Stablecoins enter an era of fierce competition, USDC sparks a paradigm dispute

On the eve of Aave and Curve entering the stablecoin space, MakerDAO showcases its pure Web3 lineage. Under the strong pressure of regulation, what is the future path for stablecoins?

On the eve of Aave and Curve entering the stablecoin space, MakerDAO showcases its pure Web3 lineage. Under the strong pressure of regulation, what is the future path for stablecoins?Author: Biscuit, Chain Catcher

As Aave is intensively formulating the specific parameters for the GHO stablecoin, MakerDAO announced that it might choose to sell all USDC exposure in the protocol. This is undoubtedly a bombshell that could redefine the standards for decentralized stablecoins.

According to Yearn core developer banteg's statement, MakerDAO may purchase $3.5 billion worth of ETH, converting all USDC from the pegged stable module into ETH.

MakerDAO's initial design was based on an ETH-over-collateralized stablecoin protocol, but it had to urgently introduce USDC during the "312" black swan event to survive, thereby losing its identity as a purely crypto protocol.

After the U.S. Treasury blacklisted Tornado Cash, Circle froze the USDC in Tornado Cash wallet addresses. This means that users who deposited USDC into Tornado Cash may not be able to withdraw their funds. This has left all crypto users anxious: Oh, it turns out our pride in decentralization is so fragile.

MakerDAO community member @Tetranode, who was once the largest liquidity provider for the protocol, angrily left after the protocol decided to introduce USDC. Now, he believes that Circle is helpless in the face of regulators, and the crypto world should explore stablecoins that do not rely on real-world redemptions.

According to CoinGecko data, the total market capitalization of stablecoins is approximately $153 billion, accounting for over 13% of the total cryptocurrency market capitalization, which is also a historical high. Centralized stablecoins (USDT, USDC, BUSD) account for as much as 90%. The crypto world seems to have been hijacked by centralization.

At the end of July, the Aave community's decentralized stablecoin GHO proposal passed with 99.9% of the votes, marking the highest level of participation in decision-making by Aave community members since 2022. Additionally, the founder of Curve revealed plans to launch an over-collateralized stablecoin. Why are these leading DeFi protocols shifting their focus back to stablecoins? Why are stablecoins a battleground for everyone?

The Quadruple Dilemma of Stablecoins

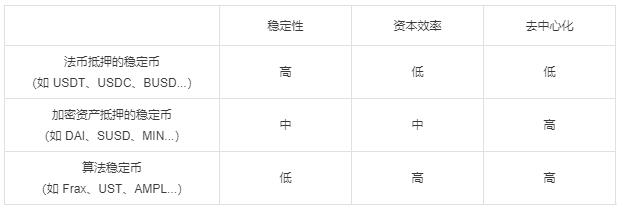

Compared to the "impossible triangle" of public chains, stablecoins also have their own triple dilemma: price stability, capital efficiency, and decentralization. Therefore, many crypto teams focus on one characteristic when designing stablecoins, making their stablecoin protocols more narrative-driven.

- Fiat-collateralized stablecoins (e.g., USDT, USDC, BUSD…): Stablecoins are issued by collateralizing fiat assets (e.g., USD, EUR, etc.), with each stablecoin backed 1:1 by real USD value.

- Crypto-asset collateralized stablecoins (e.g., DAI, SUSD, MIN…): Stablecoins are issued by collateralizing crypto assets (e.g., BTC, ETH, etc.), usually using an over-collateralization method.

- Algorithmic stablecoins (e.g., Frax, UST, AMPL…): Rely on complex algorithms to balance the supply and demand of stablecoins to maintain price stability through smart contracts.

Additionally, some emerging NFT protocols are also attempting to issue stablecoins, such as JPEG'D, which draws on MakerDAO's CDP (Collateralized Debt Position) model, allowing users to pledge NFTs to borrow stablecoin PUSD.

