Web3 Investment in a Bear Market: Which Tracks Are Worth Investing In? Exploring Leading Funds and Alpha

The Web3 market is experiencing a winter, but builders are still continuously cultivating and laying out plans. Which sectors are still hot? What projects have top funds invested in during the bear market? A&T Capital has compiled financing data from the cryptocurrency market between May 1, 2022, and August 13, 2022, summarizing the primary market financing situation, trends in Alpha & Beta projects, and the main investment preferences of some leading institutions.

The Web3 market is experiencing a winter, but builders are still continuously cultivating and laying out plans. Which sectors are still hot? What projects have top funds invested in during the bear market? A&T Capital has compiled financing data from the cryptocurrency market between May 1, 2022, and August 13, 2022, summarizing the primary market financing situation, trends in Alpha & Beta projects, and the main investment preferences of some leading institutions.Authors: Jessica, Aaron, Rosie, A&T Capital

Introduction

First, we define the investment directions involved in our research.

Layer 1 includes scaling solutions for the data layer, network layer, consensus layer, and incentive layer, with typical examples including Avalanche, Solana, etc.

Layer 2 includes - contract layer projects, with typical examples including Perpetual protocol, Scaling, etc.

The application layer projects involve 21 different industry tags, among which the following need to be specified:

Web Builder: Represents web3 network, blockchain building services, distinguished from infrastructure.

Legal: Represents compliance services.

Environment: Represents ESG-related services.

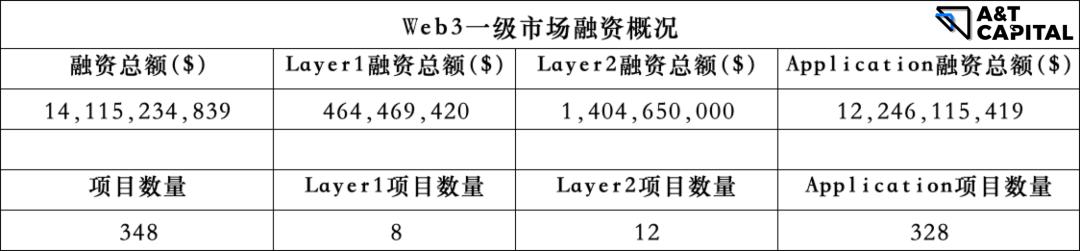

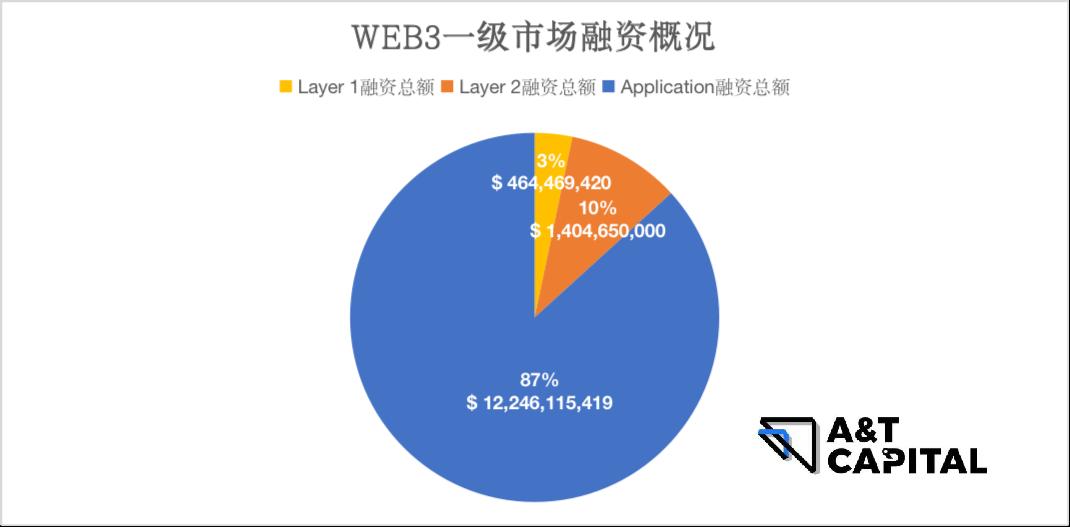

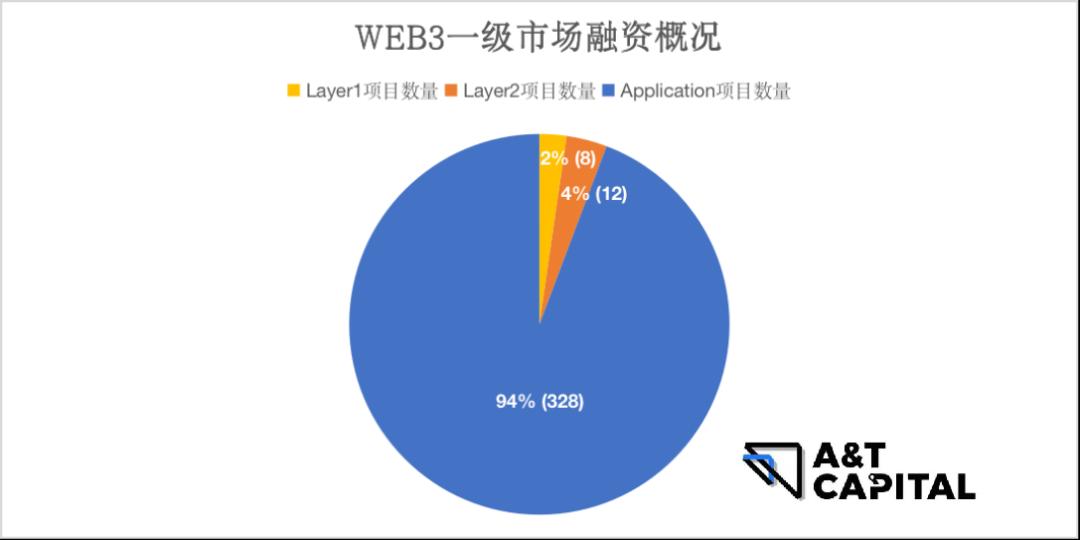

1: Overview of Crypto Primary Market Financing

Based on the above statistics, from May 1, 2022, to August 13, 2022, the application layer received the most attention from Web3 industry capital, with the highest number of funded projects: 87% of funds flowed into the application layer, and 94% of financing projects were also in the application layer.

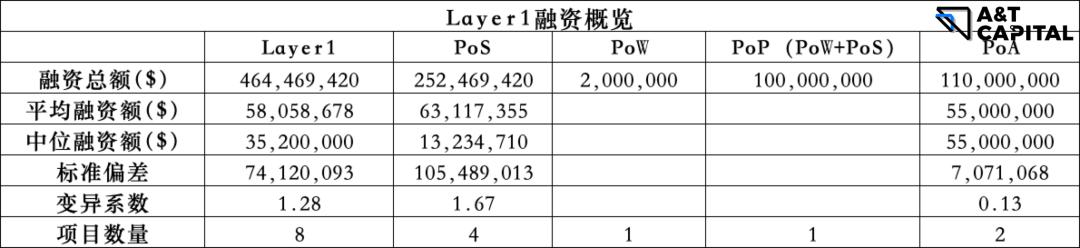

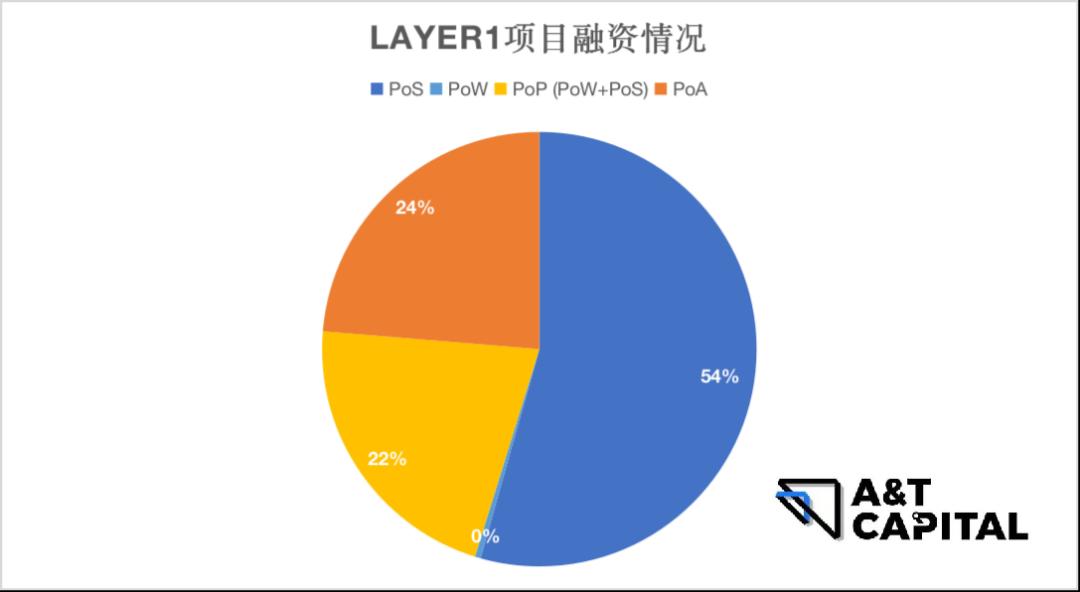

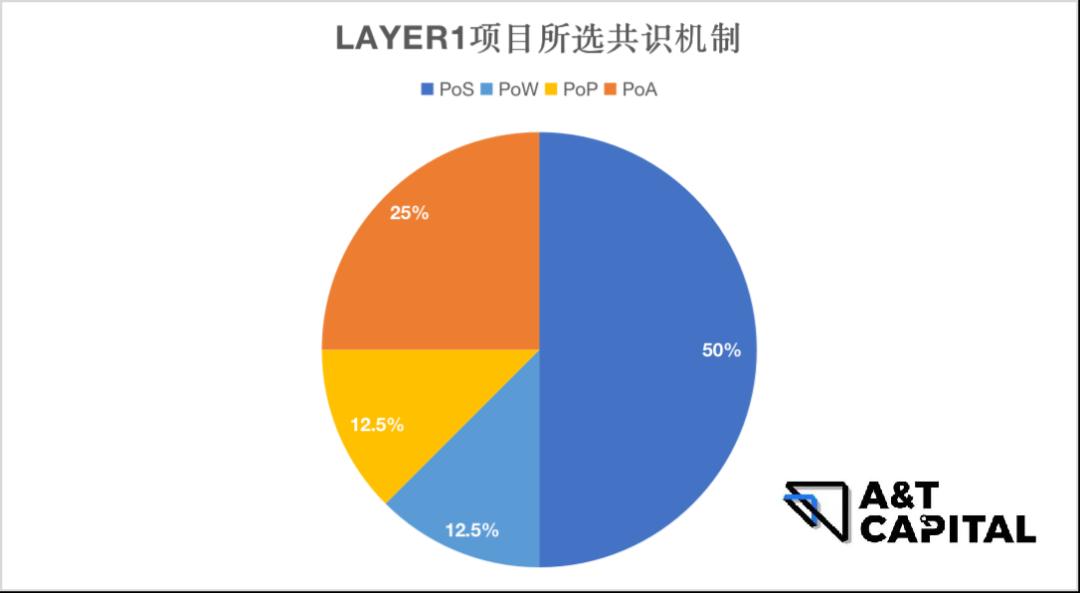

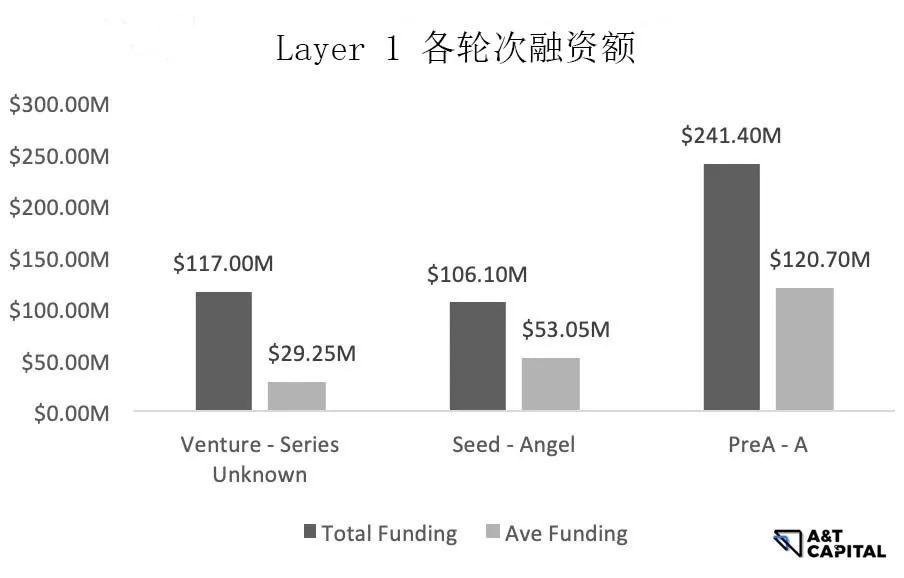

1.1 Layer 1

PoW accounts for a very small proportion, with its financing amount less than 1% of the total financing amount: This indicates that PoW has many issues (high energy consumption, inefficiency in large-scale usage scenarios, and the high hardware costs and competitive environment of PoW lead to capital intensification characteristics in mining, fostering a trend towards centralization), thus capital favors models outside of PoW.

PoS is the best-performing financing category in Layer 1, accounting for about 50% of the total amount, significantly surpassing other categories. From the financing situation, the market is particularly optimistic about PoS Layer 1. PoS has lower energy consumption, higher scalability, and transaction throughput compared to PoW.

PoP (a hybrid model of PoW and PoS): accounts for 22% of the total financing amount.

. PoS is not a perfect solution; the hybrid mechanism combines the benefits of both PoW and PoS.

. It avoids 1. centralization 2. security risks 3. MEV risks 4. DoS risks caused by PoS protocols.

. It avoids the high energy consumption and low performance of PoW.

PoA accounts for about 25% of the financing amount. This model can ensure speed and high performance without sacrificing security. It differs from traditional blockchain operations but provides an emerging blockchain solution that may be very suitable for private blockchain applications.

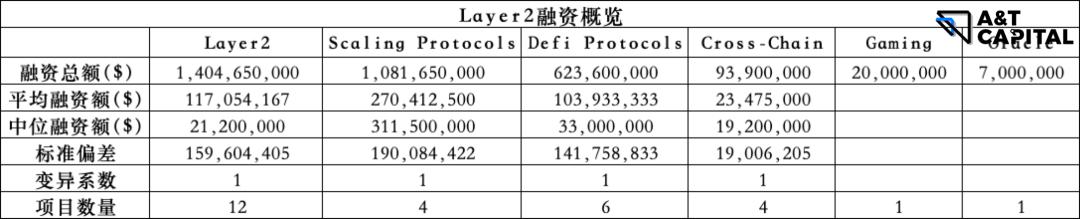

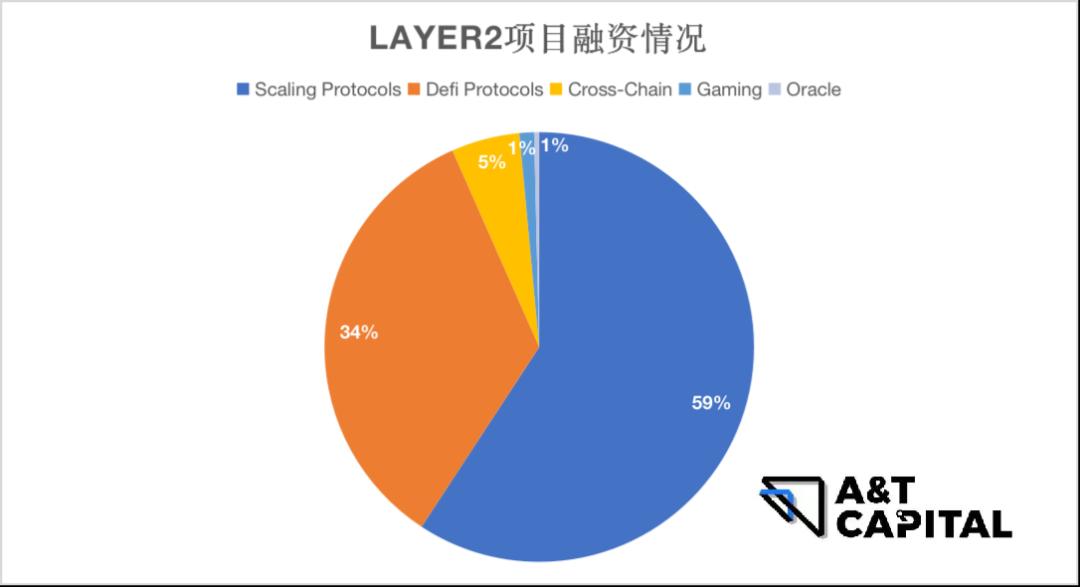

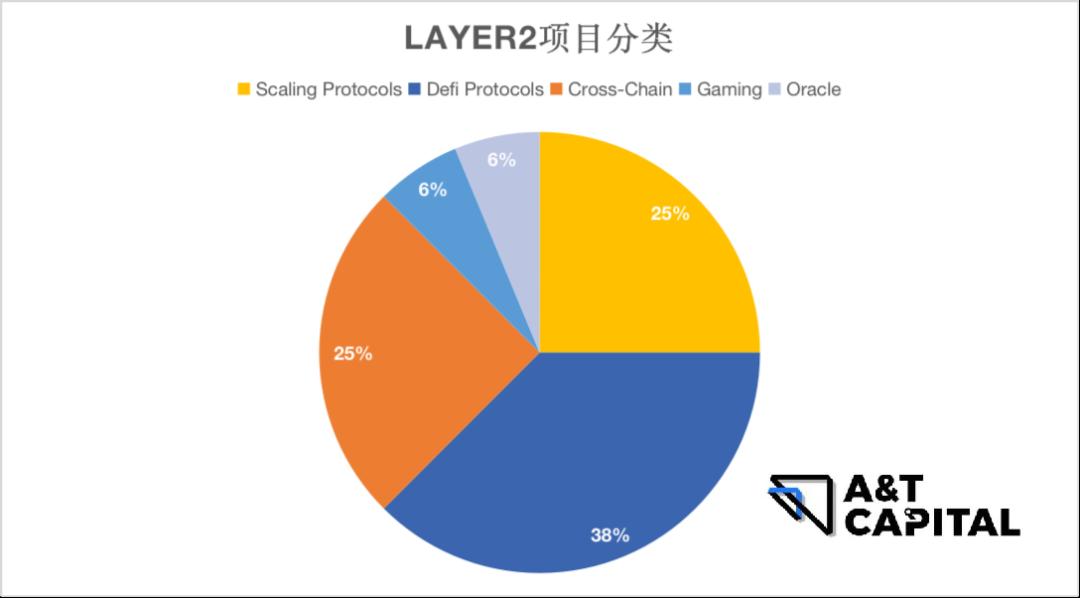

1.2 Layer 2

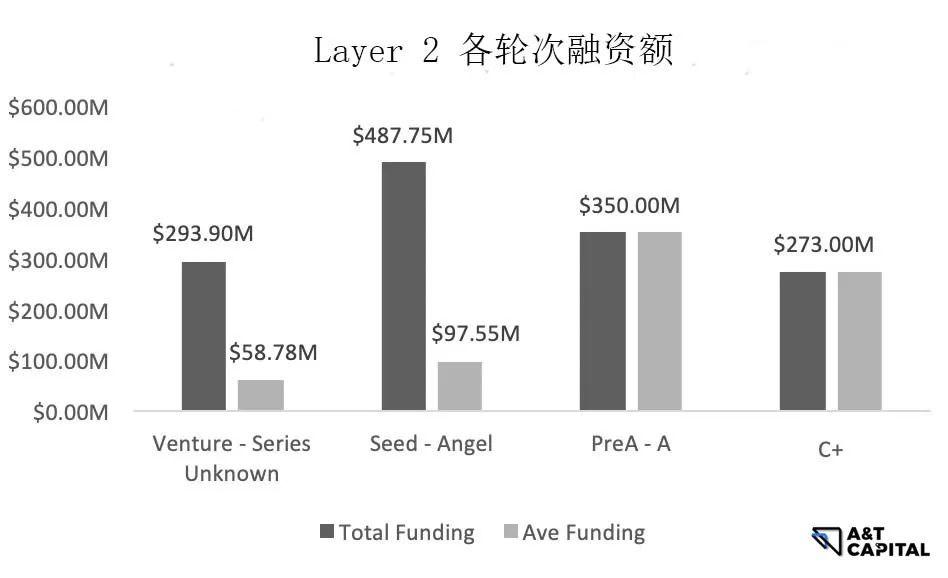

Overall, Scaling Protocols and DeFi Protocols have better financing performance.

Scaling Protocols

. Scaling Protocols: Investment institutions are increasing their bets on the overall track of scaling protocols.

. The market demand for scaling solutions has strengthened due to higher gas fees / TPS / latency.

DeFi Protocols

. The DeFi Protocols track has high overall attention (34%).

. 66% of projects are focused on cross-chain protocols (DEX cross-chain aggregation protocols), but in terms of financing amount, they do not perform prominently, accounting for only 11.5% of the total financing amount.

. In DeFi Protocols, infrastructure financing accounts for 56%, and stablecoin lending protocol financing accounts for 32%.

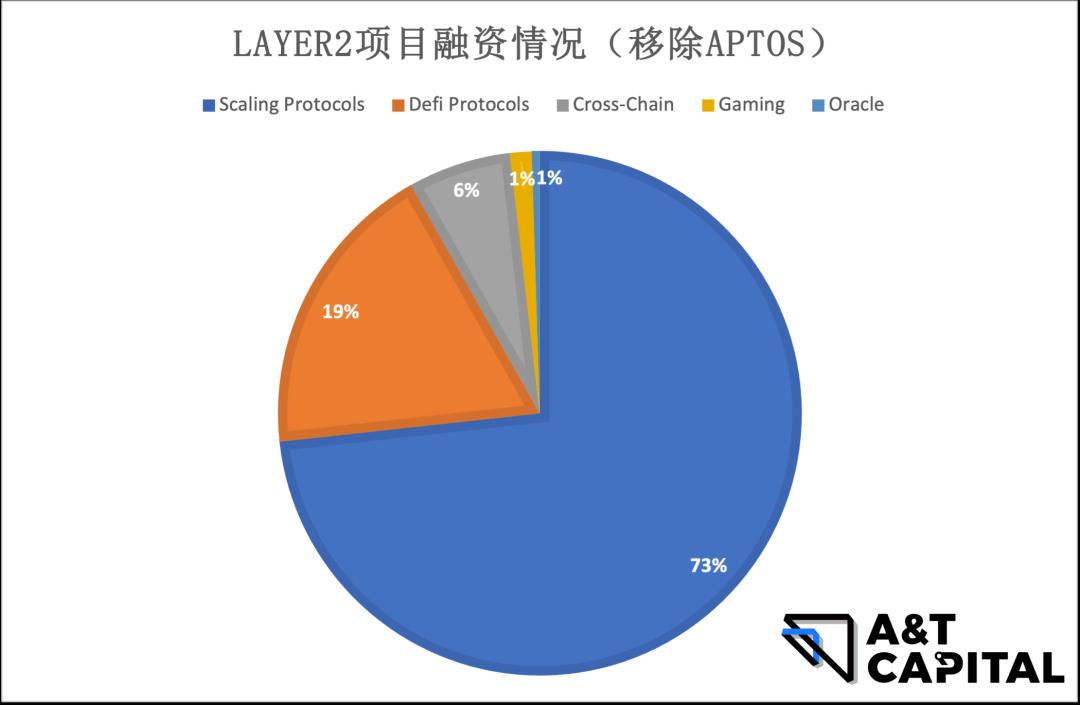

. Aptos is considered an industry alpha and can be viewed as an outlier. Removing Aptos from DeFi Protocols reduces the funding amount proportion of DeFi Protocols to 19%, indicating a cooling trend in the attention towards the DeFi track, while the proportion of Scaling Protocols has reached an overwhelming majority (73%), making it the most popular trend in market attention.

Oracle

Very few projects in the Oracle direction received financing, accounting for 1% of the total financing amount in L2. The reasons may include: 1) The concept of Oracle is not innovative; 2) The use of Oracle is industry-restricted and requires real-world data (i.e., insurance/real estate), while currently popular tracks like GameFi and NFT mostly do not require Oracle.

Gaming

GameFi has higher requirements for transaction speed and gas fees compared to other tracks like DeFi. General Layer 2 provides potential scaling solutions, but in this research, there are projects specifically designed for GameFi. This may indicate that GameFi-type applications have specific needs that general Layer 2 cannot perfectly address, and this direction is worth further research.

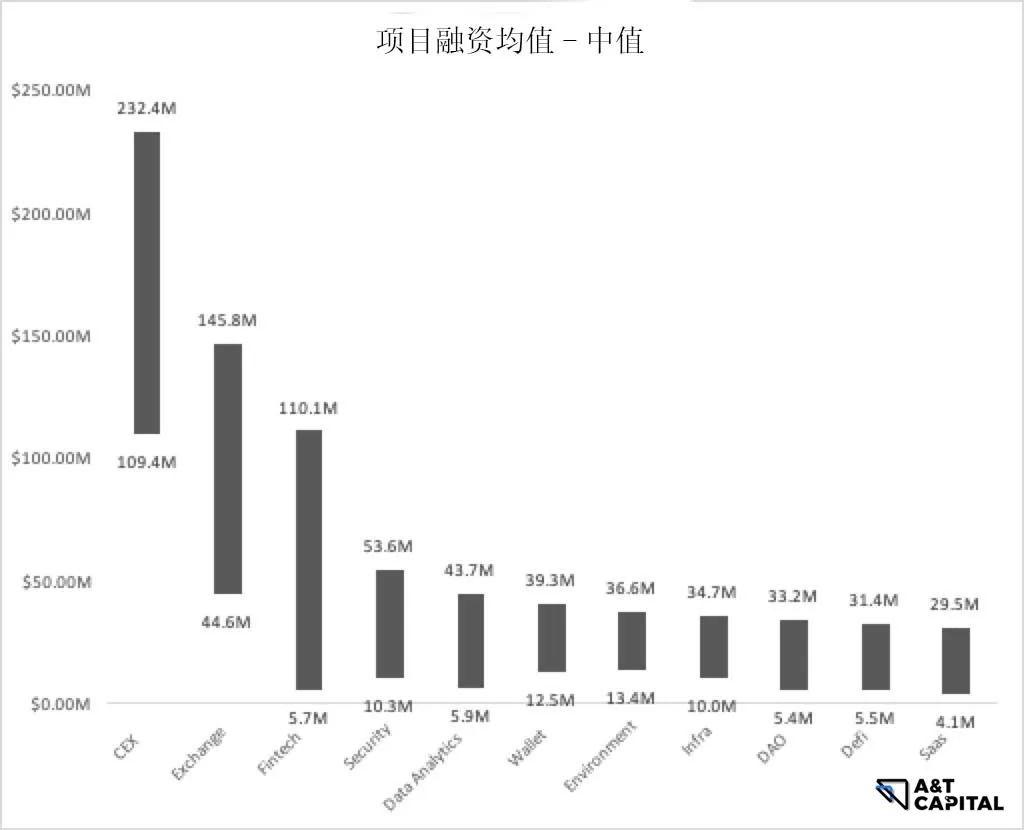

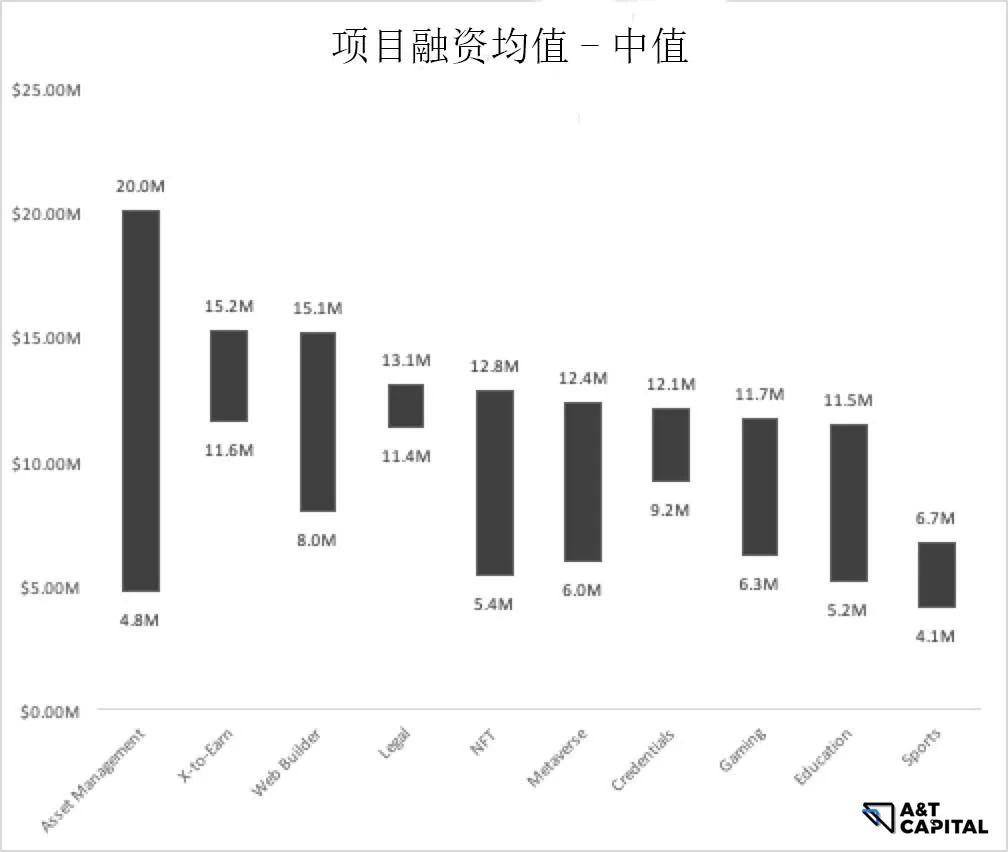

1.3 Applications

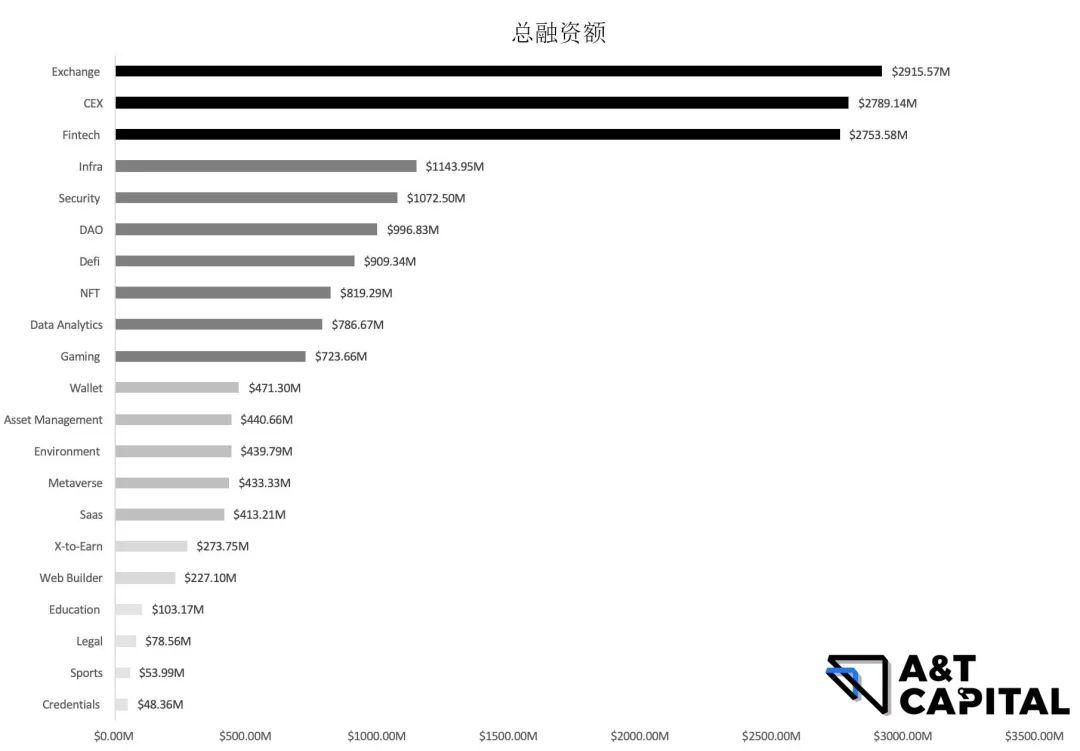

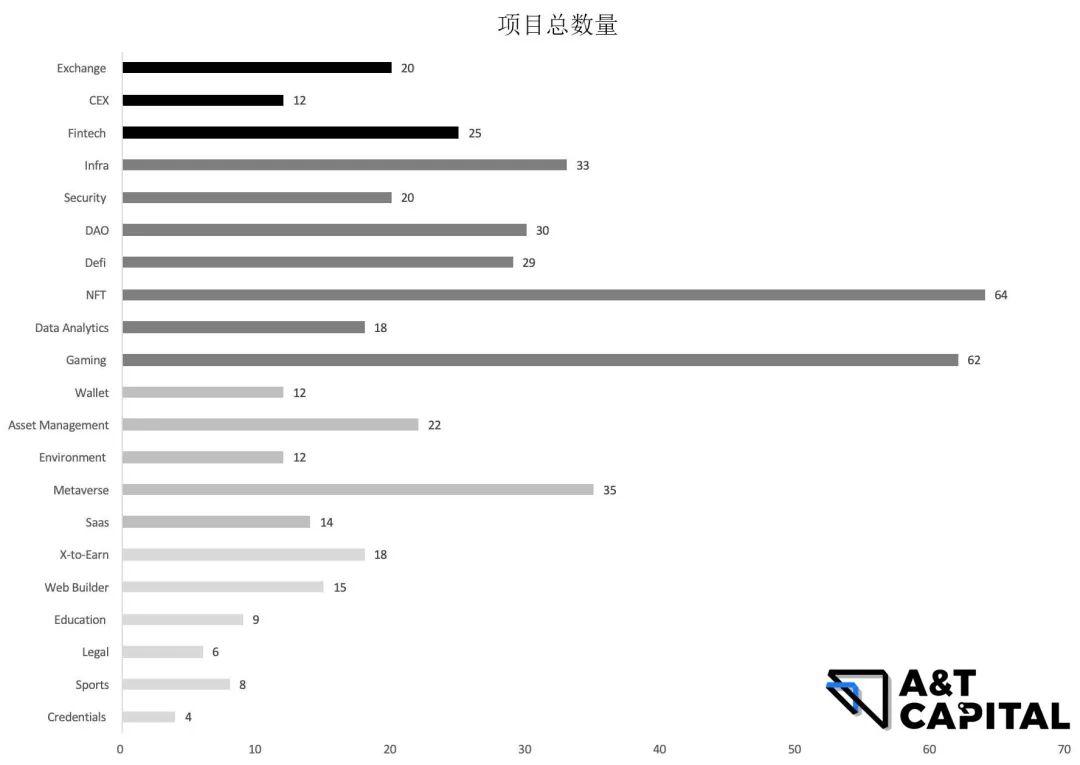

As seen in the above figure, exchanges and fintech account for 47% of the financing targets, while the rest are all below 6%, with a relatively even distribution.

Major Trends (Overall)

The top three categories by financing amount: exchanges, centralized exchanges, fintech.

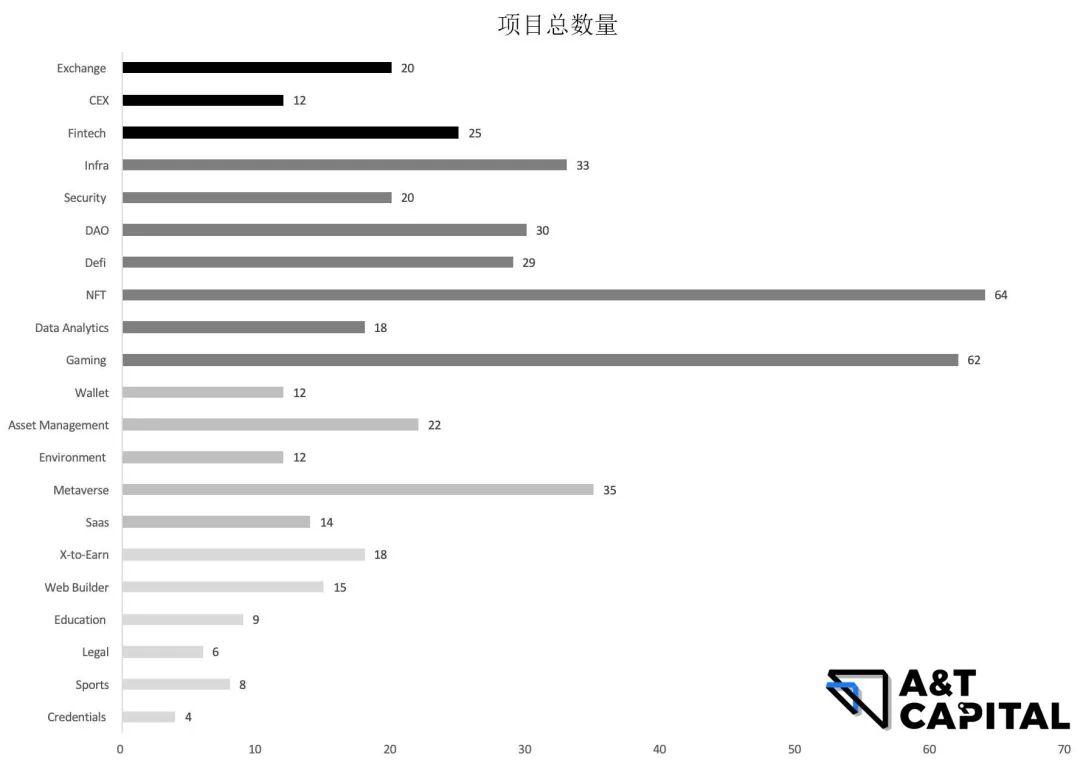

The top three categories by number of financing projects: NFT, gaming, metaverse.

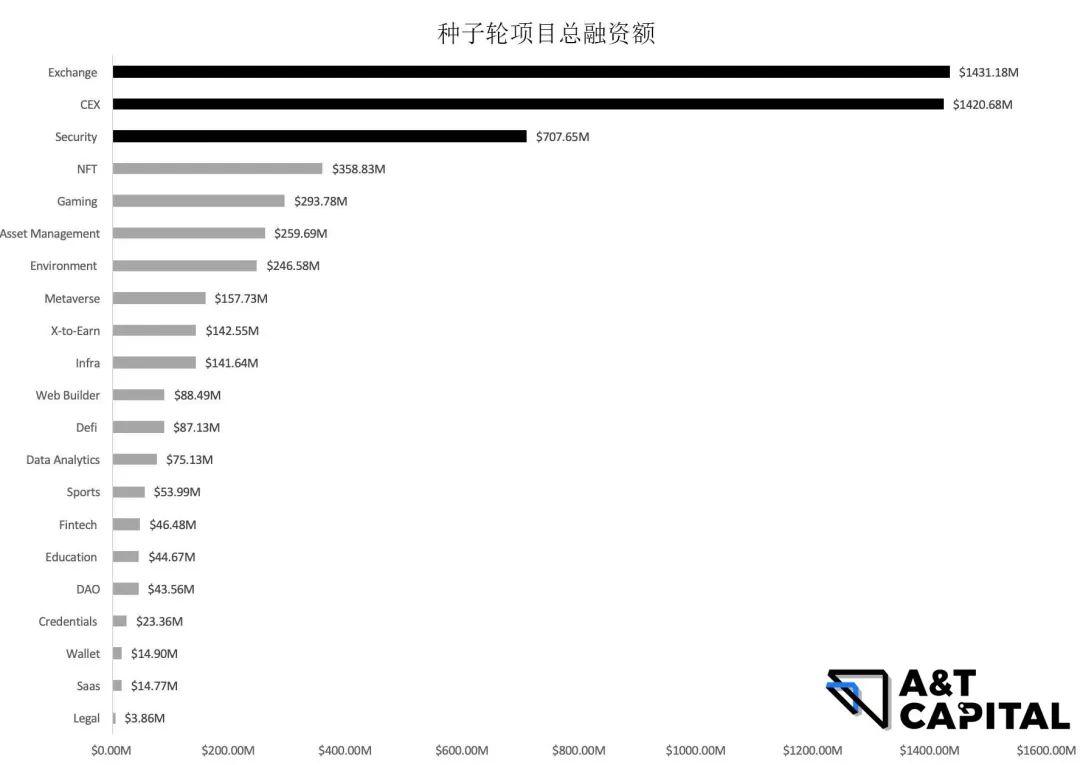

New Trends (Pre-seed - Pre-A round)

As shown in the figure, the top three categories by number of seed round financing projects: gaming, NFT, metaverse. The top three categories by seed round financing amount: exchanges, centralized exchanges, security.

As shown in the figure, the top three categories by number of seed round financing projects: gaming, NFT, metaverse. The top three categories by seed round financing amount: exchanges, centralized exchanges, security.

1.4 Summary

Layer 1 - PoS and hybrid chains are the main popular trends, with increasing attention on hybrid chains, indirectly proving that everyone is concerned about the potential security issues of PoS and is looking for solutions that can balance security and efficiency.

Layer 2 - General scaling protocols are the main popular trend, with new directions including industry-specific Layer 2 chains.

Application - Both major trends and new trends focus on projects that can circulate in the secondary market in the short term, with a new major direction being security.

2: Alpha & Beta Trends

2-1 Alpha

First, we define Alpha:

The characteristic of the Alpha market is financing driven by trading. Projects with Alpha characteristics need to significantly outperform other projects within the same Layer category. The Alpha projects we are looking for in this article need to meet the criterion of total financing exceeding twice the average financing of their respective track.

2-1.1 Layer 1

As shown in the figure, no alpha is seen in Layer 1.

As shown in the figure, no alpha is seen in Layer 1.

2-1.2 Layer 2

As shown in the figure, there is Alpha in the Seed-Angel stage in Layer 2, with Polygon being the alpha project in this stage. Other stages such as Pre-A, B-C, and C+ do not have Alpha.

As shown in the figure, there is Alpha in the Seed-Angel stage in Layer 2, with Polygon being the alpha project in this stage. Other stages such as Pre-A, B-C, and C+ do not have Alpha.

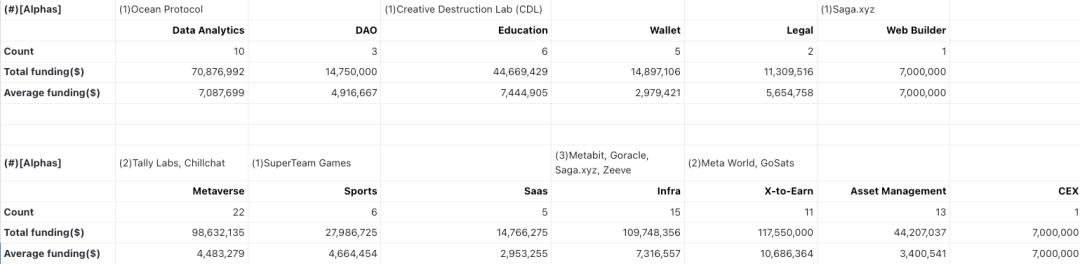

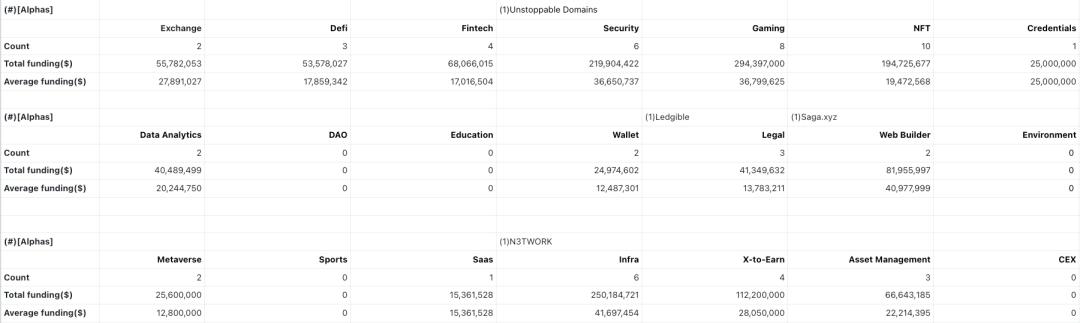

2-1.3 Application Layer

- Seed-Angel

- Pre-A

- B-C & C+

2-2 Beta Define Beta:

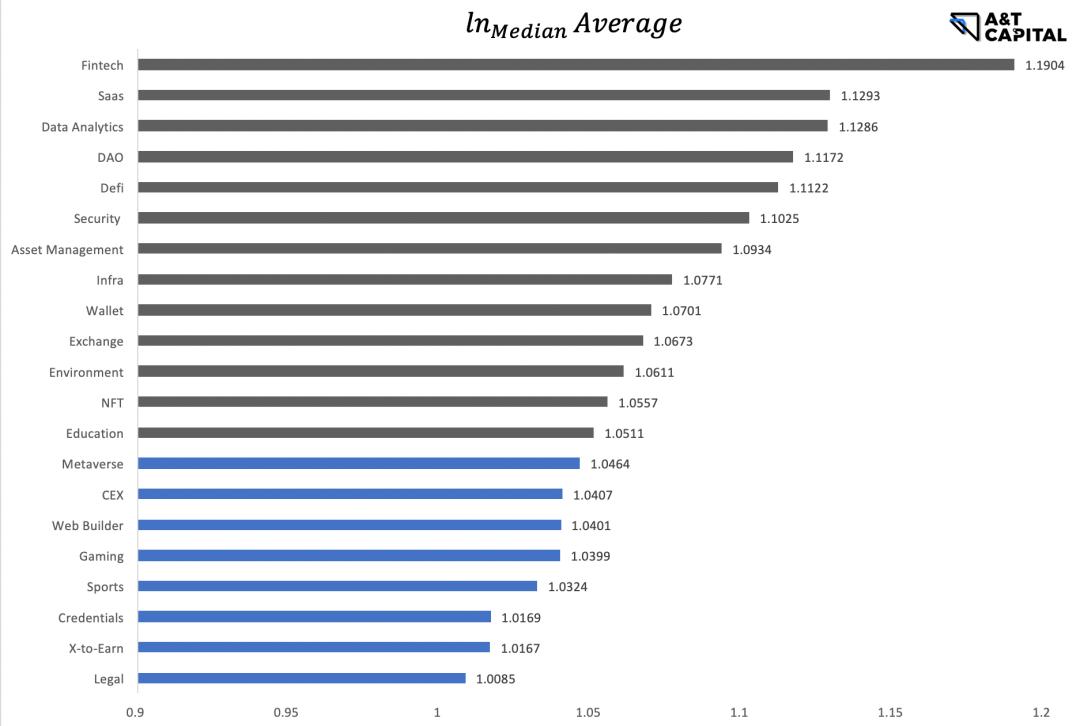

The characteristic of the Beta market is market-driven financing. Beta measures whether the market is optimistic about a particular industry/technology category. Tracks with Beta attributes generally have good financing. A lower coefficient of variation (CV) indicates lower financing dispersion in the track, reflecting the market's Beta attributes. We further cross-verify using the difference between the average and median. Markets with low CV and a small difference between average and median better reflect Beta characteristics. We use CV < 1.5 and log(average)/log(median) < 1.05 for judgment.

2-2-1. Layer 1 & Layer 2

The overall number is too small to have statistical significance. Overall, Layer 1 & Layer 2 belong to high financing amounts and hot tracks. When categorized by technology flow, the financing amounts do not differ significantly.

2-2-2. Application

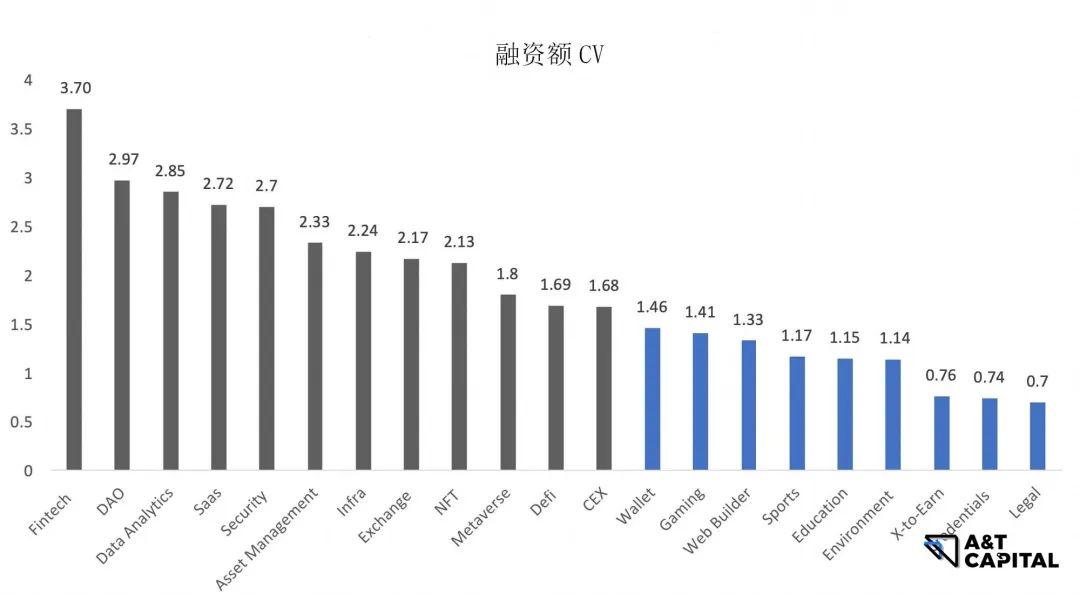

As seen in the above figure, from the perspective of low dispersion below CV 1.5, the beta market can be roughly defined as Wallet, Gaming, Web Builder, Sports, Education, Environment, X-to-earn, Credentials, and Legal. However, the data volume of one quarter may affect the credibility of CV, so we use AVE-MEDIAN for cross-verification, as follows.

As seen in the above figure, from the perspective of low dispersion below CV 1.5, the beta market can be roughly defined as Wallet, Gaming, Web Builder, Sports, Education, Environment, X-to-earn, Credentials, and Legal. However, the data volume of one quarter may affect the credibility of CV, so we use AVE-MEDIAN for cross-verification, as follows.

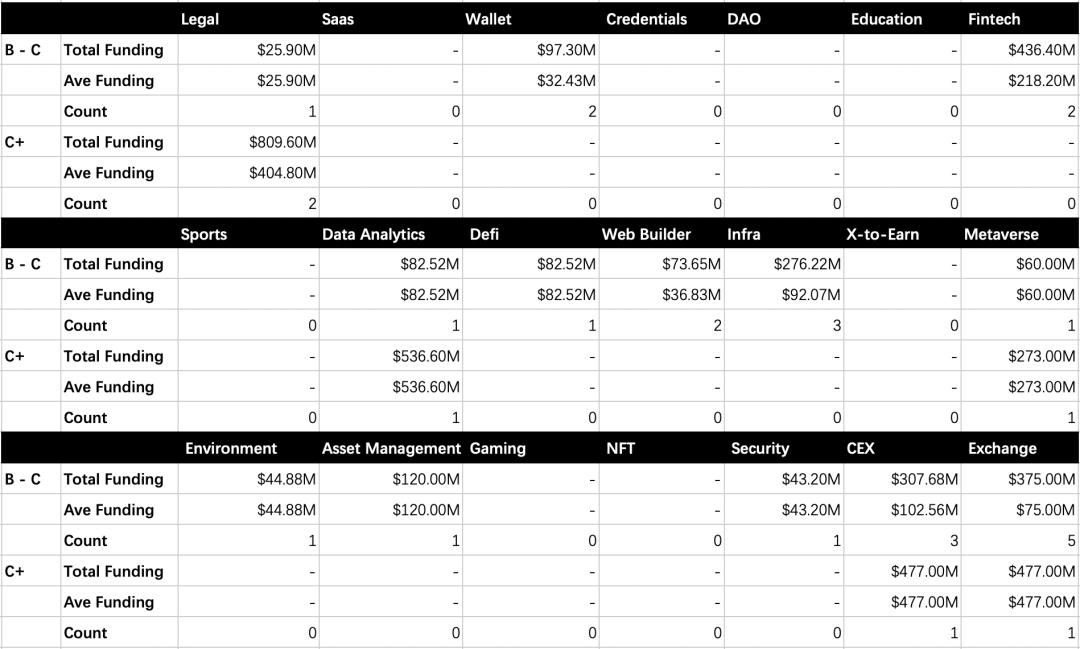

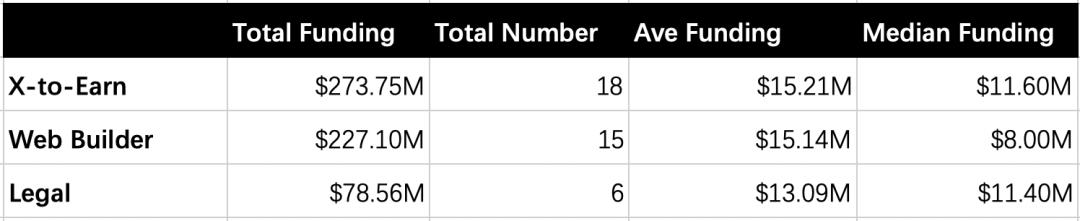

As seen in the above figure, X-to-earn, Web Builder, and Legal are verified as beta. Their specific financing data is as follows.

As seen in the above figure, X-to-earn, Web Builder, and Legal are verified as beta. Their specific financing data is as follows.

2-2-3. Summary

2-2-3. Summary

In the application layer, through the comparison of the two methods of calculating beta, we conclude that X-to-earn, Web Builder, and Legal have beta attributes.

3: Preferences of Some Leading Institutions

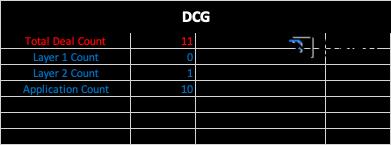

3.1 Digital Currency Group

DCG has invested in 10 projects. There is no preference in stages, with investments from seed to series F. The Layer 2 project invested by DCG is Polygon, while the other 9 projects are all applications. Among the 9 applications invested, the preferences from high to low are:

Wallet, which also includes built-in wallets in exchanges.

Security, including code auditing and security testing.

Analytics tools, mainly for data analysis, tracking, and alerts.

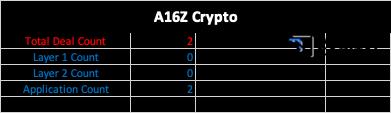

3.2 A16Z Crypto

A16z crypto has invested in 2 application projects, both in the seed round. Both projects are platform-type projects:

A16z crypto has invested in 2 application projects, both in the seed round. Both projects are platform-type projects:

Creator platform gathers creators and helps them NFT their original works.

NFT pledging platform allows players who cannot access certain games due to high barrier NFTs to successfully access these games through this NFT lending platform, ultimately owning these NFTs after completing all payments on the platform.

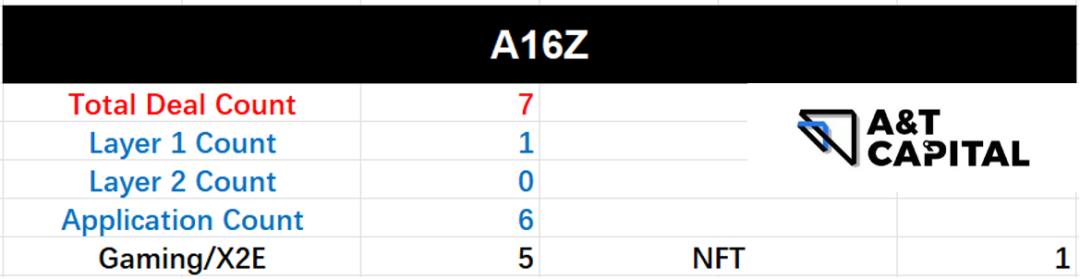

3.3 A16Z

A16Z has made 7 investments, including 1 Layer 1 project - Aptos, and 6 application projects.

A16Z has made 7 investments, including 1 Layer 1 project - Aptos, and 6 application projects.

Among the 6 applications invested, the rounds include 2 seed rounds and 4 series A, with directions including:

5 gaming/x-to-earn

1 NFT project

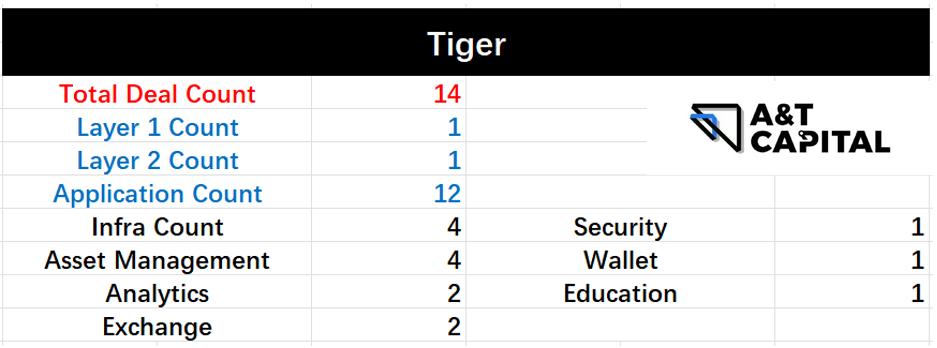

3.4 Tiger

Tiger has made 14 investments, including 1 Layer 1, 1 Layer 2, and 12 applications. The Layer 1 project is Aptos, and the Layer 2 project is Polygon. In terms of investment stages, the 14 projects span from seed to series D, with no obvious stage preference.

Among the 12 applications invested, the preferences from high to low are:

4 Infra projects, including staking service, DID, deployment platform.

4 asset management.

2 analytics and 2 exchanges.

3.5 Lightspeed

Lightspeed has made 7 investments, all in applications. In terms of investment stages, they have invested from seed to series D, with no preference in stages.

Among the 7 applications invested, the preferences from high to low are:

- 2 asset management

- 2 wallets

- 2 exchanges

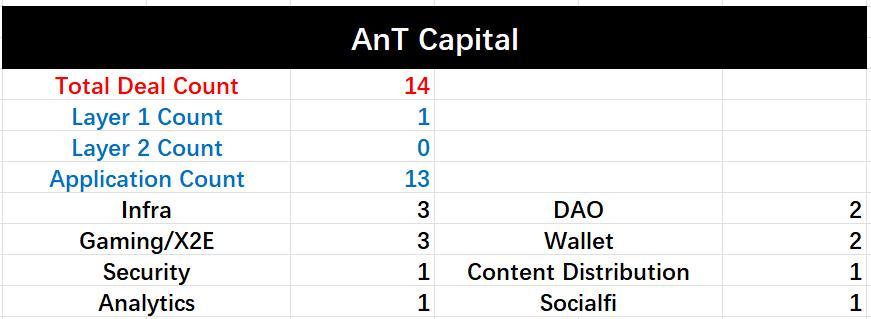

3.6 A&T Capital

A&T Capital has made 14 investments, including 1 Layer 1 - Mysten Labs. There is a clear preference for early-stage investments, including 7 seed rounds and 2 A rounds.

Among the 13 applications invested, they include:

3 infrastructure

3 gaming/x2e

2 wallets

2 DAO tools

3.7 Paradigm

Paradigm has made 4 investments, all in applications. All 4 investments are in the seed round. Among the 4 applications invested, they include NFT marketplace, gaming/x2e, social, and metaverse.

3.8 Dragonfly

Dragonfly has made 12 investments, including 1 Layer 2 cross-chain bridge, while the other 11 are all applications. In terms of investment rounds, they mainly focus on early seed rounds and growth stages. Among the 12 applications invested, the preferences from high to low are:

5 gaming

3 asset management

2 social

3.9 Sequoia

Sequoia has made 5 investments, including 1 Layer 2 - Starkware, while the other 4 are all applications. In terms of investment rounds, there is a clear preference for later stages, including one ICO round project. Among the 4 applications invested, they include:

2 metaverse

1 asset management

1 insurance

Conclusion

In this article, we reviewed the projects that received institutional fund investments in the crypto industry from May 2022 to August 2022, summarizing the following major trends:

From the investment stage perspective, funds in the market are more willing to invest in very early or later-stage projects during the bear market; exit strategies mainly focus on projects that can enter the secondary market in the short term, with an observable increase in investments in chain games and crypto asset management projects.

From the investment direction perspective, Layer 1 is mainly focused on PoS, with a significant increase in attention to hybrid chains; Layer 2 is mainly focused on general scaling, with increased attention to industry-specific chains; the application layer is primarily focused on gaming and NFTs, with a noticeable increase in attention to security tracks.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles