Grayscale: Reassessing the Future Market Size of Bitcoin from the Perspectives of Digital Value, Settlement Layer, and Applications

From digital value storage to medium of exchange, and then to the settlement layer of non-monetary blockchain activities, Grayscale reassesses the future of BTC.

From digital value storage to medium of exchange, and then to the settlement layer of non-monetary blockchain activities, Grayscale reassesses the future of BTC.Original Title: "Bitcoin's Purpose: Sizing the Addressable Markets"

Original Authors: Zach Pandl, William Ogden Moore

Original Source: Grayscale

Compiled by: Lynn, MarsBit

From digital value storage to medium of exchange, and to the settlement layer for non-monetary blockchain activities, Grayscale reassesses the future of BTC.

- Today, Bitcoin is a scarce digital commodity and an alternative to physical gold. Compared to the size of the gold investment market, Bitcoin remains relatively small. We expect Bitcoin to continue to capture market share from gold as a value storage asset more suited to our digital age.

- However, Bitcoin's potential uses are not limited to its role as a potential gold substitute, as the decline in transaction costs through the adoption of the Lightning Network or other solutions may help Bitcoin compete with fiat currencies in certain areas of the global economy, and new innovations are constantly emerging in the global economic landscape. Over time, networks (such as the development of second-layer protocols for NFTs and smart contracts) may contribute to Bitcoin's potential.

- The overall size of these potential markets may imply significant room for growth in Bitcoin's valuation over time.

Despite Bitcoin's more than 14-year history and ownership by millions (1), the potential uses of the network remain contentious. To some extent, this is not surprising: Bitcoin is fundamentally different from what came before, and the core technology and ecosystem surrounding it need time to mature. For investors, this means that the potential market for this asset (the existing economic structures that the technology can disrupt) is always a moving target. While we can quantify certain aspects of Bitcoin's market opportunities, innovation is always expanding the possibilities of the world's first public blockchain. We see a range of potential use cases: from digital value storage to medium of exchange, and to the settlement layer for non-monetary blockchain activities.

Bitcoin as a Store of Value

Today, Bitcoin has been established by some as a scarce "store of value" asset and a digital competitor to gold. This use case was evident from the beginning—Bitcoin's creator, Satoshi Nakamoto, likened the token to a rare base metal with special properties: it "can be transmitted over communication channels" (2). Although gold has existed for a longer time, Bitcoin possesses certain characteristics that are attractive to its holders, particularly its portability; as long as holders have access to the internet and their private keys, Bitcoin can be used anywhere in the world. The economic conditions since Bitcoin's inception—financial crises, pandemics, and soaring inflation—have accelerated the demand for tools that may help preserve the actual value of assets and support Bitcoin as a digital alternative to gold.

Compared to the physical gold market, Bitcoin's market capitalization of about $500 billion (3) is relatively small. We estimate the market value of above-ground gold stocks to be around $13 trillion, with about $3 trillion in private gold investments (ETFs plus held bars and coins), and slightly over $2 trillion held by central banks (see Figure 1) (4). Despite Bitcoin's significant growth over the past decade, the size of the gold investment market is still about five times (or nine times, including gold held by central banks) that of Bitcoin. We expect Bitcoin to continue to capture market share from gold as a value storage asset more suited to our digital age.

Figure 1: Bitcoin remains small compared to the gold investment market

Bitcoin as a Medium of Exchange

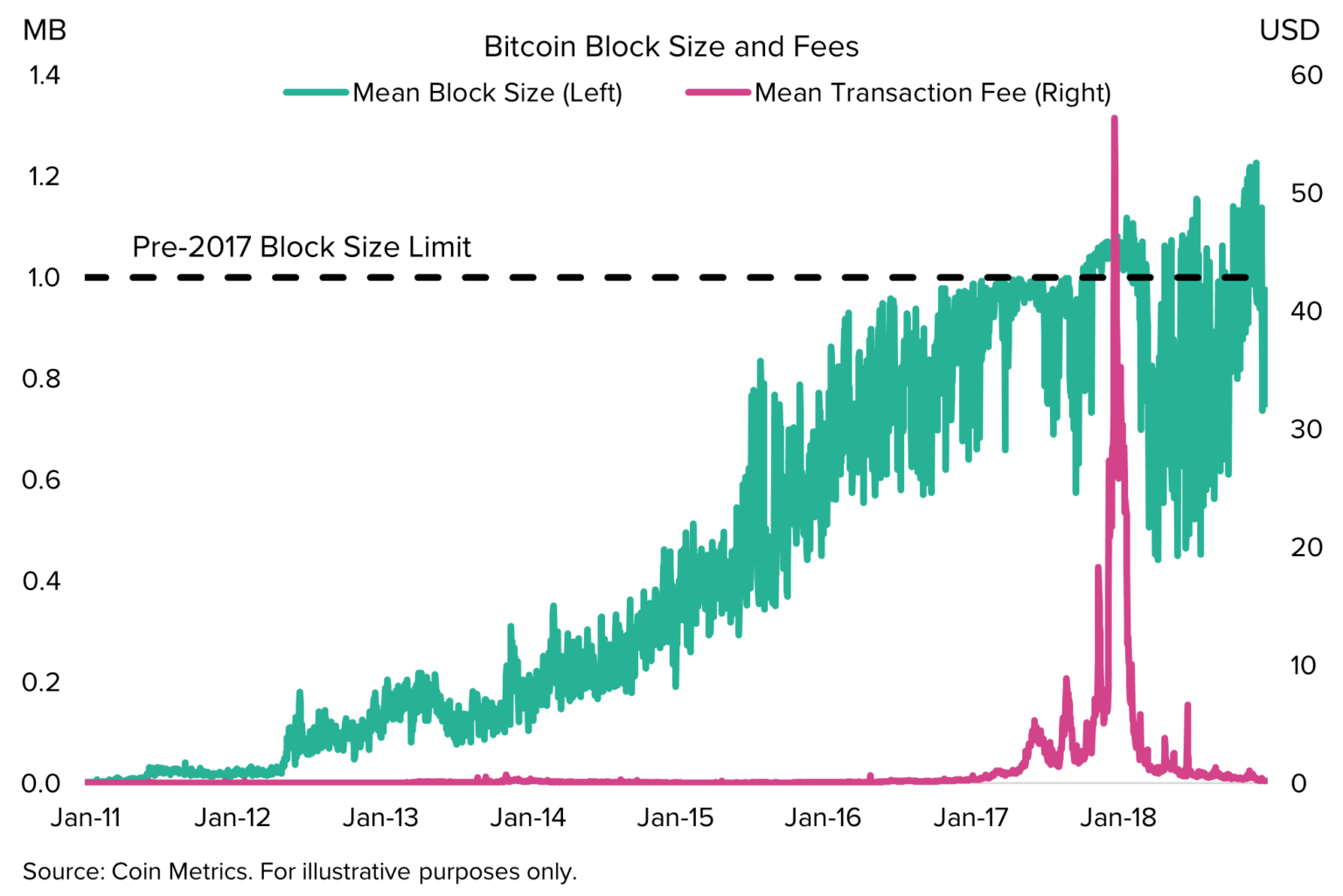

Bitcoin's intended use is as a peer-to-peer electronic cash system, but its adoption as such a digital medium of exchange has been slow. This may reflect a variety of factors, including its historical volatility, the network advantages of existing currency systems, and the transaction costs associated with Bitcoin. In the early history of the network, transaction costs for Bitcoin were relatively low, and it was often used as an experimental medium of exchange. As network usage increased and blocks began to fill up, transaction costs became higher and more volatile (see Figure 2). These fees are a function of transaction complexity—the number of bytes occupied in a block—rather than the dollar value. Thus, Bitcoin transactions are more cost-effective for high-value payments and may indeed be cheaper than traditional payment systems, but they are not cost-effective for low-value or retail payments.

Figure 2: Bitcoin transaction costs increase when block size limits are reached

Can Bitcoin gain wider adoption as a medium of exchange? In developed market economies with stable currency systems, this seems unlikely even in the long term. Blockchain technology may help improve existing payment infrastructures, but we believe that the vast majority of retail transactions are more likely to use stablecoins, and ultimately may use central bank digital currencies (CBDCs). While some users may value the fact that Bitcoin transactions avoid centralized intermediaries, the dominance of card-based digital payments today suggests that most users prioritize speed, convenience, and stability.

That said, we can foresee Bitcoin being used more widely as a medium of exchange in parts of the global economy that meet certain conditions. For example, in countries where the national currency or banking system is unstable, Bitcoin may be the preferred medium of exchange; in these cases, users may also appreciate Bitcoin's censorship-resistant properties, especially when transaction costs are low or the network advantages of existing currency/monetary systems have been overcome. The use of Bitcoin in El Salvador meets some of these conditions: the Chivo wallet (5) covers all retail transaction fees, and government mandates have overcome network challenges (6), but importantly, the country did not have an unstable national currency beforehand (it has dollarized), and it remains to be seen to what extent Bitcoin will remain a lasting medium of exchange.

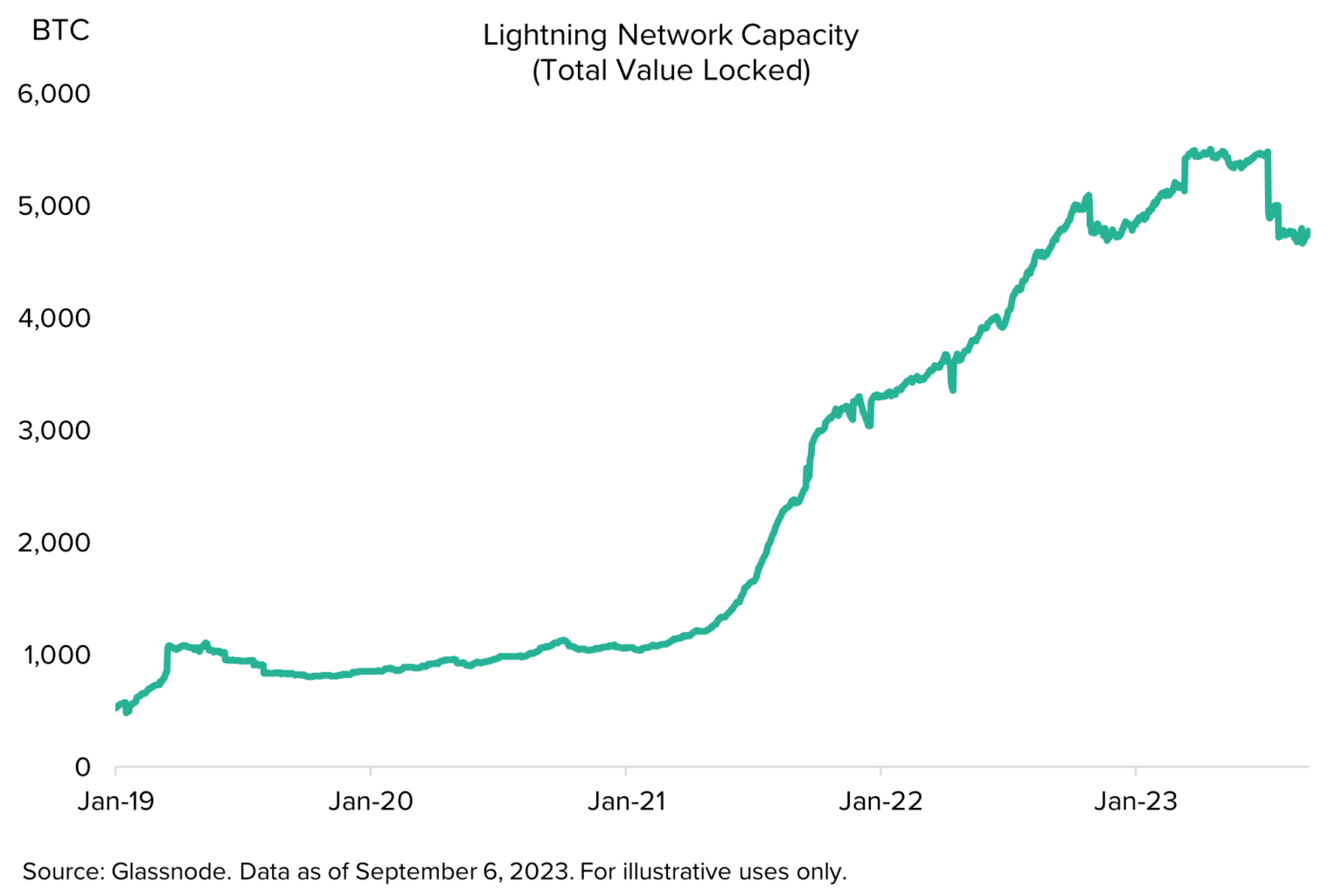

Efforts to reduce Bitcoin transaction costs through the Lightning Network (a "second-layer" protocol) may naturally increase adoption. The first-layer blockchain serves as a foundational database or "digital ledger," where transactions are settled. The second layer consists of additional protocols that coexist with the first-layer chain and benefit from its consensus mechanism and security. The second layer typically provides additional application functionality and/or lower costs.

The Lightning Network is a second-layer scaling solution for Bitcoin designed for low-cost and high-volume payments. Users do not settle each transaction on the first-layer blockchain but send and receive payments through off-chain channels, which can then be periodically settled to the main network. The initial adoption rate of the Lightning Network was low, but it has shown more progress as development continues (see Figure 3). Notably, the Lightning Network can facilitate not only direct Bitcoin transactions; in the future, it could also support stablecoins (7) or fiat payments made through Bitcoin (i.e., fiat to Bitcoin to fiat payments). In these cases, Bitcoin would accumulate value as a settlement asset for a network used for digital payments, even if it is not directly used as a digital payment medium.

Figure 3: The development of the Lightning Network improves the prospects for transaction use cases

If Bitcoin can make progress as a medium of exchange or as a network facilitating digital fiat transactions, the potential market opportunity could be substantial. For example, we estimate that the global "M1" (the traditional definition of money for transactions) totals about $60 trillion (8). Therefore, if Bitcoin can capture a small portion of this market, we believe it will have a meaningful impact on the potential valuation of the token.

As mentioned above, we expect Bitcoin will not become the primary medium of exchange for retail transactions in developed market economies, as we predict stablecoins are more likely to fill that role. However, not all types of "money" are the same, and some portions of the existing quasi-money asset stock should be more easily disrupted.

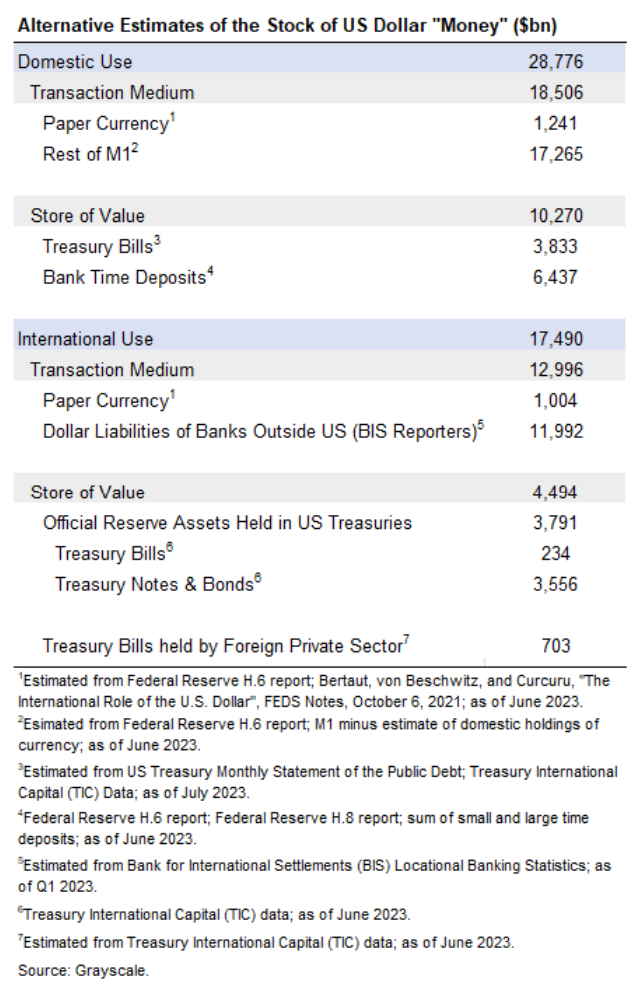

Consider the international use of the dollar: the dollar is widely used outside the United States, including in transactions that do not involve U.S. residents. These uses may be more easily disrupted by blockchain-based mediums. In domestic economies, national governments can control public use of specific currencies through rules and regulations (for example, requiring taxes to be paid in the national currency or limiting the amount of foreign currency that can be held in bank deposits). In contrast, in international markets, the effective medium of exchange and store of value is a matter of choice and is determined by public demand. Therefore, the dominance of any international currency medium may change over time.

Although the dollar's monetary stock is smaller than that of domestic currencies, the international dollar market is also very large (Figure 4). For example, it is estimated that about $1 trillion (mostly in large denominations) of paper currency circulates outside the United States, and dollar deposits in major foreign banks amount to about $12 trillion. The latter figure does not include all dollar-denominated deposits in underdeveloped economies in Latin America, many of which have become significantly dollarized (9). The complex geography and multifaceted functions of money in the global economy may imply market opportunities for Bitcoin and/or other cryptocurrencies as mediums of exchange, even if fiat-backed stablecoins are the primary transaction medium of the future.

Figure 4: Bitcoin could compete with the dollar as an international currency

Bitcoin as a Settlement Layer

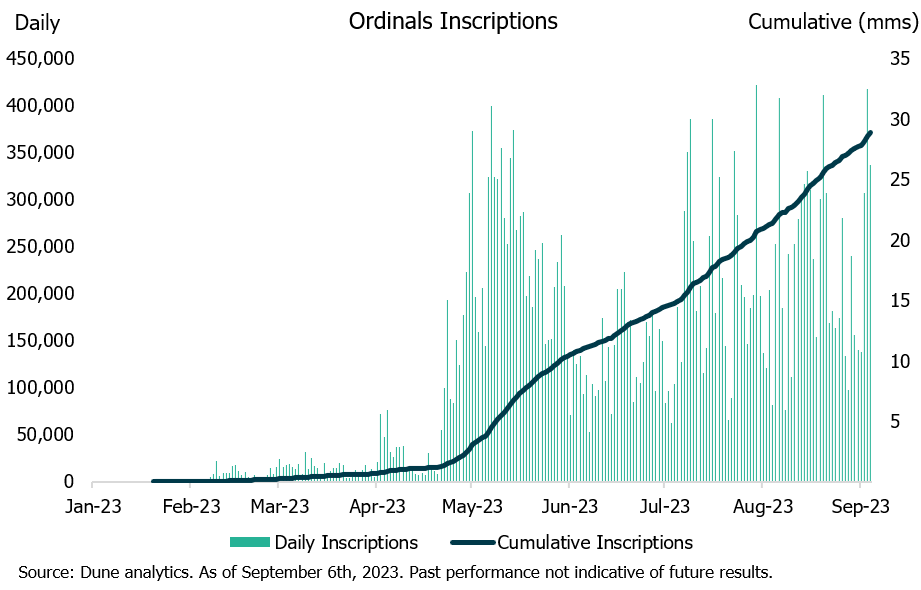

While Bitcoin was initially conceived for financial applications, the potential uses of the network may extend beyond financial applications in the long run. Over the past year, smart contracts and NFTs on the Bitcoin network have developed, effectively expanding the network's reach. In December 2022, Bitcoin developer Casey Rodarmor released the ORD software, paving the way for Ordinals or similar NFT assets on the Bitcoin network. A Bitcoin protocol upgrade in 2021 reduced the cost of storing arbitrary data, allowing Ordinals to enable users to mint non-fungible tokens (NFTs) from the smallest unit of Bitcoin (one satoshi). This use case also opens the Bitcoin network to the digital art and collectibles market. In May 2023, the early popularity of this feature helped miners earn 1,390 BTC (10) in fees, accounting for 30% of the total network fees of 4,540 BTC (11) for that month. Although the volume of Ordinal transactions later slowed, new inscriptions continue to occur, with a total of 26 million inscriptions this year (12), indicating that digital art on Bitcoin may continue to persist (see Figure 5).

Figure 5: NFTs on Bitcoin may continue to exist through Ordinals

The potential of smart contracts on the Bitcoin blockchain will further expand the network's impact. One of the early leaders in this work is Stacks, a second layer for Bitcoin that brings smart contract functionality into the Bitcoin ecosystem and provides decentralized applications (dApps) across various domains, including finance, gaming, and social applications. With a Total Value Locked (TVL) (13) of only $20 million, Stacks can still be viewed as a pilot project; larger smart contract platforms—such as Ethereum, its largest scaling solutions, and Solana—each maintain a TVL of over $300 million. Last year, the platform also garnered significant interest and attention from developers, with over 90 dApps (14) and 43 full-time developers (15), ranking 28th among all smart contract platforms, ahead of Lido, Chainlink, The Graph, and XRP. Overall, the early progress of Ordinals and Stacks suggests that Bitcoin has potential relevance across a range of areas from digital art and collectibles to any asset that can be programmed into smart contracts. These new use cases are in the early stages of bringing new end users (including artists, developers, speculators, collectors, or gamers) into the network, but if Bitcoin can translate the growing activity and interest from developers into long-term global significance in these areas, we believe it will also benefit from investments in new domains (such as the $67 billion art market (16), the $372 billion collectibles market (17), and the $227 billion video game market (18)).

Progress of Use Cases

From its universal status as a digital counterpart to gold, to its use as a means of payment and its potential relevance in other areas in the future, the utility and significance of Bitcoin have evolved and will continue to evolve. Currently, we expect Bitcoin as a store of value to continue to grow, capturing a larger share of the global gold investment market. Looking ahead, assuming large-scale adoption of scaling solutions like the Lightning Network, the use of Bitcoin as a means of payment may open up larger markets for the network, and Bitcoin's status as the first and most trusted cryptocurrency may also make it a formidable competitor to other smart contract platforms, unlocking opportunities in several new markets.

The potential market for Bitcoin can only be roughly estimated, and there is naturally a great deal of uncertainty in providing such estimates, as Bitcoin is just one asset that must compete with other cryptocurrencies (or unknown future innovations) to capture market share from gold and fiat currencies. Moreover, as the experience of Ordinals suggests, it is difficult to predict how developers will apply the Bitcoin network in the future. Nevertheless, Grayscale Research maintains an optimistic outlook on the various pathways for Bitcoin's continued growth.

References:

- As of August 2023, there were about 40 million Bitcoin addresses with a balance greater than $1; Source: Coin Metrics.

- Bitcoin forum, August 27, 2010.

- As of September 7, 2023.

- Data on above ground gold stocks in tonnes in 2022 from the World Gold Council, valued at current market prices.

- Chivo is a Spanish language digital token wallet.

- For details see "El Salvador: Staff Report for the 2021 Article IV Consultation", International Monetary Fund, January 2022.

- CoinDesk.

- Grayscale estimate based on data from national sources for 2022 or latest available year, depending on data availability by country.

- In Uruguay, for example, about 75% of deposits and 65% of loans are denominated in foreign currency, according to the IMF's Financial Soundness Indicators.

- Dune Analytics.

- Coin Metrics.

- Dune Analytics.

- Total Value Locked (TVL) is a measure of the dollar value of digital assets deposited in smart contracts.

- Stacks.

- Electric Capital Developer Report.

- UBS and Art Basel.

- HSBC.

- PwC.

Risk warning Risk warning

Risk warning Risk warning