Countless crypto teams have attempted to challenge the throne of decentralized stablecoins, most of which have ended in failure. These bold social experiments are not without merit; we can extract viable successful experiences from these diverse solutions.

MakerDAO is the most successful decentralized stablecoin protocol, with advantages including support for multiple collateral types (including real-world assets RWA), adjustable loan interest rates, a quadruple tier liquidation mechanism, PSM module, and a Flash Mint module that allows users to quickly mint DAI.

Bolder innovations are happening in the realm of algorithmic stablecoins, such as the hybrid algorithmic stablecoin FRAX, which uses partial hard currency asset collateral to improve capital efficiency and balances market circulation through an algorithmic market controller (AMO). Ampl issues perpetual notes SPOT to hedge against AMPL's supply fluctuations. RAI's PID control module implements a dual-price model, and so on.

Although these successful experiences have limitations, it is undeniable that they will serve as a skill set for decentralized stablecoins, allowing designers to flexibly choose when necessary.

In addition to the triple dilemma, stablecoins are under special scrutiny from regulators, and the compliance (availability) of collateral has become a hidden fourth dilemma. From a traditional perspective, the "central bank" issuing stablecoins is the driving force behind all crypto activities, so regulators are more eager to strengthen oversight of stablecoin issuers.

The stablecoin project Libra by internet giant Facebook also met its demise due to regulatory challenges. Particularly, the collapse of the Terra ecosystem's Luna/UST pure algorithmic stablecoin resulted in a $40 billion evaporation, even causing issues in the real world. The U.S., Europe, and South Korea are all hastily drafting stablecoin legislation.

It cannot be ruled out that these regulatory bodies also want to "get a piece of the pie" in the crypto world. It is foreseeable that stablecoins will face stricter regulations. Therefore, when designing a stablecoin protocol, how to cooperate with regulation and what type of crypto collateral to use has become a new dilemma for stablecoin protocols.

The Competition Among Leading Protocols

On April 2, Terraform Labs community members proposed introducing a new "gold standard" for stablecoin liquidity, the 4pool. This move is essentially a declaration of war against DAI. In the presence of a rival, how can one rest easy? The intensity of the battle is well-known; UST suffered a devastating loss, and the market cap of decentralized stablecoins was halved.

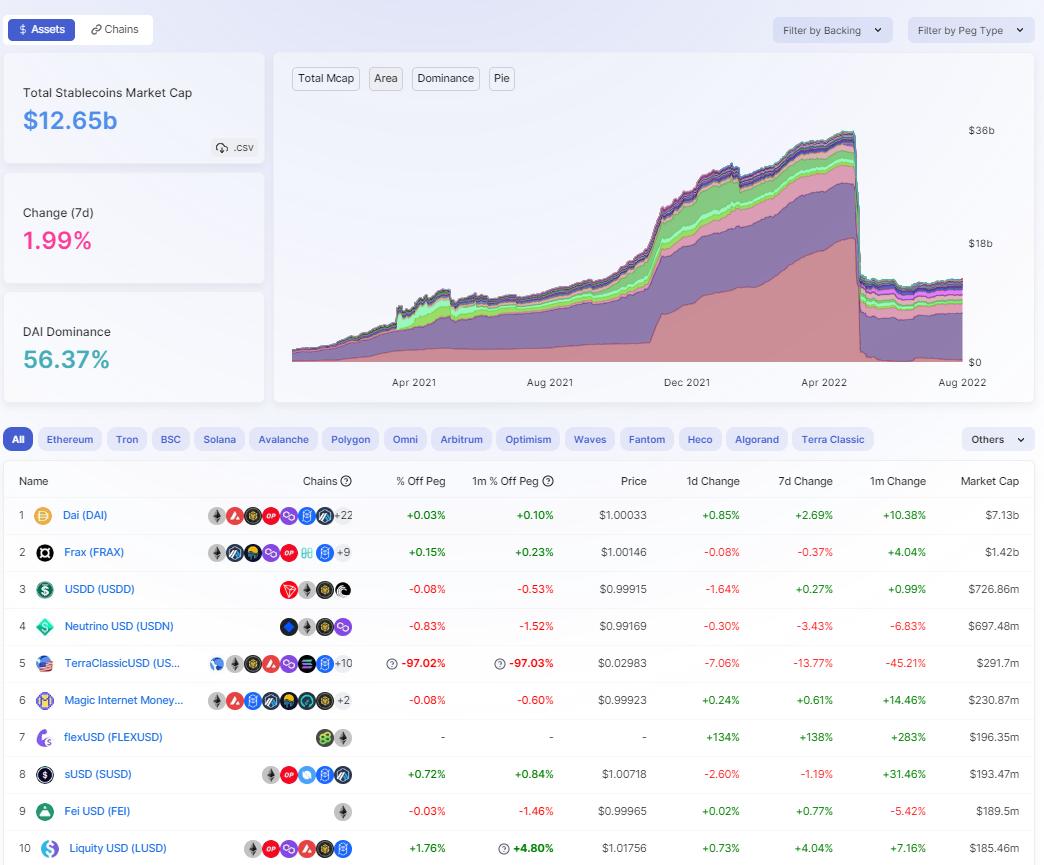

According to Defillama data, DAI's market share exceeds 56%, and GHO is likely to be positioned near the top, competing with DAI. Thus, the arena for decentralized stablecoins can be divided into major players (MakerDAO, Aave, Frax…) and marginal players (sUSD, Acala…).

Defillama Data

MakerDAO

MakerDAO has long acted as the central bank of the crypto world, with its issued DAI stablecoin ranking fourth among all stablecoins. The highly cohesive community and years of practical experience are the reasons MakerDAO has become the leader in decentralized stablecoins.

However, this decentralized "central bank" also faces its own dilemmas. According to DeFi researcher @kermankohli, MakerDAO's pure protocol revenue over the past 180 days was $24 million, which may only be enough to break even. The buy and burn model of the governance token MKR may also have issues; over the past five years, only 2.24% of the MKR supply has been consumed, and MKR's value capture ability may leave holders lagging behind other protocols.

Additionally, MakerDAO's endgame plan, the "EndGame Plan," may hinder the protocol's exploration in stablecoins. Proposed by MakerDAO founder Rune Christensen, this plan aims to restructure the protocol into multiple subDAOs to escape financial losses and community member apathy. However, when the flagship product DAI is no longer tightly held, will it be easily defeated by external forces and become a scattered entity?

To maintain its monopoly in decentralized stablecoins, MakerDAO is making strides in L2 networks and the real world. According to Defillama data, DAI's circulation in multiple L2 markets can rival USDT/USDC; within five days, DAI on Optimism increased from 30 million to 140 million, and even in the Aztec network, DAI is the only stablecoin.

Moreover, Maker has made significant progress in its real-world asset strategy, deciding to allocate $500 million from PSM to short-term government bonds and corporate bonds. Huntingdon Valley Bank has secured a partnership for loans equivalent to up to $1 billion in DAI, expected to generate $30 million in protocol revenue annually.

Aave

GHO is a decentralized stablecoin native to Aave, created by users (or borrowers). Like all loans on the Aave protocol, users must provide collateral (at a specific collateralization ratio) to mint GHO. Correspondingly, when users repay borrowed positions (or are liquidated), the protocol will destroy the user's GHO.

The collapse of Celsius prompted MakerDAO to disable the D3M module, which is likely the direct reason for Aave issuing the GHO stablecoin. The D3M module, or Direct Deposit Dai Module, allows users to borrow DAI directly from Aave at the highest interest rate. D3M provided Aave with stablecoin liquidity and minting discounts, while also bringing DAI minting revenue to MakerDAO. More importantly, DAI could quickly enter other public chains following Aave's multi-chain expansion strategy. This was a win-win collaboration.

Although the specific operational parameters of GHO have not yet been released, the proposal indicates that GHO is similar to DAI in many aspects, such as over-collateralization, decentralization, multiple collateral types, community governance, and so on.

Notably, GHO introduces the concept of "facilitators," which allows stablecoins to be issued entirely based on "credit," enabling GHO to be generated and destroyed without collateral. The overall exposure to specific vertical industries (i.e., RWA, over-collateralization, algorithms, etc.) may be very valuable. Aave DAO elects a facilitator through governance, then sets supply limits for GHO, allowing the facilitator to deploy in selected markets.

Additionally, GHO can leverage Aave's E-Mode to expand into more application scenarios, making it easier to integrate GHO into networks beyond L1.

Curve

Curve is also set to issue an over-collateralized stablecoin, which will release more liquidity for Curve and increase its total TVL. Previously, Curve launched a liquidity token, 3CRV, defined as a "3pool" token composed of DAI, USDC, and USDT.

In the face of the increasingly refined trends in the DeFi ecosystem, the composability and capital efficiency of 3CRV are obstacles limiting Curve's further expansion. If Curve issues the "Curve USD" stablecoin, 3CRV could be split into three pools, significantly enhancing the overall asset efficiency of Curve.

Frax

Frax is a hybrid algorithmic stablecoin protocol with the ultimate goal of becoming a complex and policy-flexible monetary system. From Frax's collateral structure and operational style, it seems that the protocol favors a "middle path." The protocol has established itself in the CRV wars by aggressively purchasing CVX and left a comment expressing interest in becoming a facilitator as soon as the GHO proposal was issued. Frax is unlikely to choose to compete head-on with leading protocols; perhaps "accumulating grain to wait for the king" is its core strategy.

Synthetix

sUSD is an over-collateralized stablecoin based on SNX, and due to a staking rate as high as 400%, the minting cost of sUSD is extremely high, often resulting in a premium of 2% or more. Therefore, the application scenarios for sUSD are limited. sUSD is primarily used for trading with other Synths within the Synthetix system. Previously, the UST from the Terra ecosystem was an experimental improvement of sUSD, reducing the staking rate to 1:1, but this experiment was too aggressive and ultimately ended in failure.

Final Thoughts

In the long run, centralized stablecoins will continue to hold the majority of market share, algorithmic stablecoins resemble a zero-sum game experiment, while over-collateralized stablecoins will have greater growth potential.

Stablecoins may enter a "dual-track" era. Centralized stablecoins (USDT/USDC), while lacking innovation, will do their utmost to embrace regulation, bringing real-world assets to the crypto space and maintaining their dominance in the crypto world. Meanwhile, decentralized stablecoins (DAI, GHO) will serve as the cornerstone of DeFi Lego blocks, fully exploring the value stability of the crypto world.

The fundamental contradiction of compliance lies in the fact that stablecoins want the real world to recognize the compliance and value of their assets while also maintaining decentralization (not being manipulated by third parties). Therefore, truly applicable stablecoin regulatory frameworks require more communication between crypto parties and regulators. A16z has also stated that it is wrong for crypto critics to use the collapse of Terra as a weapon against stablecoins and the entire crypto industry; tailored rule-making can support the crypto ecosystem and protect consumers.

We are currently in the mid-stage of the internal struggle for decentralized stablecoins, but it is unclear how long this process will take. GHO and DAI will inevitably become competitors, and healthy competition can drive DeFi forward. The war for decentralized stablecoins is essentially a struggle to maintain maximum liquidity and price stability.

Additionally, the hard fork triggered by the Ethereum merge will also impact all DeFi protocols, as almost all stablecoin protocols accept ETH/stETH as collateral. The risks posed by potential spot premiums, POW/POS collateral recognition, oracle pricing, liquidity, etc., require stablecoin protocols to prepare in advance.

Risk warning

Risk warning Risk warning

Risk warning