Is RWA, which major institutions like Binance and Goldman Sachs are competing to invest in, the next growth engine for DeFi or just a fleeting phenomenon?

Why has RWA become popular again? What are the representative use cases of RWA?

Why has RWA become popular again? What are the representative use cases of RWA?Written by: flowie, ChainCatcher

RWA (Real-World Assets), seen as the next growth engine for DeFi, is gaining momentum.

Recently, after the crypto lending protocol Maple Finance announced the launch of a U.S. Treasury pool, its token $MPL surged over 20%. In the past three months, RWA concept tokens like $CREDI, $SMT, and $FACTR have all increased by more than tenfold.

Additionally, last week, Binance announced it would become a node operator for the Layer1 blockchain Polymesh, which has also drawn market attention to RWA. Polymesh is not an ordinary Layer1 but an institution-grade blockchain tailored for regulated assets such as security tokens. Following the announcement, the Polymesh token POLYX rose over 10%.

Currently, an undeniable trend is that in addition to Binance, major traditional financial institutions like Goldman Sachs, Hamilton Lane, and Siemens, as well as leading DeFi protocols like MakerDAO and Aave, are all vying to establish a presence in the RWA space.

According to the crypto data platform Rootdata, the RWA sector has nearly 50 projects, with many innovative projects focused on lending and real estate. Among them, projects like Goldfinch, Centrifuge, and Maple Finance have notable investors such as a16z, Coinbase Ventures, and Distributed Capital.

Why is RWA gaining popularity again?

RWA ------ the tokenization of real assets, is not a new concept. Since the inception of blockchain, discussions about the tokenization of real-world assets such as real estate, commodities, private equity, credit, bonds, and art have been common, and several conceptual projects have emerged, but none have made significant waves.

In 2020, MakerDAO officially incorporated RWA into its strategic focus and released guidelines and plans for introducing RWA, gradually attracting more attention. In addition to issuing the stablecoin DAI, MakerDAO passed proposals to use RWA as collateral in the form of tokenized real estate, invoices, and receivables to expand the issuance of DAI. It is reported that about 70% of MakerDAO's revenue in December 2022 came from RWA. Aave followed closely behind MakerDAO and announced the launch of an RWA market at the end of 2021, also allowing for the collateralized lending of real assets. However, despite the involvement of leading protocols, RWA has remained relatively lukewarm.

Recently, Binance's entry into the market, along with the intensive layout by traditional financial giants like Goldman Sachs, Hamilton Lane, and Siemens, has brought RWA back into the spotlight.

Earlier this year, Goldman Sachs announced the official launch of its digital asset platform GS DAP, which has already helped the European Investment Bank (EIB) issue €100 million in two-year digital bonds. Shortly after, private equity firm Hamilton Lane, managing over $100 billion, tokenized part of its $2.1 billion flagship equity fund on the Polygon network and sold it to investors; electrical engineering giant Siemens also issued €60 million in digital bonds on the blockchain for the first time.

In addition to becoming a node operator for the Layer1 blockchain Polymesh, Binance also released a 34-page in-depth research report on RWA in March of this year.

Aside from the actions of major institutions, we also noticed that several projects supporting on-chain U.S. Treasury bonds, represented by Ondo Finance and TProtocol, are very active. Last week, Ondo Finance announced the launch of the dollar stablecoin OMMF based on money market funds (MMF), TProtocol launched a liquidity mining program, and Maple Finance announced it would introduce a U.S. Treasury pool.

Some crypto-friendly government agencies are also experimenting with RWA, such as the Monetary Authority of Singapore (MAS), which announced a pilot project called "Project Guardian," which will tokenize bonds and deposits for various DeFi protocols, with JPMorgan and DBS Bank as pilot partners.

Since RWA is not a new concept, why is it being re-emphasized at this point? What are the driving factors?

The Binance RWA research report mentions that in the short term, the most direct reason is that the persistently low yields in DeFi cannot meet the growing yield demands of crypto users. During the DeFi Summer, the high yields of the bull market could satisfy the yield needs of crypto investors. However, after experiencing significant market turbulence and a prolonged bull market, the TVL of DeFi has dropped over 70% from its peak in December 2021, and DeFi yields have plummeted to rock bottom, necessitating a new growth channel for yields for DeFi protocols or crypto investors.

From this perspective, it is also easy to understand why on-chain U.S. Treasury bonds are currently the hottest trend in the RWA space. With the Federal Reserve's continuous interest rate hikes, the yields on U.S. Treasury bonds are much higher than those of DeFi protocols. The average yield of established DeFi protocols like Curve, Aave, and Compound has dropped from over 10% to between 0.1% and 2%, while the yield on U.S. Treasury bonds has risen from 0.3% to 5%. The latter also carries fewer security risks compared to the former.

Additionally, in the long term, the story of RWA bridging traditional finance and crypto finance indeed brings a lot of imagination.

The real assets of traditional finance, such as real estate and non-financial corporate debt markets, are trillion-dollar markets. If DeFi can be compatible with them, it can provide users with greater liquidity, capital efficiency, and investment opportunities.

At the same time, traditional finance also faces many pain points, such as high entry barriers, numerous intermediaries, and various restrictions. For example, the investment capital for private equity funds generally exceeds $500,000, and real estate investments also require substantial capital support, making it nearly impossible for ordinary investors to enter. Additionally, there are high fees from intermediaries, regulatory restrictions on entry, and risks associated with assets in third-party systems. The design of DeFi can also address some of the pain points of traditional finance, attracting more investors into DeFi.

A recent report from the Boston Consulting Group indicates that by 2030, RWA is expected to become a market worth $16 trillion.

What are the representative use cases of RWA?

The aim of RWA to bridge traditional finance and crypto finance is easy to understand, but truly achieving this and injecting a large scale of new assets into Web3 is not an easy task.

"We are still far from the ultimate goal," @ThreeDAO member Jason Chen believes that the development of the RWA space currently has two stages. The first is the early process of using blockchain for the rights verification of real assets like real estate and collectibles, such as many consortium chains that put stamps on the blockchain. The second stage emerged after the rise of DeFi, featuring stablecoins and DeFi derivatives that brought fiat and other real assets onto the chain. We are currently exploring the second stage.

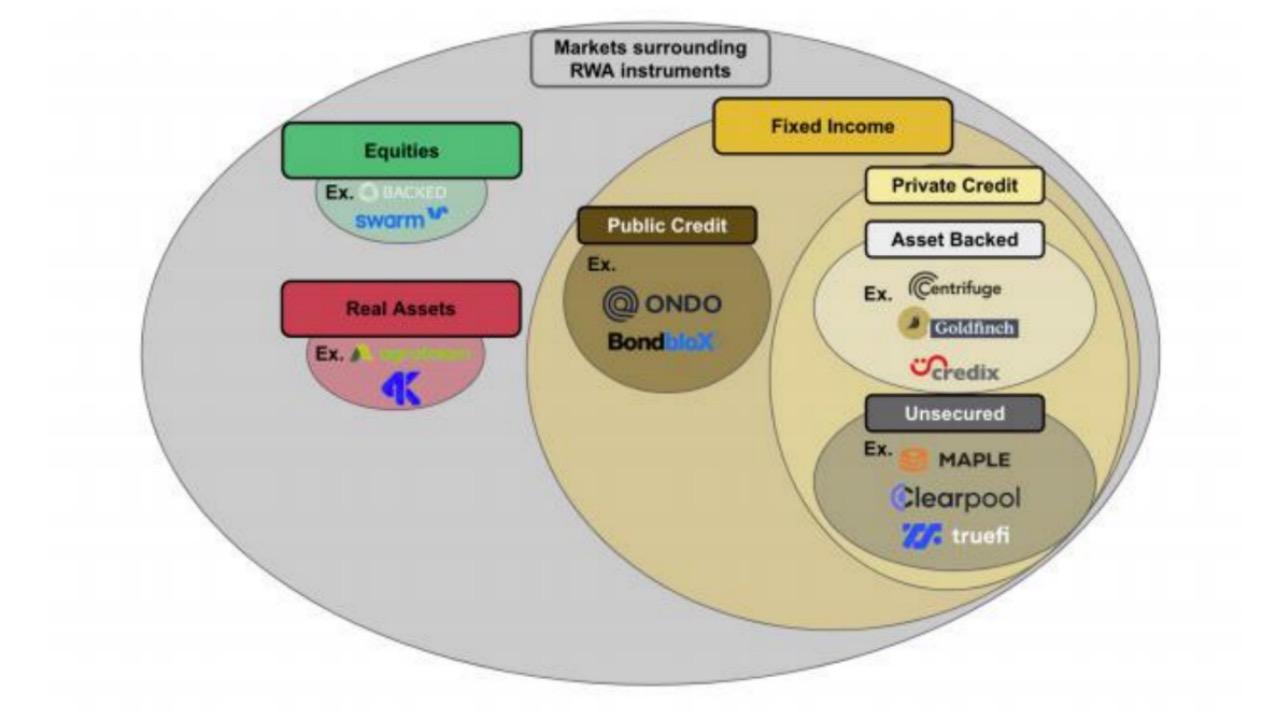

According to the classification in the Binance research report, the current RWA market mainly consists of three major markets: the equity-based DeFi market, the physical asset-based DeFi market, and the fixed-income-based DeFi market.

Among them, the fixed-income-based DeFi market is currently the most significant market for RWA, which mainly includes DeFi protocols that provide private credit and public bonds. Other projects related to real estate, art, and tokenization of private equity or stocks are relatively few or have limited activity.

Private Credit

In terms of private credit, one category includes asset-backed private credit protocols like Centrifuge, Goldfinch, and Credix, while another category includes unsecured private credit protocols like MAPLE, Clearpool, Truefi, and Ribbon Lend. Currently, these seven largest RWA private credit protocols have a historical loan amount exceeding $4 billion, with active loans nearing $500 million and an average annual interest rate exceeding 12%.

Centrifuge, established as one of the earliest DeFi protocols involved in RWA, is also a technology provider behind leading protocols like MakerDAO and Aave, with investors including Distributed Capital, Coinbase Ventures, and IOSG Ventures. In December 2022, Centrifuge announced a partnership with DeFi Fintech, MakerDAO, and BlockTower Credit to establish a $220 million fund.

Centrifuge aims to help central enterprises finance with lower barriers while allowing investors to earn income from real assets. Centrifuge essentially simulates the process of corporate credit in traditional finance, but uses DeFi + NFT to eliminate some intermediaries' participation and cumbersome off-chain processes.

The financing process on Centrifuge can be summarized as follows: borrowers package and upload their off-chain real assets, generating a legally effective NFT for collateral, and receive interest-bearing ERC20 tokens, which investors can purchase using DAI; upon maturity, the initiator redeems the financing, and investors receive returns. The funds generated from the interest-bearing ERC20 tokens are also divided into primary and secondary pools, where primary pool investors have higher returns but also higher risks, while the secondary pool has relatively lower returns and risks.

Although Goldfinch, created by former Coinbase employees, entered the market slightly later than Centrifuge, it has secured significant funding from well-known institutions due to its innovative model, accumulating $37 million in financing, with a16z leading two rounds, and notable investment institutions like Coinbase Ventures, Alliance DAO, BlockTower Capital, and angel investors like Balaji Srinivasan also participating.

Goldfinch primarily provides loans to debt funds and fintech companies, offering borrowers USDC credit lines and supporting conversions to fiat currency for borrowers. Goldfinch's model resembles traditional banks but features decentralized auditors, lenders, and credit analyst pools. Auditors for Goldfinch borrowers must hold staked governance tokens (GFI). Goldfinch can offer high yields due to low collateral requirements, allowing its borrowers to pay interest rates of 10-12%, and it has not yet experienced any defaults.

Compared to asset-backed private credit protocols, protocols like Maple and TrueFi have provided high active loans during the bull market due to their unsecured credit models. Unlike Goldfinch, which uses users as auditors, Maple employs professional credit reviewers to strictly audit borrowers' credit. However, under the unsecured model, following the collapses of Three Arrows Capital and FTX, Maple faced $52 million in bad debts, and its KYC requirements have raised concerns about its centralization. Recently, Maple has also expanded into a lending model backed by real assets to mitigate risks.

Public Bonds

In contrast to private credit protocols, on-chain bonds have also benefited from the Federal Reserve's continuous interest rate hikes. As mentioned earlier, in addition to traditional financial institutions, there are also many protocols focusing on this field, such as Flux Finance (developed by the Ondo Finance team), TProtocol, Backed Finance, PV01, Kuma Protocol, Arca Labs, Stream Protocol, Cytus Finance, and BondBlox.

Notably, Ondo Finance, founded by former Goldman Sachs digital asset team member Nathan Allman and former Goldman Sachs technology team vice president Pinku Surana, has currently secured $34 million in investments from well-known institutions like Pantera Capital, Coinbase Ventures, Tiger Global, and Wintermute.

Ondo Finance offers investors four types of bonds: U.S. Money Market Fund (OMMF), U.S. Treasury Bonds (OUSG), Short-Term Bonds (OSTB), and High-Yield Bonds (OHYG). After participating in KYC/AML processes, users can trade fund tokens and use these fund tokens in permitted DeFi protocols. Among them, OUSG has the largest usage scale, allowing KYC-compliant OUSG holders to deposit into the decentralized lending protocol Flux Finance developed by Ondo Finance to lend their tokens for USDC leverage; non-KYC USDC holders can earn a low yield of 50 basis points by providing loans to KYC-compliant leverage seekers.

Investor Tzedonn from Tioga Capital mentioned in a recent report that the existing market value of bond tokens is $168 million, with Ondo (OUSG) holding a 61% market share, of which 28% is deposited in Flux Finance. Currently, Flux Finance's total supply has exceeded $40 million, and the market value of OUSG has surpassed $100 million.

Real Estate and Other Physical Asset Markets and Equity Markets

Compared to private credit and public bonds, projects based on real estate, art, and tokenization of private equity or stocks are relatively few or have limited activity. On one hand, these assets can only be provided by registered and vetted exchanges, which are subject to strict regulation. On the other hand, they typically require off-chain physical ownership of the underlying asset class, making operations more complex. However, many protocols in this field are still exploring ways to introduce more valuable real assets into Web3.

There is a growing trend in the tokenization of real estate, with representative projects including Propy, ReaIT, Atlan, LABS Group, ELYSIA, and Tangible. By tokenizing real estate, liquidity and transaction cost issues can be addressed. For example, properties that originally needed to be bought and sold as whole units can be fragmented, allowing ordinary investors to participate in investments by holding partial ownership.

In addition to real estate, the tokenization of carbon credit certificates for trading on the blockchain is also an emerging and potentially lucrative market, with representative projects like Toucan, Flowcarbon, and Regen Network.

Is the RWA narrative overly optimistic?

The renewed interest in RWA also faces many criticisms. Many crypto enthusiasts point out that many current RWA projects are merely DeFi derivatives dressed in a new RWA concept, and the real obstacles to bridging traditional finance and crypto finance are substantial.

First is regulation. Many crypto enthusiasts have pointed out that tokenization implies the need for global trading liquidity, while real assets are geographically restricted. The core of RWA lies in the credit mechanism, and the key to facilitating global circulation is establishing internationally applicable legislation, which should also have strong enforcement capabilities. However, currently, RWA faces significant compliance hurdles.

A Twitter user @0xChok, who previously worked on putting assets like stamps on the blockchain, agrees with this view, stating that they could only use consortium chains for assets like stamps, "on the surface it's blockchain+, but essentially it's still centralized endorsement, which cannot be universally applied globally, making true liquidity very difficult."

At the same time, a reality is that some asset protection mechanisms also face challenges. Currently, many private credits like MAPLE and TrueFi have encountered bad debts, but since the collateral is not liquid ERC-20 tokens, liquidating these assets to recover lenders' capital is much more complicated than loans using crypto collateral.

Additionally, there are views that the attractiveness of RWA to crypto users may decline once DeFi recovers. Once the macroeconomy and DeFi show signs of recovery, the appeal of RWA to crypto users may be far from sufficient, making it difficult to escape the fate of being a fleeting trend.

Despite the significant challenges, infrastructure specifically established for RWA is emerging. Due to regulatory and other restrictions, permissionless public chains like Ethereum may struggle to meet the trading needs of RWA assets, leading to the emergence of vertical application chains specifically designed for RWA. For example, Polymesh, an institution-grade blockchain tailored for regulated assets like security tokens, has recently been announced by Binance as one of its nodes. Additionally, RWA vertical application chains like MANTRA Chain, Realio Network, Provenance, and Intain are also worth watching.

Currently, the RWA space is still in its early stages and needs to wait for regulatory and infrastructure improvements. However, the RWA narrative still holds tremendous growth potential, and by linking to real assets, it may also bring more traditional users into the DeFi and Web3 world, truly reshaping the landscape of the crypto market.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles