EMC Labs November Briefing: Internal Awareness and External Response, the Fifth Bull Market is About to Unfold

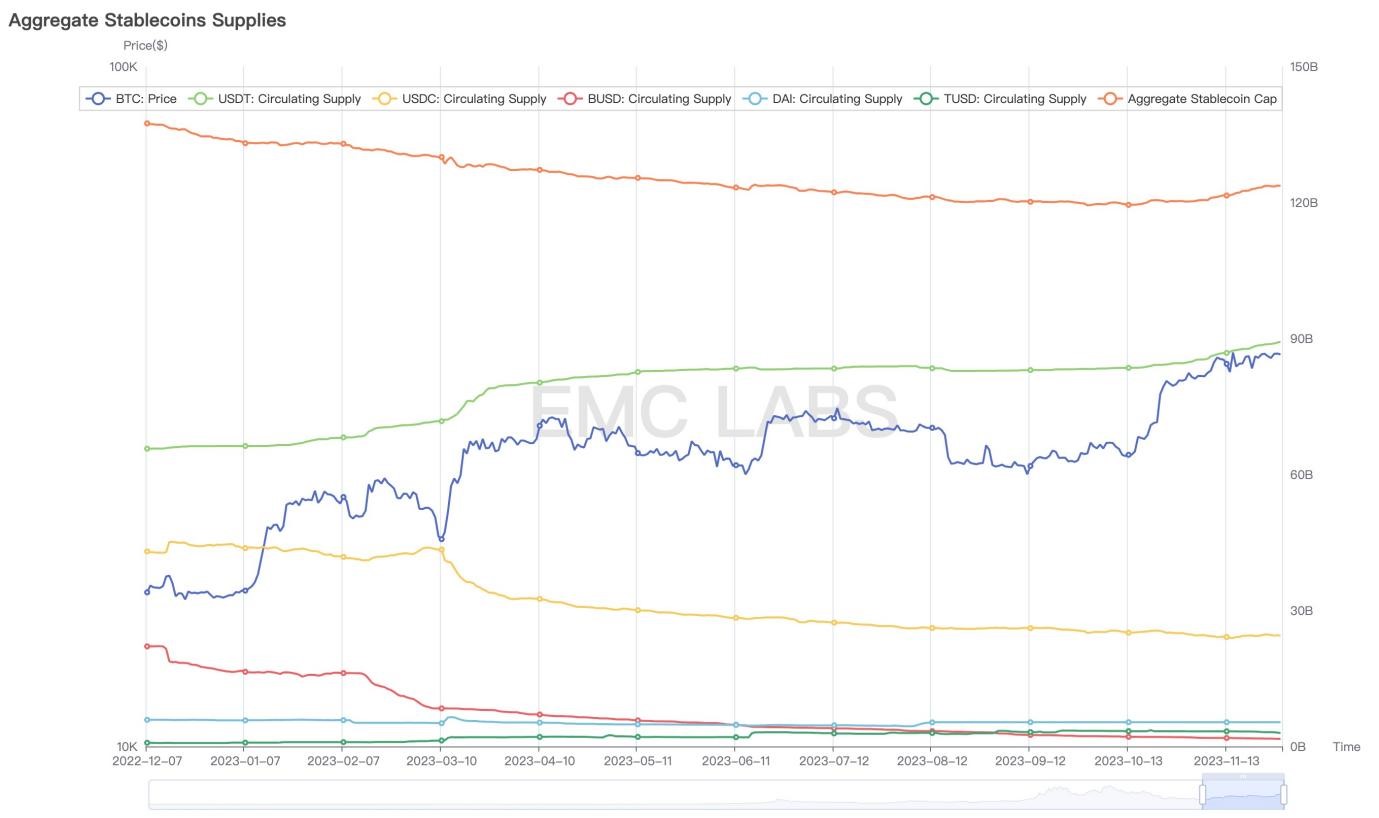

The continuous inflow of external funds is a necessary condition for the initiation of a bull market. In November, stablecoins achieved the second positive inflow month of the year, with an inflow scale of 3.5 billion dollars, nearly 3.5 times that of October.

The continuous inflow of external funds is a necessary condition for the initiation of a bull market. In November, stablecoins achieved the second positive inflow month of the year, with an inflow scale of 3.5 billion dollars, nearly 3.5 times that of October.Written by: 0xWeilan

(The information, opinions, and judgments regarding markets, projects, currencies, etc., mentioned in this report are for reference only and do not constitute any investment advice.)

Macroeconomic Market

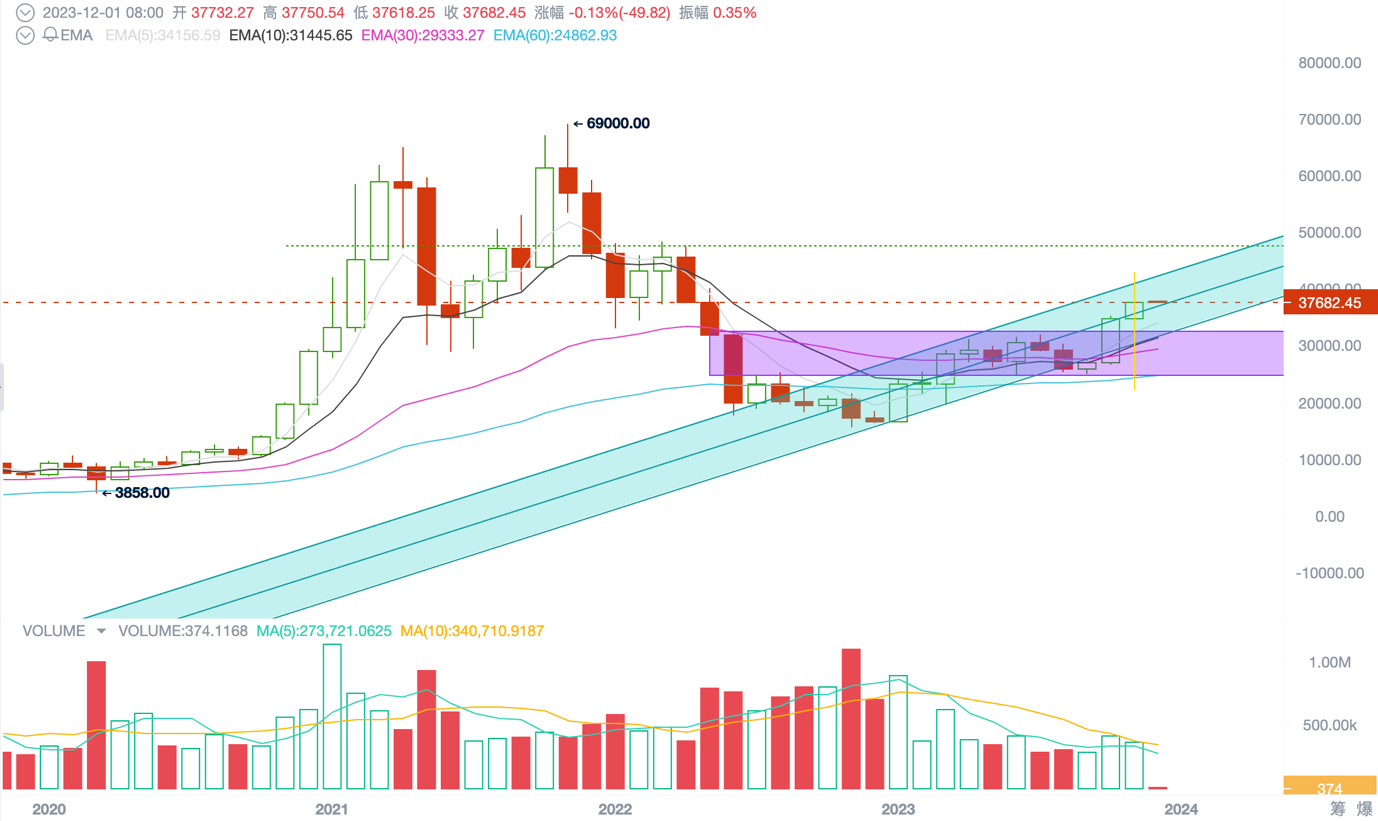

As predicted by EMC Labs in the October Briefing, after achieving an annual breakthrough in October, BTC continued to oscillate upward along the rising channel in November, pushing the price to around $38,000.

After consecutive increases of 28.54% and 8.88% in October and November, respectively, the profit level for BTC holders reached its highest point of the year. The locking in of profits and concerns over high-level consolidation have caused BTC to continue oscillating near the mid-point of the rising channel (around $37,000), with trading volume shrinking.

BTC Monthly Chart

++Although there is still one month left in this year, all parties in the market generally agree that the current interest rate hike cycle has ended. Labor employment data has begun to decline, and a mild recession in the U.S. economy has started, with major investment banks beginning to predict the start of a rate cut cycle—sometime in the summer or second half of 2024.++

In this context, the U.S. dollar index recorded a 3% decline for the month, indicating that expectations for easing are growing stronger, and funds are beginning to flow into riskier equity assets.

The macro financial market has started to turn upward. The Nasdaq, which had fallen for three consecutive months, rebounded significantly near the October moving average, achieving a monthly increase of 10.7%.

Nasdaq Monthly Chart

This month, Binance, the largest centralized exchange globally, which has played a significant role in industry development and thus posed challenges to the old system, reached a settlement with the U.S. Department of Justice, bidding farewell to its wild past with a hefty fine of $4.3 billion and the resignation of its founder as CEO. ++The overall market attitude towards this is optimistic, although not all "black swan" level uncertainties have been cleared. We tend to believe that the crypto industry is bidding farewell to the era of wild development, and in the coming years, compliance development that connects with the traditional world will become mainstream.++

This is the pain of adulthood, as well as a medal covering the wounds. Only then can crypto technology deeply integrate into human society, and the crypto market may reach a scale of $10 trillion in the coming years, becoming one of the largest equity markets for humanity.

Crypto Market

In November, BTC opened at $34,656 and closed at $37,732, achieving an increase of 8.88% for the month, with a volatility of 12.7%.

The most significant market achievement for BTC this month was completely breaking free from the oscillating box that had troubled its movement for half a year (the purple area in the chart below), operating above $34,000, which was the high point after the breakthrough in October. Although trading volume has shrunk, it continues to push upward amid hesitation and ambiguity.

The mid-point of the rising channel (the green box in the chart below) has also become the focal point of contention between bulls and bears. On November 15/16 and 20/21, both sides engaged in fierce clashes near the mid-point. The trading volume on conflict days showed an increasing trend, indicating a strong determination from both profit-taking sellers after a significant rise and new funds entering the market.

BTC Daily Chart

Ultimately, the bullish forces prevailed, and despite several technical indicators applying pressure, the BTC price maintained a strong upward trend, reaching new highs in the rebound.

++A more positive aspect is reflected in the L1 sector outperforming BTC's monthly increase. ETH rose by 13.08% this month, outperforming BTC by 5,500 basis points, while L1 altcoins like SOL, AVAX, and OSMO have seen increases of up to three times since the launch in October, faintly indicating a trend of funds flowing from BTC into segmented sectors.++

The continued outperformance of ETH over BTC is one of the signs of a bull market and is worth close attention.

Capital Supply

Through technical analysis, we can understand the trend changes in the static market. However, the main driving force behind the market since October has been the accelerated inflow of off-exchange funds. To make judgments about the future market, we must analyze this primary factor in depth.

Following a positive inflow in October, stablecoins continued to see net inflows in November, with the inflow scale expanding to $3.5 billion, 3.5 times that of October. EMC Labs pointed out in the October briefing titled "EMC Labs October Briefing: As Expected Breakthrough! BTC Likely to Oscillate Upward Along the Channel": "The outflow trend reversed in October, and stablecoins achieved a single-month net inflow. Stablecoins have begun to emerge from the bear market."

In November, this judgment continued to be realized. BTC has emerged from the bear market since the beginning of the year, stablecoins have emerged from the bear market in October, and the overall bull market for crypto assets is getting closer!

Total Supply of Stablecoins

This month, stablecoins accelerated their inflow. ++EMC Labs believes that if stablecoins continue to maintain inflows in December, they will confirm their entry into a bull market. Coupled with BTC, which has already emerged from the bear market, the most optimistic estimate is that the market will enter the early stage of the fifth crypto asset bull market as early as January.++

Although the overall supply of stablecoins only turned positive in October this year, the supply of USDT had already shifted from outflow to inflow since December 2022, reaching a historical supply high in October. This early inflow of funds, along with on-exchange funds, helped to capture the historical fourth bottom of Bitcoin and contributed to the strong rebound of 130% that Bitcoin achieved in the first 11 months.

++Compared to the overall net inflow in October, the most significant achievement of the stablecoin market this month is that USDC has also ended its outflow status and started to achieve net inflows. This indicates that traders using these two types of stablecoins are beginning to be optimistic about the future market and are starting to increase their positions.++

Supply Trends

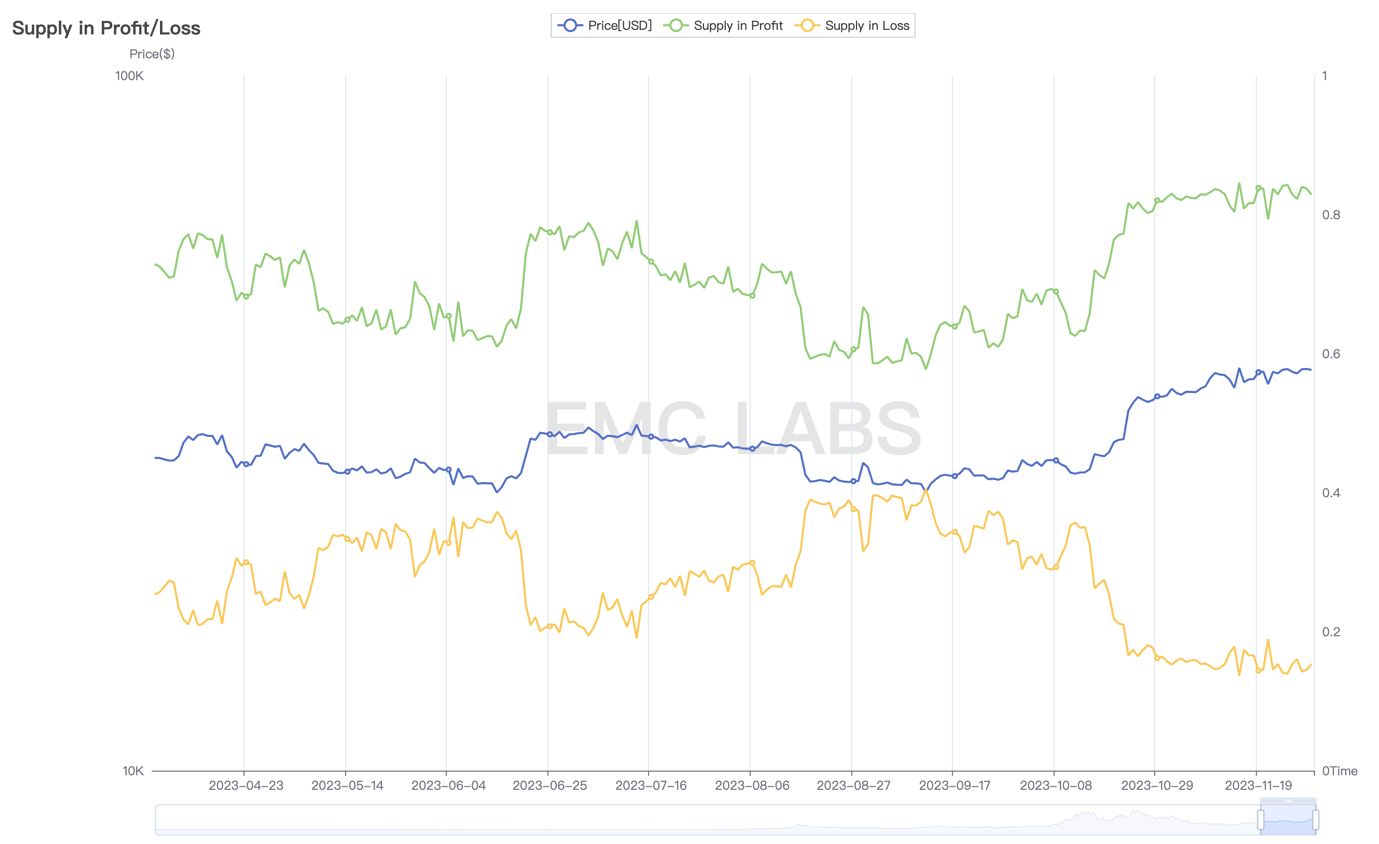

With the continuous rise in October and November, the overall supply of Bitcoin is becoming increasingly optimistic. This is an internal factor that we must continue to pay attention to, aside from net inflows of funds.

By the end of the month, 87% of Bitcoin's total supply was in profit. This is due to the rise in BTC prices and the large-scale capitulation and bottom-fishing that occurred during the bottoming and recovery periods.

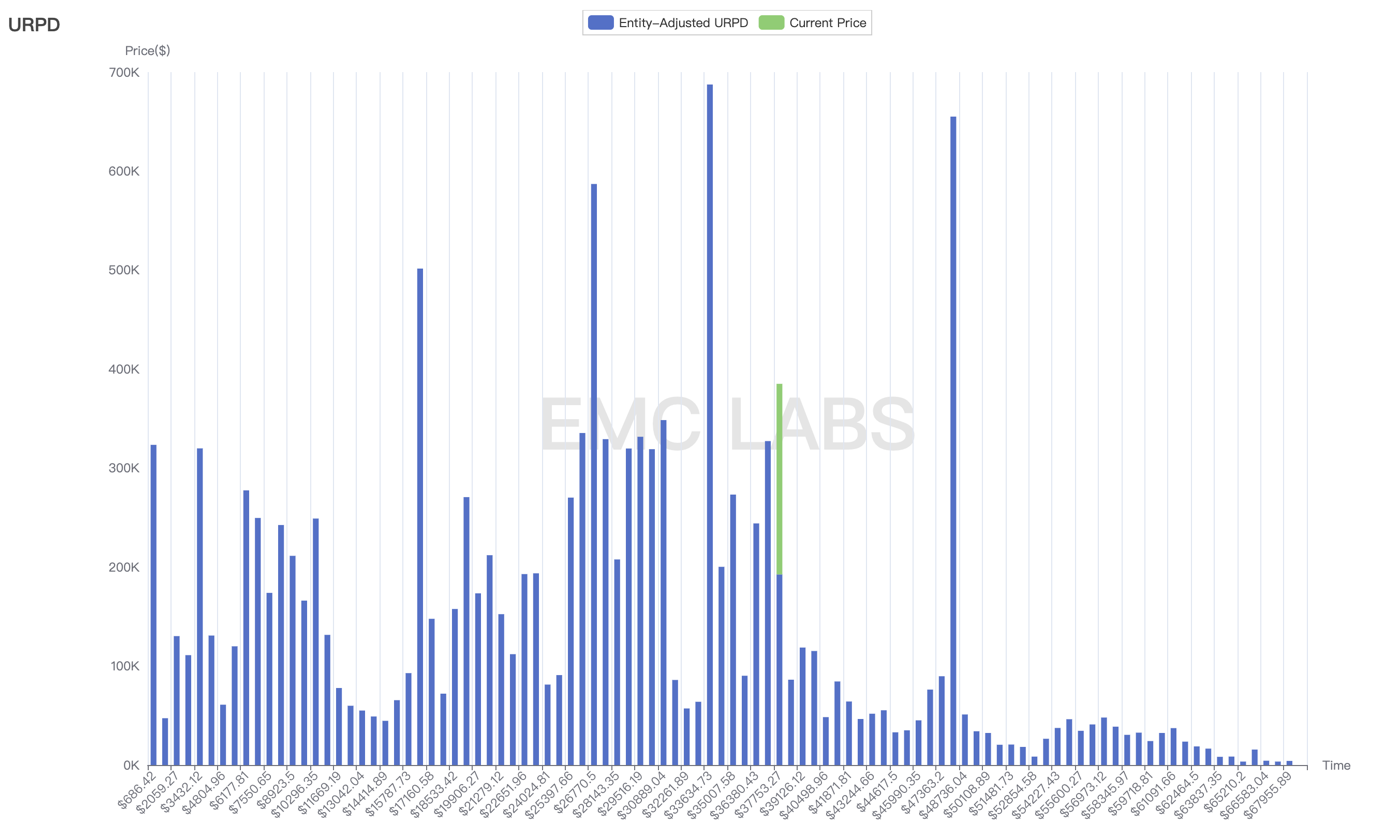

BTC Overall Supply Profit and Loss Distribution

Correspondingly, BTC's cost structure has also undergone significant changes------

BTC Overall Supply Cost Distribution

$33,634 has become the largest accumulation area, with most of these positions being built in October. This is also one of the reasons we judged in the October briefing that the market in November would not correct but continue to rise.

++Above that is $48,000, which is the accumulation area formed during the last bear market decline, and it is also where we judge the peak of the recovery period to be. This peak may be reached in December or January.++ Judging the price is almost meaningless, but if realized, December could see a significant double-digit increase.

Long-Short Game

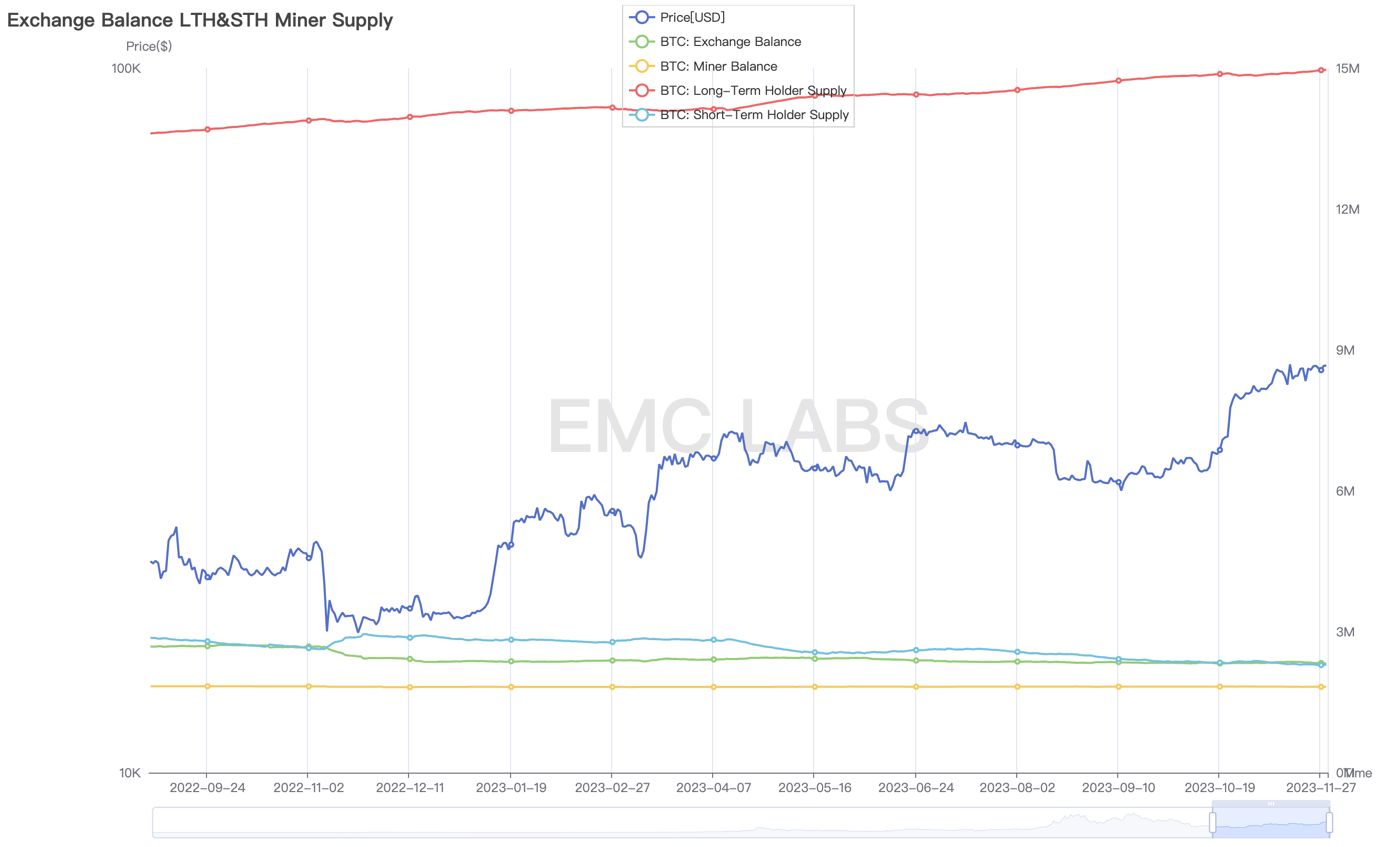

Looking at the positions of long and short hands and exchanges throughout November------

Market BTC Position Scale

Longs: +110,000, to 14.96 million;

Shorts: -70,000, to 229,000;

Exchanges: -40,000, to 232,000.

Longs are still accumulating positions, while shorts are still giving up positions. This performance aligns with the convergence trend of "continuous loss of liquidity" during the recovery period. The continuation of this trend makes it difficult for the short-term market to experience a significant decline.

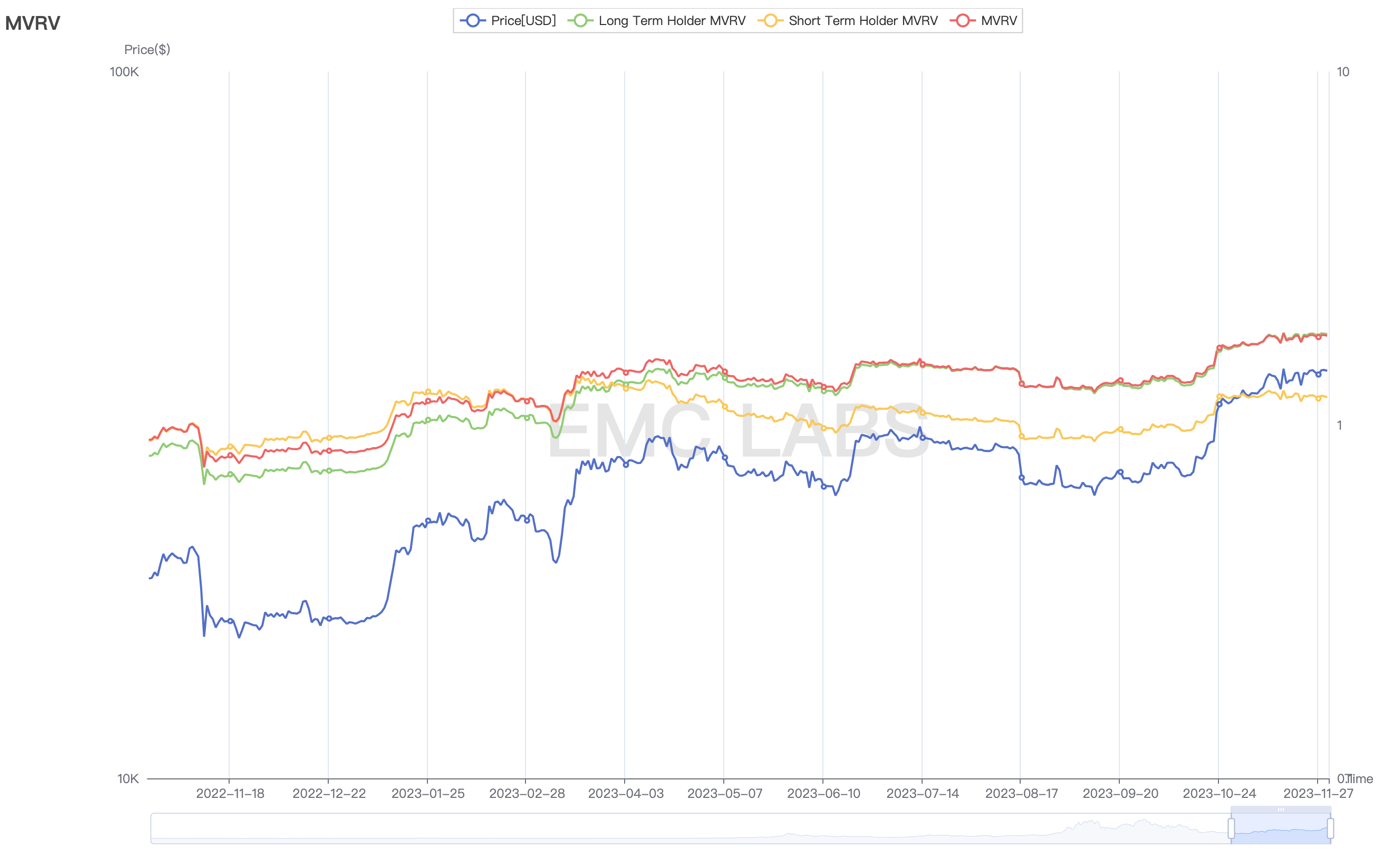

Next, let's look at the floating profit situation of longs and shorts. Longs have a floating profit of 81%, while shorts have 21%. Compared to October, the floating profit of longs continues to rise, while the floating profit of shorts has slightly decreased by 1%, remaining at a high level for shorts.

Floating Profit Situation of Longs and Shorts

During the recovery period, profit levels will gradually recover, and as the recovery period progresses and optimism about future trends increases, the floating profit threshold for all market participants will gradually rise.

Continuing to examine the profit-locking situation: the profit level for selling longs is between 30% and 70%, while the profit level for selling shorts is between 0% and 3%.

From the profit level of longs, those weak hands among the longs are selling (their profit levels are below the overall profit level of longs).

From the profit level of shorts, those strong hands among the shorts choose to hold (the profit level of sellers is far below the overall profit level of shorts).

++The market is currently in the late stage of the recovery period. During this period, the profit expectations of longs are getting higher (after entering the upward phase, i.e., the bull market, their expectations will increase several times), while the profit expectations of shorts are also gradually rising.++ At the same time, the weak hands among shorts and the weak hands among longs have become the last "clearing" targets, and the positions accumulated by longs this month come from this part of market participants.

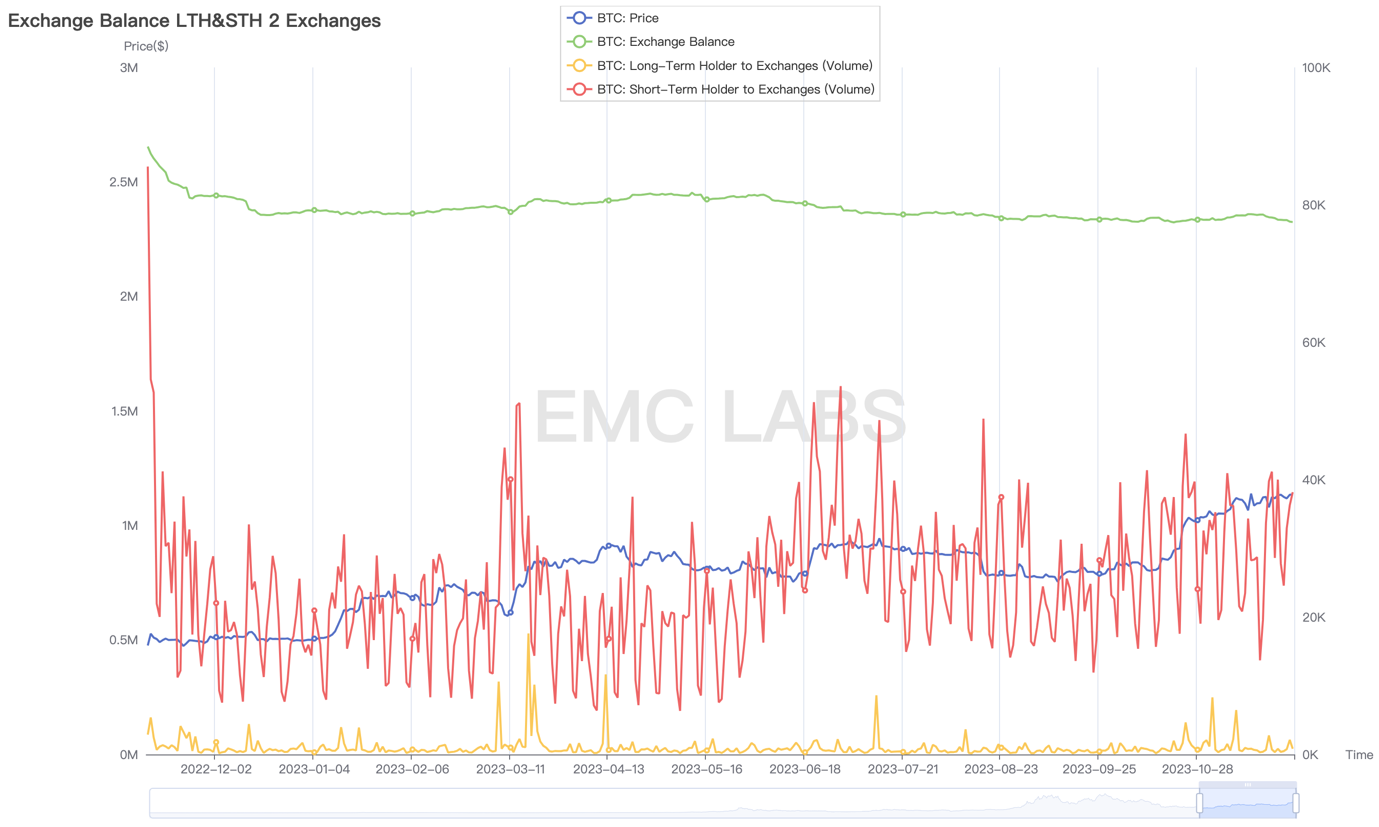

Revisiting the selling scale of longs and shorts in November------

Longs experienced significant sell-offs on November 2, 10, 21, and 28, selling 21,653 BTC over four trading days.

Shorts experienced significant sell-offs on November 7, 21, 22, and 24, selling 161,839 BTC over four trading days.

This reflects the selling situation of weak hands among the long and short groups. Compared to other months of this year, the overall selling level is on a downward trend, which also indicates that all parties in the market maintain an optimistic outlook for the future.

Long-Short Selling Scale Statistics

In summary, regarding the crucial long-short game in the market, EMC Labs maintains its previous judgment: ++The market is still in the recovery period, with positions continuing to "shift from short to long," and liquidity further diminishing. Although both longs and shorts have set historical records for floating profits during this recovery period, the selling scale has not expanded. The market has entered the late stage of the recovery period, and the upward phase, i.e., the "bull market," is faintly emerging.++

On-Chain Data

On-chain data serves as a stabilizer for BTC prices; price increases supported by on-chain data are more sustainable, while increases or decreases that diverge from on-chain data are bound to be unsustainable.

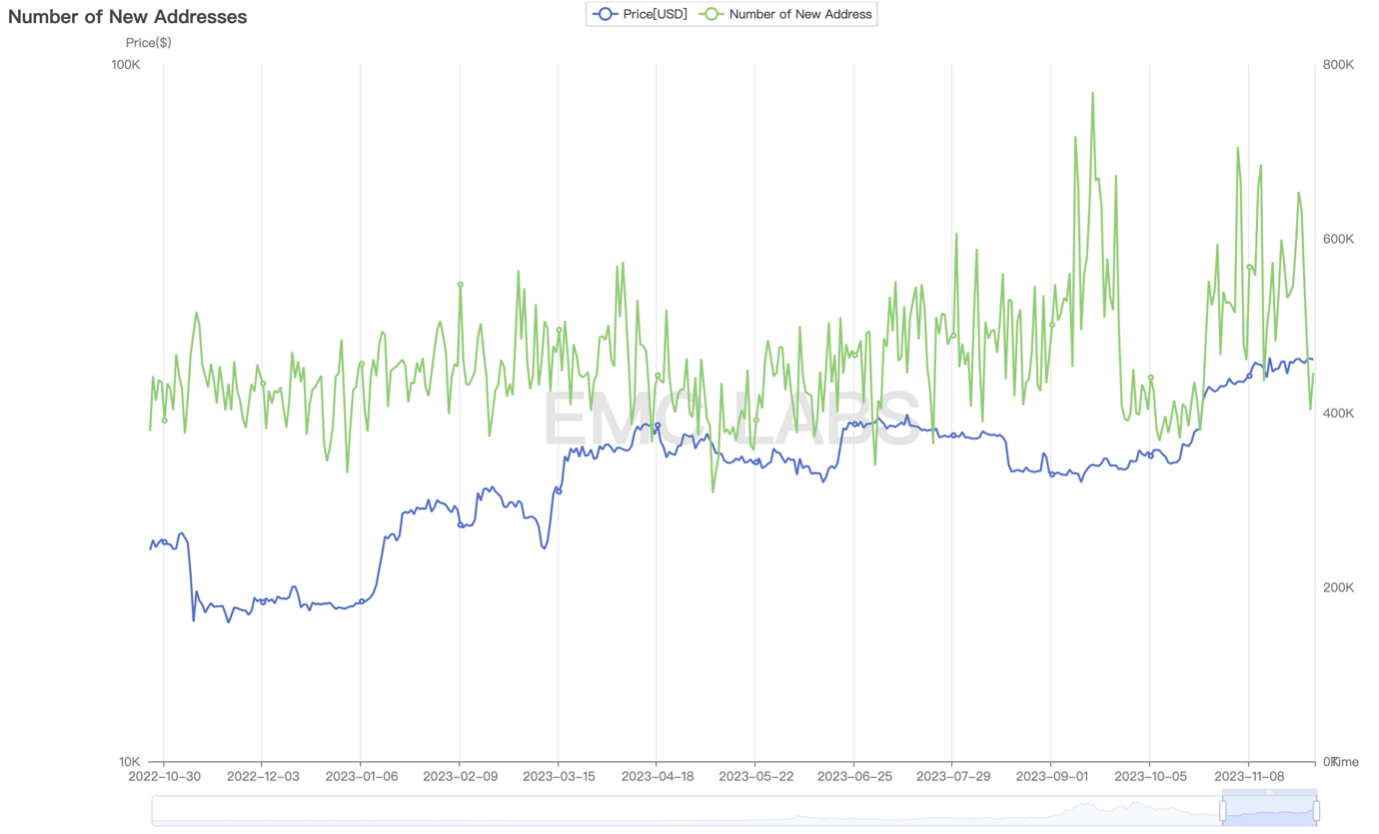

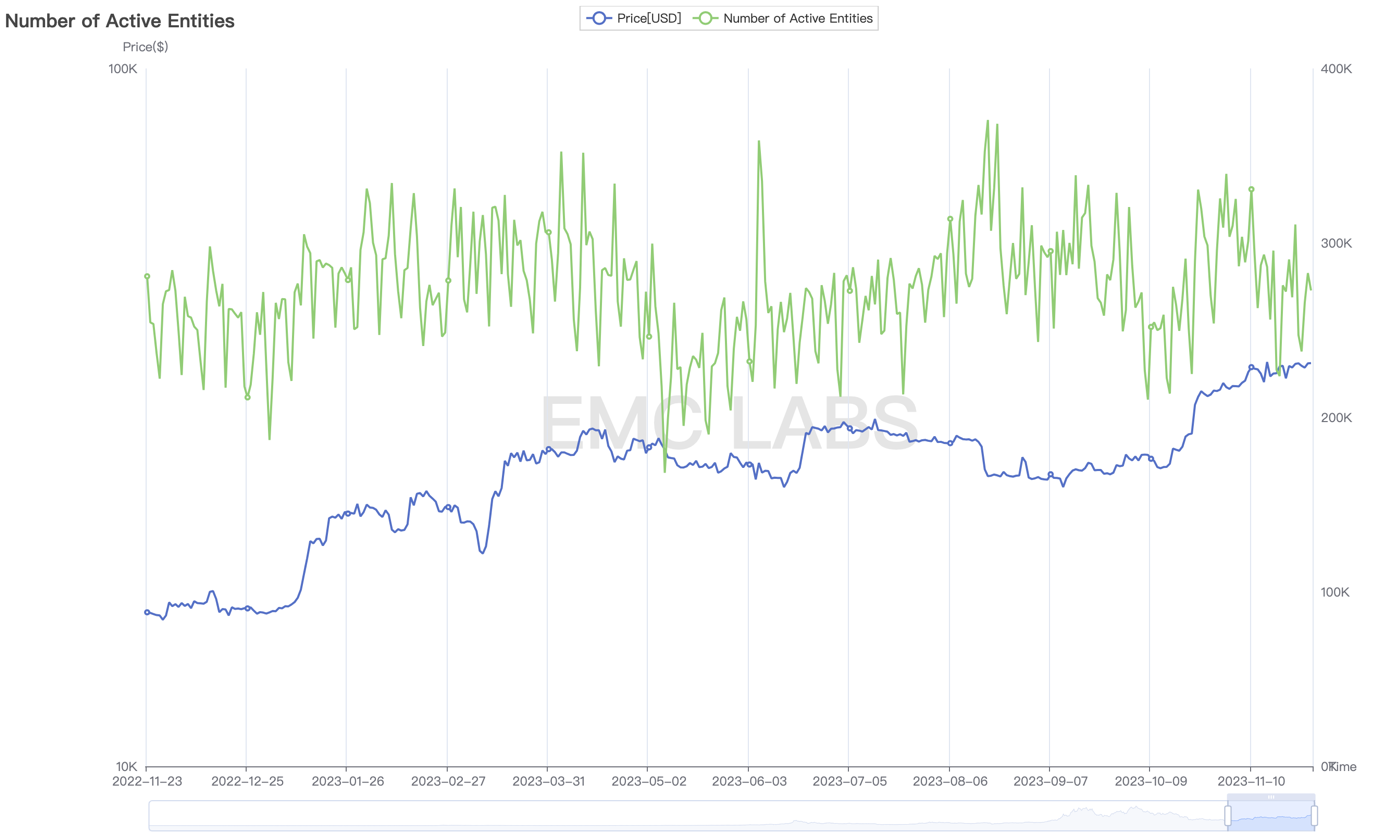

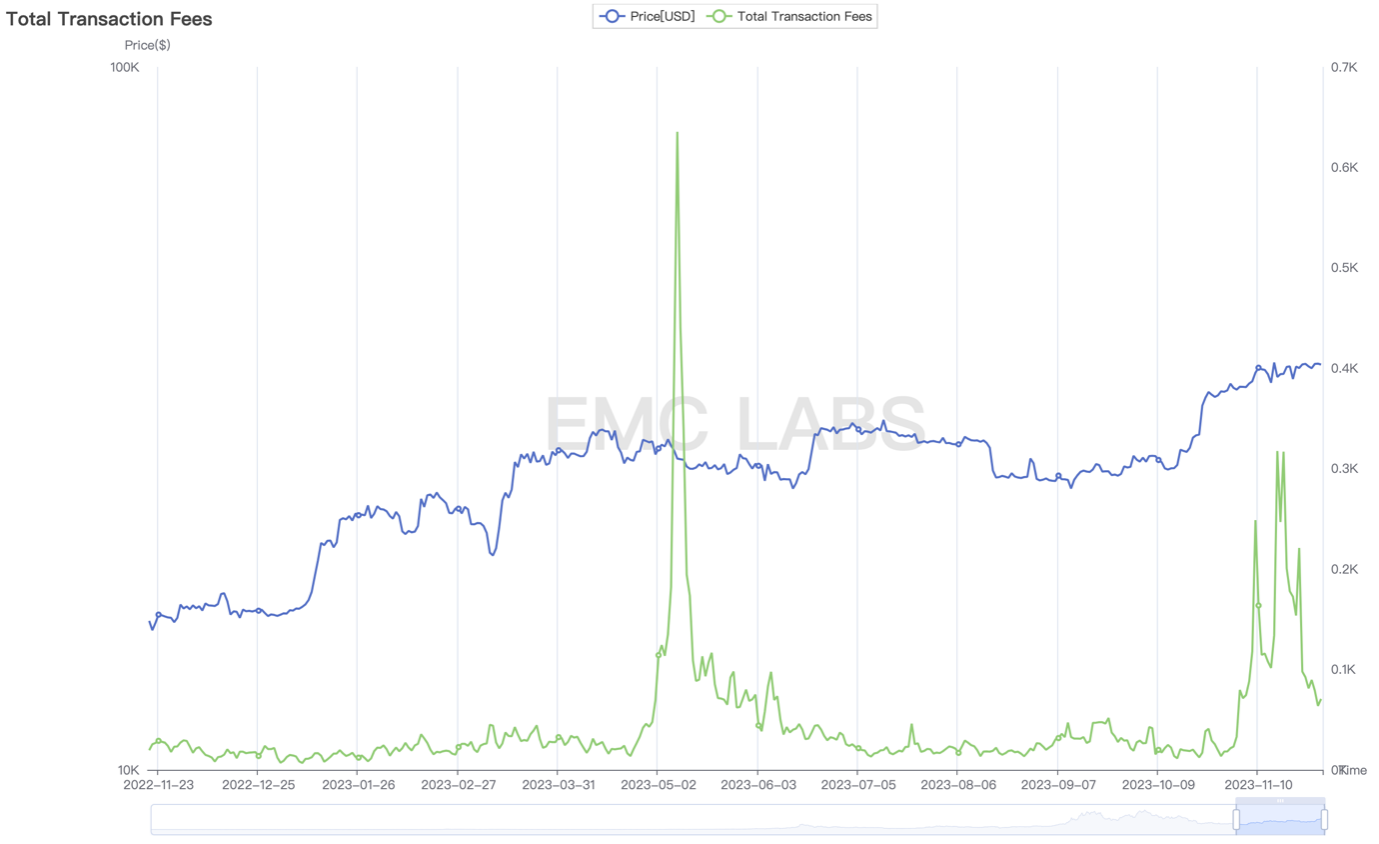

In October, we observed significant declines in the number of new addresses, daily active entities, transaction volume, and miner revenue. This divergence was effectively corrected in November.

New Addresses on the Bitcoin Network

Active Entities on the Bitcoin Network

Miner Gas Revenue on the Bitcoin Network

Since the rise of Ordinals assets, especially the BRC-20 MEME tokens, in April this year, over 30,000 BTC have entered miners' wallets as new "consumption-type" gas. Whether these tokens will become a new type of asset remains a significant debate, but the transaction surges triggered by the two waves of enthusiasm in April and November have indeed "polluted" the data. Therefore, we should view the on-chain data recovery in November with an objective perspective.

As the BRC-20 MEME craze cools rapidly, we need to observe further in December for the "bullish" trend based on accumulated and sold on-chain behaviors.

About the Bull Market

According to the Emergence Engine developed by EMC Labs, the repair period index has been at the maximum of 100 for nearly a month. Historically, if this duration reaches two months, the market will enter a bull market.

The EMC Labs repair period index integrates multi-dimensional on-chain data, reflecting the internal factors of the market. The external factors, namely the capital inflow situation, are also very optimistic. October saw the first net inflow of the year, and November's inflow scale reached 3.5 times that of October. If December continues to accelerate inflows, the inflow duration will reach three months. Three months is a sufficient period for judging medium to long-term trends.

++The last month of 2023 is very important; it serves as a dual focus for examining the internal and external factors of the crypto asset market. The light emitted from this focus illuminates the next bull market.++

This is the conclusion drawn by EMC Labs based on objective data from the Bitcoin network.

Challenges still exist------

For example, the mild recession in the U.S. has just begun, and the equity market may adjust downward, potentially affecting the inflow of stablecoins?

January 2024 is the final response time for U.S. BTC ETF applications. If the applications are rejected, the crypto market may enter an adjustment phase.

After Binance, will other exchanges, public chains, or stablecoin issuers be prosecuted by the U.S. Department of Justice or SEC?

After the bankruptcy of FTX, asset disposal parties are selling billions of tokens to the market. Will significant sell-offs by a single entity disrupt the market rhythm?

In the face of the already-promoted internal and external factors, we prepare for the most aggressive positions; in the face of uncertainty, we should control risks strategically. If so, this "uncertainty" becomes less significant.

We eagerly anticipate the arrival of December and are prepared to share our conditions for determining the bull market and our main track hypotheses in the next monthly briefing.

Conclusion

November is an important month.

We have witnessed the recovery of on-chain data, the continued upward movement of BTC prices, the small-scale exit of weak hands, and the continuous rise in the floating profit thresholds for both long and short hands.

The crypto asset market welcomed the resolution of the hefty fine, USDC ended its divergence, and stablecoin supply saw large-scale inflows throughout the month.

December is an even more important month.

Amid ambiguity and anxiety, the "internal sense" and "external response" of the crypto asset market will approach a critical point.

The long recovery period is about to end, and the upward phase (bull market) is imminent!

Risk warning Risk warning

Risk warning Risk warning