IOSG: The Optimal Deconstruction of Uniswap Governance Token Valuation Model

In order to optimize the value of the UNI token, governors should not limit themselves to a binary choice.

In order to optimize the value of the UNI token, governors should not limit themselves to a binary choice.Author: Momir, IOSG Ventures

Investors often use relative valuation/comparative valuation methods to assess early-stage projects (such as comparing a project's P/S, P/E, etc.), which is usually the most direct and effective way to estimate a project's/company's total revenue. However, when we evaluate AMM projects like Uniswap in the crypto space, a challenge arises: there is currently no universal consensus in the market on what kind of revenue structure should be used to value the tokens of a decentralized AMM trading protocol. This is because, compared to traditional business entities, the stakeholders involved in revenue distribution for decentralized protocols may be more numerous and complex.

Currently, there are basically two main approaches:

● Classifying the total fees charged to liquidity providers as the total revenue of the protocol.

● Not counting the fees of liquidity providers as the total revenue of the protocol, with the total revenue being a percentage (x%) of the total fees charged on the platform.

If we directly apply the accounting practices of traditional finance, we would arrive at the argument that total fees should equal total revenue. However, this is unfair in common sense, as a large portion of this revenue actually does not belong to the protocol but to the liquidity providers. For example, using deductive reasoning, if a bank considers the interest income of depositors as the top line revenue, then a lending protocol could consider the interest income of LPs as the top line revenue, and thus AMMs could make a similar analogy regarding the total fees charged by the protocol. On the other hand, when benchmarking AMM exchanges against CLOB exchanges, this accounting could lead to some inconsistencies.

Evaluating AMMs Against CLOBs

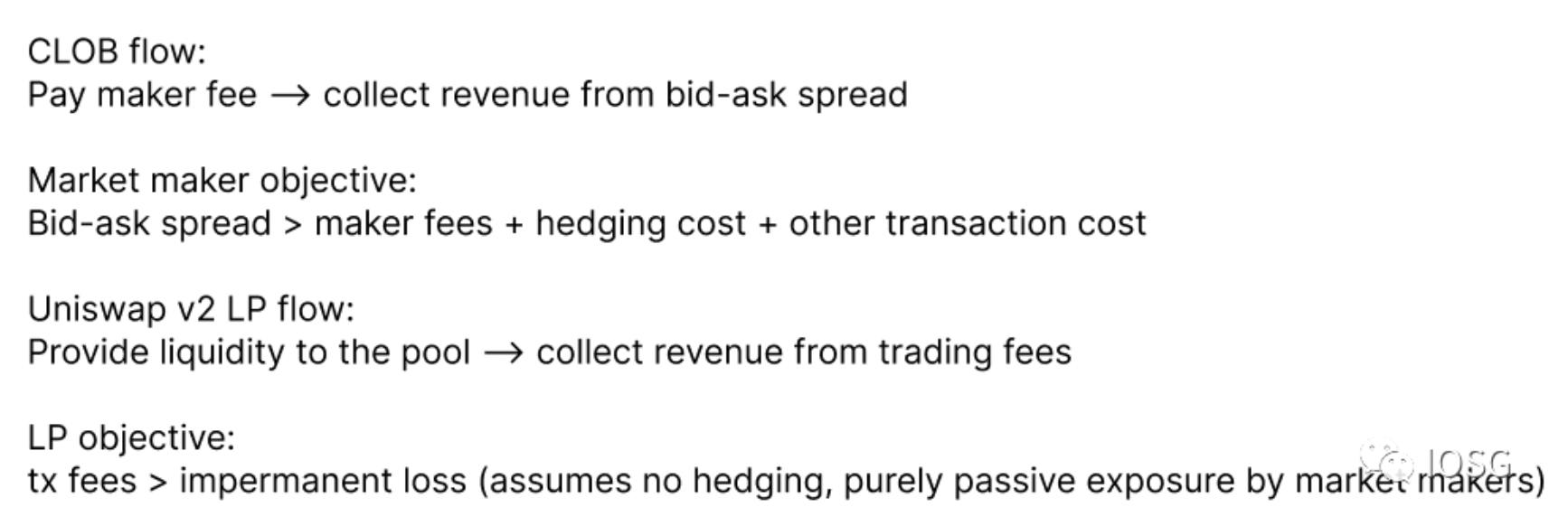

For Uniswap v2, the main premise of the design is that all LPs have a uniform passive exposure. The only revenue comes from a fixed 0.3% trading fee, rather than earning from the bid-ask spread like liquidity providers/market makers in order book exchanges.

