The Federal Reserve opens a new chapter: Cryptocurrency officially included in Washington's agenda

The U.S. payment system is preparing to integrate the assets and infrastructure you are already trading.

The U.S. payment system is preparing to integrate the assets and infrastructure you are already trading.Article Author: Crypto Unfiltered

Article Compiled by: Block unicorn

Introduction

On October 21, the Federal Reserve held its first Payment Innovation Conference in Washington, D.C. The conference lasted a full day, bringing together central bank governors, large asset management firms, major banks, payment companies, and key crypto infrastructure teams. The agenda covered stablecoins, tokenized assets, DeFi, artificial intelligence in payments, and how to connect traditional ledgers to blockchains. The message conveyed at the venue was simple: crypto technology has now become part of the discussion in the payments sector.

Why This Time Is Different

For years, the U.S. attitude towards cryptocurrencies has sounded like "regulate first, then talk." This time, a Federal Reserve governor stated at the conference's opening that the goal is to embrace disruptive technologies in the payments space and learn from the experiences of DeFi and cryptocurrencies. This shift in tone is significant. It tells investors that the question has moved from whether this technology is applicable to how to integrate it safely into the core system.

The "Streamlined" Account Concept

The most concrete news is that the Federal Reserve is developing a payment account with limited access (commonly referred to as a "streamlined account"). It can be seen as a simplified version of a master account, allowing certain legally compliant non-bank institutions to access the Federal Reserve's payment services directly under strict regulation. This includes limits, no interest, no credit lines, and stringent reporting requirements. Currently, many stablecoin issuers and cryptocurrency companies rely on commercial banks for settlement and critical services. If a limited access Federal Reserve account becomes a reality, it could reduce single points of failure. This is not a free pass, nor will it happen overnight, but it is a clear direction of development.

Recommendations from the Crypto Industry to the Federal Reserve

To achieve true institutional scale, three challenges need to be addressed. First, make traditional systems compatible with blockchains for auditing and compliance checks. Second, standardize the proofs and metadata carried by transactions to meet the needs of regulators and counterparties. Third, create a "regulated DeFi" variant where smart contracts automatically enforce compliance, identity verification, and cross-chain control by default. None of these are mere fluff. All of these are precisely what large pools of capital need.

Why Stablecoins Are at the Core

Stablecoins have already become one of the largest practical uses of cryptocurrencies. Its biggest operational risk is the reliance on key channels from partner banks. Direct, limited access from the Federal Reserve will set higher thresholds for reserves, reporting, and settlement, reducing the likelihood of disruptions or de-banking events. This does not eliminate risk, but it does transform the system into a standardized, regulated system that institutions can understand.

Tokenized Assets Entering the Agenda

When the world's largest asset management firms, multinational banks, and crypto data providers gather with the Federal Reserve to discuss tokenized funds, tokenized cash, and on-chain settlement, what you see is a roadmap. Tokenization is not a gimmick. It is a way to accelerate the circulation of traditional assets, featuring instant settlement, 24-hour markets, and programmatic compliance. The longstanding obstacles have been standards, identity verification, and secure access to payment systems. All three are of utmost importance.

Market Impact

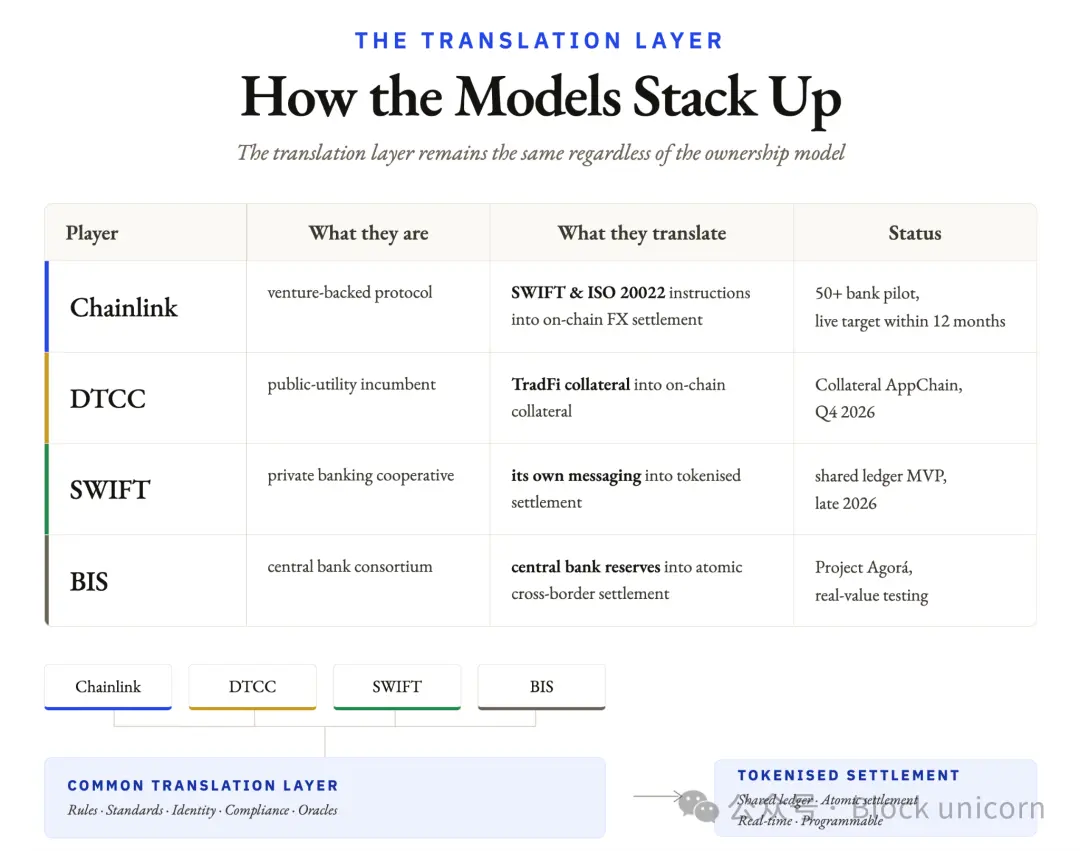

Price volatility around such events is significant. Bitcoin may drop several percentage points in a day, while Ethereum and Solana may also see sharp declines or spikes due to headlines, only to reverse. Structural signals are stronger. The U.S. central bank is currently openly discussing how to connect cryptocurrency channels with the core of payments. When policy clarity improves, capital flows often first concentrate on assets most suitable for institutional investors. Bitcoin remains the entry point for macroeconomics. Ethereum is at the core of stablecoins and tokenization. Solana continues to excel in speed and consumer applications. Chainlink positions itself as the data and compliance bridge connecting blockchains and institutions.

None of these guarantee a straight rise in prices. But they do determine where new allocations can be directed when legal and operational mechanisms shift. This often means first Bitcoin, then Ethereum, followed by a basket of large-cap assets with clear use cases. After that, if liquidity is strong and risk appetite rebounds, small-cap assets will begin to rise. The same cyclical rhythm, different driving factors.

Recent Catalysts

Stablecoin rulebook, standardizing reserves and real-time reporting.

More tokenized cash products, government bonds, with built-in on-chain identity.

DeFi versions hard-code counterparty checks, asset eligibility, and restrictions, allowing institutions to participate without changing their authorizations.

Stories at the intersection of artificial intelligence and cryptocurrency have real economic designs, not just branding, especially in the context of tightening emissions.

How to Position

Keep your plan simple and aligned with your investment horizon. If investing, focus on assets that institutions can actually purchase. For most, the core is Bitcoin and Ethereum, with a moderate allocation to Solana, and a small amount reserved for cross-chain bridging data and compliance infrastructure. If trading, assume volatility based on market dynamics, use isolation risk strategies, and set your stop-loss points in advance.

Final Conclusion

The Federal Reserve has convened crypto companies, banks, asset management firms, and large tech companies to collaboratively plan a shared payment system and proposed a concrete path for direct, limited access to the Federal Reserve's payment system. Prices will fluctuate. This indicates that the U.S. payment system is preparing to integrate the assets and infrastructure you are already trading. Stay patient, assess risks, and focus on those assets that institutions can genuinely hold when the payment gates open wider.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles