Interpreting the HKEX Report: The Development of ETFs and the Global Financial Market Virtual Asset Ecosystem

ETFs, as a type of fund that tracks changes in a "benchmark index" and is traded on stock exchanges, can also use virtual assets as the underlying, thereby compliantly launching "virtual asset ETFs."

ETFs, as a type of fund that tracks changes in a "benchmark index" and is traded on stock exchanges, can also use virtual assets as the underlying, thereby compliantly launching "virtual asset ETFs."Source: TechFlow Deep Tide

In April 2023, the Hong Kong Stock Exchange officially released a research report titled "The Development of ETFs and the Global Financial Market Virtual Asset Ecosystem."

As a highly influential securities exchange in both domestic and global financial markets, the Hong Kong Stock Exchange's research and practice on virtual assets are representative and referential, to some extent even reflecting traditional finance's attitude towards the crypto world and feasible compliant participation methods.

Among them, ETFs, as a type of fund that tracks changes in a "benchmark index" and is traded on a stock exchange, can also use virtual assets as the underlying, thus compliantly launching "virtual asset ETFs"—this is currently an important way for the Hong Kong Stock Exchange to connect with digital currencies.

In this report, the topics discussed are not limited to the concept of ETF products themselves, but also cover the development of global virtual assets and their regulatory systems, market performance of virtual asset ETFs around the world, the evolution of local crypto policies in Hong Kong, and the current status of Hong Kong ETF products; the comprehensiveness of the data and the richness of the information make us feel that Hong Kong is ready to embrace the crypto world.

Deep Tide Research Institute has appropriately condensed, reordered, and interpreted the report, extracting its core viewpoints for reference and learning.

I. A Few Days Apart: From Geek Experiments to Alternative Assets, Overview of Scale, Volatility, and Policies

Editor’s Note: The original report's first part spent considerable time introducing the concept of Web 3.0 and the types and classifications of crypto assets, which we have removed, directly entering the market insights section.

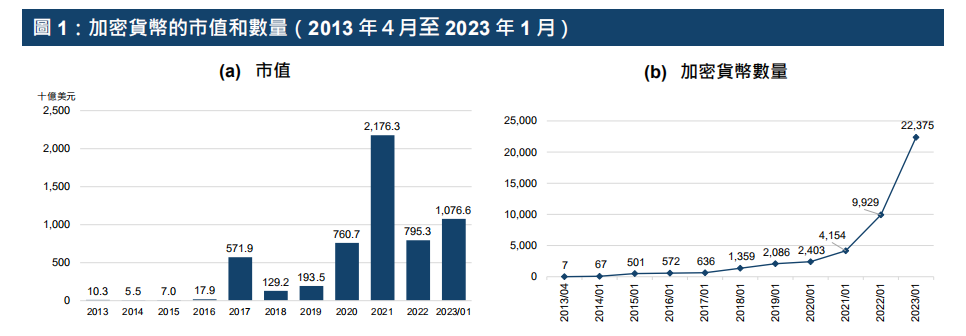

In terms of total volume: The expansion of the market capitalization of the crypto market over the past three years may have gradually attracted the attention of the Hong Kong Stock Exchange:

The market capitalization of virtual assets has grown from $10.3 billion in 2013 to $1,076.6 billion in January 2023;

The number of cryptocurrencies has significantly increased from 7 in April 2013 to 22,375 by the end of January 2023;

The number of people holding virtual assets globally rose from 306 million in January 2022 to 425 million in December 2022.

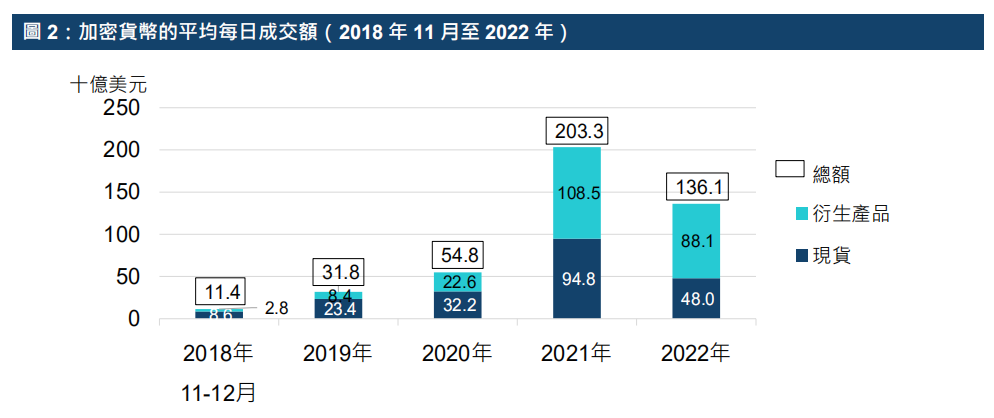

Structurally, the number of crypto asset holders has increased, and the proportion of derivatives in trading structure has gradually expanded:

The average daily trading volume (including spot and derivatives) increased from $31.8 billion in 2019 to $136.1 billion in 2022;

The average daily trading volume of spot trading during the same period grew by 105% from $23.4 billion to $48 billion, equivalent to about 21% of the combined average daily trading volume of stocks listed on the New York Stock Exchange and NASDAQ;

In 2021, the trading volume of crypto derivatives exceeded that of spot trading, and in 2022, the trading volume of derivatives was nearly double that of spot trading.

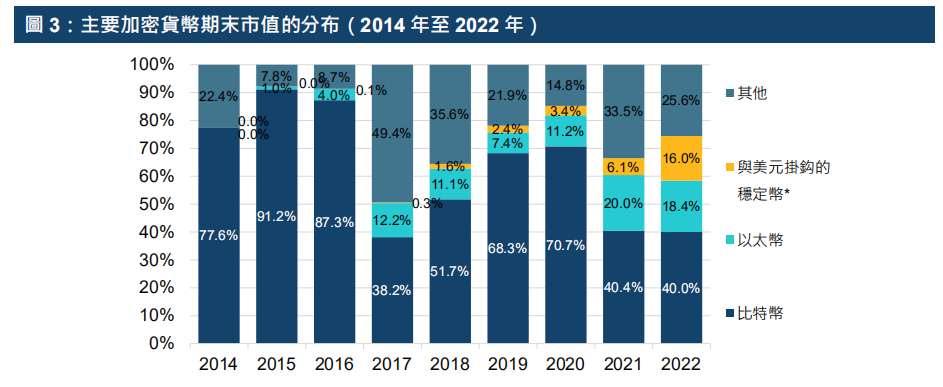

Changes in the market capitalization structure of Bitcoin, Ethereum, stablecoins, and other crypto assets:

Bitcoin's market capitalization shows a shrinking trend but remains a pillar;

Ethereum's market capitalization is gradually expanding, and stablecoins exhibit the same characteristics during the same period;

The trend becomes more apparent when viewed year by year in the chart.

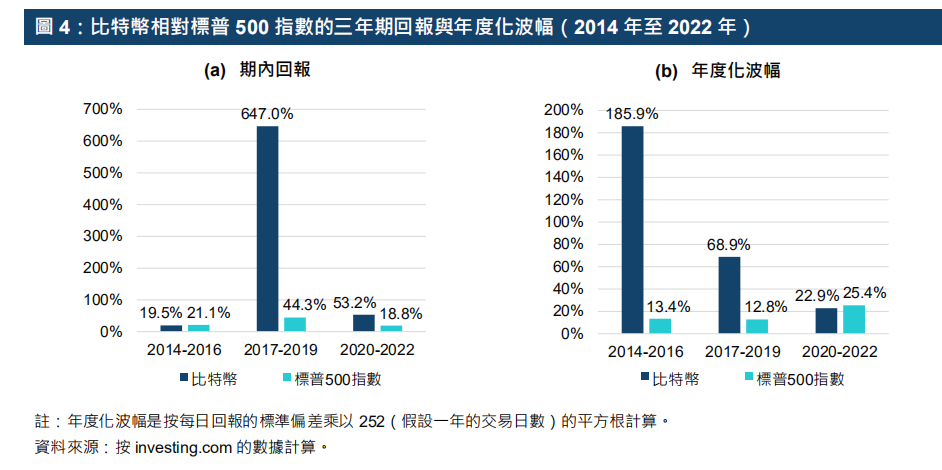

Crypto assets are gradually becoming an "alternative" investment choice, with significantly higher volatility and unstable returns compared to mainstream investments:

The annualized price volatility of Bitcoin ranged between 22.9% from 2020 to 2022 and 185.9% from 2014 to 2016;

The S&P 500 index ranged between 12.8% and 25.4%;

Over time, Bitcoin's annualized volatility shows a downward trend.

