Pantera: Cryptocurrency assets will reshape the global macro trade landscape

Pantera Capital believes that the prices of crypto assets will soon decouple from other risk assets. At that time, a world where bond yields exceed 5.0%, stock prices and real estate prices decline, while crypto assets rise tenfold will indeed exist.

Pantera Capital believes that the prices of crypto assets will soon decouple from other risk assets. At that time, a world where bond yields exceed 5.0%, stock prices and real estate prices decline, while crypto assets rise tenfold will indeed exist.Written by: Pantera Capital

Compiled by: Paimon, ForesightNews

Global Macro Trading Leader

Blockchain is the cornerstone of global macro trading.

Taking the USD/JPY exchange rate in traditional financial markets as an example, it has fluctuated within the range of 120 ± 20 for the past 35 years. A researcher with 35 years of trading experience has navigated the ups and downs of the exchange rate, only to be surprised to find that today’s rate has returned to the position it was at when he first entered the industry in 1987 -- 128.38. The cyclical nature of the exchange rate and its return makes the years of effort by USD/JPY traders seem futile.

In contrast, blockchain is currently changing the landscape of global macro trading -- if every smartphone user adopts blockchain within the next decade, the number of on-chain users will increase to 3.5 billion. This means we will no longer have the opportunity to buy Bitcoin at the "cheap" price of $38,342/BTC.

This is precisely why most macro traders who "repeat the past" favor Bitcoin or blockchain. Although the concepts studied in traditional fields are no different, the emergence of blockchain aims to optimize the operation of the entire world at a higher dimension.

Now, blockchain risk trading has even opened up a global macro perspective. For example, going long on Circle equity is a good way to hedge against rising interest rates. Circle earns floating funds on the USDC stablecoin. Rising interest rates drive up yields, making it a good counter-cyclical investment strategy.

Another cool fact is that the DeFi protocol Celsius paid its customers more interest in 2021 than American banks.

Institutional Transition Phase

Institutional investors are in a dilemma -- a few years ago, proposing to invest in blockchain meant facing significant career risks, while a few years later, not investing will pose a huge trust risk.

Trying to figure out which protocol will ultimately prevail is meaningless, yet many investors waste most of their meeting time on such questions.

No one asks a stock manager to explain which company will ultimately take over the world’s business when selecting a stock manager. Investors simply choose a high-performing manager, entrust them to build a portfolio, and win returns based on the changing composition over time. The investment process in the blockchain space should be consistent with that of traditional financial markets.

The advantage of blockchain is that choice is the investor's right -- they can buy both Ethereum and Solana simultaneously; they can buy Polkadot, Terra, and 20 to 30 other tokens at the same time.

The blockchain investment deadlock is gradually being broken -- over the past 12 years, more and more investment institutions have begun to enter the market. They generally invest about 0.2% of their funds into the blockchain industry. Once they start investing, this exposure will only increase, and in the next 5-10 years, the institutional investment proportion is expected to rise to around 8.0%. The funds being injected into blockchain assets will drive prices up.

Since the beginning of 2021, several blockchain industry funds represented by Pantera have raised $2 billion and will invest in the next year or two.

In the coming years, institutional investment in the blockchain space will increase by an order of magnitude, and the rapid rise in market enthusiasm seems inevitable.

Another dilemma is that today’s traders still believe that blockchain trading should be correlated with most other risk assets. However, the market should soon realize that, due to the lack of cash flow to discount, blockchain trading is fundamentally different from traditional markets. The pricing of cryptocurrencies is entirely based on supply and demand and is not affected by interest rate hikes. Assuming the number of people using cryptocurrencies multiplies by 10 every two years, as long as a fixed amount of currency exists and 10 times the number of people want to hold the currency, its price will rise.

In a world where most risk assets perform poorly, investors will take a leap of faith -- hoping that new investment methods like blockchain will perform better.

Pantera Capital believes that the prices of blockchain assets will soon decouple from other risk assets. By then, a world where bond yields exceed 5.0%, stock prices and real estate prices decline, while blockchain rises tenfold will indeed exist.