Fundamentally, the bid-ask spread is a potential trading cost that users pay beyond the trading fees on the exchange. Therefore, the bid-ask spread of market makers in CLOBs can be compared to the trading fees of LPs in Uniswap v2. If we consider market makers as external personnel to the exchange, their income should not be counted as the exchange's revenue. Token holders could potentially receive 10-20% of the total fees charged to liquidity providers as the net income of the protocol; this is the case for Sushiswap, the most famous fork of Uniswap. In other words, 25 basis points of each trade on the Sushiswap DEX are allocated to liquidity providers, while 5 basis points (16.67% of total fees) are allocated to SUSHI stakers.

Uniswap also has the opportunity to introduce fees, which could generate economic value for UNI token holders.

Market Consensus

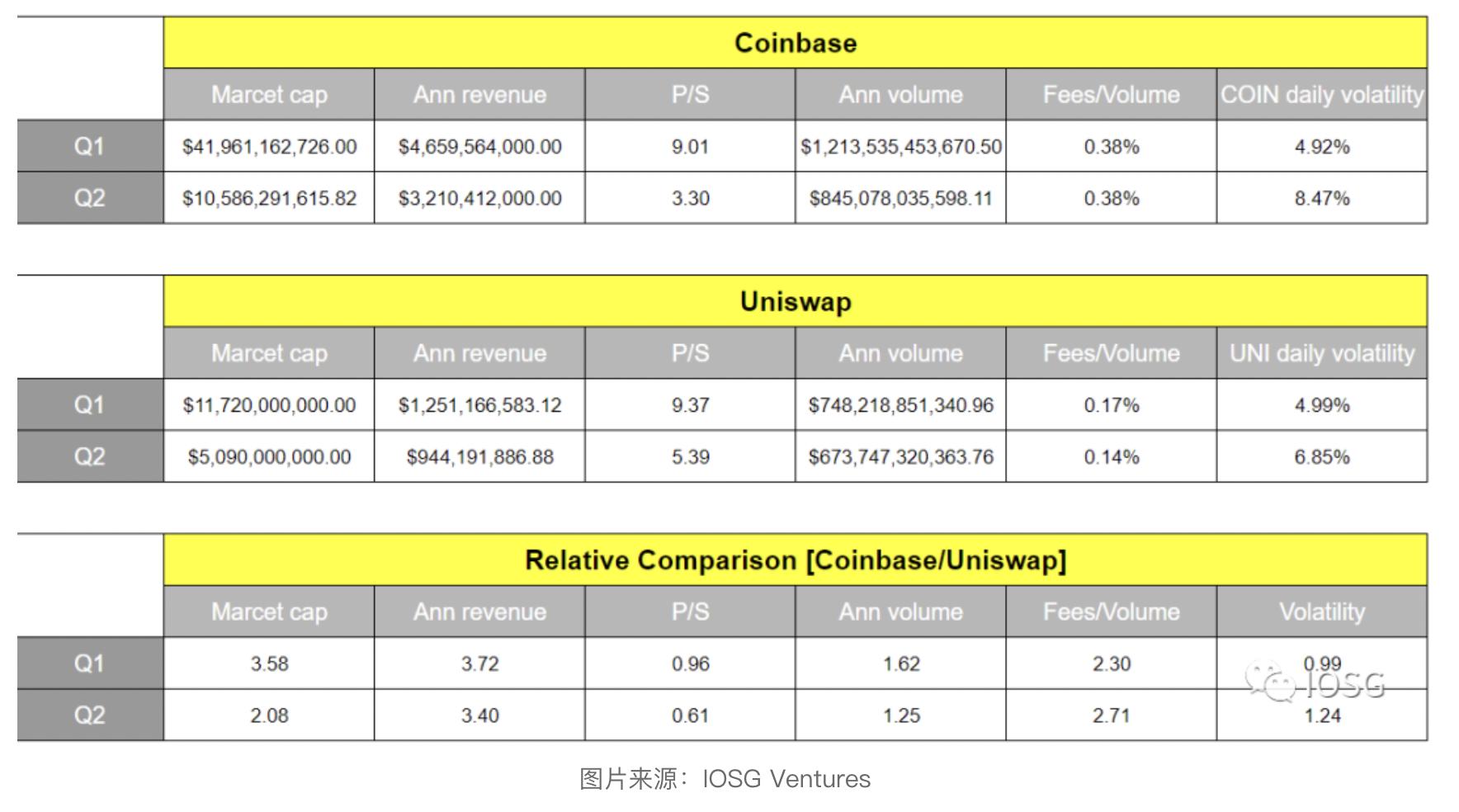

However, if we observe market pricing, it seems that the market indeed does not recognize the different revenue structures between AMMs and CLOBs. As shown in the figure below, it compares the total revenue of Uniswap (total fees charged to liquidity providers) and Coinbase using similar multiples, despite the obvious structural differences between the two.

Nevertheless, if we adjust the P/S calculation, defining total revenue as 16/17% of the total fees charged to LPs (assuming this does not adversely affect trading volume), the annualized revenue would be approximately $160 million ($945 million * 0.17), with a P/S multiple of about 32 ($5B/$160 million), which is 6 times higher than in the table above. While Uniswap is a leading blockchain application, does this justify a multiple of 32 vs. 3.3 that is 10 times larger than Coinbase? Or does this model not provide an overall picture?

Diving Deeper

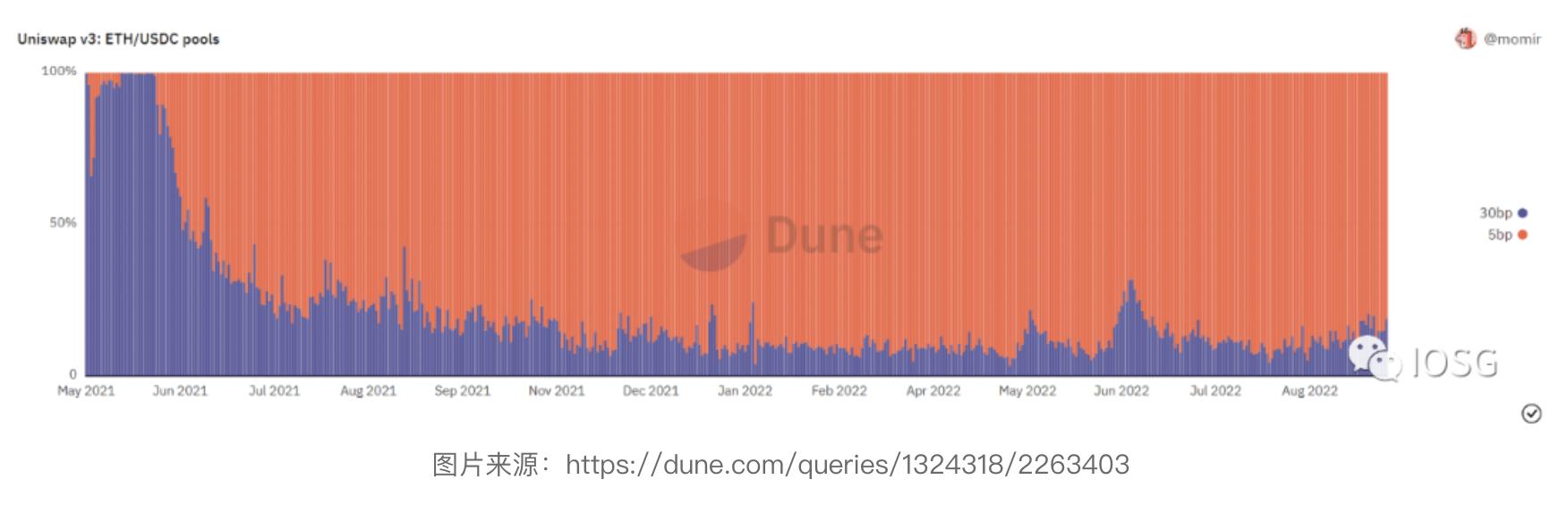

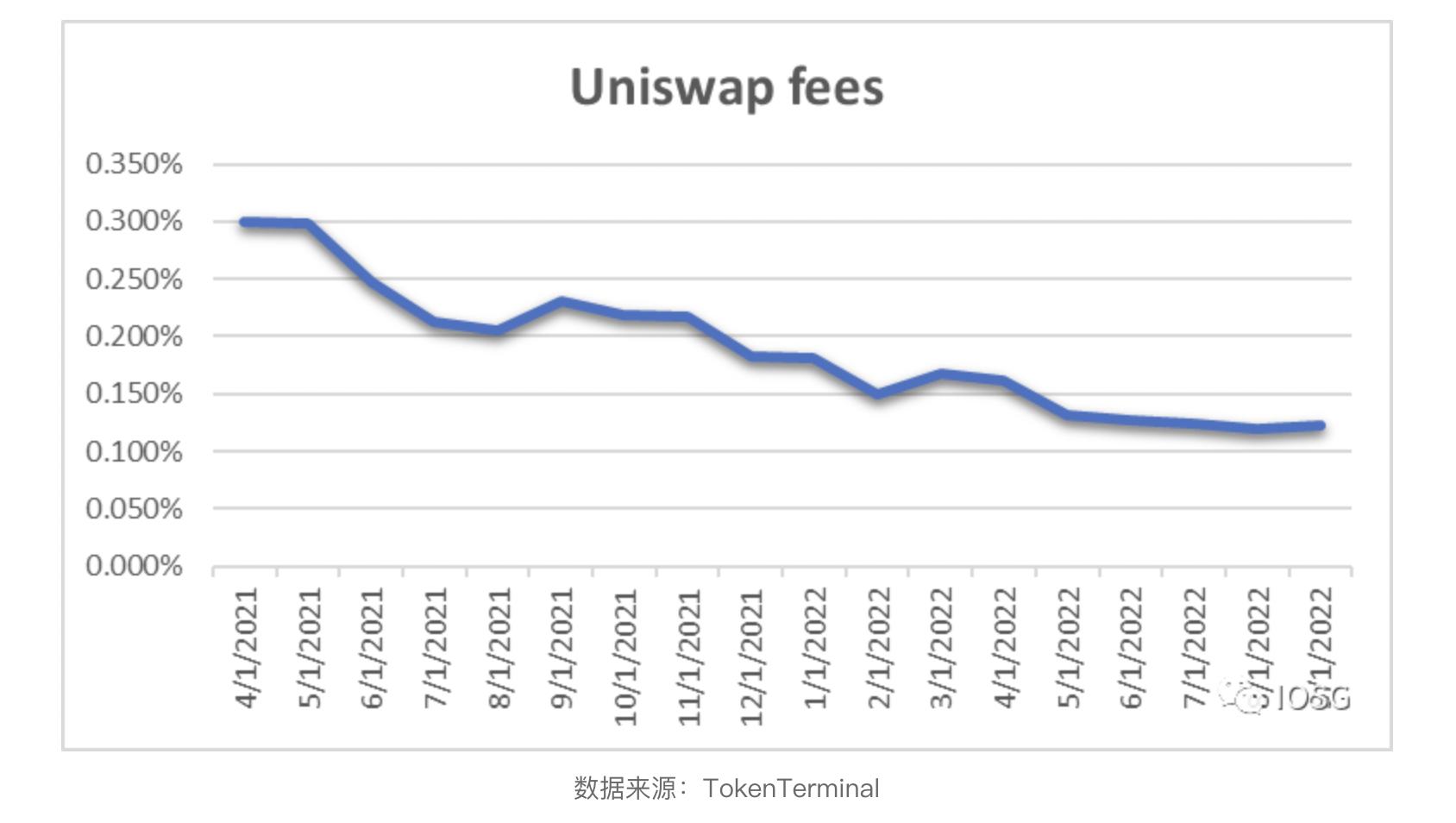

In 2021, Uniswap launched v3, significantly changing the way LPs interact with the platform. That is to say, in v3, liquidity providers do not have to adhere to a uniform distribution and have the opportunity to manage their exposure more actively. This has led to an increasing number of 5bps and 1bp pools, where liquidity providers/market makers can balance lower trading fees with more active management and potentially profit from the bid-ask spread.

While using total fees as a basis for multiples in AMMs like Uniswap v2 may lead to overpricing of the project, in a model similar to Uniswap v3, it could also lead to the completely opposite result. For example, it is possible that trading volume on the exchange increases, but overall more trades come from low bp pools, causing fees to stagnate.