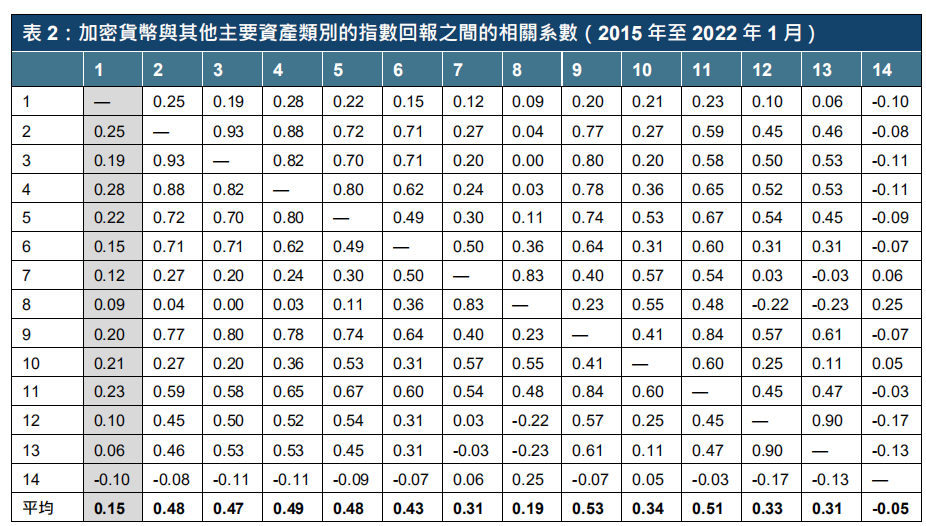

How is the correlation between "alternative" and "mainstream":

- From 2015 to January 2022, the average correlation coefficient between virtual assets and other major asset class index returns was 0.15%,

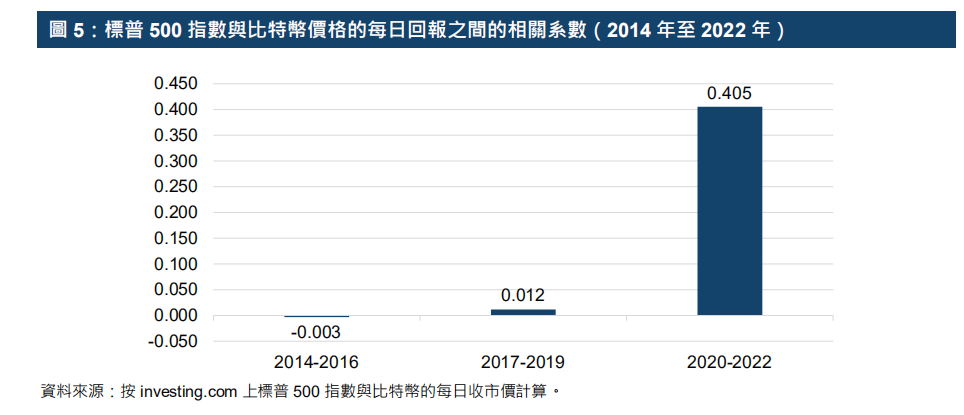

Correlation may change over time: The correlation coefficient between the daily returns of the S&P 500 index and Bitcoin prices rose from 0.012 between 2017 and 2019 to 0.405 between 2020 and 2022;

This increase in correlation may be due to traditional financial institutions gradually increasing their investments in virtual assets.

Global regulatory systems vary, and some regions have formed compliant ETFs for investing in virtual assets:

II. The Path to Compliance: Global Trends, Correlation, and Market Performance of Virtual Asset ETFs

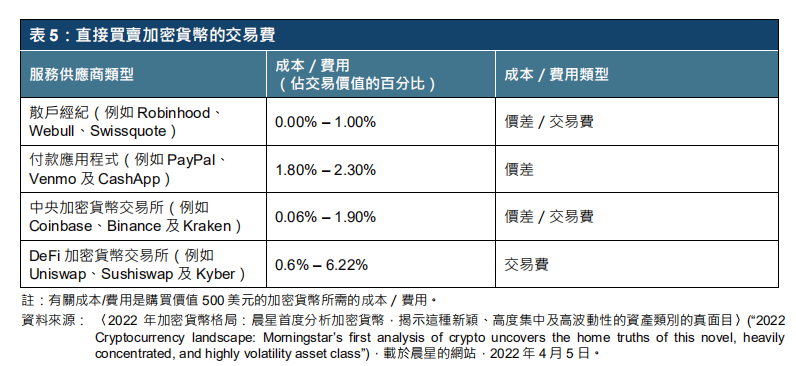

All channels for entering the virtual asset market have been fully summarized by the Hong Kong Stock Exchange:

Direct channels: Buying and selling cryptocurrencies through cryptocurrency brokers or exchanges, or ICOs;

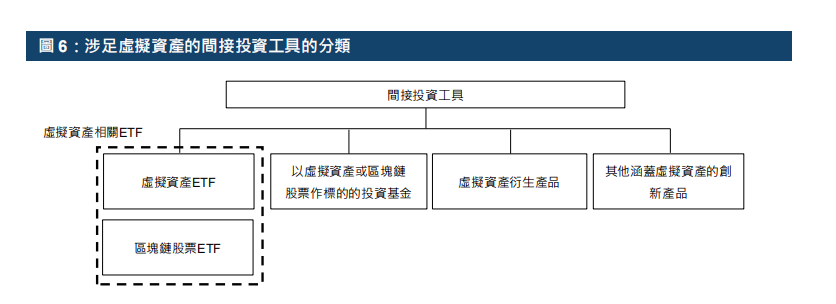

Indirect channels: Investing in stocks of blockchain companies, cryptocurrency futures + ETFs, and other funds.

The Hong Kong Stock Exchange believes that ETFs in indirect channels are safer, more compliant, and have more controllable risks.

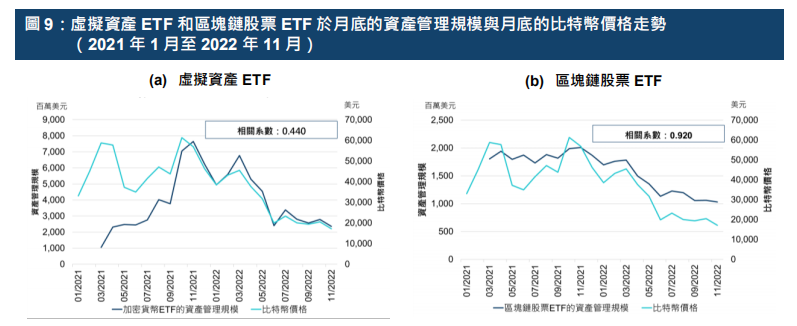

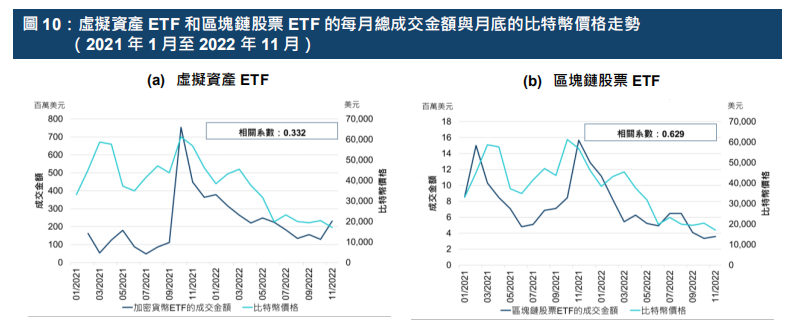

Existing ETFs in the global capital markets and their market performance:

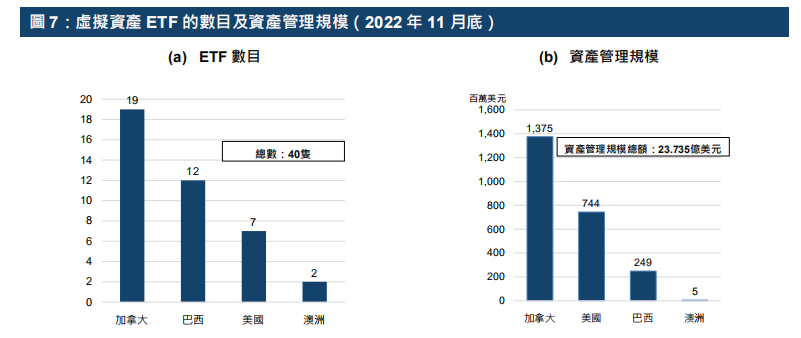

- By the end of November 2022, there were 40 virtual asset ETFs across multiple markets in Canada, Brazil, the United States, and Australia, with a total asset management scale of $2.4 billion;

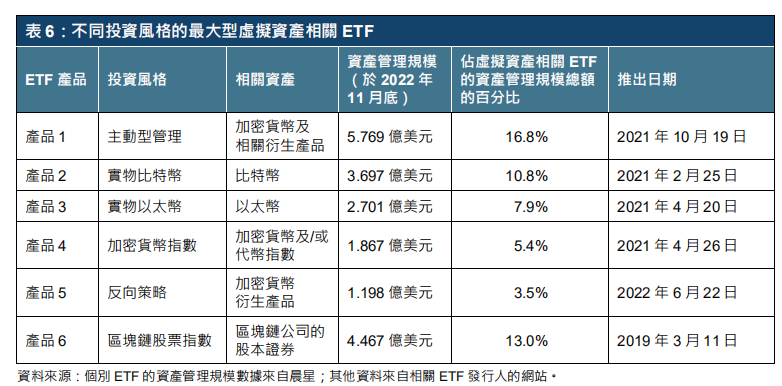

Characteristics of virtual asset ETFs and current market scale:

Product types: Physical ETFs—holding physical virtual assets; Virtual ETFs—holding futures contracts;

Underlying types: BTC + ETH are mainstream, with DeFi indices also available;

Management strategies: "Long only," "Options combination," "Inverse (short) strategy," "Cryptocurrency index."

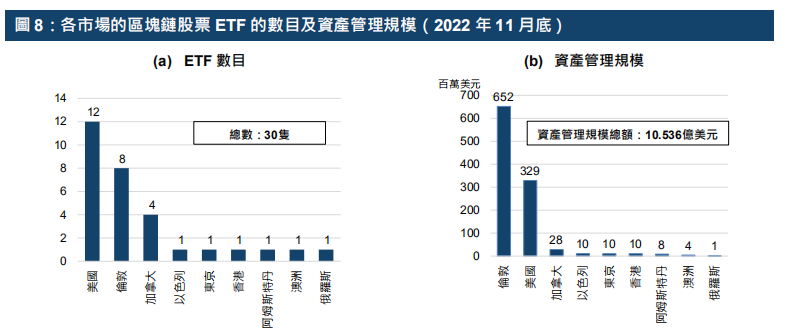

In terms of scale and quantity, North America and the UK are leading.

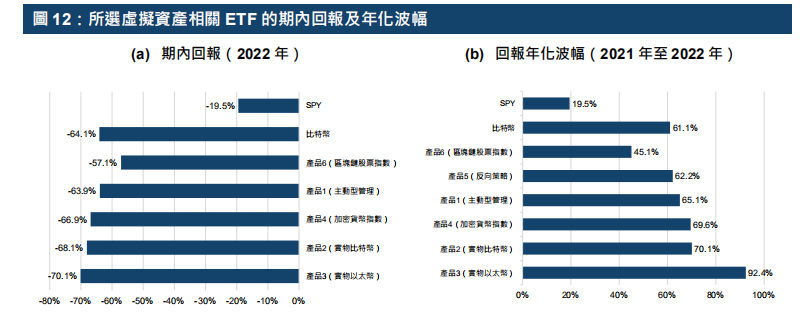

As expected—there is a certain correlation between ETFs and Bitcoin prices:

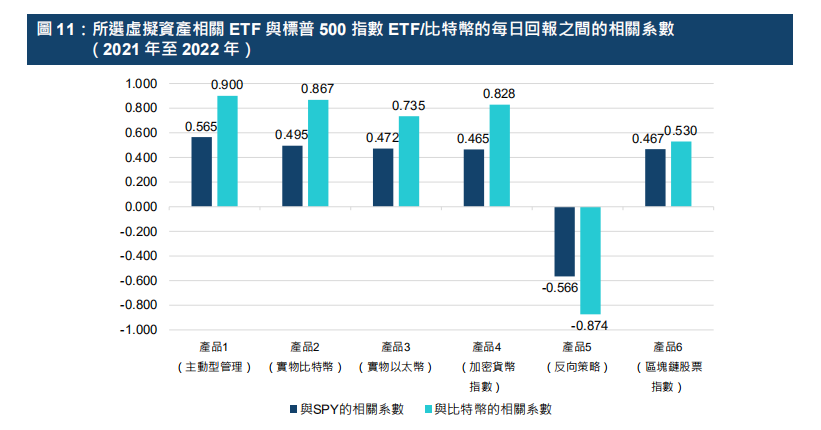

Representative ETFs of different management strategies:

Conclusions on the correlation of ETF returns with traditional securities markets and BTC:

Virtual asset ETFs (Products 1 to 5) have a high correlation with Bitcoin's daily returns, but the correlation with the studied SPDR S&P 500 Index ETF (Ticker: SPY) is only moderate;

The blockchain stock ETF (Product 6) has a moderate correlation with both SPY and Bitcoin's daily returns, with a slightly higher correlation with Bitcoin price returns;

Conclusion: Compared to traditional equity securities investments, virtual asset ETFs can help achieve portfolio diversification, and blockchain stock index ETFs can do the same (though to a lesser extent).

Volatility of virtual asset ETFs: The bigger the waves, the more expensive the fish, but can you withstand the storm?

ETFs vs. Non-listed Funds:

Compared to non-listed funds, ETFs are often more cost-effective;

ETFs have higher liquidity and transparency than non-listed funds;

ETFs can be bought and sold at any time during trading hours on the exchange;

ETF holding information is usually updated daily, while non-listed funds' information is not frequently disclosed.

III. Hong Kong's Attitude: Regulation, Practice, and Future Determination of Local ETFs

1. Hong Kong has made significant progress in market system structure and policies:

In 2021, investors purchased virtual asset funds worth HKD 10 billion through overseas platforms, a substantial increase from HKD 8 million in 2020;

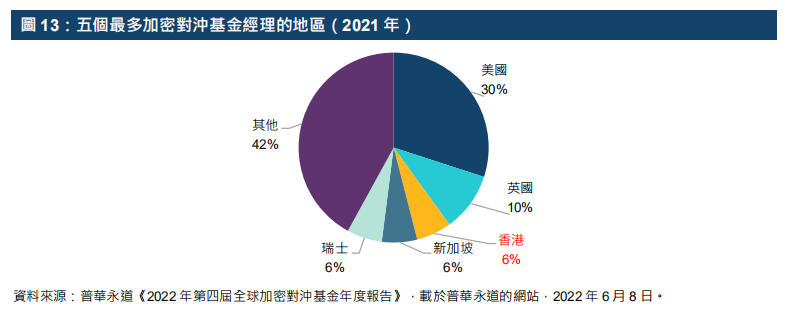

Hong Kong ranks third in the number of fund managers, with 6% of the world's crypto hedge fund managers;

2. Historical overview of the formation of the regulatory framework:

2018: The Securities and Futures Commission (SFC) launched its regulatory framework for virtual assets, stipulating that crypto asset clients "are limited to professional investors." These clients include those from SFC-licensed trading platforms, STOs (Security Token Offerings), and virtual asset funds.

January 2022: The SFC and the Hong Kong Monetary Authority (HKMA) issued the "Joint Circular on Virtual Asset-Related Activities of Intermediaries," allowing securities brokers and banks to provide virtual asset trading services for their clients.

October 2022: The then Deputy CEO of the SFC provided guidance on the issuance of virtual asset futures ETFs and STOs. The Financial Services and the Treasury Bureau published the "Policy Declaration on the Development of Virtual Assets in Hong Kong," outlining several pilot programs:

(1) Issuing NFTs for Hong Kong FinTech Week 2022

(2) Tokenization of Green Bonds—allowing the government to tokenize green bond issuances for institutional investors to subscribe.

(3) Digital Hong Kong Dollar

February 2023: The SFC released a consultation document on the new licensing regime for virtual asset service providers. The content includes the types and conditions of products for retail investors to buy and sell virtual assets, such as market capitalization, liquidity, and other criteria, indicating that Hong Kong's financial services industry has the opportunity to expand its virtual asset business to retail investors.

June 2023: A new licensing regime for virtual asset service providers was implemented.

Editor’s Note: More regulatory details can be found in the original report.

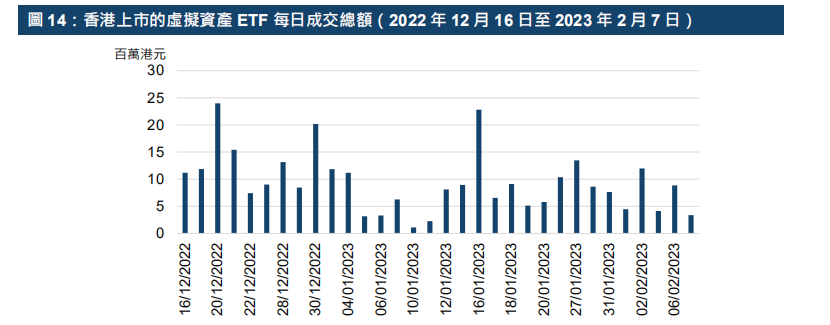

3. The first batch of virtual asset ETFs launched in Hong Kong:

On December 16, 2022, two ETFs were listed on the Hong Kong Stock Exchange: Bitcoin Futures ETF + Ethereum Futures ETF;

In January 2023, a third virtual asset ETF was listed in the Hong Kong market;

Using an active management strategy, the relevant assets are standardized, cash-settled futures contracts traded on the CME;

The average daily trading volume of the ETFs is about 9.3 million HKD.

Investors can easily enter the market by buying and selling virtual asset ETFs, unlike directly buying and selling virtual assets, which requires another dedicated trading account and crypto wallet.

This reflects the authorities' determination to develop Hong Kong's virtual asset ecosystem and the market's demand for related products. Looking ahead, it is expected that the Hong Kong market will launch more virtual asset-themed ETFs and other virtual asset products.

IV. Conclusion

Driven by the development of Web 3.0 and blockchain technology, virtual assets are becoming an increasingly important part of the financial system. The regulatory framework for virtual assets is also continuously evolving, striving to balance market development and financial stability.

Currently, investors can trade virtual assets directly through cryptocurrency exchanges or brokers, or indirectly through investment funds (including ETFs) to engage in virtual assets.

Various types of virtual asset ETFs have already been launched in the global market, allowing investors to capture investment opportunities in cryptocurrencies and publicly listed blockchain companies.

As an international financial center with a robust regulatory framework, the Hong Kong market is fully prepared to seize the potential opportunities brought by the development of virtual assets. Hong Kong has now established foundational regulatory systems to support the healthy development of its virtual asset ecosystem, and the first batch of virtual asset ETFs has been listed as a starting point for innovation in related products. Continuous improvements in the regulatory framework are expected to facilitate the development of Hong Kong's virtual asset ecosystem.

The complete content of the report in both Chinese and English is available on the Hong Kong Stock Exchange's official website:

Risk warning

Risk warning Risk warning

Risk warning