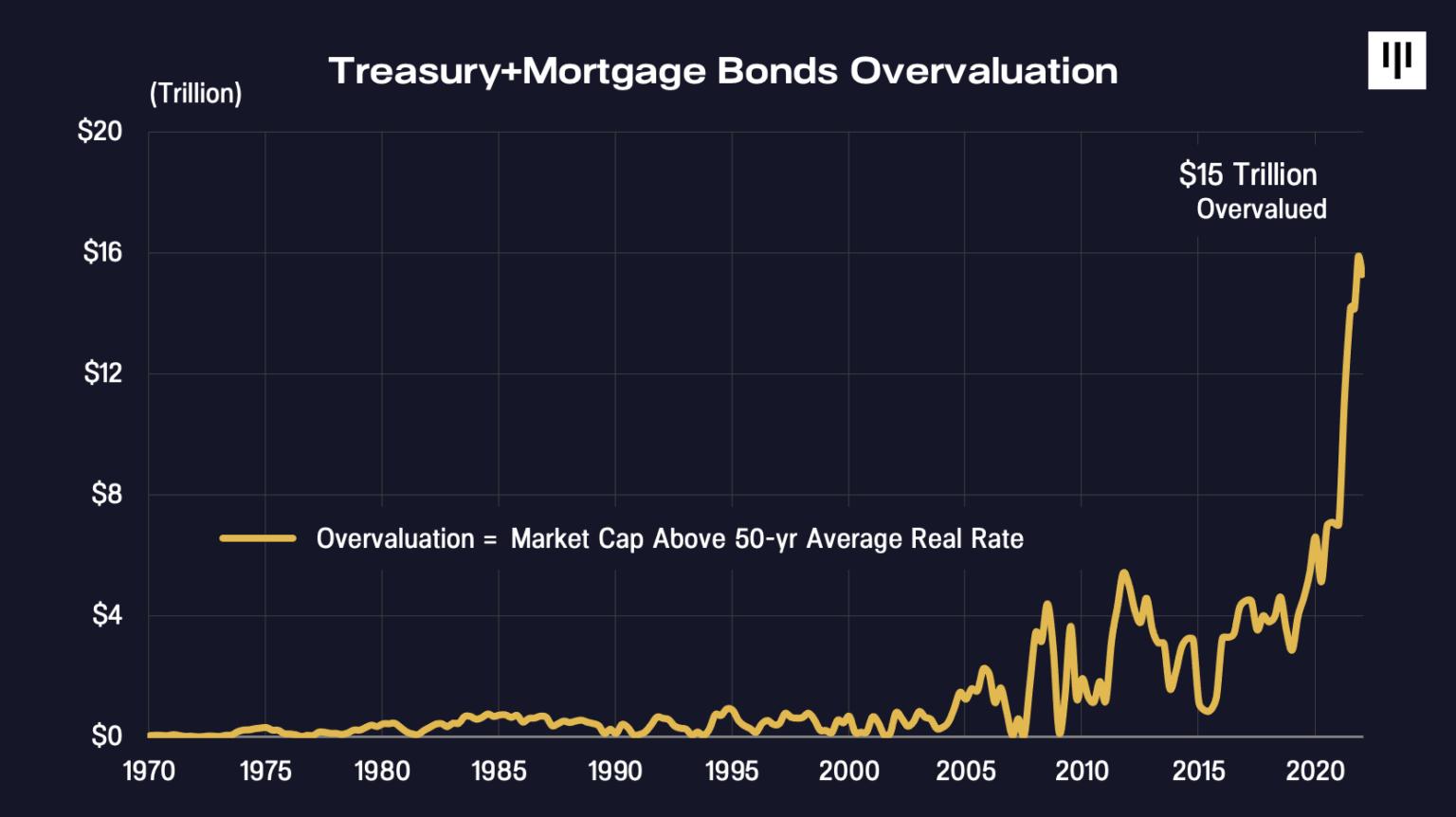

The Federal Reserve's manipulation of the U.S. Treasury and mortgage bond markets is so extreme that it is now overvalued by $15 trillion (relative to the 50-year average real interest rate).

If you own any bonds but have not sold them to the Federal Reserve, you may want to sell them as soon as possible. When the Federal Reserve's bond-buying operations eventually stop, bond prices will experience a Wile E. Coyote moment (referring to a rapid drop).

In the blockchain letter we released to investors on December 7, we predicted the bursting of this bubble. Since then, the 10-year note has dropped by 5 points, and interest rates have risen by 70 basis points. The next great trading era has begun.

Market participants still do not grasp the scale of this trend. The 10-year interest rate will triple—from 1.34% (when we predicted this burst) to around 4-5%.

Impact on Cryptocurrency: Highlights from Recent Conference Call

This is a time in trading that I (the trader) would call a massive trade—a bursting bond bubble, a massive pivot from the Federal Reserve—but missing/not predicting this now obvious side effect—crypto will be stifled.

So, either I am wrong, and this is no big deal for blockchain assets, or the market is wrong.

Some recent thoughts from our February 1 conference call with investors:

Dan Morehead: "The first thing that comes to mind is the market; since we last spoke, the market has clearly changed dramatically. This is a situation in trading where investment managers have correctly predicted some massive disruptions or changes in the market—like we did in November and December, predicting that the U.S. bond bubble would burst and the Federal Reserve would have to raise rates.

And much more than the market expected—but sometimes you take other actions simultaneously when everyone says it is driven by the first step of prediction. In this case, we did not predict that cryptocurrency would experience such a severe downturn.

This puts traders in a position of wondering if they were wrong, if these things are related, or if the market was wrong and whether it will shake out over time.

"In this case, I firmly believe the market is really wrong, and rising interest rates (which I think is obvious, it will happen and will continue to happen) are not that bad for cryptocurrency. Relative to other asset classes, blockchain prices are actually quite good."

Joey Krug: "Our macro view is that cryptocurrency has certainly been hit by a lot of news surrounding the Federal Reserve's plans to raise interest rates. But at this point, we think it has mostly been priced in. As of today, the market is pricing in about five rate hikes—I think many of those have been exaggerated in cryptocurrency.

Ethereum dropped to around $2,200; if you look at the yield on the 10-year Treasury, its peak was around 1.9%, and it has since stabilized. Today, it trends around 1.8%. Now that things have gone through this very aggressive move, the 10-year was 1.35% at the end of last year and then quickly rose to 1.9%, I think this is a wake-up call for the market.

"But if you look specifically at cryptocurrency, when traditional macro markets drop, cryptocurrency tends to correlate with them for about 70 days, or just over two months, and then it starts to break its correlation. So we believe that in the coming weeks, cryptocurrency will essentially decouple from traditional markets and start trading on its own again.

There are several reasons for this. One is that cryptocurrency is still a relatively small market, so a federal funds rate of 1.25% versus something like 0% does not make a huge difference for something that is growing four to five times a year, especially if you look at things like DeFi, which is trading at quite cheap multiples. Many DeFi assets have price-to-earnings ratios ranging from 10 to 40 times. They are not crazy high values; tech stocks have price-to-earnings ratios of 400 to 500 times.

Our view is that it will decouple in the coming weeks, and cryptocurrency will trade independently again. Personally, I think $2,200 ETH might be the bottom."

Dan Morehead: "I completely agree with Joey that the correlation between the S&P 500 and cryptocurrency is temporary. Since Bitcoin began trading in 2010, the correlation during the last six declines of the S&P 500 has spiked within months (71 days). I think this will happen again here, and then they will decouple.

"Once people actually have a little time to think about this, they will realize that if you look at all the different asset classes, blockchain assets are the best relative asset class in a rising interest rate environment. Most asset classes will indeed be directly algebraically impacted by rising interest rates. Bonds, obviously, when interest rates rise, prices fall.

I think bonds will be killed. Most other things like stocks have cash flows that need to be discounted, which means if yields are higher, prices will be lower. Real estate and most other types of assets are the same.

"And blockchain is not a cash flow-oriented thing. It behaves completely differently from interest rate-oriented products. I think when all is said and done, investors will have a choice: they must invest in something, and if interest rates rise, blockchain will be the most attractive."

"We want to quickly review our position in the market. This chart, which we have used many times over the past decade, is very important. It shows Bitcoin as a representative of our industry, in relation to its 11-year logarithmic trend. Now it is trading 60% below trend."

Bitcoin has been below trend for 12.7% of its historical time.

"This does not guarantee that Bitcoin will not drop next week. It does not guarantee that it will not drop further next month or at any time, but it just means that the market is in an extreme state and the likelihood of a relatively quick rebound is very high.

In the nine years we have managed funds in the blockchain space, I have to admit that I sometimes sweat nervously when the market is down—now is not that time. I think the market will come back immediately. I think we need a few weeks or months to rebound very strongly. We are very optimistic about the market, and we think prices are relatively cheap.

"We have some updates from the investor letter. This is a graphic of the bond bubble, with the gold line at the top representing the market value of U.S. Treasuries and mortgage bonds.

"You can see that about a year ago, the Federal Reserve completely pushed it up, which is really crazy. I think the actions of the Federal Reserve are a complete policy mistake, and they are basically about to stop. The Federal Reserve will have to stop what they are doing, and then there will be such a large gap in bonds.

So if you haven't sold your bonds to the Federal Reserve, you should do so. By next month, the last buyer of bonds (and the only buyer) will disappear. This will prompt many people to enter alternative asset classes like cryptocurrency."

I think all the dismissive notions repeatedly expressed by Federal Reserve Chairman Powell and others that "this is just a supply shock" are very wrong. This has nothing to do with the container ships waiting off the port of Long Beach. The supply shock is labor. Three million Americans have left the labor force. There are 11 million job openings and only 4 million unemployed.

There is a severe imbalance in labor supply. Stimulus checks, remote schooling, early retirement. This is why wage inflation is so high right now. It will remain high for a long time.

CPI switched to "owner's equivalent rent" (OER) in 1982—now it is growing year-on-year at 4.1%. The actual inflation people are experiencing is much higher—the annual growth rate reported by S&P/Case-Shiller is 16.8%. OER accounts for 24.2% of CPI. If the YoY OER report is 16.8%, then the YoY CPI is 10.5%, which is 3.0 percentage points higher than the headline 7.5%.

Ultimately, the OER portion of CPI will catch up with reality. This will make it difficult for the reported YoY CPI to drop significantly in the next year or two. The federal funds rate will reach 4-5%.

I think our market will decouple soon. Investors will think: as the Federal Reserve goes from being the only buyer on Earth to a seller, bonds will be crushed. Rising interest rates will reduce the attractiveness of stocks and real estate. So where do you invest when both stocks and bonds are down? (They are usually negatively correlated.) Blockchain is a very legitimate place to invest in that world.

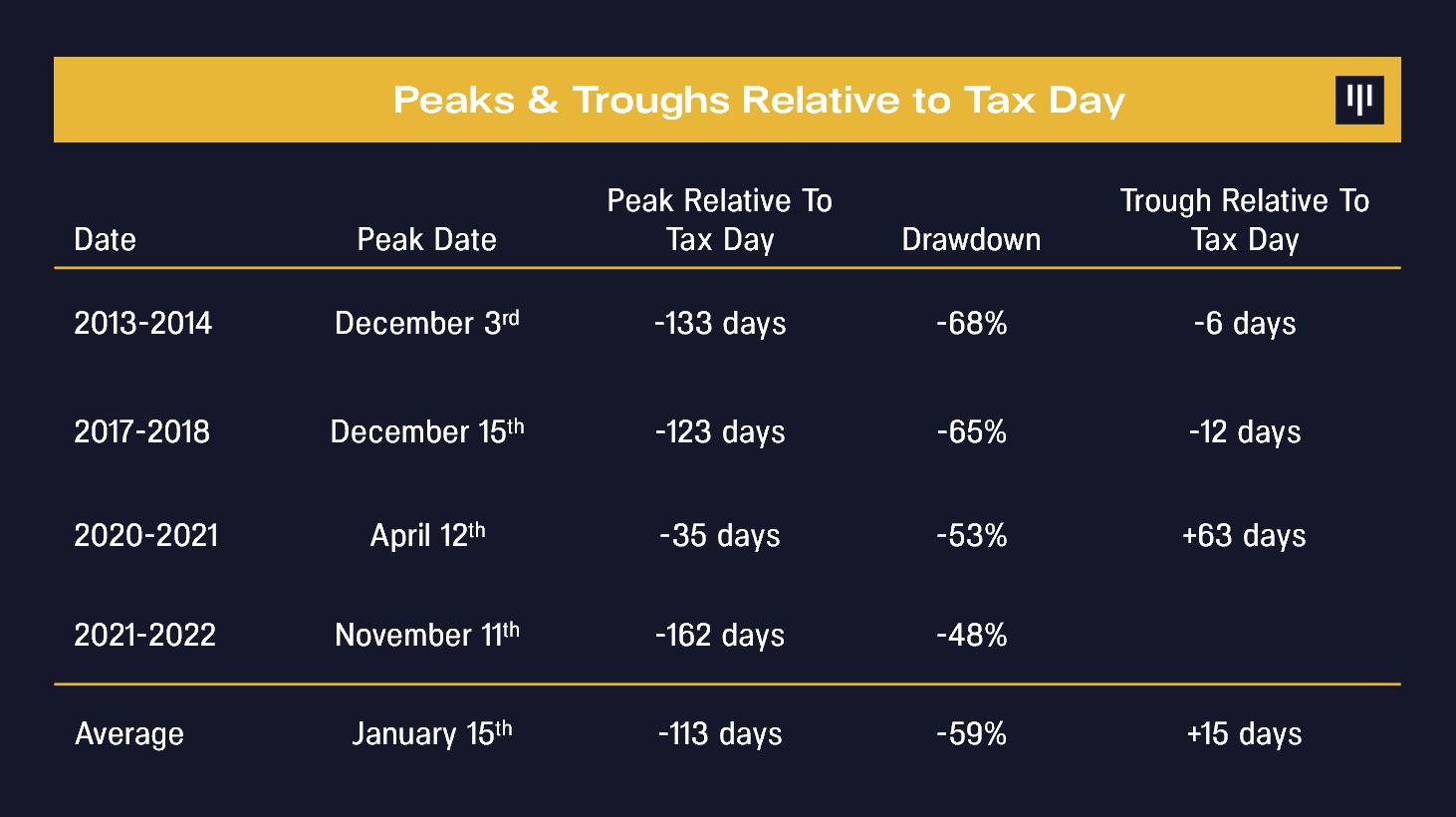

Unexpected Tax Sales Before Tax Day

Some of the selling pressure in cryptocurrency is due to unplanned taxes. Imagine a trader actively buying and selling BTC, ETH, XRP, etc. A great year. Made a lot of money. Put it all on the market.

Spring comes, and their accountant tells them that every profitable sale will generate taxable gains, which must be paid by April 15. Last year, there were $1.4 trillion in capital gains from cryptocurrency. This could lead to a significant portion of recent sales.

Tax Day could be significant for cryptocurrency prices. After experiencing three major upswings in 2013, 2017, and 2020, and this recent surge in 2021, Bitcoin peaked 35 days before tax day, then dropped to a low at that time as investors sold assets to pay taxes accumulated in 2020. In some sense, many cryptocurrency traders are new investors.

You can imagine a person buying as much Bitcoin as possible. After a while, they decide to swap it for Ether. Then their tax preparer tells them they owe 34% on capital gains. Because they are "all in" on cryptocurrency, the only way to raise cash to pay taxes is to sell some cryptocurrency. Prices drop before tax day.

This year's tax day is April 18. (Last year it was May.)

Year-on-Year Comparison

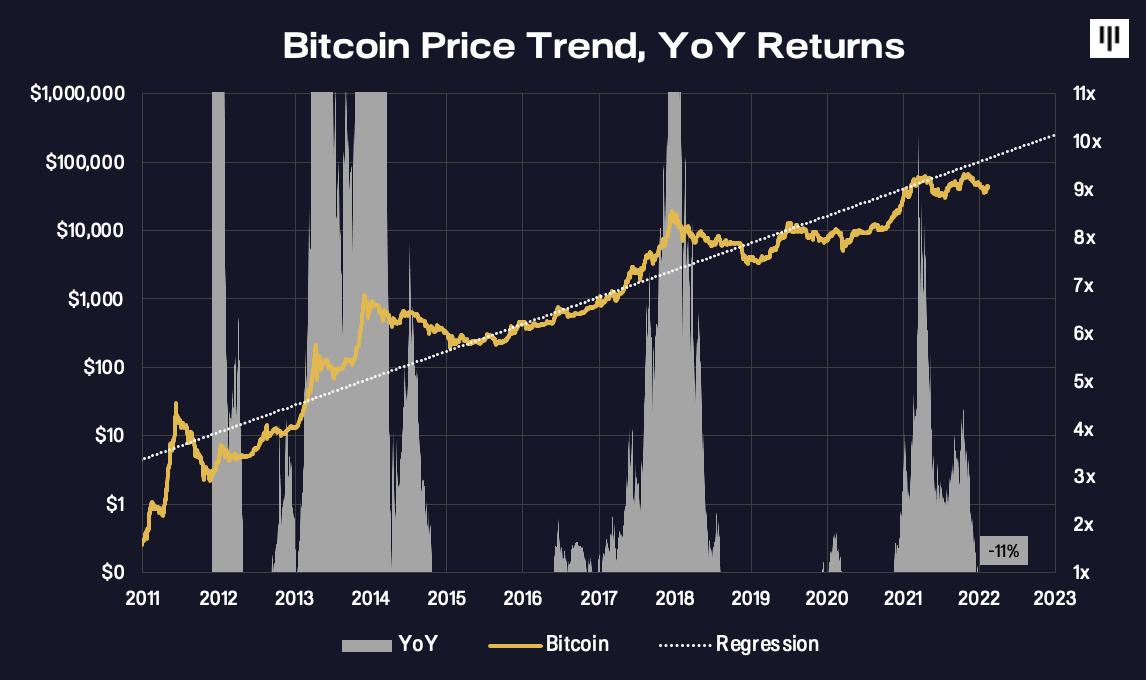

We have updated some Bitcoin charts first shown in the June 2021 letter. They confirm our feeling that the market is not overvalued and is actually very cheap right now.

Year-on-year returns have never deviated from the chart like during past peaks. A year-on-year decline of -11%—during the period when the Federal Reserve printed $5 trillion—seems quite cheap.

The four-year year-on-year return for Bitcoin is at the low end of its historical range. Again, it does not appear to be overvalued.

Joey Krug, Paul Veradittakit, I think we have seen most of the panic.

Human Nature is Cyclical: Resist the Impulse

[This section is a reprint from the June 2021 letter, not updated, for those who did not see it at the time.]

Humans have an innate herd instinct. This is what kept our ancestors alive—when those with wild wolf/reverse tendencies were "Darwin-ed" out.

When the market is soaring—when the FOMO devil whispers in our ears, we want to buy; it is human nature.

When the market crashes—when our spouses/friends/bosses mess up, we want to flee… we want to stop the pain.

We all do this.

I may not win a Nobel Prize in Physiology or Medicine for this, but I can imagine that the traits we left on the Serengeti plains may not be the best choice for trading early protocol tokens.

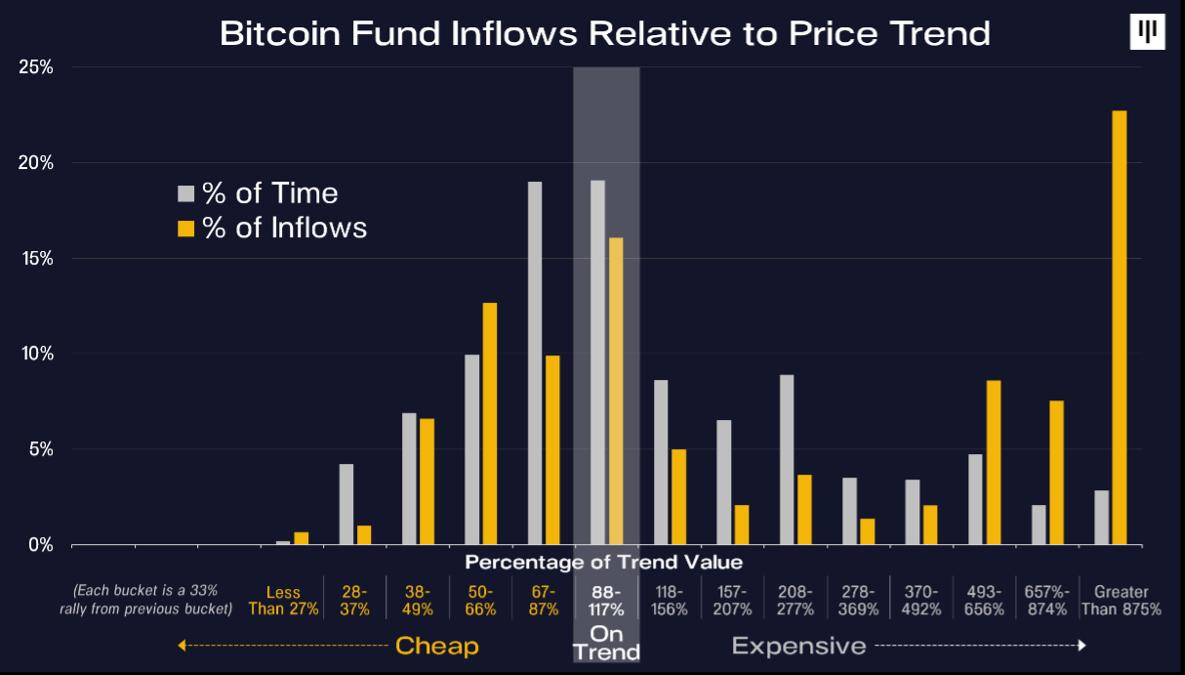

The Pantera Bitcoin Fund is the oldest cryptocurrency fund, so it has the most complete data on investor behavior across three cycles. This is an update of the histogram we originally released in 2014, after the peak in 2013. After the peak in 2017, we updated it in 2018. While it is still too early to call 2021 a peak, a quick update is useful.

Going with the flow is human nature.

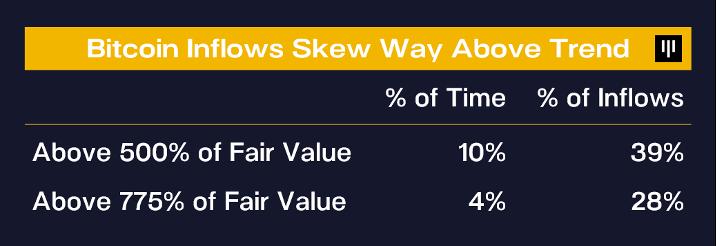

The following chart plots the percentage of time Bitcoin prices have spent in each price bucket. This time we added a new perspective: the buckets are on a logarithmic scale. Each bucket is a rebound of 33% from the lower bucket. They are marked according to the percentage of Bitcoin trading trend prices.

The gray bars represent the percentage of time Bitcoin has traded within each price range. The price distribution is fairly normally distributed. Most of the time is spent at or near trend.

The gold bars show the percentage of inflows into each valuation bucket. The inflows are very skewed—heavily cyclical. When Bitcoin is very weak, inflows are very low. When Bitcoin's trading price on trend dollars is equal to or below 37 cents, very few investors are willing to buy.

On the other hand, when its trading price is far above its trend, there is a large influx of funds. Most of the funds tend to cluster together.

For example, the market spends only 10% of the time above fair value by 500%, but 39% of the inflows reach or exceed that level.

This is not all bad. As we have emphasized, Bitcoin tends to go up. It has averaged more than double its value every year for a decade. Anyone who has held Bitcoin for 3.25 years has made money. Bitcoin has only experienced one calendar year of lower lows. Therefore, most of these investors have seen significant gains.

Resist the impulse to close out. If you have emotional and economic resources, take another path.

For new investors, it is best to buy when the market is below trend. Now is one of those times.

Update: In the past 11 years, the proportion of time the market has been so "cheap" or cheaper relative to trend is only 13%.

Blockchain Fund: Additional Close

Because we believe this is a particularly attractive investment opportunity, we will add an additional close for the Blockchain Fund on March 1. Investors entering at that time can still lock in these attractive valuations.

Blockchain Fund: Final Close

Many investors view blockchain as an asset class and hope their managers will allocate across various asset buckets. This prompted us to create the Pantera Blockchain Fund, a new "integrated" wrapper for the entire range of blockchain assets. We believe this new fund is the most effective way to gain exposure to blockchain as an asset class.

The Pantera Blockchain Fund is like a super collection of our existing four sector funds.

The most important feature is that we can invest in the huge value fluctuations between tokens and venture capital. Token reconfigurations happen very quickly, while venture capital progresses slowly.

Like our previous Pantera venture funds, we offer a co-investment class. Limited partners (LPs) investing $15 million or more will have the option to co-invest at least 10% in each venture capital and early token trade.

If you do not meet this threshold and are interested in co-investing, we will provide additional co-investment opportunities for all LPs in the fund. In the past 12 months, LPs without co-investment rights had the opportunity to invest in 8 transactions, such as Arbitrum and Bitso. They were able to co-invest $25 million.

For investors who prefer venture capital, the new fund offers a venture capital-only class. This class will only access the equity transactions we make—and will not invest directly in tokens. It is essentially "Pantera Venture Fund IV."

Pantera Blockchain Fund Investment Highlights

The Pantera Blockchain Fund has invested in 41 early token projects and venture equity transactions.

Pantera led a $12 million Series A round for Aurora—a bridge for the NEAR blockchain aimed at providing Ethereum compatibility and scalability for NEAR smart contracts. In addition to a few DeFi investments, we also invested in Arbitrum, a leading Layer 2 scaling solution that supports some of the largest decentralized applications in the ecosystem.

The team has also been looking for deals in two of the hottest areas—blockchain gaming/metaverse and NFTs. Pantera has led or co-led 24 transactions and will announce more deals in the coming months.

Blockchain Fund Venture Capital

As blockchain attracts some of the smartest minds and entrepreneurs from big tech companies and Wall Street, the deal flow is setting records. Our investment team is looking for projects that make blockchain more accessible and usable for mass adoption. We will announce many of these deals in the coming months.

Why Web3 is Important

Following the debate sparked by comments from Elon Musk and Jack Dorsey about the merits of Web3 applications at the end of last year, we decided to hold a conference call on why Web3 is important, inviting Nader Al-Naji from the DeSo Foundation and Roneil Rumburg from Audius. Here are some highlights from the discussion:

Q: How do you define "Web3"?

Nader Al-Naji: "I personally think Web3 is something built on the blockchain. If you are using a blockchain, to me, that is Web3. You might ask, 'What does that mean? Why is a category of applications based on blockchain so interesting or different?'

I think the biggest reason Web3 is interesting is that when developers build on the blockchain, all assets and content are actually shared among all developers, allowing them to build and innovate with each other in ways they could not achieve in Web2. This concept is called composability.

To give a concrete example, using the DeSo blockchain, the applications built on it actually share the same content pool. This means interesting things happen. Just like when you post in one app, it actually appears in all other apps.

If you build followers in one application and then want to move to another application, all your followers can actually access that new application as well. As I mentioned, the concept of sharing data across all applications is called composability, and I think it is key to distinguishing Web2 from Web3 applications."

Q: Recently, Jack Dorsey and Elon Musk publicly questioned the reality and vision of Web3 on Twitter. When tweeting, Elon stated: "[It] seems more like a marketing buzzword than reality right now." Is he right?

Nader Al-Naji: "I think those who dismiss Web3 may not understand the power of composability—the power of assets and content being shared and truly owned by users. I think when you have composability, platforms that fully support it (Layer 1 and similar) are inevitable.

Because a single killer application built on them will lead to all these users and data being shared, and then more applications will be created, creating a virtuous cycle. We have seen this on Ethereum, and I think when this happens, it cannot be ignored.

Q: Jack Dorsey has a critical view of ownership in Web3, saying, 'You don't own Web3' and 'it ultimately is a centralized entity with a different label.' Do you agree?

Roneil Rumburg: "I both agree and disagree. I think one point I agree with is that most crypto networks today are in their early stages. This often means that the distribution of token ownership in the broader community is not super decentralized.

However, when you consider this in comparison to existing Web2 products, it is a novelty for these companies to actively provide ownership to users who are so young in their lifecycle. But more importantly, the way these products are actually designed is that they continuously allocate ownership to the users who make them valuable.

The typical Web2 lifecycle for a company is: sell equity to investors, use that money for marketing and customer acquisition to attract users, from which you can gather data and sell to advertisers. The growth flywheel operates fundamentally around the separation between capital owners and those who actually create valuable assets (i.e., data) on the network.

"You can remove several layers of existence from this. I think this is what these networks do by incentivizing users to create valuable resources (i.e., data) by allocating ownership to them to guide network effects in the early stages—this is a very powerful incentive mechanism. 5 to 10 years from now, if you predict the expected inflation rates and distribution timelines for most of these networks, they will not look centrally owned or centrally controlled at all…

"So I think [Jack]'s criticism is valid today, but it misses the mark. I think no one is saying these things have ideal ownership distributions. But I certainly think these products, assuming they have a 2, 3, 4, or 5-year history, have ownership distributions that are more user-oriented than products like Twitter, which at the time were owned by six or seven investors and then possibly a few early employees."

Paul Veradittakit's Views on the Metaverse and P2E

Play-to-earn: Play-to-earn (P2E) is a blockchain-based game where players can earn money based on their in-game activities, undoubtedly one of the most important industry themes this year.

Axie Infinity generated over $15 million in revenue daily at its peak, demonstrating the power of the game-as-earn experience. Many other games, from Star Atlas to Genopets, have announced that this vibrant in-game economic trend will continue.

To maximize performance and earnings—in many of these games, players sometimes need to make an initial asset investment to start their journey from gaming to income. For example, in the Axie Infinity model, users must have a team of three "Axies" to start battling, which can cost hundreds of dollars.

This issue has sparked the creation of gaming guilds. Guilds lend in-game assets (like those Axies) to their "scholar" networks, enabling them to play the game and earn a share of the income in return. Many of the largest guilds, such as Yield Guild Games or Merit Circle, have thousands of scholars and are valued in the billions.

Metaverse: "NFT" may be the word of the year for Collins Dictionary, but another concept in the tech space entered mainstream consciousness in 2021: "metaverse."

Everyone is talking about it. Partly driven by macro factors, such as the digitization of our lives due to COVID—and possibly pushed over the edge by Facebook's recent rebranding to Meta—this topic is one of the most discussed, from New York Times op-eds to casual dinner table conversations.

This is a topic that has been discussed in detail elsewhere. I have even mentioned it in some of my recent articles. However, at the risk of sounding like a broken record, I think this topic is still worth exploring in depth.

What exactly is the metaverse?

Defining "metaverse" has been an impossible task from the start.

On one hand, it is still too early to predict what the metaverse will evolve into and what it will ultimately mean for us, much like predicting that Snapchat would be a phenomenon immediately after the iPhone was released.

Worse yet, there is a lot of semantic debate. Some people think "metaverses" (plural) is more appropriate because there will be multiple different virtual experiences accessible through various interfaces. Some people do not like to use the term at all because it has become a buzzword—"metaverse" has come to encompass almost everything in the virtual world. Perhaps "metaverse" itself will eventually be phased out; who knows!

For now, at least, it is useful to attempt to derive an accurate definition for this concept. The best one I can find comes from Matthew Ball, an investor whose writings on the metaverse are must-reads. While he acknowledges that a perfect description is impossible, he defines the metaverse as:

"A massive and interoperable network of real-time rendered 3D virtual worlds that can be experienced with a sense of personal presence and data continuity, such as identity, history, rights, objects, communication, and payments."

There is a lot to unpack there, but some of the standout elements are: it is 3D, open to nearly infinite people, and has some continuity elements similar to real life.

For some, this may evoke images of Second Life, the popular MMORPG from the early 2000s. While this analogy has some merits, it visualizes a single-type metaverse. In reality, the design space for metaverse builders will be vast and ultimately driven by us users.

So, who is building the metaverse? So far, they have been divided into two camps: non-crypto and crypto metaverses. And until recently, they have been building more or less in parallel.

Non-Crypto: The Tech Giants' Metaverse

Given the long-standing association of the metaverse with virtual reality, we believe that "metaverse" has been developed by many VR companies for several years. For example, VRChat and AltspaceVR have been two of the most prominent platforms for working and socializing in virtual reality. Especially for COVID, the use case for virtual events found early appeal.

This year, two major tech companies—Facebook (now Meta) and Microsoft—have placed significant bets on the future of the metaverse, directly incorporating it into their near-term roadmaps.

Of course, Facebook rebranded to Meta at the end of last year and launched their own Horizon Workrooms product for VR-based teamwork. However, they seem to have larger ambitions, not only financially (about $10 billion annually for various metaverse-related R&D) but also in scope.

At least from his public statements, Zuckerberg seems to "understand" why interoperability and openness are important and claims to be moving in that direction because he believes this is a new era for the company.

We will see what Meta ultimately does. After all, they are still deeply rooted in the profit-maximizing, zero-sum competitive cycles of Web2 tech companies, so I do not expect them to necessarily build the metaverse we hope for. But I also will not jump to conclusions too early.

Crypto: A Community-Owned Metaverse

In our industry, the approach is different. The core principles of decentralization, trustlessness, pseudonymity, and community ownership have been ingrained from the start.

Some of the earliest virtual worlds created using blockchain technology include The Sandbox, Decentraland, and Cryptovoxels. While each has different elements and world economies, the power of blockchain and NFTs allows for true digital land ownership, opening up entirely new types of activities, from renting out your land to customizing homes for others.

Many early activities have come from buyers hoping to reserve their land for future generations in the metaverse, but some interesting uses have begun to emerge. For example, Decentraland hosts events almost daily that users can participate in and experience. Brands like Dominos, Atari, and others have also purchased land to promote their goods, host events, and build visibility in the virtual world.

Where Do We Go from Here

We have a long way to go before the metaverse moves into the "mainstream." Frankly, we are not even close.

It will start with enterprises (like Microsoft, Meta) and gaming (like Decentraland) and then slowly expand from there. Personally, I believe that an open, decentralized, and community-owned metaverse will defeat closed, rent-extracting, and surveilled systems, which is one of the many reasons I believe Web3 will disrupt Web2. But this future is by no means predetermined; it needs to be built!

In many ways, we are still in the picky stage of this industry. The metaverse needs its own currency—we have more or less covered that. But the metaverse also needs its own sovereign infrastructure stack that does not fail when AWS goes down.

Or decentralized messaging to project management tools that allow a group of people to easily collaborate with each other. Or standards for NFTs as they cross between "metaverses" and different rendering environments. In short, we have a lot to do for this new future.

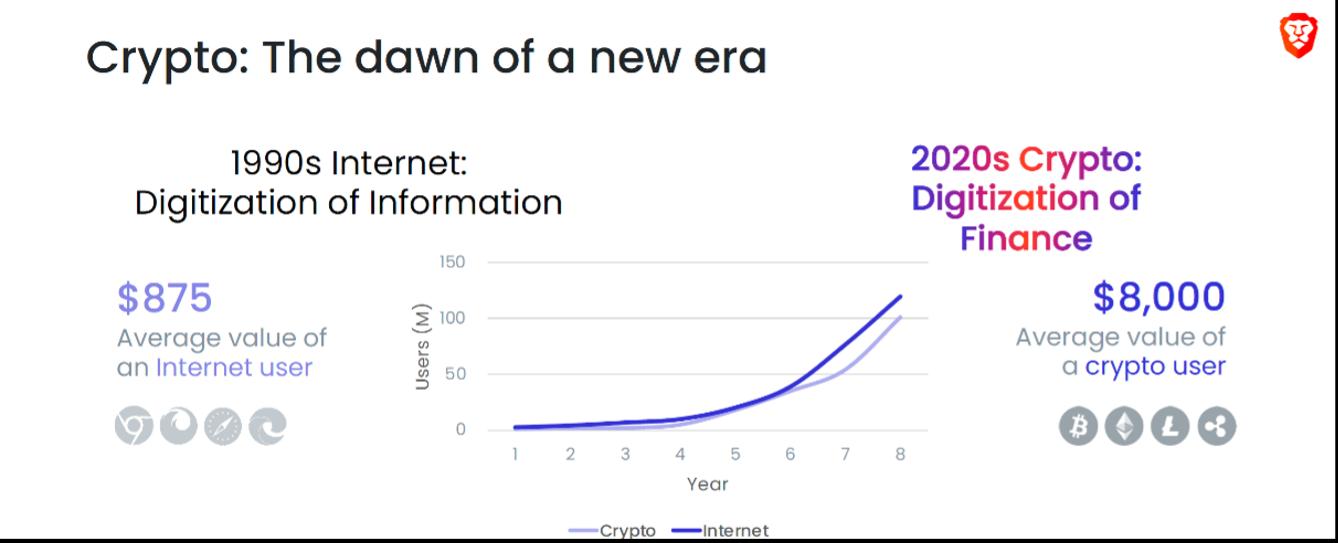

Internet vs. Blockchain Analogy

Brave released this cool chart showing the number of people using cryptocurrency closely following the internet in the 1990s—reaching 100 million users every eight years.

This captures the essence of the Pantera thesis:

"Cryptocurrency and blockchain technology are the foundation of new financial infrastructure, just as the internet is the foundation of new information infrastructure."—Pantera Capital Co-CIO Joey Krug

The value created by financial digitization is much greater than that of the previous generation's information digitization. Today, the average value of a crypto user is $8,000, compared to $875 in the 1990s.

Companies like Brave combine the advantages of digital assets with everyday tools like browsers. They have seen explosive user growth over the past five years.

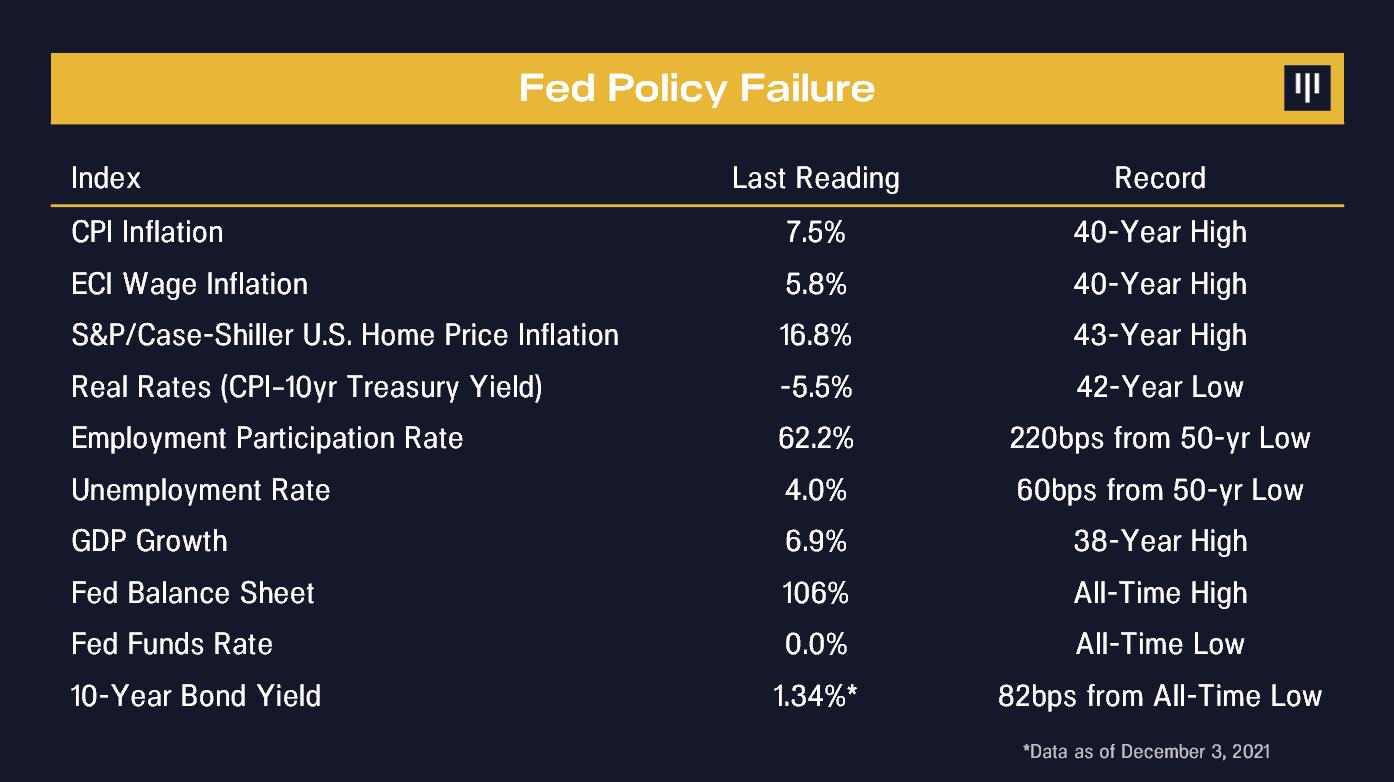

Federal Reserve Policy Failure

The policy inertia of the Federal Reserve is shocking. The data has been overwhelming since we started writing this article in November. Everything is in an extreme overheating state not seen in half a century—yet the Federal Reserve is still trying to suppress bond yields and set the federal funds rate to zero?!?

If you had handed this chart to an economist a few years ago and asked what the appropriate federal funds rate should be, no one on Earth would have chosen zero.

What Game is the Federal Reserve Playing?

St. Louis Fed President Bullard said in an interview with The Wall Street Journal on Monday that he sees no need for a significant rate hike. "We do not want to be disruptive or surprising to the markets," Mr. Bullard said. He stated that he would change his view "if the data here is unfavorable to us."

What they will ultimately have to do to unwind their manipulation will be surprising and hugely disruptive. As they wait for the data to turn against them, I look at the chart above, and I really cannot imagine what else they are waiting for.

His colleague, Cleveland Fed President Loretta Mester, said on Wednesday that she thought "there is no compelling reason to start" raising by 0.5 percentage points.

(The appropriate rate is 5.00%… not 0.5%.)

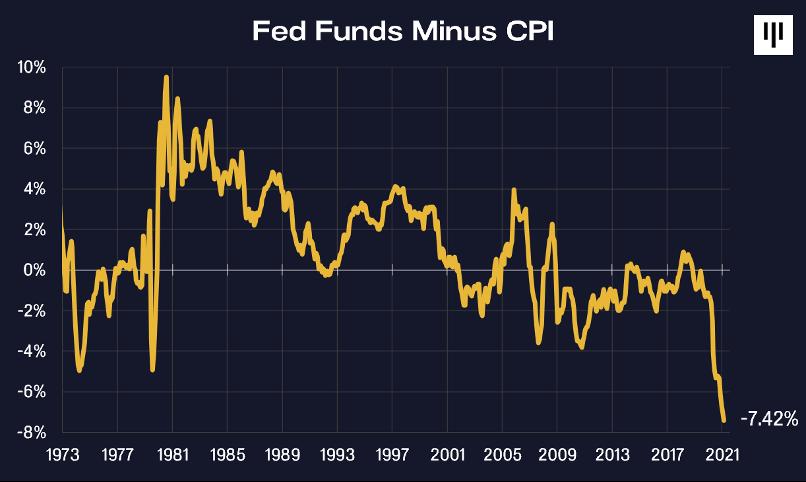

Real Federal Funds Rate

Inflation is 7.42% higher than the federal funds rate (el zippo). For most of my career, the Federal Reserve has kept rates above inflation to exert downward pressure on inflation. The average is +0.99%. For whatever reason, they are still pouring gasoline on the fire. We are at a historic low.

Money Printing

According to data released by the Treasury on Tuesday, as of January 31, the total outstanding public debt was $30.01 trillion. This is nearly $7 trillion more than in late January 2020, before the pandemic hit the U.S. economy.

This makes the math easy. The U.S. has just over 300 million people. In this country, $30 trillion is $100 for every man, woman, and child. The average family's share of the national debt is $243,902.

I think printing this debt to lower mortgage rates—thereby pushing up home prices—so that many citizens cannot afford homes will be seen as a massive policy failure. And the Federal Reserve is still **buying mortgages with printed money today.

There will be many PhD theses on whether printing money is a wise investment for our future.

Labor Inflation

The U.S. Employment Cost Index (a quarterly measure of wages and benefits paid by employers) shows that labor costs continue to grow at the fastest pace in twenty years. The Labor Department reported a 4% increase in the fourth quarter compared to a year ago.

The labor force participation rate remains close to a 50-year low. The lowest proportion of Americans in two generations are either working or looking for work.

The very low unemployment rate is because many people do not want to work, not because there are many jobs to fill. This is crazy— we lost 2.4 million jobs, yet the unemployment rate went down.

The Labor Department stated that in October, there were about 3.6 million more job openings than unemployed workers. This has prompted employers to look for ways to attract new workers.

Inflation: Causality

"If car prices are too high right now, there are two solutions: increase the supply of cars by making more cars, or reduce demand for cars by making Americans poorer. There are many people in the second camp… I reject it."—President Biden, January 7, 2022

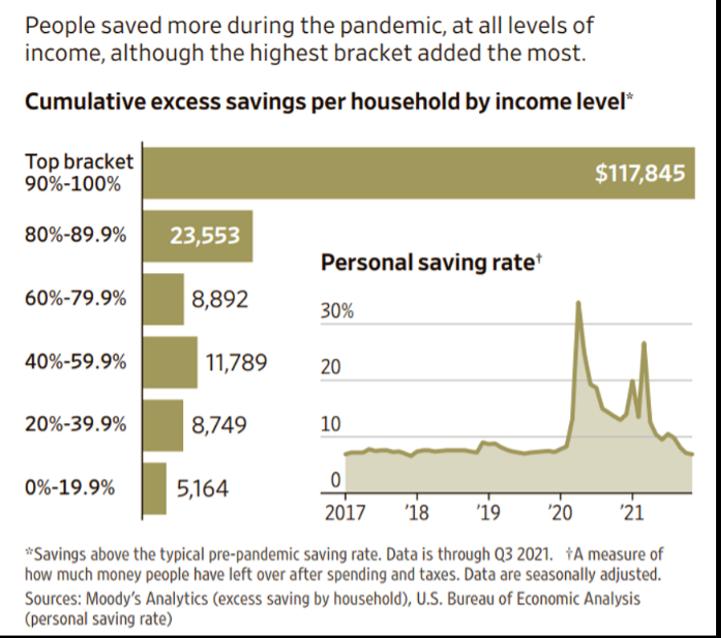

Of course, President Biden is correct. If you reverse this logic, it explains why there is so much inflation. The government printed $9 trillion and handed out this free money to everyone. A small portion of those people actually needed it—indeed, they could have used more help. Most people did not need free money. The savings rate proves this.

(Unfortunately, printing money is an extremely inefficient way to combat an invisible virus. Most of the printed money flowed to those who were already wealthy.)

Too much money chasing too few goods.

According to the Bureau of Economic Analysis, the personal savings rate (which measures how much people have left after spending and taxes) reached a record 33.8% in April 2020. This ratio averaged just below 8% in the two years leading up to the pandemic.

The second problem with this logic is that when policies lead people to stop working, it is hard to increase the supply of goods. The labor participation rate in the U.S. is close to a 45-year low. When policies make millions of workers unwilling to work, it is hard to produce more goods.

Federal Reserve Chairman Jerome Powell stated in recent congressional testimony that the reduction in the U.S. labor force "could be a problem for future inflation, possibly more severe than these supply chain issues."

I believe this is the biggest reason for inflation.

Key Points from Bloomberg's Interview with Pantera Founder Dan Morehead

Many people wish they had bought cryptocurrency earlier when it was just a curiosity.

Former Goldman Sachs bond trader Dan Morehead is one of the few who did, launching his first crypto fund when Bitcoin cost less than a bag of groceries.

"I was captivated," said the 56-year-old Morehead in an interview, calling it "the first truly global macro trade that crossed borders."

As a result, since 2013, the Pantera Bitcoin Fund has returned over 65,000%, while his Pantera Capital Management, which once was a traditional hedge fund betting on macroeconomic trends, now oversees "5.6 billion dollars in crypto assets at the end of the year. This is the basis for the $6 billion the firm has returned to investors.

The crypto market always has the potential to crash and burn. Bitcoin fell 17% earlier this year, trading at $38,600, as the U.S. market opened in New York on Friday, far below the November peak of about $68,000—this was due to expectations of rising global interest rates and central banks taking aggressive measures to curb soaring inflation.

This is where Morehead's world collides.

Morehead emerged during the adolescence of cryptocurrency, as he fully immersed himself in it after a legendary career in finance. He began trading bonds at Goldman Sachs in the 1980s, later worked for hedge fund legend Julian Robertson, and then founded Pantera in Menlo Park, California, in 2003.

"Rising inflation—and how central banks respond to it—will be a major theme in 2022," Morehead said, who previously bet that inflation and yields would decline for a long time.

That trade "basically made my career," he said, "I think it has reached the end of that story."

Morehead expects this dynamic reversal to weigh on cryptocurrency prices, but that does not diminish his enthusiasm for the underlying technology.

"Bitcoin and blockchain are disrupting the financial world," said Pete Briger, co-CEO of Fortress Investment Group, who worked with Morehead at Goldman Sachs. "Morehead is at the center of it all."

Dan Morehead could have gotten into cryptocurrency earlier in 2011 when his brother introduced him to Bitcoin. He read a bit about it, thought it was a cool idea, and then almost forgot about it.

Then, two years later, Briger brought him to Fortress's San Francisco office to discuss Bitcoin with early crypto technology evangelist Mike Novogratz. The 58-year-old Briger, a distressed debt expert, describes himself as a "garbage collector" of the financial system, and he believes Bitcoin has the potential to disrupt traditional banking.

"Blockchain is a game changer in financial services," Briger said. "It forces the banking and payments industries to rethink their reliance on traditional barriers to protect competitive advantages."

After the meeting, Morehead committed to doing more research, and a month later he told Briger that crypto was the most exciting thing he had seen in his career. He opened a shop in Fortress's office and began working on creating a cryptocurrency investment fund.

In addition to the returns from the Pantera Bitcoin Fund, the venture fund, which also debuted in 2013, has generated a 51% internal rate of return, and in 2021, Pantera's Liquid Token Fund soared 385%.

Risk warning

Risk warning Risk warning

Risk warning