The starting gun for SpaceX's IPO hasn't fired yet, but the smart money in the "space sector" has already started to rush ahead?

The "Five Little Dragons," which have generally recorded double-digit increases, may be an important angle to understand this round of commercial space revaluation.

The "Five Little Dragons," which have generally recorded double-digit increases, may be an important angle to understand this round of commercial space revaluation.Written by: Frank, MSX

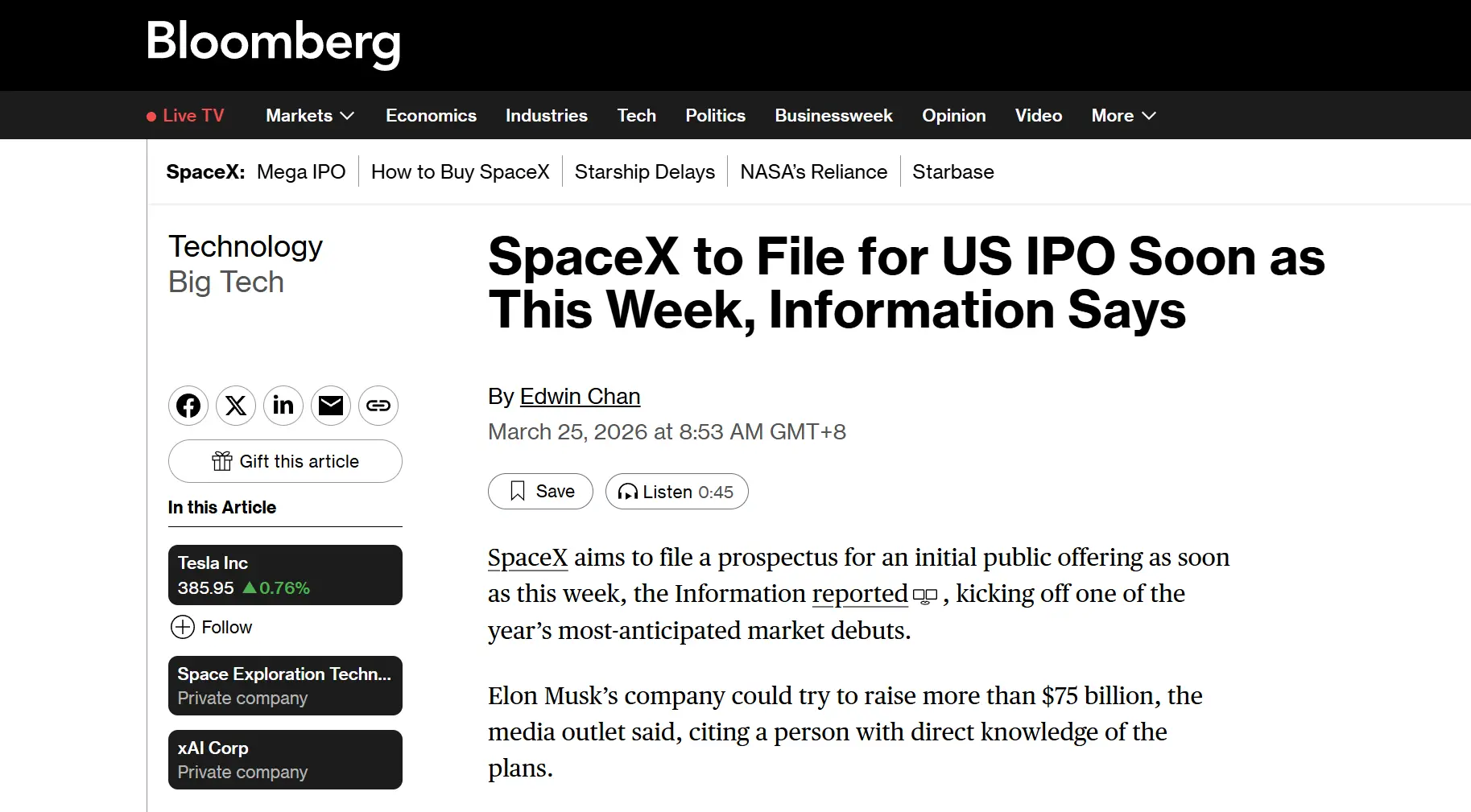

The most anticipated unicorn IPO in the US stock market this year seems to be just a step away.

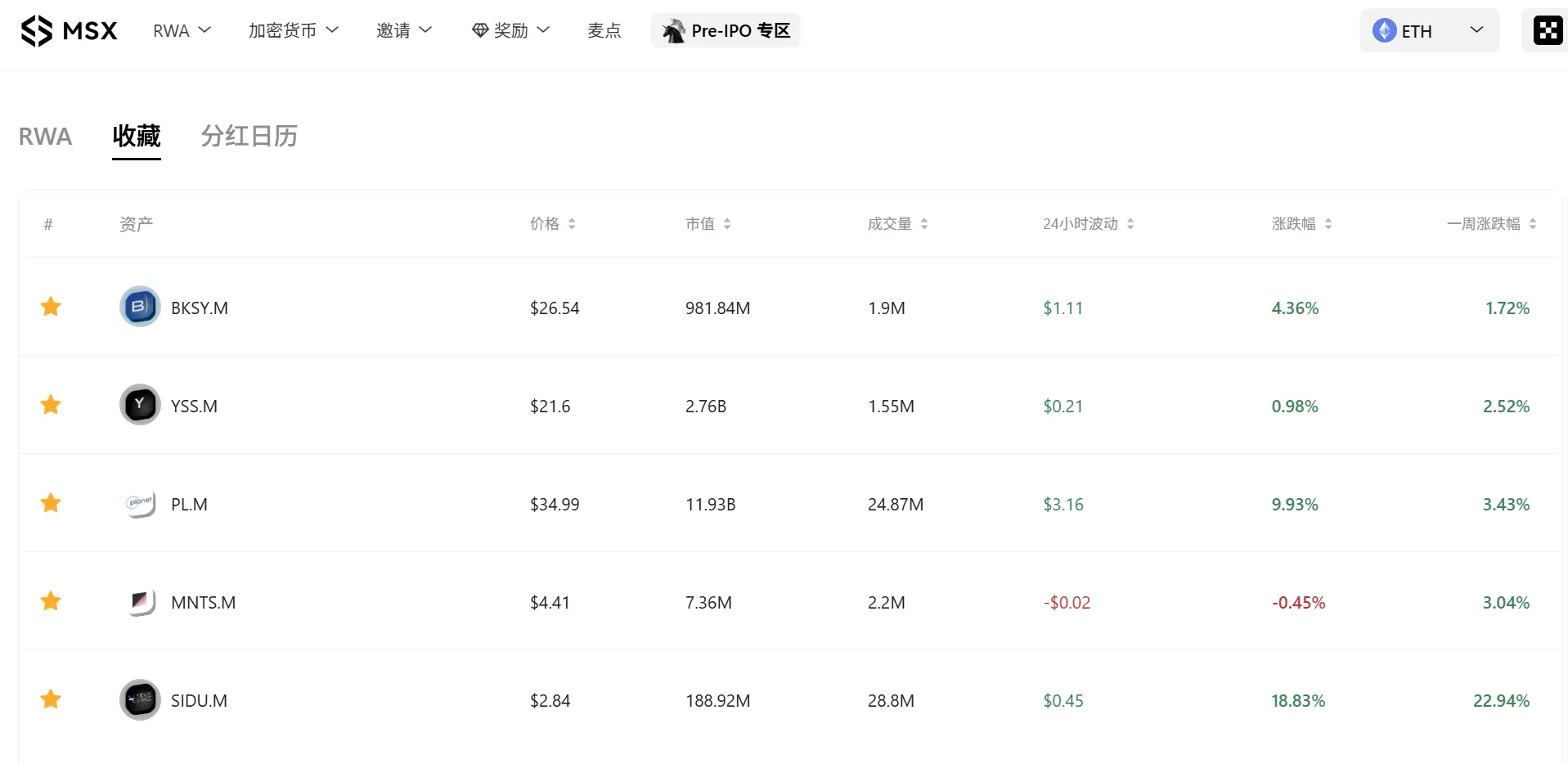

Insiders reveal that SpaceX plans to secretly submit its IPO prospectus as early as this week or next week, aiming to go public in June. The commercial aerospace and space concept sectors have responded accordingly. Just before this wave of market activity began, MSX screened and added 5 commercial aerospace US stock tokens: MNTS.M, SIDU.M, PL.M, BKSY.M, YSS.M on March 23, all of which recorded double-digit gains, with some stocks rising nearly 30% during intraday trading, providing investors with a relatively ample entry window.

It is worth noting that SpaceX's financing scale may exceed $75 billion. If this comes to fruition, it will not only significantly surpass the previously circulated market target of about $50 billion but will also far exceed Saudi Aramco's $29.4 billion fundraising record in 2019, making it the largest IPO in history, bar none.

This leads us to the real question this article aims to discuss: Beyond the emotional catalyst of the SpaceX IPO rumors, what deeper logic is at play behind this round of increases in the commercial aerospace sector? And does this wave of revaluation have a foundation for further diffusion?

1. SpaceX IPO: The Starting Gun for the Commercial Aerospace Sector?

Although SpaceX has not gone public, its influence on the secondary market has never been absent.

To understand this, one must first grasp SpaceX's position within the entire commercial aerospace ecosystem. It is no longer just a rocket company; it is an infrastructure provider that supports the operation of the entire commercial aerospace industry chain, serving as the strongest "valuation anchor" in global commercial aerospace—from launch capacity to Starlink communication, from orbital transport to manned flight, every technological breakthrough by SpaceX reduces costs and increases efficiency for a number of downstream small and medium-sized aerospace companies.

For this reason, the recent strength in space stocks is naturally tied to the catalyst of SpaceX potentially initiating its IPO, with a financing target of $75 billion and a potential valuation of $1.75 trillion. These two figures serve as a strong stimulus for the entire commercial aerospace sector.

Thus, we see that it is not just a single company that is strengthening, but the entire space concept is beginning to heat up simultaneously, forming a noticeable sector resonance.

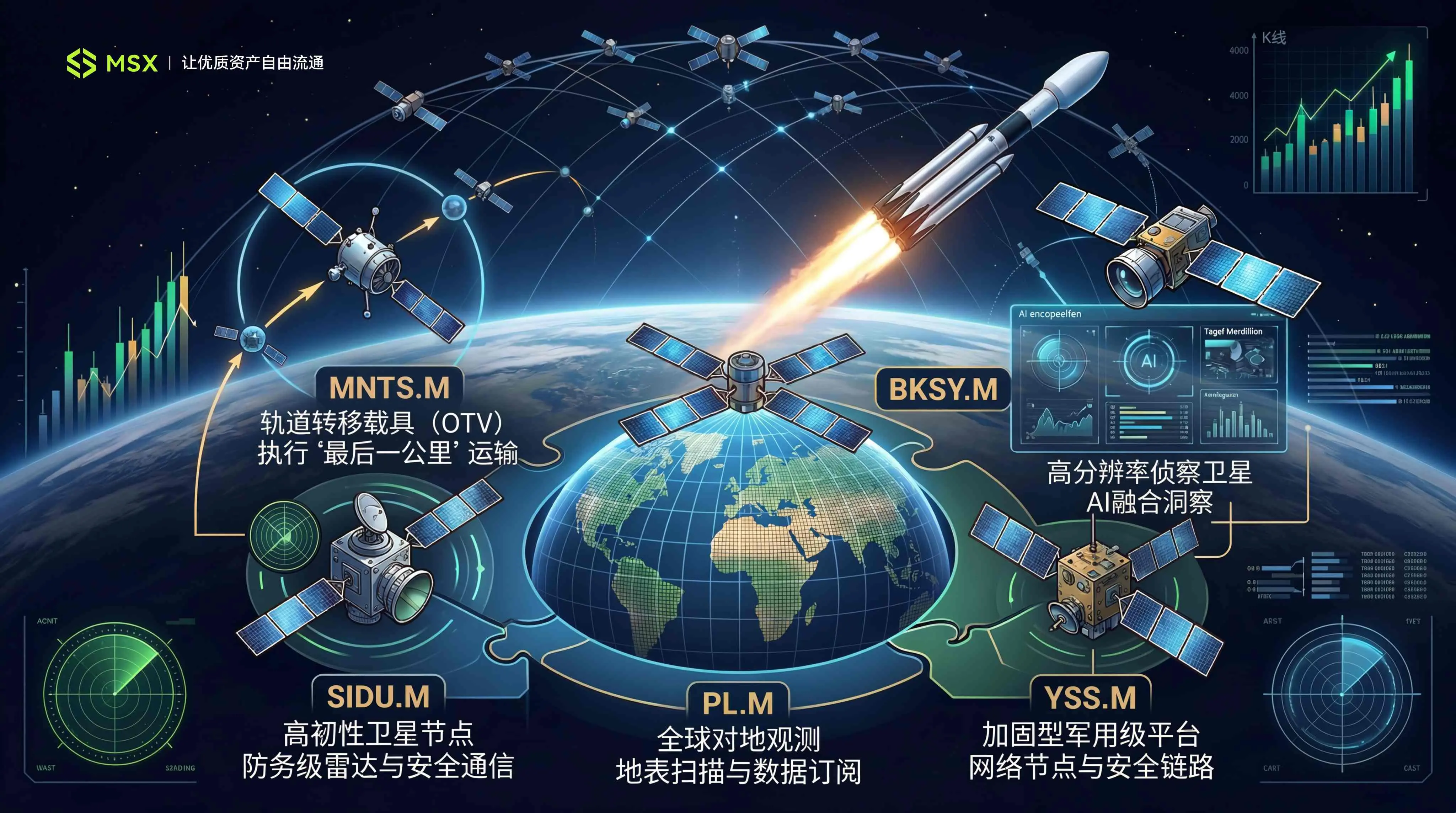

The most obvious manifestation is that the newly added commercial aerospace "Five Little Dragons" MNTS.M, SIDU.M, PL.M, BKSY.M, YSS.M all have solid fundamental support, representing a concentrated coverage of several core directions in the commercial aerospace industry chain:

MNTS.M** (Momentus) focuses on "last mile" orbital transfer services in low Earth orbit**, with its Vigoride spacecraft scheduled to ride SpaceX's Falcon 9 for its next mission. Therefore, this is not just a simple launch; it is more like a commercial validation, indicating that as global satellite networking accelerates, the demand for orbital transfer is shifting from "optional" to "essential."

SIDU.M** (Sidus Space) serves as a "stepping stone" for the defense system and has qualified for multiple project office contracts with the U.S. Missile Defense Agency (MDA)**, providing it with a ticket to continuously bid within the defense procurement system. For early-stage aerospace companies, government contract qualifications are the most direct trigger for valuation reconstruction and the most stable revenue anchor outside of commercial orders.

PL.M** (Planet Labs) is the most fundamentally solid leader in remote sensing in this round of market activity**, and it is also the stock with the highest market capitalization among the 5 US stock tokens newly screened by MSX. It has a global satellite constellation, daily revisit capabilities, and a real-world commercial data subscription model.

This also makes it one of the few space companies that can be discussed in terms of ARR and gross margin, with backlogged orders growing 79% year-on-year, nearing $900 million, and achieving profitability for the first time—this turning point's significance goes far beyond just a quarterly report number.

