The merits and faults of CeFi from a liquidity perspective

The crypto industry should first fully recognize the existing problems, then establish an industry-level collaborative mechanism, clearly introduce infrastructure such as reputation, credit, and term financial products on the blockchain, and strive to create inter-institutional lending and repurchase markets, establishing a money market that is separate from the secondary market. Only in this way can the crypto industry enter a relatively stable and healthy development stage, supporting the significant development of Web3 and blockchain industry applications.

The crypto industry should first fully recognize the existing problems, then establish an industry-level collaborative mechanism, clearly introduce infrastructure such as reputation, credit, and term financial products on the blockchain, and strive to create inter-institutional lending and repurchase markets, establishing a money market that is separate from the secondary market. Only in this way can the crypto industry enter a relatively stable and healthy development stage, supporting the significant development of Web3 and blockchain industry applications.Author: Solv Research Group, Meng Yan's Thoughts on Blockchain

[Note] This article is the third in-depth analysis by the Solv Research Group regarding the recent crash in the crypto market. Following the previous discussion on the dollarization of the crypto market, it focuses on how CeFi institutions in the crypto market have effectively played the role of banks, providing liquidity supply, leverage management, and maturity transformation services to the entire industry, while exploring their flaws and reasons.

TL;DR

After the dollarization of the crypto market, liquidity (in the form of stablecoins) is primarily supplied through external inputs to support investment, speculation, and operational needs within the industry. During the 2017-2018 ICO phase, the main financing in the crypto industry was through direct equity investments, which had the drawbacks of extreme volatility and high moral hazard, leading to significant fraud.

Since 2020, as the crypto industry has dollarized, there has been a large-scale emergence of debt financing, resulting in a situation where equity financing and debt financing, as well as direct and indirect investments coexist. Therefore, the crypto industry needs institutions similar to banks to provide four important functions:

First, create liquidity;

Second, provide credit, help the production sector leverage, and manage leverage risk;

Third, conduct maturity transformation, manage maturity risk, and perform necessary risk isolation;

Fourth, optimize capital allocation.

To provide these functions, the ability to manage credit risk is essential. However, at the current level of technology and infrastructure, there is no credit mechanism in DeFi; almost all DeFi protocols aggressively push risks onto users without bearing any risk themselves. This is both the success and limitation of DeFi.

Over the past two years, centralized financial institutions (CeFi) in the crypto industry have effectively played the role of the banking system, bearing risks and providing the aforementioned services to the entire market. However, due to a general lack of corresponding knowledge and experience, they have made a series of mistakes in risk management, including:

- Arbitrary, unregulated, opaque lending;

- Pro-cyclical aggressive leverage, exposing huge risk exposures;

- Mixed operations and arbitrary misappropriation of funds for high-risk speculative trading.

Many people now attribute the collapse entirely to the stupidity and greed of certain CeFi institutions, which is convenient but meaningless. Essentially, this is because the crypto industry is still in its early stages of development, very immature, lacking a reputation-based credit system, failing to fully leverage the advantages of blockchain, and not establishing mechanisms for information disclosure and behavioral supervision of centralized financial institutions, let alone infrastructure like fixed-term DeFi lending and inter-institution borrowing markets. Therefore, when the bear market hit, CeFi institutions collapsed one after another, not only failing to manage and isolate risks for the industry but also exacerbating the crisis.

The crypto industry must first fully recognize the problems, then establish an industry-level collaborative mechanism, explicitly introduce reputation, credit, and maturity financial products as infrastructure on the blockchain based on mechanisms like SBT, and strive to create inter-institution borrowing and repurchase markets, establishing a money market separate from the secondary market. Only then can the crypto industry enter a relatively stable and healthy development phase, supporting the significant development of Web3 and blockchain industry applications.

[Main Text]

The crypto bear market of 2022 occurred against the backdrop of the dollarization of the crypto market. If we were to assign responsibility, two-thirds would be attributed to external macro monetary policy, and one-third to internal industry issues. However, for the development of crypto, it is precisely this one-third of internal issues that needs to be deeply explored and improved.

Let's start with stablecoins.

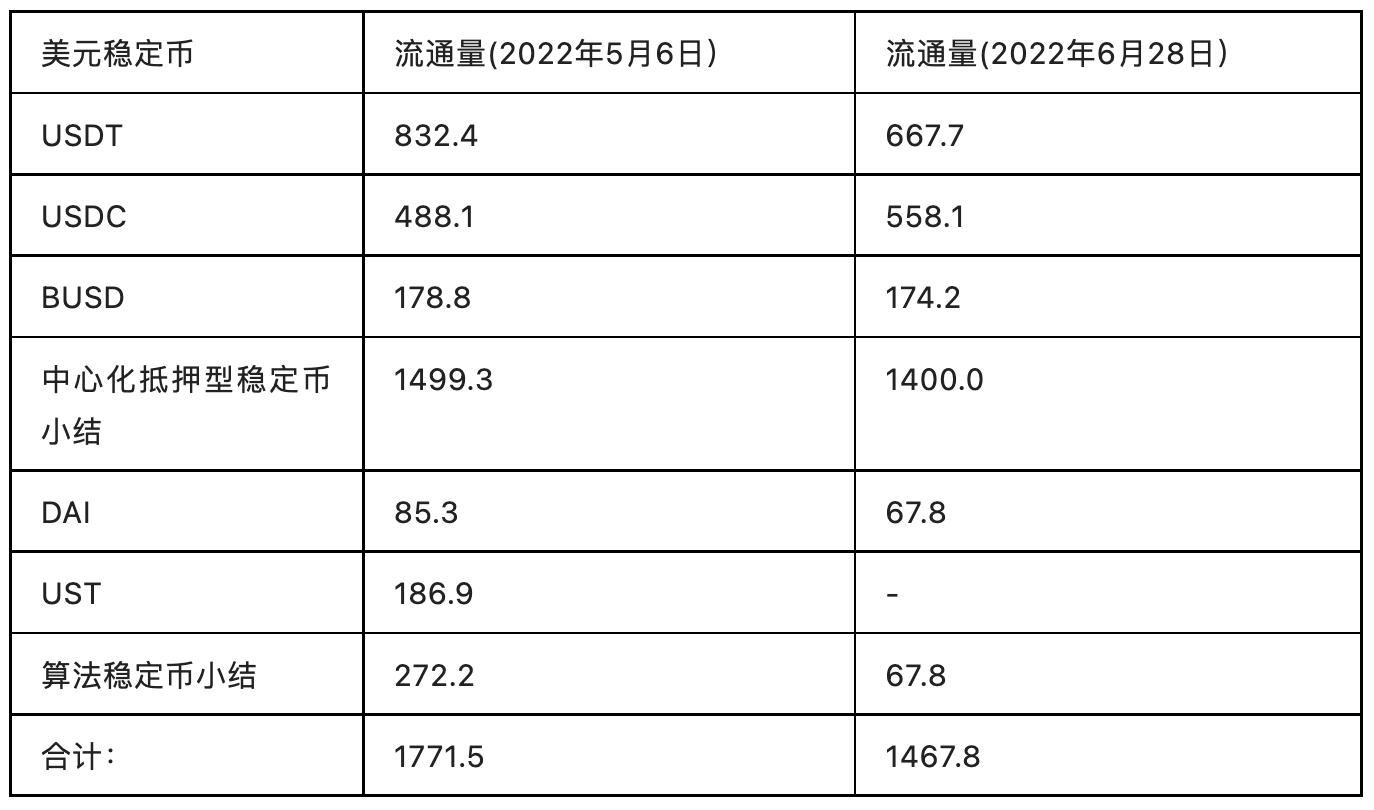

Before the full outbreak of the Terra crisis on May 6, 2022, the circulation of several major stablecoins was as follows:

Unit: 100 million USD

Figure 1. Circulation of major stablecoins before and after the collapse of Terra

As can be seen, the crash from May to June 2022 caused a 17.1% decline in liquidity in the crypto market, of which 10.6 percentage points were due to the collapse of Terra. Undoubtedly, this is a very serious liquidity contraction and a direct reflection of the current market entering a bear phase.

How did these stablecoins enter the crypto economy? Who created them? Through what means were they created?

1. The Supply and Demand Contradiction of Stablecoin Liquidity

During the 2017-2018 ICO phase, the main financing in the crypto industry was through direct equity investments, which had the drawbacks of extreme volatility and high risk, leading to significant fraud. Individual investors lack professional financial knowledge, risk management, and maturity transformation capabilities, and are particularly susceptible to herd mentality. The liquidity they provide is highly pro-cyclical, meaning it exhibits characteristics of "buying high and selling low," self-reinforcement, and extreme fluctuations. During the rising cycle of digital assets, these funds often flood in, leading to excessive market liquidity and a mix of good and bad projects. In the declining cycle, these funds often rush out, accelerating liquidity contraction and asset price declines, leading to rapid market collapse. Furthermore, equity investments share risks between investors and project parties, resulting in extremely high moral hazard and making fraud very likely. In practice, the crowd formed by individual investors often exhibits "adverse selection," consistently choosing the most fraudulent options among numerous projects, leading to poor capital allocation. Therefore, after the collapse of the ICO bubble in 2018, the entire crypto industry basically eliminated this financing model.

After 2020, with the rise of lending businesses and lending protocols, the entire industry presented a situation where debt financing coexisted with equity financing, and indirect investments coexisted with direct investments. Many people chose not to invest their stablecoins directly into projects but instead into intermediary institutions like funds, with more opting for debt financing. This has made the following two models the main drivers of liquidity creation:

First, centralized collateralized stablecoins like USDT, USDC, and BUSD are created using fiat currency as collateral. Before the crisis, this type of stablecoin accounted for about 85% of the total, and after the crash, this proportion increased to 95.4%.

Second, algorithmic stablecoins like MakerDAO and Terra over-collateralize digital assets such as BTC, ETH, and LUNA to create stablecoins like DAI and UST. This portion of stablecoins accounted for about 15% of the total before the crisis and decreased to 4.6% after the crash.

Once debt financing became mainstream, it immediately posed new challenges for liquidity management in the crypto market. As the true value builders and entities of the economy, project parties generally have the following capital requirements:

First, they hope for ample capital supply, but not excessive flooding. Ample funds enable quality projects to receive strong support, but excessive flooding allows many poor-quality projects and even Ponzi schemes to thrive, posing risks to the industry.

Second, they need stable and predictable capital supply that can isolate risks brought by market fluctuations, allowing project parties to focus on long-term planning.

Third, they require a rich selection of maturities, such as obtaining long-term financing through equity or tokens, or short- to medium-term liquidity through collateral or credit loans.

Fourth, they need to establish a clear, professional, and value-oriented evaluation system to optimize capital allocation, filter out poor-quality projects, and allow truly innovative and value-creating quality projects to succeed in the competition for funds and achieve long-term success.

However, such demands cannot be met by DeFi. Protocols like Terra and Maker, or lending protocols like Compound and Aave, also exhibit strong pro-cyclicality; they can expand liquidity when collateral asset prices rise, but aggressively liquidate collateral assets and withdraw liquidity when prices fall. This characteristic has been widely recognized following Terra's real-world demonstration over the past year. Another less-discussed issue is that existing DeFi does not bear any risks but aggressively pushes all risks onto users through algorithms. For example, almost all DeFi protocols lack the concept of credit and do not handle maturity transformation; they are all "on-demand" protocols. When collateral assets decline, DeFi stablecoin protocols or collateral lending protocols aggressively liquidate in real-time, immediately flooding the market with assets, which can easily trigger cascading market collapses. This situation has been frequently observed in the market crashes since 2020 and is an important force that turns volatility into collapse.

Now the problem is very clear. As the crypto industry dollarized, large-scale debt financing emerged, resulting in a situation where equity financing coexists with debt financing, and direct investments coexist with indirect investments. Therefore, the crypto industry needs institutions similar to banks to provide four important functions:

First, create liquidity;

Second, provide credit, help the production sector leverage, and manage leverage risk;

Third, conduct maturity transformation, manage maturity risk, and perform necessary risk isolation;

Fourth, optimize capital allocation.

Who has played the role of a bank over the past two years?

2. CeFi as Crypto Banks

The rise of numerous CeFi institutions is another phenomenon of the bull market cycle from 2020 to 2022. Before 2020, during the bear market cycle, although there were already many CeFi institutions, they primarily engaged in speculative businesses such as trading and arbitrage, with few CeFi institutions involved in productive investments and lending, and those that did were small in scale. After the bull market arrived in 2020, CeFi institutions emerged in large numbers, with the scale of managed funds increasing exponentially, and their functions underwent significant changes, effectively playing the role of the crypto banking system.

According to the Bank of England, the banking system primarily has three functions: money creation, leverage, and maturity transformation. A careful examination of the crypto industry during this bull market reveals that CeFi institutions indeed executed these functions. Particularly, the series of defaults and explosions that occurred among CeFi institutions during the recent two months of continuous crashes have helped us better understand the role of CeFi.

First, the liquidity of stablecoins is primarily created on the balance sheets of CeFi institutions. CeFi institutions generally raise funds through their own established fund institutions and convert the raised funds into stablecoins. This transformation ultimately occurs on the balance sheets of stablecoin operating institutions like USDT, USDC, and BUSD, which is also the mainstream method of stablecoin liquidity creation today. Therefore, it can be fully asserted that CeFi institutions are the currency creators of the entire crypto industry.

Second, CeFi institutions leverage other sectors through lending. Lending activities are widespread among CeFi institutions, and unsecured or partially secured credit loans are also very common. The recent series of explosive events involving Three Arrows Capital, Celsius, Voyager, and other CeFi institutions indicate the enormous scale of mutual credit lending among CeFi institutions in the industry. According to reported information, most of the borrowed funds were used for high-risk speculation, which was the direct cause of these institutions' collapse. However, it should also be noted that CeFi institutions provide credit loans to project parties, thereby leveraging the production sector, and this business is also developing. For example, on the Solv platform, the borrowing scale of project parties has approached 30 million USD, all used to support project development.

Additionally, CeFi institutions also bear the function of maturity transformation. When CeFi institutions invest in projects through token equity, they are essentially using short-term and on-demand funds for long-term investments. This "borrowing short to lend long" behavior inevitably introduces liquidity risk. CeFi institutions bear this risk, providing long-term funds to project parties, enabling them to engage in long-term planning and development. For instance, Three Arrows Capital announced investment news for entrepreneurial projects just weeks before its collapse. From the perspective of the invested projects, once financing is completed, obtaining funds from Three Arrows Capital means that even if the latter runs out of liquidity and collapses, there is no obligation to return the investment, allowing them to focus on development plans. In this sense, Three Arrows Capital converted its short-term liquidity into long-term liquidity and provided it to project parties, bearing the corresponding risks and acting as a firewall, ensuring that even if it collapsed, it would not implicate the invested projects. In contrast, since DeFi lending is mostly on-demand, once liquidity risks arise, they are immediately pushed onto users, so there is no maturity transformation. Why can't DeFi conduct maturity transformation? This is because maturity transformation requires the introduction of a credit mechanism, and since there is no credit mechanism in DeFi, it naturally cannot support maturity transformation; this task can only be accomplished by CeFi.

From the above three points, it is evident that many CeFi institutions have indeed played the role of the banking system in the industry.

Therefore, despite the chain reaction collapses of CeFi institutions during the bear market, which severely deepened the market downturn and led to media and public criticism, with some even advocating for "de-CeFi" and claiming that all financial functions in crypto should be realized through DeFi, we should view the issue more fairly. As long as it is finance, there will always be risks. To enable stable development in the industry, there must be someone to manage risks and, at critical moments, bear risks, even acting as a firewall to prevent crises from spreading further through their own bankruptcy. In the crypto industry, it is precisely the numerous CeFi institutions, rather than DeFi protocols, that have taken on the function of risk management, providing funds and stable expectations to the production sector. The continuous development of the crypto industry owes much to CeFi institutions.

3. The "Three Sins" of CeFi Risk Management

It is necessary to acknowledge that CeFi institutions have indeed played the role of the banking system in the crypto industry over the past few years. However, how do we evaluate the quality of their work as banks? It should be said that it is quite poor. Specifically, their performance in providing liquidity to the production sector is passable, but in managing their own risks, it can be described as a complete mess. Banks are institutions that manage risks; if they cannot manage their own risks well, they certainly cannot manage risks for the industry, making their work unqualified. The poor performance of CeFi institutions in risk management has also exacerbated the intensity of this market crash.

Specifically, some CeFi institutions have made the following three mistakes in risk management.

First, large-scale unregulated underground lending. Many CeFi institutions engage in large-scale unsecured credit lending among themselves. This is normal; similar to interbank lending in traditional finance, it is necessary for optimizing the allocation of funds and risks among various operating entities within the banking system. However, in the current CeFi landscape, there is no regulated, transparent, and supervised credit market, so credit lending among CeFi institutions occurs in a opaque, chaotic, and ruleless manner, without accepting interbank supervision or disclosing relevant information. We can only view these loans as a set of underground transactions, thus preventing the positive factors of market mechanisms from functioning. For example, Three Arrows Capital, which once had an asset scale of up to 18 billion USD, borrowed billions of dollars in unsecured credit from over twenty CeFi institutions after losing hundreds of millions due to the collapse of LUNA. These lending institutions neither knew the true asset status of Three Arrows Capital nor understood the use of the funds, nor did they know how much it was simultaneously borrowing from other institutions. As a result, after Three Arrows Capital's bankruptcy, several CeFi institutions like Voyager and Celsius were chain-reactively implicated, leading to bankruptcy or restructuring. This case fully illustrates how dangerous non-market underground lending transactions can be.

Second, mixed operations and arbitrary misappropriation of funds for high-risk speculative trading. Many CeFi institutions engage in large-scale speculative activities such as trading cryptocurrencies, trading contracts, quantitative trading, and DeFi arbitrage. If they were only using their own funds for speculation and bearing the risks themselves, that would be acceptable. However, due to the lack of necessary information disclosure and supervision mechanisms, they often use funds raised under other pretenses for speculative activities, crowding out the liquidity that should have been provided to the production sector. For instance, many crypto venture capital firms raise funds under the guise of investing in startup projects, but then buy or short mainstream assets like Bitcoin and Ethereum when they see a profitable opportunity. In the crypto industry, it is well known that during times of intense market speculation, innovative projects often struggle to secure financing, not because there is no money in the market, but because a large amount of capital is being used for speculation. Funds used for speculation merely participate in a zero-sum game and cannot create long-term value for the industry. The behavior of some CeFi institutions can be said to deviate from the principles that the "banking system" should uphold.

Third, aggressive leverage and unrestrained expansion of risk exposure. Many founders of CeFi institutions come from trading backgrounds and have years of market experience; the institutions themselves often engage in leveraged trading for extended periods. During bull market cycles, it is often the institutions willing to take on high leverage that stand out and achieve explosive growth in asset scale. Therefore, in the CeFi landscape, where heroes are often judged by asset scale and growth rate, the winners are typically those who dare to aggressively leverage and expand risk exposure. This risk preference and operational style are undoubtedly contrary to the requirements of the banking system. For example, a certain centralized lending institution long expanded its lending scale through circular pledging and leverage, and during the market crash in March 2020, it was once on the brink of bankruptcy. Although it took some hedging measures afterward, it continued to use self-financing to increase leverage during the bull market cycle, achieving astonishing high growth for a time. However, during the market crash from May to June 2022, due to the reverse effect of leverage, this CeFi institution rapidly collapsed.

When discussing these mistakes, it is easy for people to attribute responsibility to the stupidity and greed of certain CeFi institutions, as if the problem lies solely in the moral defects of individuals and specific institutions. Blaming "bad people" is certainly a convenient explanation, but it has always been a shallow and meaningless emotional outburst. The leaders of CeFi institutions, like everyone else in the world, will never be without moral flaws; there will always be greed and fear. The problem does not lie with individuals but with the systems and infrastructure.

The crypto industry is still in its early stages of development, very immature, lacking a reputation-based credit system, failing to fully leverage the advantages of blockchain, and not establishing mechanisms for information disclosure and behavioral supervision of centralized financial institutions, let alone infrastructure like fixed-term DeFi lending and inter-institution borrowing markets. Credit financial services like bonds are only just beginning to emerge. Therefore, when the bear market hit, CeFi institutions collapsed one after another, not only failing to manage and isolate risks for the industry but also exacerbating the crisis.

The crypto industry must first fully recognize the problems, then establish an industry-level collaborative mechanism, explicitly introduce reputation, credit, and maturity financial products as infrastructure on the blockchain based on mechanisms like SoulBound Token, and strive to create inter-institution borrowing and repurchase markets, establishing a money market separate from the secondary market. Only then can the crypto industry enter a relatively stable and healthy development phase, supporting the significant development of Web3 and blockchain industry applications.

We will propose a series of improvement suggestions in the fourth article of this series.

Risk warning

Risk warning Risk warning

Risk warning