Optimizing the Value of UNI

Recently, the accumulation of value for the UNI token has become one of the most discussed topics in the DeFi space. Community members proposing to open the fee switch have suggested a pilot program, where selected liquidity pools would introduce a 10% fee, cutting into the income of liquidity providers. On the other hand, opponents of the proposal argue that if Uniswap rushes to monetize its position, it could potentially lose its competitive edge in a possible fork. However, to optimize the value of the UNI token, governors should not limit themselves to a binary choice.

The goals of the Uniswap DAO should be:

- Maximize trading volume.

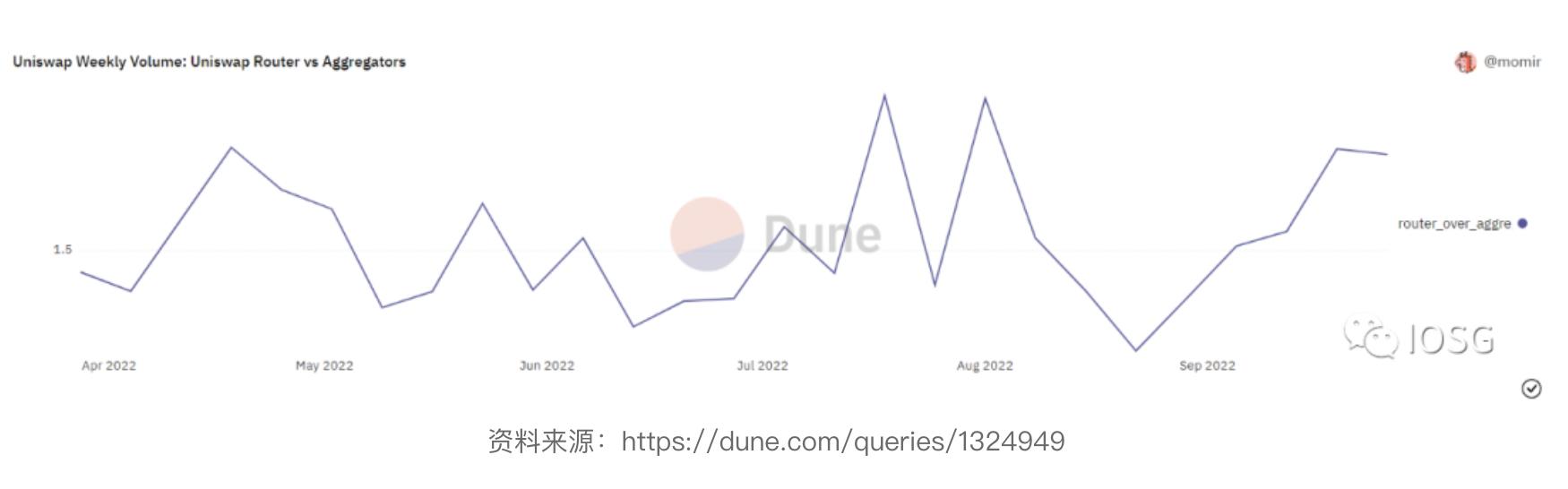

- Engage with users: Only by establishing direct connections with users can Uniswap reduce their price sensitivity. That is to say, a significant portion of Uniswap's trading volume comes from DEX aggregators, which provide orders for a highly liquid user base that focuses solely on obtaining the best price and has no loyalty to any specific exchange. As DEX aggregators grow, Uniswap has the potential to compete with other major sources of liquidity while monetizing the relationship between aggregators and users.

- Introduce fees beyond market maker fees at the protocol level: As shown in the comparison table above, the fees charged by Coinbase are 2.7 times those of Uniswap, indicating that there may be significant opportunities for Uniswap to increase fees beyond existing market maker fees and funnel them into the DAO treasury. The extent of these fees depends on the above perspectives—loyalty of their user base, or perhaps more importantly, the loyalty of their LPs (who are constantly being arbitraged by market makers). The increasing share of low-fee pools opens up greater space for protocol-level charges. Experimenting with non-uniform charges for different tiers of traders and using machine learning to classify arbitrageurs could be quite interesting.

