In the eyes of the "old farmer" in DeFi, what are the current dangers and opportunities, and when will the wheel of fate start to turn?

Since the bear market, the TVL and token prices of DeFi projects have significantly declined. PANews invited several industry insiders to share their views and practical operations.

Since the bear market, the TVL and token prices of DeFi projects have significantly declined. PANews invited several industry insiders to share their views and practical operations.Author: Jiang Haibo, PANews

With the decline in TVL and the severe depreciation of token values, today's DeFi "old farmers" often reminisce about that summer of 2020.

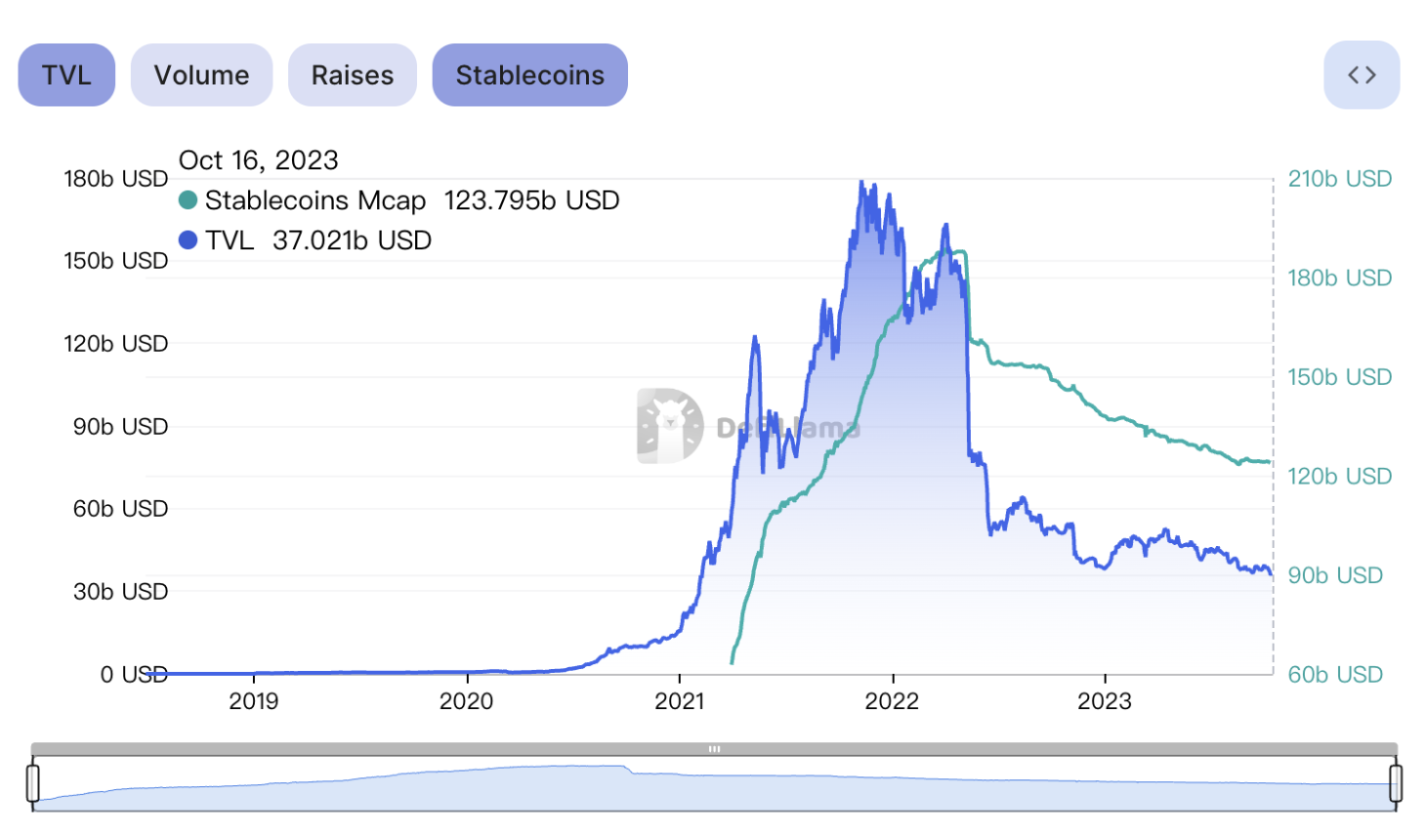

At that time, numerous new projects emerged in the DeFi space, and with the craze of "liquidity mining," annualized return rates (APR) reaching three to four digits allowed many early participants to reap substantial rewards, further attracting new users and new capital. However, with the arrival of the bear market, the key metric for measuring the liquidity and scale of DeFi projects, TVL (Total Value Locked), has dropped from its peak of $179.1 billion in November 2021 to $37 billion as of now (October 16, 2023).

Source: DefiLlama

Even governance tokens of leading DeFi projects like UNI have seen prices drop by 90% from their relative highs, and some projects that can generate real yields seem to have fallen into reasonable valuation ranges. What has caused the sharp decline in DeFi tokens? Has DeFi's valuation fallen out of the "golden pit"? Which tracks in DeFi are still considered promising for the future? What opportunities remain for participants in the DeFi market? PANews interviewed several industry insiders deeply involved in DeFi to gather their insights.

After enjoying high premiums, DeFi projects see "declining volume and price," with some projects shutting down

As the TVL of DeFi projects declines, the prices of their governance tokens are also continuously falling, yields are decreasing, and even the most recognized safe projects like Curve and Balancer are facing issues, exacerbating capital outflows. Against this backdrop, some projects have proactively liquidated and shut down, such as Saddle Finance, a former competitor of Curve on Ethereum, Algofi, a lending, trading, and stablecoin project in the Algorand ecosystem, and Friktion, an automated portfolio manager on Solana. Market confidence in DeFi seems to have reached a freezing point.

Source: Saddle Finance Official Twitter

Regarding the decline in TVL of DeFi projects, dForce founder Mindao believes that the TVL of DeFi projects does not reflect the true development situation; a more reasonable metric is the change in stablecoins. Stablecoins have dropped from a peak of $190 billion to $125 billion, a decline of 34%, which is relatively mild compared to the drop in DeFi TVL, indicating that a lot of capital remains in the market. As for the decline in governance token prices, he provided several reasons: first, the DeFi Summer that began in 2020 marked the first cycle for the DeFi category, with most projects established after 2020. As tokens are unlocked, there is significant selling pressure on prices; additionally, this process is also a validation of models, with many overly Ponzi-like projects (such as Luna) being disproven, leading to the collapse of this bubble; finally, regulatory issues have had a significant impact on project operations, especially for operators in the U.S., which is also reflected in the prices of DeFi tokens.

Nothing Research partner Todd pointed out that DeFi tokens performed well in the bull market primarily because they enjoyed liquidity premiums. In simple terms, "Ethereum's price is too high, so investors buy the leaders in various tracks within the Ethereum network." However, in the bear market, funds perceive Ethereum as undervalued, leading to a return to Ethereum, thus eliminating the liquidity premium. Therefore, even though DeFi projects are withdrawing from new products and the products are better than before, prices have actually fallen.

In the view of PANews research director Haibo, due to the existence of liquidity mining, DeFi tokens are more susceptible to spiraling up or falling into a death spiral. When governance token prices rise, the APR for mining increases, attracting more funds and pushing governance token prices higher. Similarly, during market downturns, declining yields lead to capital outflows, further exacerbating the decline in governance token prices.

Has it fallen out of the "golden pit"? Projects with real yields are more favored

DeFi tokens have experienced a relatively significant decline in this bear market, but DeFi is also one of the few categories that can generate real yields. With the market downturn, metrics such as fees and price-to-earnings ratios have received more attention. Does this mean that DeFi's valuation has fallen out of the "golden pit"?

Source: Token Terminal

Mindao stated that after years of development, DeFi protocols now emphasize real yields. For example, the recently popular RWA track, which brings U.S. Treasury yields into DeFi, represents a reasonable evolution. From a valuation perspective, many projects' secondary market valuations are indeed attractive, but most projects have yet to find a sustainable path. Therefore, not every project has fallen out of the "golden pit" of valuation.

According to Haibo, compared to the previous valuation system relying on TVL or future expectations, using traditional financial metrics such as price-to-earnings (P/E) ratios to assess projects is an advancement. Only a few projects can clearly calculate P/E, with DeFi projects being representative. Among PoS mechanism public chains, ETH performs well under this valuation system, with a deflation rate of 0.2%, and staking ETH for a year yields about 4%. In contrast, the staking yields of almost all other PoS native tokens, minus the inflation rate, are negative. In the DeFi space, assets like MKR have P/E ratios below 25. With stricter valuation standards, there is greater certainty when bottom-fishing for assets with real yields, and the requirements for similar projects will also be stricter. Some projects that cannot generate yields or are continuously losing money may experience even greater declines in the bear market.

Hedy, chief researcher at OKLink, pointed out that the overall market is still relatively small and easily influenced by market sentiment, leading to frequent price-value discrepancies. This phenomenon can cause excessive prosperity or pessimism in the short term, potentially misaligning asset prices with their fundamentals. Additionally, in the Web3 industry, culture and consensus, or emotional value, are also amplified. Due to the decentralized nature of DeFi, a project's success often relies on community consensus and support. This culture and consensus can trigger fluctuations in emotional value in the market, further impacting asset prices.

Current practical strategies: ETH Staking and Maker DSR provide yield opportunities

In a bear market, opportunities for safely obtaining yields are reduced, and Maker's DAI deposit rate offers a good opportunity. Maker will use the collateral for issuing DAI to purchase short-term U.S. Treasury products and distribute the yields to DAI holders. As of October 16, the issuance of DAI stands at $5.55 billion, but only $1.69 billion DAI is deposited in the DAI Savings Rate (DSR) contract. Even if this portion of funds yields 5%, Maker would still have a net profit of about $70 million a year after costs. Following Maker, Frax also launched a product similar to sDAI in its V3 version this month, currently offering a yield of 6.85%.

Due to the zero-cost exchange between USDC and DAI through Maker's Peg Stability Module (PSM), and with an initial yield set at 8%, some yield strategies combining ETH liquid staking and Maker DSR have emerged. On August 7, Shen Yu shared a strategy of staking ETH through Lido as wstETH, using wstETH as collateral in MakerDAO to mint DAI, and then depositing DAI into DSR, which could generate an income of 50 ETH and 25,000 DAI from an investment of 1,000 ETH over a year.

Todd shared his asset holdings and yield strategies. He mentioned that a lot of funds are currently in SparkDAO, followed by ETH Staking, corresponding to the two largest positions, ETH and USDT, both with average yields around 4-5%.

In addition to the highly regarded Maker DSR, Haibo believes there are other options from a yield perspective, such as Frax's sFRAX, which offers yields comparable to Maker DSR. For those seeking higher yields, ETH liquid staking derivatives could consider providing liquidity for wstETH/ETH or sfrxETH/frxETH on some mature DEXs (like Velodrome). Stablecoins could explore opportunities on new public chains, such as the MOD stability pool in Thala on Aptos or providing liquidity for MOD/USDC, with higher yields implying greater risks. Furthermore, after Maker's business logic has been proven profitable, many projects claiming to provide real yields through real-world assets (RWA) have emerged in the market. Since participating in such projects requires trust in off-chain entities, investors need to be cautious in distinguishing between genuine and fraudulent projects. Undoubtedly, long-standing projects like Maker with a solid background are more trustworthy.

Promising tracks for the future: native yield, RWA, stablecoins, and infrastructure

Starting from lending and trading, DeFi has developed multiple tracks, each with its own opportunities and challenges. For instance, in DEXs, even leading platforms like Uniswap, which serve numerous users, cannot provide any returns to the protocol and UNI token holders; on-chain derivatives exchanges, while considered to have vast growth potential, currently rely heavily on trading mining to capture market share.

Regarding promising DeFi sub-tracks for the future, Todd particularly emphasized projects that can generate native yield. Although some DeFi projects can bring traditional yields into crypto, which helps retain existing capital, it is clear that generating native yields is the key to attracting new users in the future.

Mindao focuses on decentralized stablecoins, stating that DeFi, as the financial infrastructure of crypto, is fundamentally centered around decentralized stablecoins. "We have recently seen decentralized stablecoins increasingly incorporating RWA asset yields. The combination of decentralized stablecoins, RWA real yields, and LSD assets presents many opportunities in this sub-field."

Hedy believes that with the development of DeFi, the importance of certain infrastructures is gradually becoming prominent. Currently, there is sustained optimism for areas such as Web3 wallets, cross-chain solutions, and on-chain data tracks. These infrastructures play a crucial role in promoting the development of the DeFi ecosystem and realizing its true significance. Additionally, RWA is worth paying attention to as it connects the outside world with DeFi. The integration of RWA will further promote the fusion of DeFi with the real economy, providing broader application scenarios and opportunities for DeFi.

The value of DeFi projects has already become apparent. In a bear market, "survival" is the most important thing. DeFi is a rapidly developing field, and almost all leading DeFi projects are actively iterating and updating. Perhaps some of the existing projects will become the engines driving the next bull market.

Risk warning

Risk warning Risk warning

Risk warning