BKSY.M** (BlackSky) is transforming itself from a "satellite company" to an "intelligence service provider"**, with its core competitiveness stemming from high-frequency revisits and AI analysis capabilities. For example, its third-generation (Gen-3) satellite constellation can provide commercial high-resolution images with a clarity of 35 centimeters (0.35 meters), combined with intelligence needs driven by geopolitical situations. This positioning's premium space is undoubtedly much higher than that of a simple remote sensing data provider.

YSS.M** (York Space Systems) is a core supplier for the U.S. Army's proliferated battlefield space awareness (PWSA) project, backed by the military**, providing predictable cash flow. As a recently newly listed IPO target, the institutional accumulation period has not yet ended, and the share structure is relatively clean, offering high upward elasticity.

Ultimately, the five stocks that MSX has added ahead of time are meant to cover the core directions in the commercial aerospace industry chain: some focus on orbital transport and mission execution, some on satellites and defense orders, some on Earth observation and remote sensing data, and some on newly listed, high-elasticity satellite platform companies.

The significance of this group of stocks is not merely betting on a single event but attempting to pre-position around the main theme of "commercial aerospace revaluation," which is also the core factor behind MSX's early bet on the broad market rally.

2. Revaluation from "Science Fiction" to "Hard Currency"

Of course, if we simply understand this wave of increases as "news-driven," we would underestimate its historical context.

Reviewing the logic behind the stock selection that hit the mark before this surge, MSX did not blindly gamble on sentiment but captured two core signals:

- On one hand, at the recently concluded NVIDIA GTC conference, Jensen Huang announced strategic layouts in the space industry, from dedicated space-grade computing chips to cosmic digital twins for orbital environments, indicating that AI is no longer just a productivity tool on the ground; it is becoming the underlying architecture for satellite autonomous navigation and real-time processing of low Earth orbit data.

- On the other hand, on March 23, SpaceX, Tesla, and xAI jointly announced the launch of the "TERAFAB" project, aiming to leverage AI and highly automated manufacturing capabilities to produce one terawatt of AI computing chips annually, primarily for space deployment. This essentially sketches a massive scalable vision for the secondary market.

Based on a deep analysis of these two signals, the MSX research team decisively completed the coverage of the commercial aerospace "Five Little Dragons" on the 23rd.

As is well known, for a long time, the commercial aerospace sector has been viewed as "chicken ribs" in the secondary market, primarily because it is a "money-burning" game: rockets, satellites, moon landings, deep space, Starlink—each term is enticing, but in the capital market, many companies face high R&D investments, long project cycles, slow profit realization, and significant cash flow pressures.

But this time, something is beginning to change.

Starting in 2025, commercial aerospace will no longer be as simple as "launching rockets," but will gradually be broken down into a clearer and more easily understood real industrial chain by the capital market. Especially beyond rocket launches, more and more genuinely viable and sustainable business opportunities are beginning to surface:

Satellite manufacturing, in-orbit services, Earth observation, defense remote sensing, low Earth orbit communication networks, AI-enabled image analysis and intelligence distribution—all of this means that the value of commercial aerospace no longer solely comes from some distant future vision, but increasingly from verifiable orders, service capabilities, and customer demands.

Looking further, there are actually three deeper logics occurring simultaneously behind this round of revaluation.

First, the significant decrease in launch costs is changing the economic foundation of the entire industry. The maturity of reusable rocket technology is continuously lowering the unit cost of entering orbit; and the decrease in launch costs, in turn, lowers the barriers for satellite networking, in-orbit services, and data commercialization.

For many small and medium-sized commercial aerospace companies, this means that businesses that could only remain in the experimental validation stage in the past are beginning to have the potential to move towards scaled deployment and breakeven. SpaceX itself is the biggest driver of this cost curve, which is why its IPO expectations have such a strong spillover effect on the entire sector.

Second, commercial aerospace is beginning to converge with larger thematic trends of the era. The strongest market themes today are AI, defense, communication, and new energy, and space infrastructure happens to intersect with these themes. AI requires a continuous stream of high-quality data and stronger edge perception capabilities, the defense system increasingly relies on real-time reconnaissance, space communication, and distributed satellite networks, and global geopolitical competition further elevates the strategic value of aerospace capabilities.

When a sector begins to embed multiple mainstream narratives simultaneously, it is no longer an isolated niche concept but is more likely to become a thematic hub for repeated capital allocation.

Finally, the market is beginning to accept differentiated pricing within the commercial aerospace sector. In the past, whenever space stocks were mentioned, the market defaulted to viewing them as emotional thematic assets that rose and fell together. Now, as the industry gradually matures, investors are beginning to realize that the values of different companies do not exist on the same level. For example, some sell satellite platforms, some sell image data, some sell defense contract qualifications, some sell in-orbit service capabilities, and some sell the elasticity of shares in the new stock phase.

This represents a transition in the commercial aerospace sector from thematic linkage to "layered pricing of the industry chain," and once a sector enters this stage, it often means that it is no longer just a short-term concept but has begun to possess the foundation for long-term research and continuous trading.

3. What This Wave of Space Stock Increases Means for Investors

So, on the surface, this wave of increases is indeed ignited by the rising expectations for SpaceX, but looking deeper, what truly drives the market to re-bet is that commercial aerospace is transitioning from a long-term narrative sector to a "priceable sector" with industry layering.

This also reflects a fundamental shift in the underlying logic that the capital market is willing to start pricing seriously.

However, after the heat, how far the market can go ultimately depends on the verification of fundamentals. The MSX research institute believes that after the short-term emotional catalyst, the true depth and sustainability of this market rally will depend on the following key variables:

- Substantial progress in the SpaceX IPO process: The secret submission of the prospectus is just the first step; each node of roadshows, pricing, and listing will continue to provide topic heat and capital siphoning effects for the sector.

- The rhythm of the U.S. defense and aerospace budget implementation: The incremental project budget for the new fiscal year has been confirmed, but which companies the contracts will flow to will gradually be revealed over the next two quarters. This is the main source of stock differentiation, as companies with contract support will have increasingly different trajectories from those purely driven by sentiment.

- The cash reserves and financing capabilities of each company: Most early-stage aerospace companies are still in a loss-making phase, and the rising market period is often a window for financing. A particularly noteworthy signal is whether management chooses to replenish ammunition at high levels rather than cashing out—this is the most direct and hardest to disguise indicator of insider confidence.

Of course, regardless of how the short term unfolds, one thing is becoming increasingly clear: SpaceX's IPO will not be the endpoint of this industry story; rather, it is more likely to be the starting point for the entire commercial aerospace industry chain to truly enter the mainstream capital vision.

Over the past decade, the story of this sector has mostly remained at the level of PPTs and concepts, with capital often pricing for "imagination"; in the coming years, the market will increasingly measure the value of these companies with real revenues, landed contracts, and verifiable profit nodes.

This presents both opportunities and demands for investors.

The window of sector resonance is rare, but those that can truly transcend cycles will always be just a few.

Risk warning

Risk warning

Popular articles