Top-Down Approach

Given all of the above, how should we comparatively benchmark decentralized hybrid exchanges like Uniswap against CLOB exchanges, and even regulated CLOB exchanges like Coinbase? The most neutral benchmark available is the trading volume generated by these platforms. What kind of multiple is relatively reasonable when comparing one platform to another depends on a range of factors, such as:

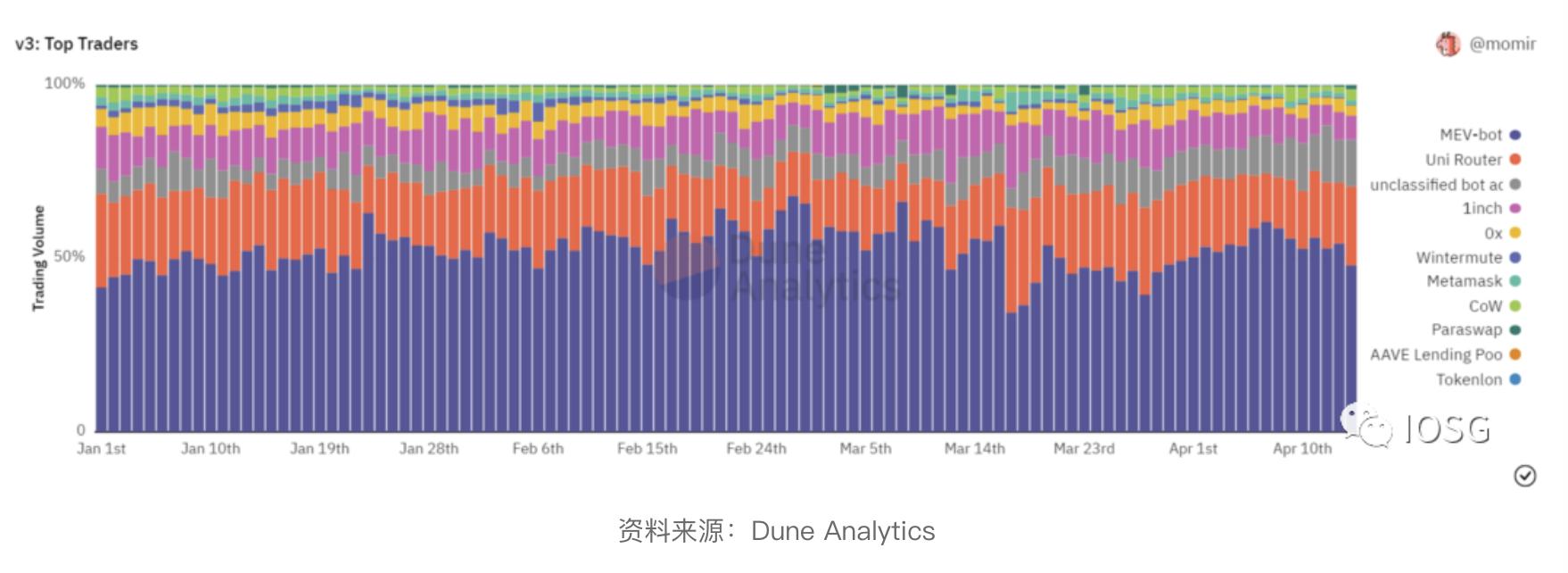

- Quality of trading volume: a) If most of the trading volume in Uniswap v3 is completed by MEV bots, why is this the case? Part of the reason is sandwich attacks targeting retail investors, but also due to inefficient liquidity providers being continuously arbitraged. If a significant portion of Uniswap's trading volume is caused by immature liquidity providers, how sustainable is this dynamic? b) Is the trading volume incentivized?

- Ability to levy protocol fees: Coinbase has over 100 million registered real-name users, while "only" 5.5 million different addresses have ever interacted with Uniswap on Ethereum. Additionally, Coinbase may have a stickier user base, while a significant portion of Uniswap's trading volume is obtained through aggregators.

- Operational efficiency and leadership: Coinbase has thousands of employees, while Uniswap's main contributor, Uniswap Labs, has 70-80 employees.

- Arguments for the importance of narrative and decentralization, belonging to a specific ecosystem, and the superiority of design.

- Trigger events: Are there opportunities to expand into new verticals (such as Coinbase expanding into staking, non-custodial wallets, etc.), how profitable are these businesses, and what is the likelihood of success?

- Risks: The relative volatility of each token may be a good representation of risk; however, adjustments need to be made based on factors such as token illiquidity, potential massive sell pressure from upcoming unlocks, and specific regulatory risks. In the upcoming articles, we will further elaborate on the issue of risk premiums.

Risk warning

Risk warning Risk warning

Risk warning