Pantera Select Fund

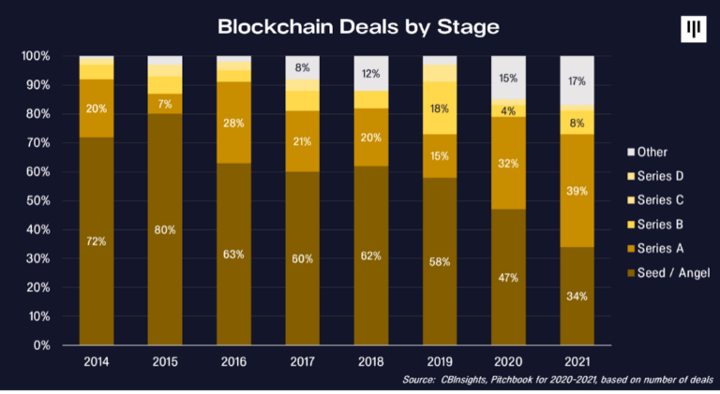

As the industry value expands to over $2 trillion, the blockchain trading market is maturing.

When we started investing, the target projects were basically in the seed and Series A stages. However, as the industry has developed, about 27% of investment targets have now passed the Series A stage.

Many portfolio companies are now valued in the billions. Pantera has spent nearly a decade helping companies like Ripple, Circle, Alchemy, Starkware, Coinbase, Amber, and FTX. For example, Pantera is the only VC that has invested in every round of funding for Alchemy.

Pantera will continue to support the best companies in the industry and is exiting a fund that is entirely in the growth stage. The Pantera Select Fund aims to allocate assets to take advantage of the industry's transition to more growth stages.

Pantera has a record-breaking trading network, and for a long time, Pantera has been providing growth financing opportunities to joint venture capital intermediaries.

In the past nine years, Pantera has simultaneously locked in three notable companies in growth-stage financing for the first time and provided them with a special fund to facilitate financing. Meanwhile, Pantera has stated that it will facilitate another seven to nine transactions next year.

The fund is expected to initially invest in three companies:

Amber: A leading cryptocurrency financial service provider for individual and institutional investors, serving as a gateway for digital assets, providing institutional-grade tools and investment products.

CoinDCX: One of the largest and safest cryptocurrency exchanges in India, known for its top-notch cryptocurrency financial services. It provides users with a secure and friendly experience to access various digital assets, along with insurance and security for its users.

[Company name confidential]: The largest supplier of NFT domain names on the blockchain; by establishing blockchain-based domain names, it allows users to replace cryptocurrency addresses with human-readable names, host decentralized websites, and simplify cryptocurrency payments, ushering the world into a decentralized network.

These growth financing opportunities will form the overall structure of the Pantera Select Fund, targeting $200 million, which is expected to complete what may be the only round of fundraising in May.

Compared to typical seed and Series A venture capital, the Pantera Select Fund will primarily focus on more mature companies that can generate revenue, with expectations as follows:

Two Years Under the Shadow of Pandemic Policies

It has been nearly two years since policymakers began implementing measures to offset the intangible virus's impact through money printing.

In April 2020, a letter marking the arrival of the post-pandemic era stated:

"This is a very distressing and chaotic time, as 99% of what is to come is up in the air. However, I firmly believe this will have a positive impact on cryptocurrency prices."

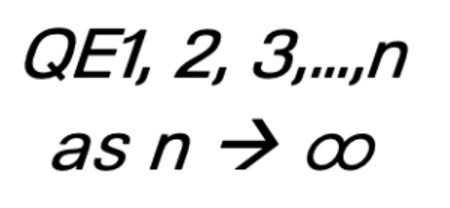

"The way children count to 100 is one, two, skip a few numbers, one hundred. It feels like we are doing just that with quantitative easing. QE1, QE2, skip a few stages, QE100."

As quantitative easing approaches "unlimited easing," it fundamentally must impact those things that cannot be relaxed in quantity.

"When the government increases the number of paper bills, more paper bills are needed to purchase things with a fixed quantity, such as stocks and real estate. Regardless of how much the money supply increases, the total amount of these assets will not be affected."

"… Like water pressure, the influx of new money causes the prices of fixed-supply assets like gold, Bitcoin, and other cryptocurrencies to continuously rise."

Since this prediction, the "tsunami" of paper money has brought unprecedented price increases, especially for cryptocurrencies. The following chart shows the performance of various fixed-supply assets since the increase in money printing:

The performance of other tokens even surpassed that of Bitcoin:

The performance of other tokens even surpassed that of Bitcoin:

Inflation, Aftermath of COVID-19

In an interview published by The Wall Street Journal around April 12 this year, Congressman Mark Pocan pointed out, "As they work to determine their campaign strategy for November, Democrats say they need to better promote the victories brought by Mr. Biden, mainly the COVID-19 stimulus and infrastructure spending, while clearly stating that they will work to lower price levels. We have done a lot. But the aftermath of COVID and inflation make it harder for us to talk about those really big issues."

What is concerning is that policymakers still do not understand that the aftermath of COVID and inflation are fundamentally the same issue, caused by excessive money printing leading to shortages of goods, declining employment rates, and a depressed real estate market. The overt policies are aimed at combating an invisible virus, but they exert a temporary squeeze on real estate, employment rates, and all other aspects. This is the biggest problem.

Foolishness of Moving Mountains? Wake Up!

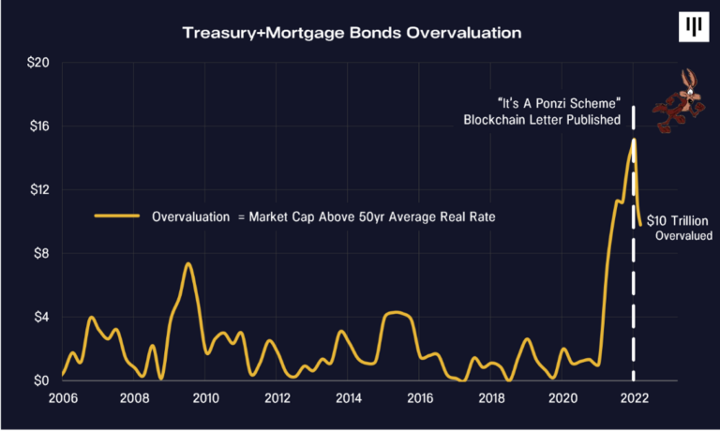

With inflation at 854 bps and tightening policies only at 25 bps, it is clearly unworkable.

Federal Reserve Chairman Powell acts as if he really intends to take significant action, perhaps raising interest rates by 50 bps at some point in the future. Inflation has increased by 17 times. Six months ago, the inflation level was about 500 bps, aimed at bursting the real estate bubble created by the Federal Reserve.

An investor told Pantera that he did just one thing in the conventional market -- buy as many houses as possible and mortgage them for 30 years.

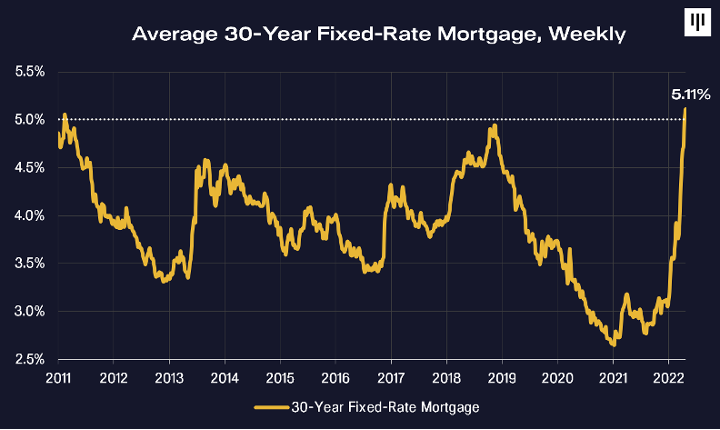

Pantera responded that the national housing market is running at a rate of 19.8%, while the Federal Reserve is still manipulating mortgage rates down to 5.0%, essentially making buying a house a last resort.

If the Federal Reserve does not hold any mortgages as they did for the previous 95 years, the free market mortgage rates will be absurdly high, directly creating the aforementioned real estate bubble.

In the coming years, the Federal Reserve will have to deal with the stagflation scenario of its continuously expanding prosperity or recession.

The U.S. Department of Commerce stated on Thursday that the annualized GDP for the first quarter of the U.S. declined by 1.4%, and GDP is negative.

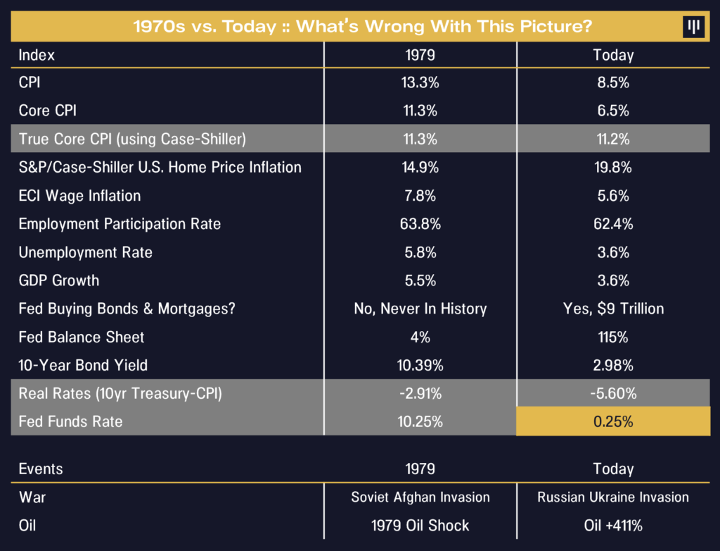

This is the So-Called 1970s

Want to play a game of "find the differences"?

Federal Reserve

Federal Reserve Vice Chair Lael Brainard stated in a public speech on April 12, "I don't want to be too rigid in thinking about the appropriate policy path for the remainder of this year and next year… Moving quickly toward a more neutral stance provides the committee with options in either direction."

This statement is quite surprising, as when everything is out of control, slowly moving toward neutrality is likely to be of little help.

The dual mandate of the Federal Reserve is price stability and full employment.

For them, price stability means allowing paper money to depreciate by "only" 2.0% each year. The real core CPI (using more realistic Case-Shiller housing prices) is in double digits, five times the Federal Reserve's target inflation rate. Clearly, this task has failed.

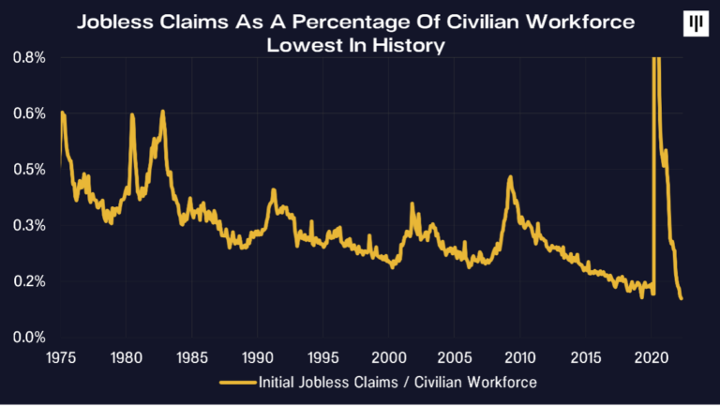

From an employment perspective, the U.S. is now clearly far beyond any optimal employment level. The proportion of people applying for unemployment benefits is less than at any historical moment in civilian labor.

Only one in a thousand loses their job, and the unemployment rate is roughly equal to the probability of being hit by a falling coconut while walking down the street.

Even the Federal Reserve Chairman admits that the tightness of the labor shortage is unreasonable.

Federal Reserve Chairman Powell stated in the minutes of the Federal Reserve's March meeting, "If you look at today's labor market, what you see is that every unemployed person has more than 1.7 job opportunities. Therefore, I would say this is a very tight labor market, tight to an abnormal degree."

Having 1.8 job openings for every unemployed person is unprecedented; typically, this ratio is reversed.

So why does this slow, slight increase ultimately lead to neutrality?

Because interest rates should be restrictive.

Former President of the Boston Federal Reserve Bank Eric Rosengren pointed out, "The Federal Reserve is certainly behind the curve. Inflation indicators like PCE and CPI are far above 2%. The unemployment rate is 4%, below the CBO's estimate of full employment. In such an environment, interest rates should be slightly above neutral levels. We are far from that target, so the Federal Reserve has a lot of room to catch up. If any mistake was made, it was not turning sooner."

The Federal Reserve's interest rates have been kept low for too long. They will raise rates to levels much higher than the futures market expects.

Unprecedented "Easing"

"When I entered this industry in October 1981, the yield on government bonds was 14%. By 2020, interest rates in all developed countries reached the lowest point in 5,000 years. With inflation and geopolitical uncertainty, this bull market has finally ended. Bond yields have rapidly risen in the 10-year sector, and I expect this trend to continue."

------April 5, 2022, at the Pantera Blockchain Summit, Bill Miller, founder of Miller Value Partners

Since the 2008 financial crisis, the vast majority of sovereign debt has been purchased by price-insensitive government buyers. This is a combination of central banks like the Federal Reserve monetizing their own debt and countries trying to keep their current account surpluses overseas, thus suppressing their currency value by selling currency and buying dollars (which requires investment in government bonds).

QE has created a rare investment world -- bonds and stocks rebounding simultaneously. (In a free market world, their prices are usually negatively correlated).

Quantitative tightening (QT) will cause both bonds and stocks to decline simultaneously.

Quantitative tightening (QT) will cause both bonds and stocks to decline simultaneously.

In response to the recent seizure of dollar reserves by hostile regimes due to sanctions on public and private entities, hostile regimes may also reduce their dollar currency reserves and liquidate U.S. Treasury bonds.

Stagflation Macro Trading: Key Points from the Bankless Podcast

Ryan Sean Adams: This is the highest inflation rate in 40 years, with an 8.5% CPI. Can you tell us what is happening?

Dan Morehead: I have been in this business for 35 years, so I have seen many cycles, and this is the craziest one. The Federal Reserve has inflated a bubble in bonds, which is just absurd. The bond market fuels the mortgage industry, and last year a record number of Americans took out mortgages and bought properties. A 19% increase in home prices was expected. If you are a homeowner, that’s a good thing, but 35% of Americans are not, so I think that’s a terrible thing.

About a year ago, the Federal Reserve Chairman said this was a transitional blip in inflation. This is not transitional; it is an enormous problem. Since Powell said it was transitional, new record highs have been printed every month. We are really back to the craziest times of the 1970s.

The cost of Uber has doubled, which for me is a huge sign of a tight labor market. Now used car prices are higher than when they were new. This is super crazy. This has never happened in history. Basically everything is on fire and more expensive.

David Hoffman: Why is there a bubble in the bond market?

Dan Morehead: First, Congress basically approved $9 trillion in spending.

The U.S. deficit over the past two years is larger than any year during World War II. During World War II, we were fighting fascism. That was a big deal. Here, the money spent on combating this intangible virus is staggering and incredibly inefficient. In the U.S., each household has to spend $50,000. I mean, that’s a huge amount of money. Of course, some policies need to happen, and some people really need help. But most people who received stimulus checks saved them. The savings rate has risen during the recession, which is also something that has never happened in history.

So, $9 trillion of new paper money has been printed and given to everyone. Similarly, a few of them really need help and may need more help. But most people do not need it. So what did they do with that money? They used it to buy things.

They bought stocks. Stocks are at historical highs. They bought gold, they bought bonds. So people used all the free new printed money to invest.

If you print $9 trillion of new paper money, you need more paper money to buy a car in 2021, or the median house in the U.S., or shares of the S&P 500 index. It really is that simple. Paper money is depreciating.

In my 35 years of trading experience, I have never seen anything so extreme and so huge. I have seen some strange trades in my little corner of the world, some strange things happening in emerging markets. But what the Federal Reserve is doing is on a scale of $9 trillion -- I mean, this is the biggest bubble.

David Hoffman: Can you tell us what you think will happen next?

Dan Morehead: I think in about two months, the Federal Reserve will realize that this thing is really getting out of control. They will have to start selling bonds instead of just waiting for these bonds to mature (which will take a long time since most of their bonds are 20-year maturities). When you go from the Federal Reserve buying billions of bonds every month to now selling billions of bonds, the bonds will be crushed.

I mentioned in our letter that this is the first non-blockchain trade I have made in eight years because it is so asymmetric. I think there is a 90% chance that interest rates will rise significantly.

The key is, you may not want to hold a lot of government bonds.

When I was growing up, there was a normal asset allocation of 60/40: 60% stocks, 40% bonds. I believe some pension plans and insurance companies still have a considerable amount of bonds in their traditional portfolios, but if you are a normal free market investor looking at all the facts we can see today, it is just hard to say, 'In the next 10 years at 2.7%, with a nominal inflation rate of 8.5%, but actually 10.7%, I want to buy a 2.7% 10-year bond.' I really can't imagine how anyone would do that.

I think money is depreciating, but the depreciation is slow. No working-age American is investing in a rising interest rate environment. This is very important for us -- I am 56 years old, and when I entered Wall Street, it had already been a bull market for six years -- the 10-year note was at 10%, so it could easily be 5% or 10% again. But most people your age have never been close to a 10% 10-year note.

For 40 years, everything has been rising because interest rates have been going down, down, down. In July last year, the 10-year rate reached 54 basis points. That marked the end of the bull market. Interest rates certainly won't go lower than that.

I think we are in a five-year bear market for bonds, and we all need to think this through. I am still trying to figure out what this means for our portfolio.

David: How do you see the cryptocurrency market digesting all this macro news?

Dan Morehead: Basically, this macro news is almost nowhere to hide, right? That’s why we call it "big unwind"; everything except cryptocurrencies will be affected, I think.

If we are even partially correct, bond yields will rise to 5% or higher, which will obviously crush bond prices, but it must also affect stocks and real estate and anything else with discounted cash flows.

I still believe that blockchain can have very low correlation with everything else because most people do not own any blockchain, right? Most institutional investors really do not own a lot of cryptocurrency assets. Some of the largest endowment funds may have one or two or 3% in blockchain. Many people still do not hold it, and most major insurance companies basically do not hold it.

So that’s how they can remain uncorrelated, and I think in the future, say, five years from now. If we are right, and blockchain is a very important thing, by then it will become an asset class, and I think there will be about 8% blockchain in everyone’s portfolio. Ten years from now, blockchain will have a correlation with the S&P index no less than anything else, commodities, bonds, or others. But for now, I really think it can remain uncorrelated.

Ryan: Can you elaborate on portfolio construction in the blockchain space?

Dan Morehead: Unfortunately, it’s not as easy as it used to be; if we want a quick answer, it’s basically unlikely.

Clearly, Bitcoin has been everything for a long time, and it’s great. I used to tell people to buy some Bitcoin. Then for a long time, I thought, buy half Bitcoin and half Ethereum, and you’ll be fine. The world now is much more complicated than that.

That theoretical answer, which is to diversify your portfolio, is clearly not super practical for all your listeners. We might invest in about 200 different things across all our funds. The reality is that there may be about 10 truly important Layer 1 blockchains. All the others are essentially companies built on other protocols.

The SEC Chairman said about five months ago that we do not need 5,000 new private currencies. I think he and many others misunderstood. There are not 5,000 Layer 1 blockchains, right? There are not. There are about 10 that are important. The rest are almost all applications built on other protocols. The U.S. has 4,500 publicly traded companies, so I have no problem with 4,500 tokens, right? We are not there yet. There are not 4,500 real tokens yet, but there will be in 10 years.

A well-performing portfolio should contain many assets, not just one or two of them. The theoretical answer is that due to the rapidly changing external information, we should try to diversify our investments. For example, last year, Bitcoin rose by 70%, and our liquid token fund rose by 325%. Many things are quietly changing, and Bitcoin is one of them, but there are also 30 other important assets in terms of liquidity.

In our portfolio, there are about 80 private tokens. Therefore, for those who can invest in fund managers, fund managers like us (who have a great group of managers in this field) are probably better now than before, when I would say just buy some Bitcoin and Ethereum, and you would be fine. These days, I think you really need a broader asset allocation.

Mortgage Inflation Rate ------38%

According to economist George Ratiu from Realtor.com, a year ago, the median mortgage payment cost for U.S. homes was $1,223 (monthly payment after a 20% down payment).

Today, such a purchase requires nearly $1,700 per month, an increase of 38%.

A Little Story About the Pantera Brand

Finally, let me conclude with a little story.

One day, I (Dan) was having lunch at an outdoor restaurant when a man named Mark Ross came over to introduce himself. He said he was an LP in our fund and asked how I named the company. I replied that it was named by my wife, Devon. When I discussed this with Devon, she gave the reason for the name, "I once worked at Tiger Management, and all the funds I encountered were named after big cats, and pantera means leopard in Spanish and Italian. Pantera was originally a global macro fund, and pan terra also means 'across the earth' in Latin. Oh, and one more thing, it’s also the name of a famous heavy metal band from the 80s."

And that’s why the man asked this question; Mark is A&R at Atlantic Records, and he discovered and signed that famous band, Pantera.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles