SignalPlus Macro Analysis Special Edition: Return to Summer Doldrums?

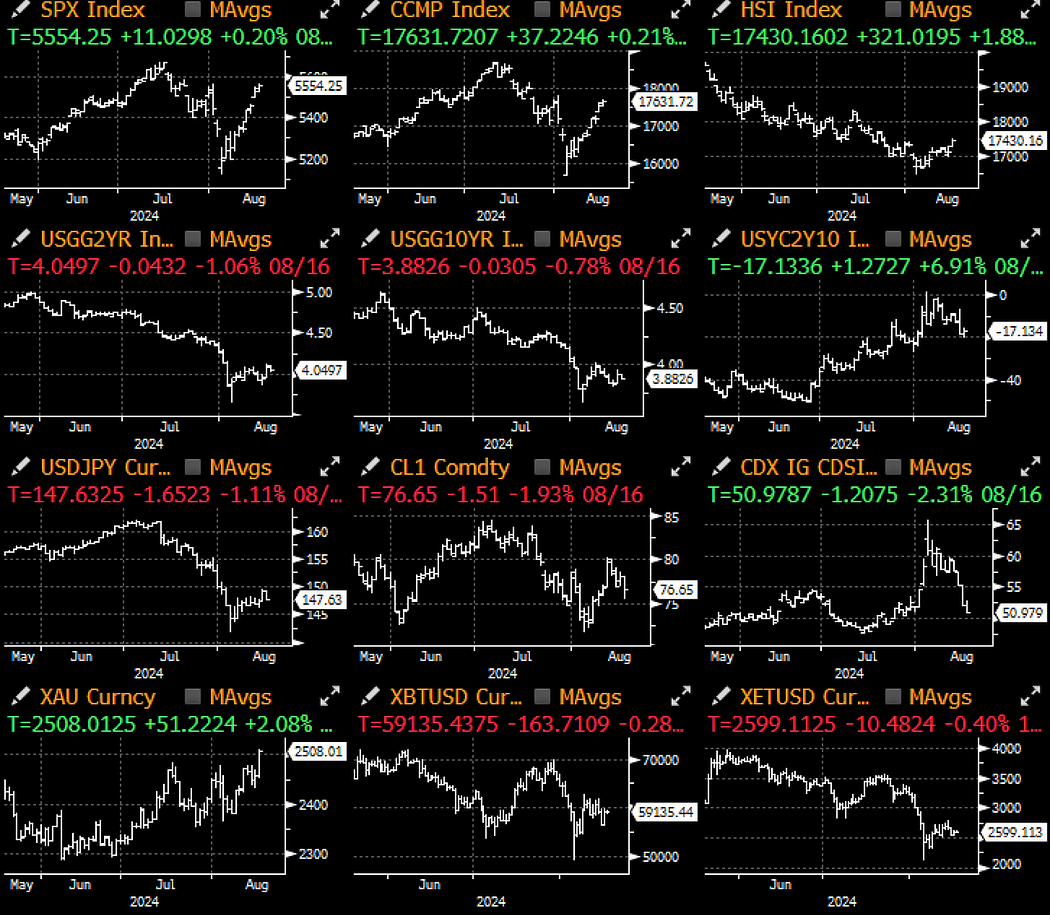

After the turmoil at the beginning of the month, the market seems to have entered the second half of the month as if nothing had happened. Due to strong retail sales data, a decline in unemployment claims, and decent corporate earnings reports, concerns about an economic recession have significantly eased, and the market has re-entered a "soft landing" mode...

After the turmoil at the beginning of the month, the market seems to have entered the second half of the month as if nothing had happened. Due to strong retail sales data, a decline in unemployment claims, and decent corporate earnings reports, concerns about an economic recession have significantly eased, and the market has re-entered a "soft landing" mode...

After the turmoil at the beginning of the month, the market seems to have entered the second half of the month as if nothing happened. Concerns about an economic recession have significantly diminished due to strong retail sales data, a decline in unemployment claims, and decent corporate earnings reports, leading the market to re-enter a "soft landing" mode.

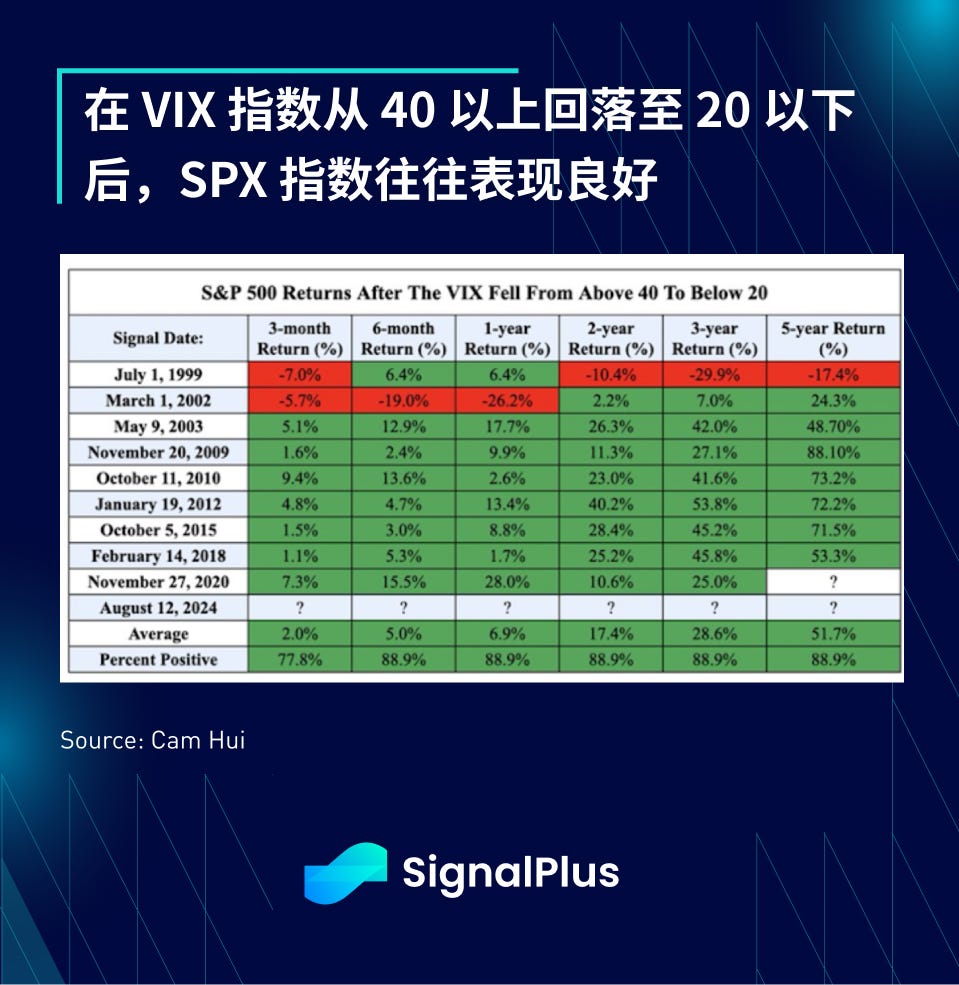

Additionally, according to Bloomberg data, the SPX growth index outperformed the value index by more than 4% in the past week, a situation that has only occurred 31 times in the past 20 years, with over 70% of those records seeing the market rise in the following week.

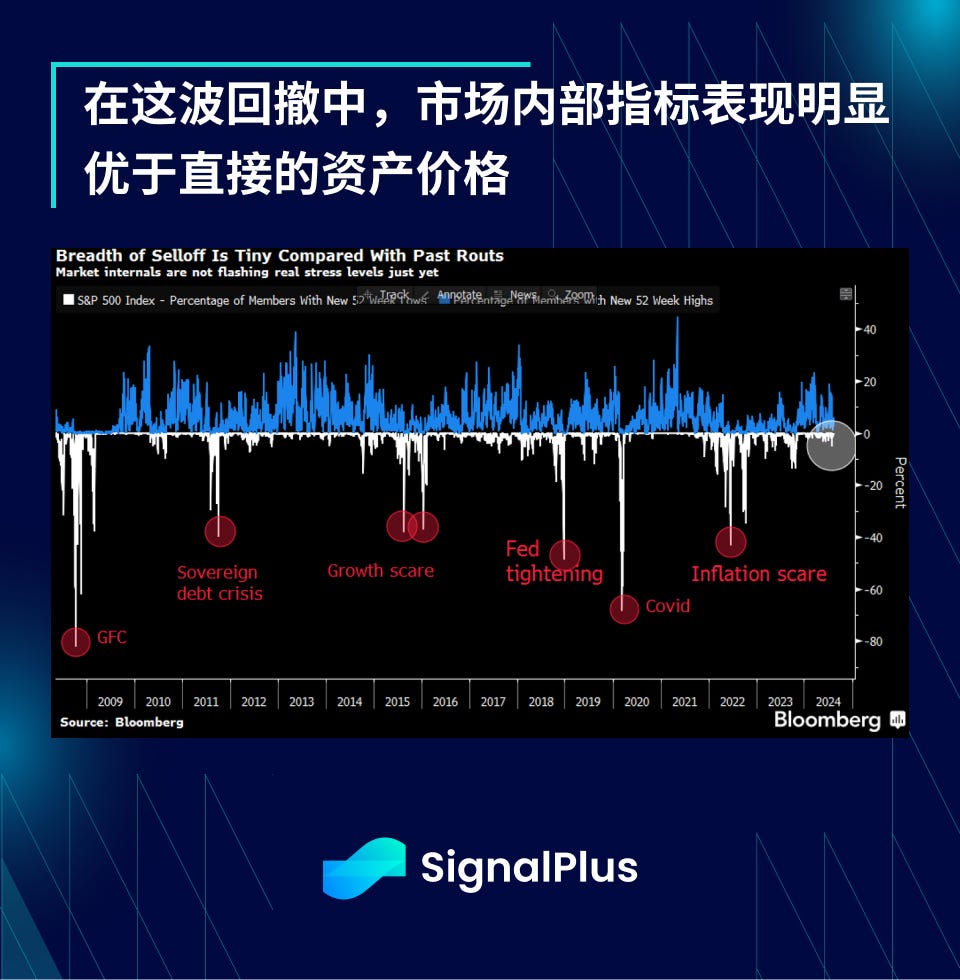

In fact, internal market indicators (measured by the number of stocks reaching 52-week highs and lows) did not show much panic during this volatility, further confirming that this wave of selling was primarily driven by positions and stop-losses rather than a change in long-term fundamental views.

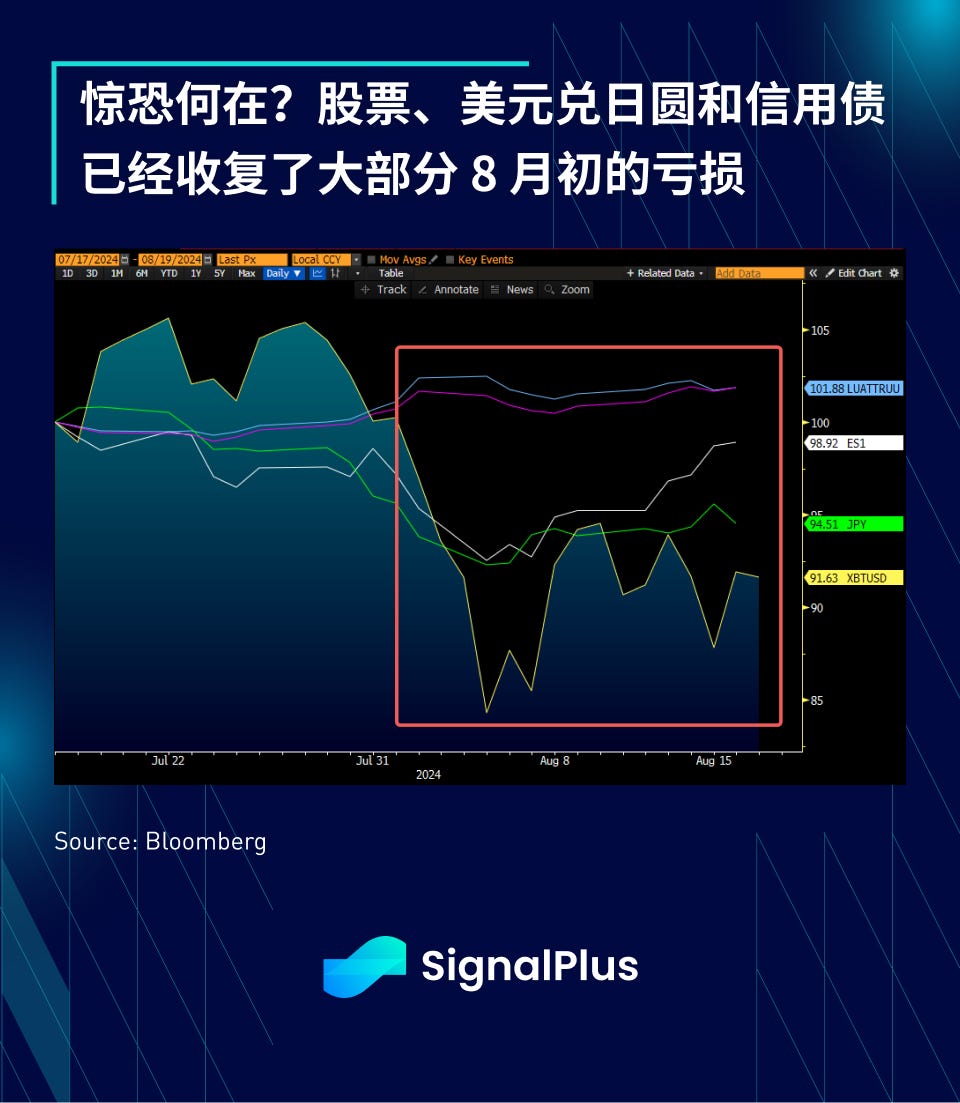

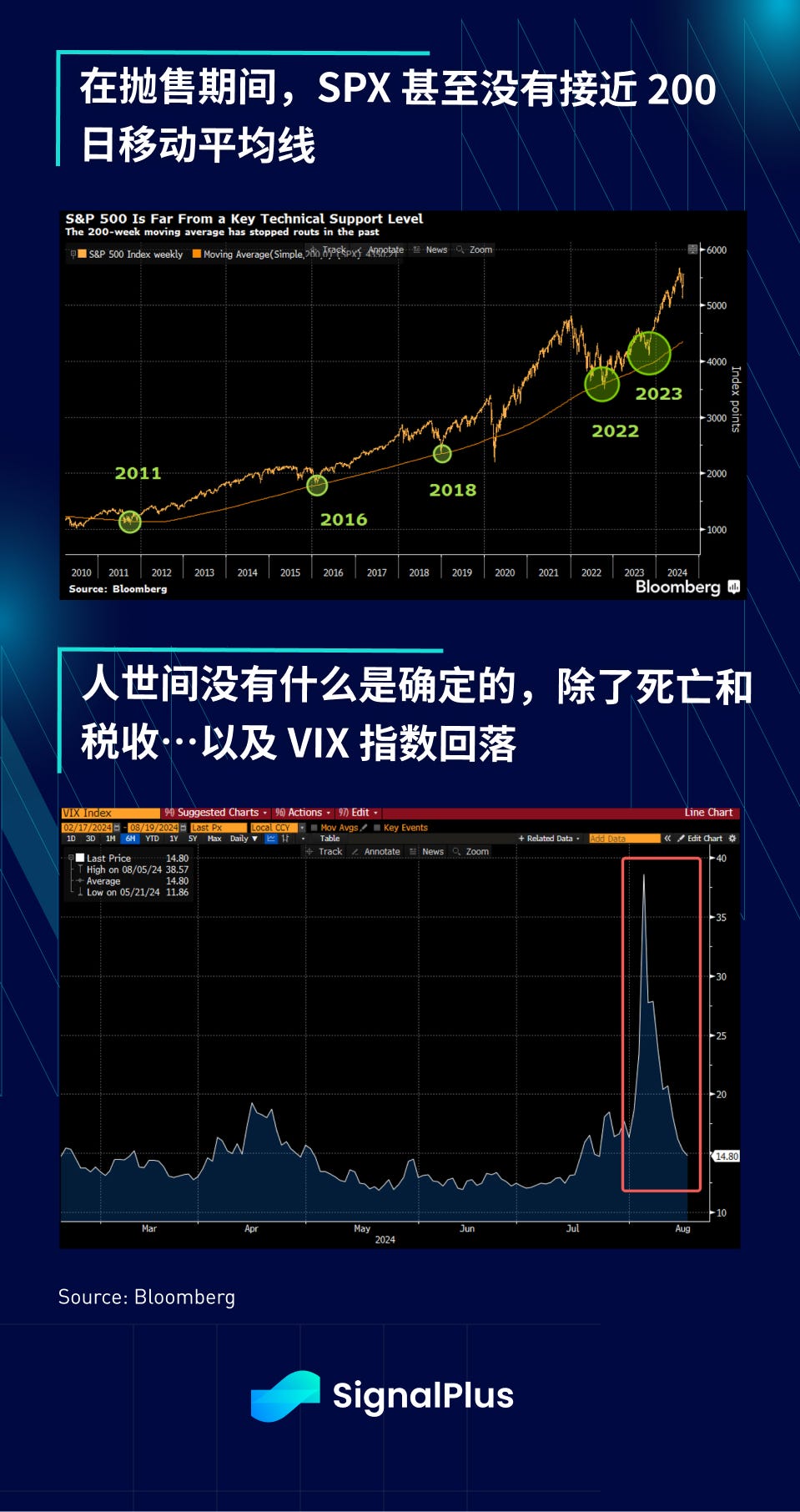

Moreover, Citigroup's estimates of market positions confirm that the de-risking behavior in August was mainly led by hedge funds, whose positions were subsequently taken over by "long-only" funds during the buying on dips. If we extend the time frame, this momentary drop in volatility is hardly noticeable on the long-term SPX chart, and the volatility index (VIX) has already retreated to this year's common range after a brief spike of less than a week.

From the perspective of individual companies, Walmart's earnings report exceeded market expectations and raised its guidance for fiscal year 2024, with its stock price rising 7% after the announcement. Other consumer brands like Home Depot and Starbucks also performed well, further alleviating market concerns about a significant slowdown in consumer spending.

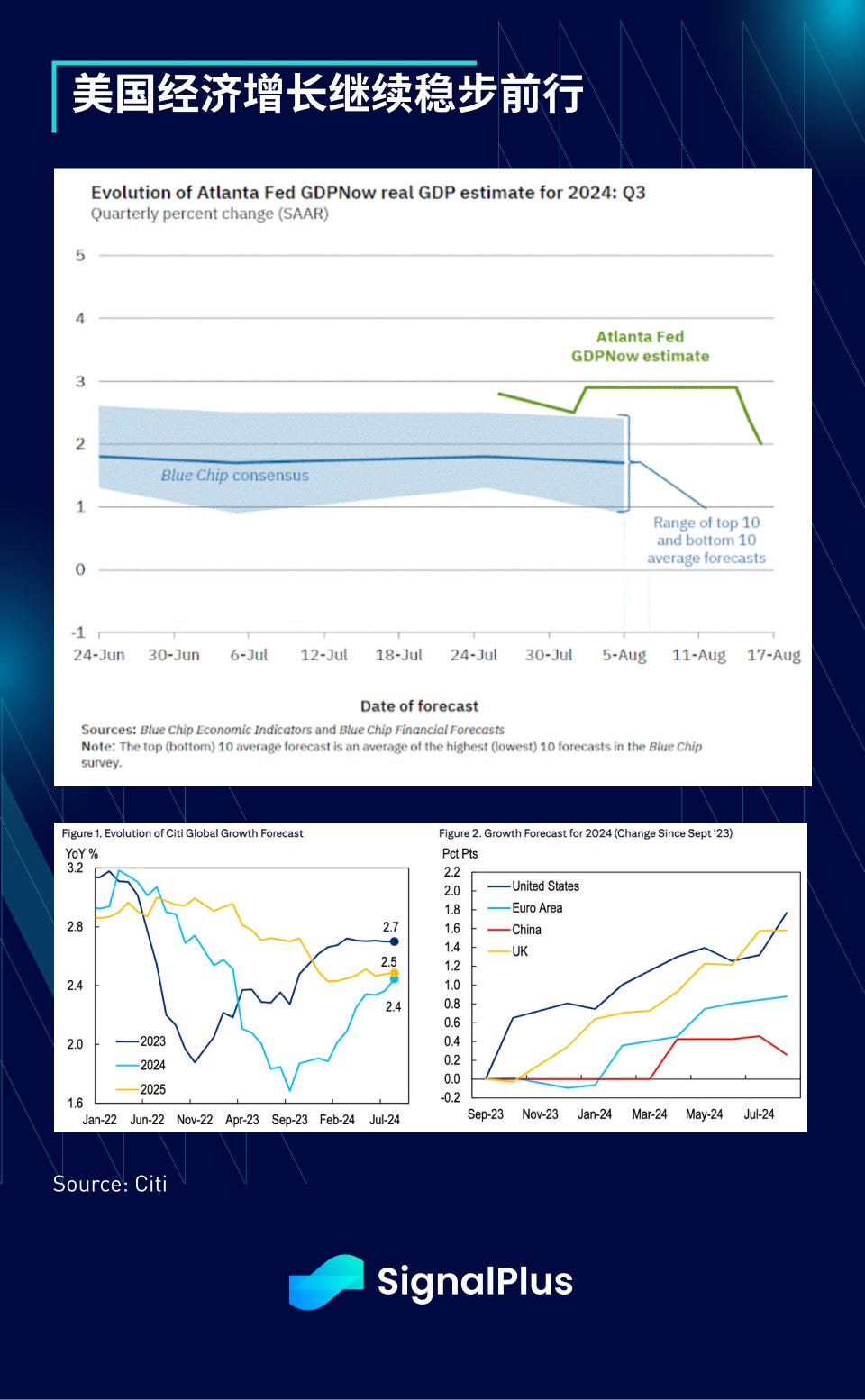

Overall, GDP growth for the third quarter has remained quite stable over the past two months, with the Atlanta Fed's GDPNow model predictions consistently hovering in the range of 2.5% to 3%. Additionally, Wall Street expects that, due to the support from the Federal Reserve, GDP growth in the U.S. (and the U.K.) will continue to lead in 2024, with growth in 2025 also expected to remain at similar levels.

In contrast to July, market expectations for Federal Reserve interest rate cuts have changed, with the market still anticipating nearly four rate cuts before the end of the year, and a 30% chance of a 50 basis point cut in September. However, due to the rapid market recovery and strong economic data, the Federal Reserve does not face the same significant dovish pressure as it did two weeks ago, and the market has entered a vacuum period as asset prices return to a wait-and-see state for more data.

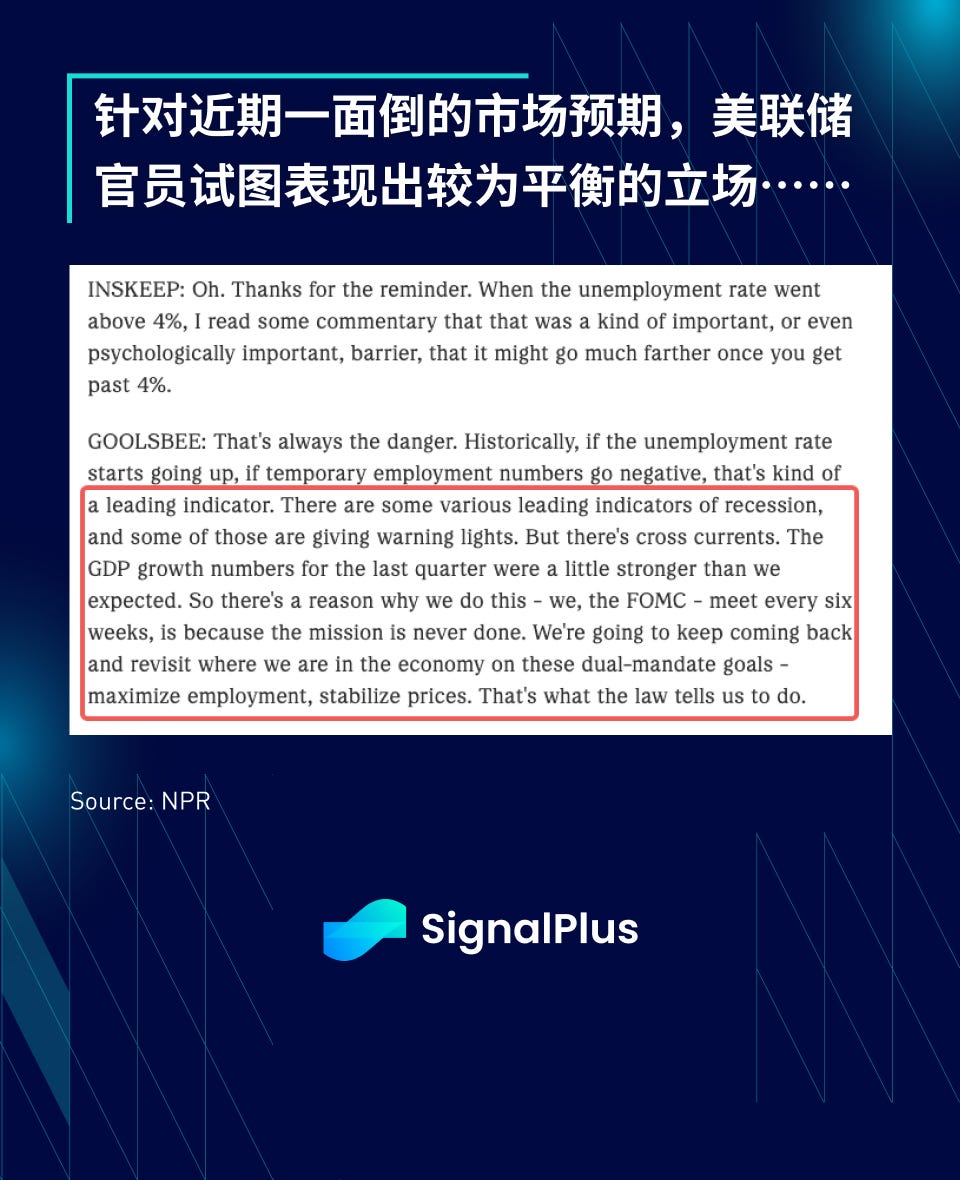

In fact, the Chicago Fed's well-known dove Goolsbee expressed a very cautious balanced stance in a recent interview, stating that the Federal Reserve should not overreact to certain recession indicators. Therefore, even though the market is eagerly anticipating, Powell may still adopt a more neutral tone at the highly anticipated Jackson Hole meeting, potentially disappointing the market. This means that Powell may only express support for a gradual easing plan while downplaying expectations for a 50 basis point rate cut in the context of rapidly easing financial conditions. He may also emphasize not to focus on a single non-farm payroll data result while keeping the option to accelerate rate cuts if the labor market deteriorates rapidly.

We believe Powell will act very cautiously and is unlikely to announce significant easing policies or information in the short term.

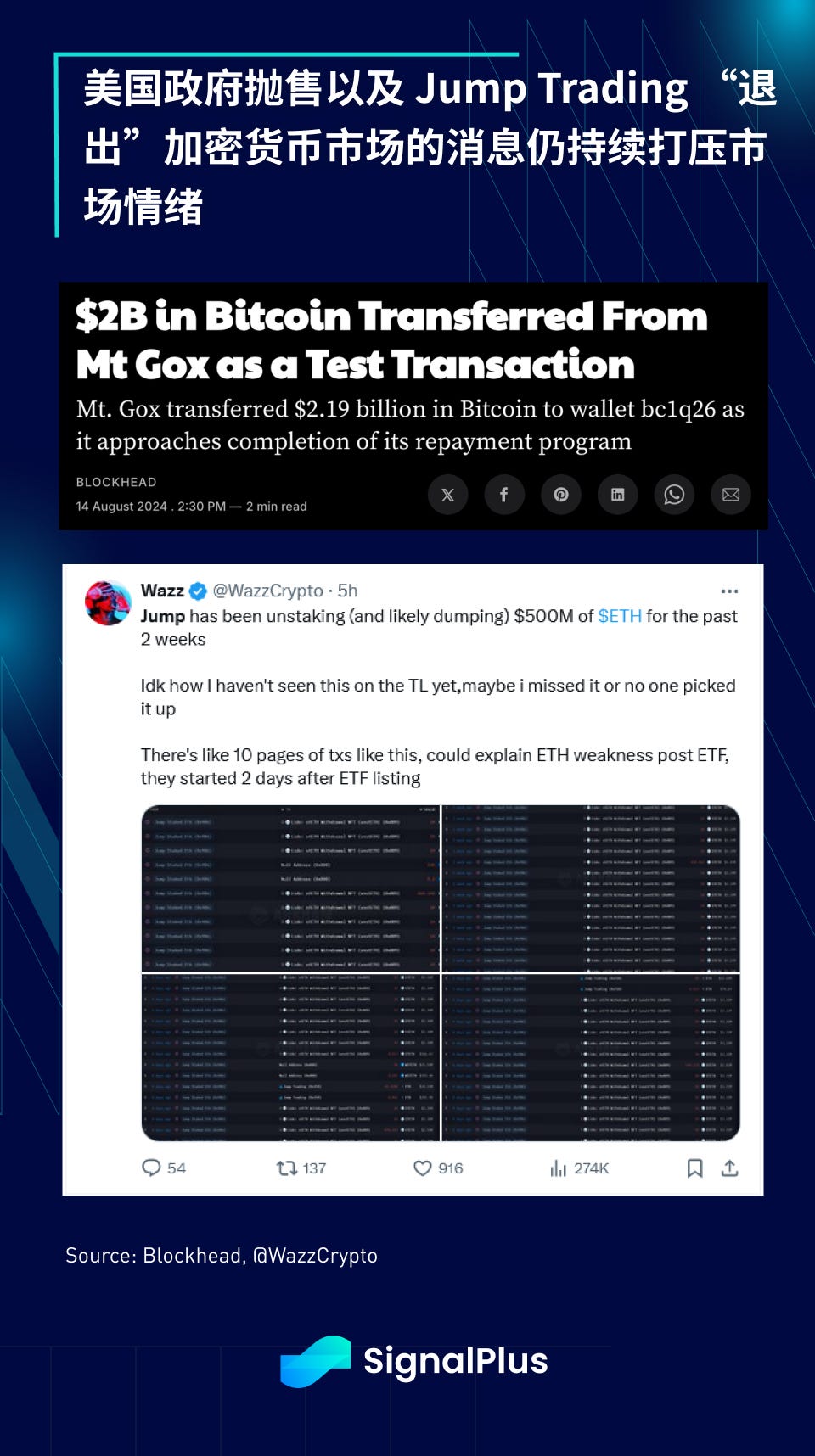

In the cryptocurrency space, due to market concerns over sell-off issues (Mt. Gox) and rumors of Jump Trading exiting the cryptocurrency market, the price performance of major cryptocurrencies continues to lag behind stocks and other risk assets. Reports indicate that Jump Trading has been continuously transferring assets to centralized exchanges, including retrieving 17,000 ETH from Lido, possibly in preparation for future liquidation and cashing out.

By the way, the conversation between Elon Musk and Trump did not discuss cryptocurrencies much, which may have disappointed some listeners who were hoping to hear more supportive (i.e., "pump") comments.

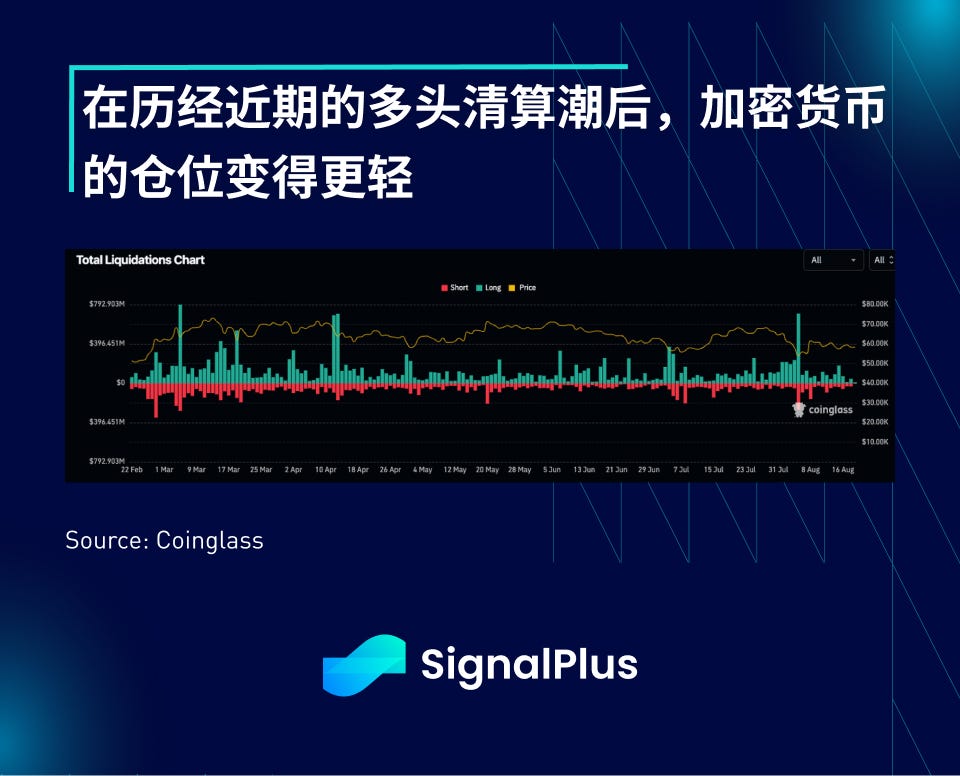

We expect cryptocurrency prices to face challenges until September, but after September, the continued improvement in macro sentiment could lift cryptocurrency prices, especially considering the recent light positioning in the market after the long liquidation and the Federal Reserve finally beginning to take easing measures.

Risk warning Risk warning

Risk warning Risk warning