Stablecoins and Latin American Remittances: The Misunderstood $174 Billion Market

In the Latin American remittance market, the real protagonists have never been the young people speculating on cryptocurrencies, but rather the 50-year-old workers who send money to their mothers every month. They don't care about blockchain; they only care about whether the money has arrived.

In the Latin American remittance market, the real protagonists have never been the young people speculating on cryptocurrencies, but rather the 50-year-old workers who send money to their mothers every month. They don't care about blockchain; they only care about whether the money has arrived.Author: Claudia

Compiled by: Jiahua, ChainCatcher

Recently, every fintech company's business plan includes the same page: "Latin America is the next big opportunity. Stablecoins are the killer app for cross-border payments."

But if you ask them how large their actual remittance channels are; ask them what percentage of users want dollars instead of their local currency; ask them why Mexico's digitalization rate is 25%, while Colombia's exceeds 50%. Most of the time, you will get silence.

I spent six months working with our local teams in Brazil, Mexico, Argentina, Colombia, and Peru, conducting field research. Talking to users, mapping competitors, analyzing internal peer-to-peer, card, and payment data, and stress-testing every assumption in public reports.

Here are our real findings. As a frontline builder, it took me six months to write this article, and I hope it helps you gain a comprehensive understanding of what is happening there. You will find that most fintech companies have misread this market, and at the end of the article, I also outline the potential of this market, hoping it will be helpful to you.

Mexico Peaks, Central America Booms

By 2025, the total remittances flowing to Latin America are expected to reach a historic high of approximately $174 billion, up from $161 billion in 2024. This accounts for about 2.5% of the region's GDP.

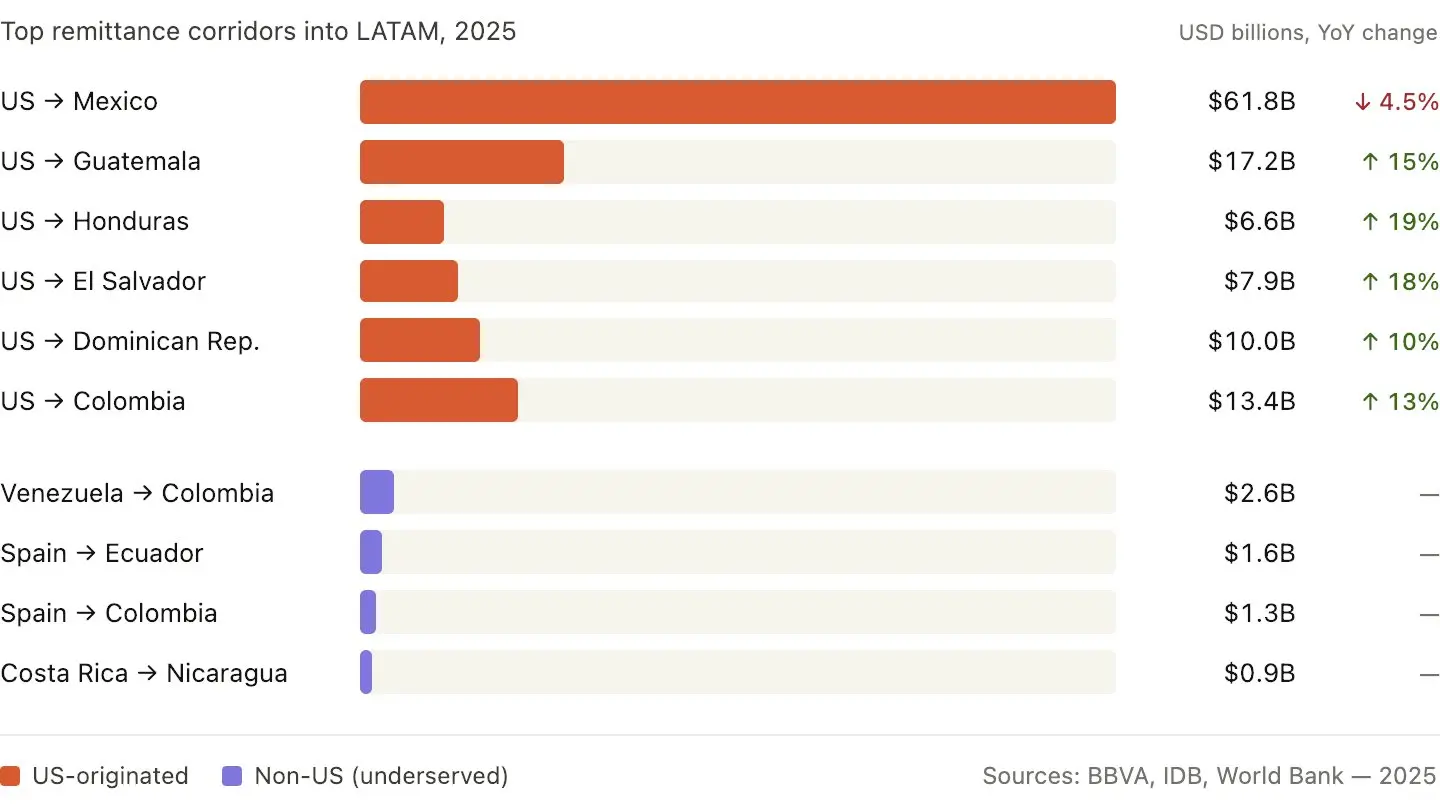

For the first time in 11 years, Mexico has seen a decline of 4.5%, down to $61.8 billion. Meanwhile, Central America is experiencing a boom: Guatemala: +15% Honduras: +19% El Salvador: +18% Colombia: +13% Dominican Republic: +10%

For the first time in 11 years, Mexico has seen a decline of 4.5%, down to $61.8 billion. Meanwhile, Central America is experiencing a boom: Guatemala: +15% Honduras: +19% El Salvador: +18% Colombia: +13% Dominican Republic: +10%

This is not a random fluctuation. It is a structural shift driven by U.S. immigration policy. Immigrants from Central America are sending more money home, faster and in larger amounts, to avoid the risk of deportation.

Mexico has a more mature and well-documented immigrant population and has not shown the same panic-driven remittance behavior. The "hot" remittance channels that appear now are not the target channels optimized by most fintech companies.

The complete data breakdown is as follows: Mexico: approximately $61.8 billion (down 4.5%) Central America: approximately $55 billion (up 20%+) South America: approximately $36 billion (up 11%) Caribbean: approximately $21 billion (up 9%)

An interesting data point: by 2027, the volume of cross-border payment transactions (trade + B2C + remittances) is expected to exceed $300 billion.

A structural fact that is hardly discussed is that in Latin America, the ratio of inflows to outflows is as high as 16 to 1. Inflows are $174 billion, while outflows are about $10 billion. The top five channels all originate from the U.S.:

U.S. → Mexico

U.S. → Guatemala

U.S. → Dominican Republic

U.S. → El Salvador

U.S. → Honduras

Everyone is competing for these markets. The untapped areas are non-U.S. remittance channels:

Venezuela → Colombia → Spain → Ecuador / Colombia / Dominican Republic → Argentina → Bolivia / Spain → Costa Rica → Nicaragua

These channels are relatively small in scale, but there are almost no remittance operators (MTOs) holding U.S. licenses providing services, and they are hardly touched by crypto payment networks.

If you want to find a defensive channel in 2026, this is where to pay attention. Especially as the U.S. 1% remittance tax (passed in the summer of 2025, affecting about half of remitters) begins to push transaction volumes toward digital and non-U.S. channels.

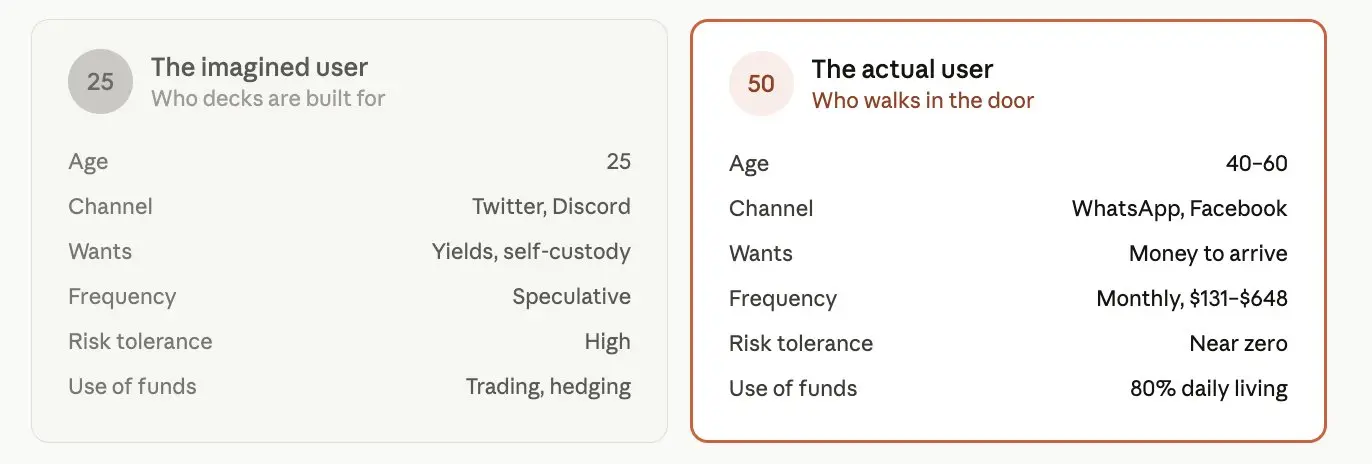

Target Users Are Not Crypto Traders

Most fintech companies are building products for 25-year-old cryptocurrency traders. This is the wrong target customer.

Based on our field research, the real profile of remittance users in Latin America is as follows:

Age: 40 to 60 years old. Sending money home every month.

Amount: $131 to $648 per month, accounting for 6% to 23% of their income.

Recipients: More than half send money to their mothers. One-third send to fathers.

Use of funds: 80% for daily living expenses, including food, housing, and transportation. Followed by medical expenses. Then education and savings.

This is lifesaving money for families. What does this mean for products?

Risk tolerance is almost zero. Trust is more important than functionality. A simple process is essential. Deposit → Confirm → Send, that’s enough.

Spanish and Portuguese are uncompromising hard requirements, not "nice-to-haves." WhatsApp and mobile-first always outperform web-based solutions.

If your product makes a 50-year-old factory worker in New Jersey think for more than 30 seconds before sending $300 to his mother in Honduras, you’ve already lost.

The crypto industry has spent five years optimizing for the wrong user group. Retail remittance customers in Latin America do not want to "self-custody." They just want to know their money has arrived safely.

In Latin America, Stablecoins Are the Product Itself

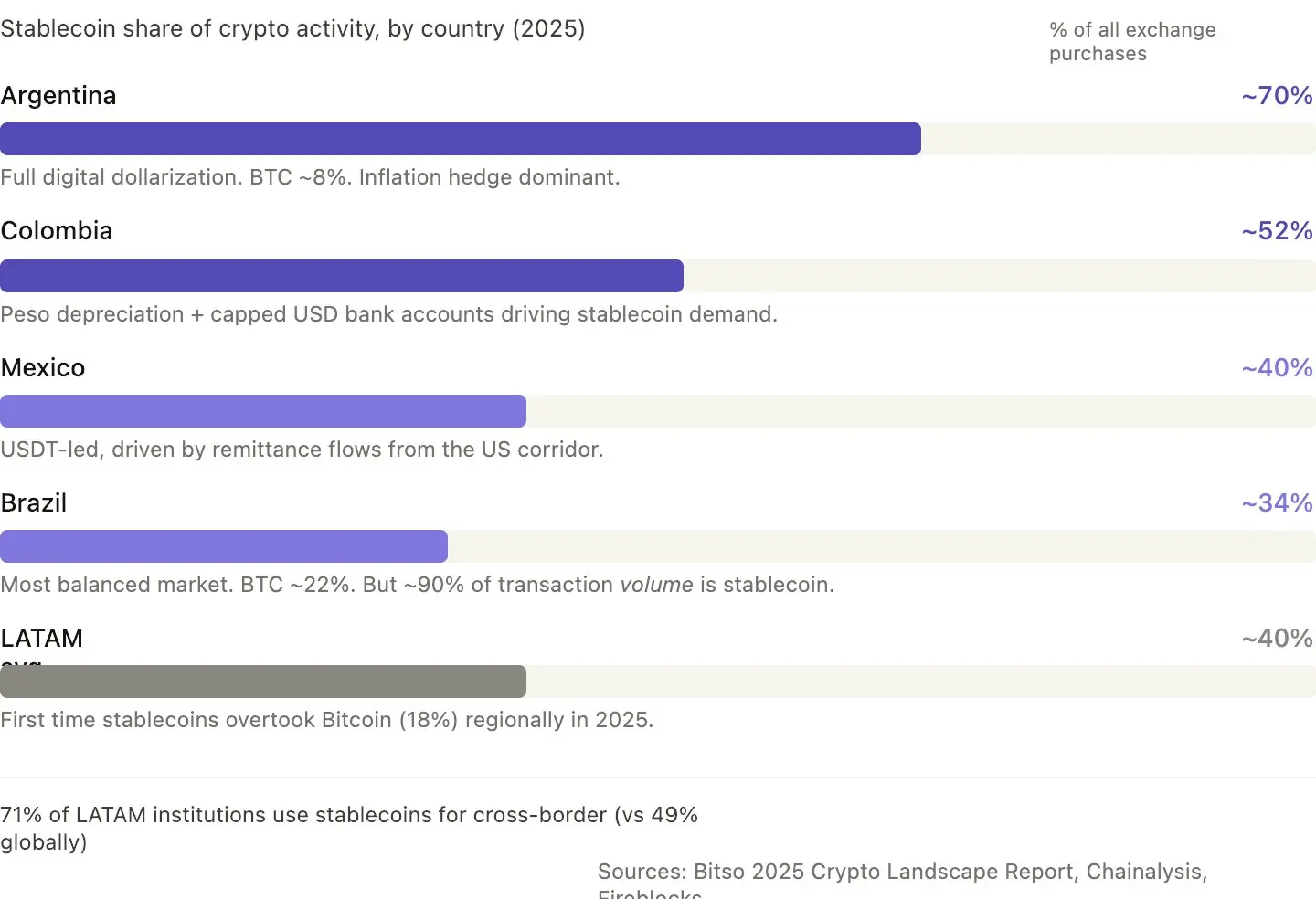

The following data should reshape every fintech company's strategy. Unless otherwise noted, all data comes from Bitso's 2025 Cryptocurrency Landscape Report (over 10 million retail users) and Chainalysis' 2025 Cryptocurrency Geography Report:

Argentina: USDC and USDT account for over 70% of all cryptocurrency purchases. Complete digital dollarization. Bitcoin's impact is minimal, accounting for about 8%. (Bitso 2025)

Colombia: Stablecoins account for about 52% of cryptocurrency purchases, up 2 percentage points year-on-year. Driven by the depreciation of the peso and the $5,000 minimum deposit limit for Colombian dollar bank accounts, stablecoins have become the only accessible dollars. (Bitso 2025)

Mexico: Stablecoins account for about 40% of cryptocurrency purchases, up from last year. Primarily USDT, mainly driven by the flow of funds from U.S. remittance channels. (Bitso 2025)

Brazil: Two numbers tell different stories. Stablecoins account for about 34% of purchases (Bitcoin accounts for about 22%), making it the most balanced retail market in Latin America.

But at the system level, central bank reports indicate that about 90% of cryptocurrency trading volume is linked to stablecoins. The assets purchased by users are mixed, but the flow of funds is denominated in dollars. (Bitso 2025; Chainalysis 2025 citing central bank data)

Across Latin America: By 2025, stablecoins will account for 40% of all cryptocurrency purchases, surpassing Bitcoin (18%) in the region for the first time. Cumulative cryptocurrency trading volume over three years (from July 2022 to June 2025) is approximately $1.5 trillion. (Bitso, Chainalysis)

At the institutional level: A Fireblocks survey of institutions in Latin America found that 71% of institutions use stablecoins for cross-border payments, the highest proportion globally, while the global average is 49%. (Fireblocks 2025 Stablecoin Status Report)

There are two ways to interpret this data, both of which are true and worth distinguishing:

In Argentina, over 70% of the assets purchased on exchanges are stablecoins. This is a behavioral signal representing complete retail dollarization. People use USDC and USDT as savings accounts.

In Brazil, stablecoins account for about 90% of trading volume. This is a funding flow signal indicating that most of the funds flowing through Brazil's crypto payment network are denominated in dollars, even if users are using Bitcoin or local tokens in the front-end experience.

These tell different stories. Argentina represents users wanting dollars. Brazil represents a system operating in dollars. Both reach the same conclusion, but the implications for products are different.

Why is this happening? Not because Latin American users love cryptocurrencies. They are addressing three pain points that banks cannot solve: hedging against inflation (Argentina, Venezuela), capital controls (Argentina, Brazil), and cheap and fast cross-border asset transfers.

This is where most Western fintech companies overlook: in Latin America, stablecoin balances themselves are the killer application. Users do not want to "use" stablecoins for a transaction and then convert back to local currency.

They want to hold dollars. Transactions are just a byproduct.

This is fundamentally different from the products being built by Wise or Remitly. This is also why the next phase of fintech in Latin America will be won by those who control daily balances, not those who control transfers.

Who Will Win in the Next Decade?

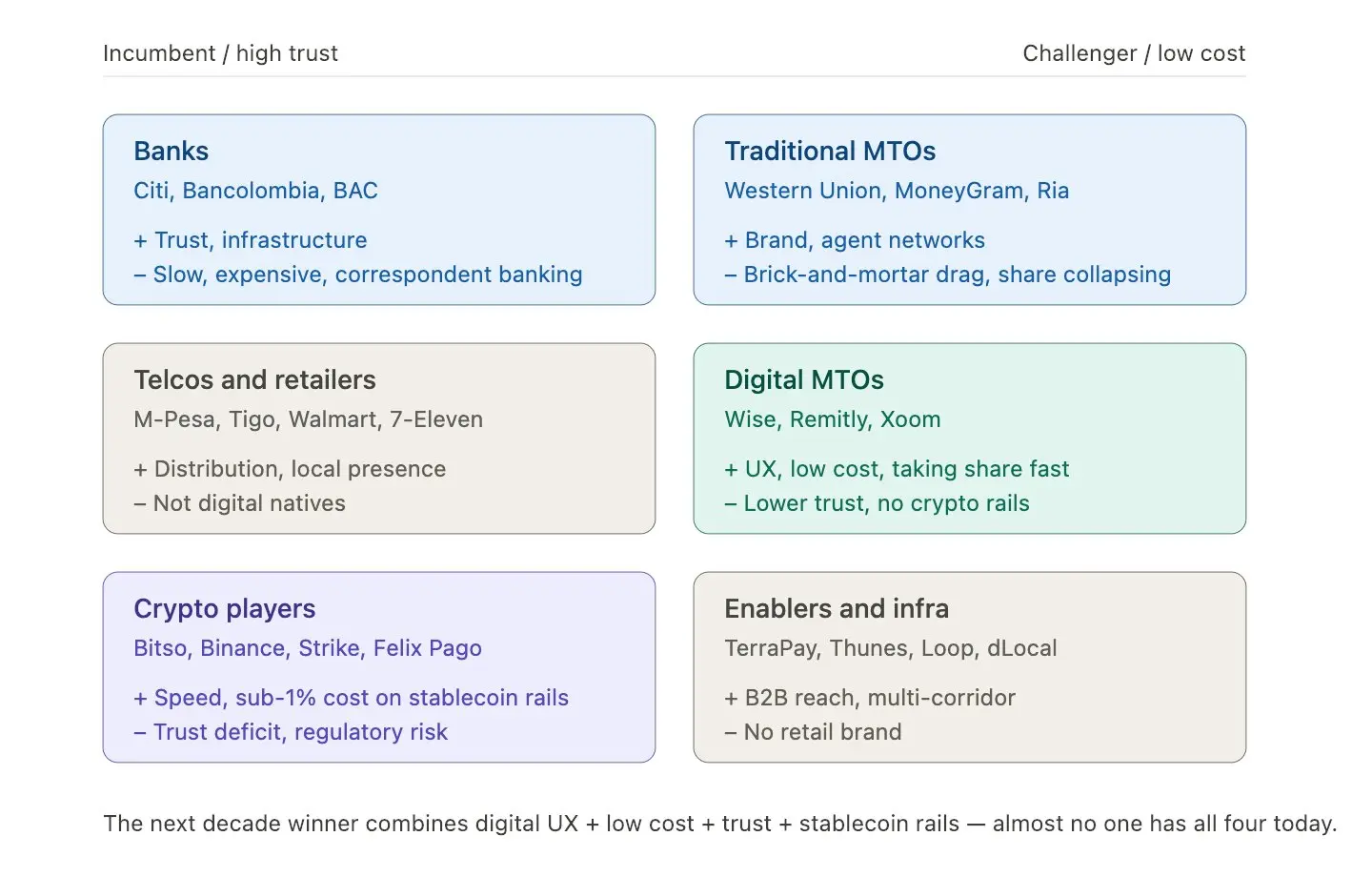

The Latin American remittance market currently has no absolute winner. This $161 billion market is divided among the following six types of players:

Banks (Citibank, Bancolombia, BAC): Have trust and infrastructure, but are slow and costly, relying on correspondent banking systems.

Traditional remittance operators (Western Union, MoneyGram, Ria): Have brand and agent networks, but high costs and are burdened by physical locations.

Telecom companies and retailers (M-Pesa, Tigo, Walmart, 7-11): Have distribution channels but are not native digital platforms.

Digital remittance operators (Wise, Remitly, Xoom): Good experience, low cost, but weaker trust and brand recognition.

Crypto players (Bitso, Strike, Felix Pago): Fast and nearly zero cost, but lack trust and face regulatory risks.

Infrastructure service providers (TerraPay, Thunes, Loop, dLocal): Have B2B coverage capabilities but lack retail-facing brands.

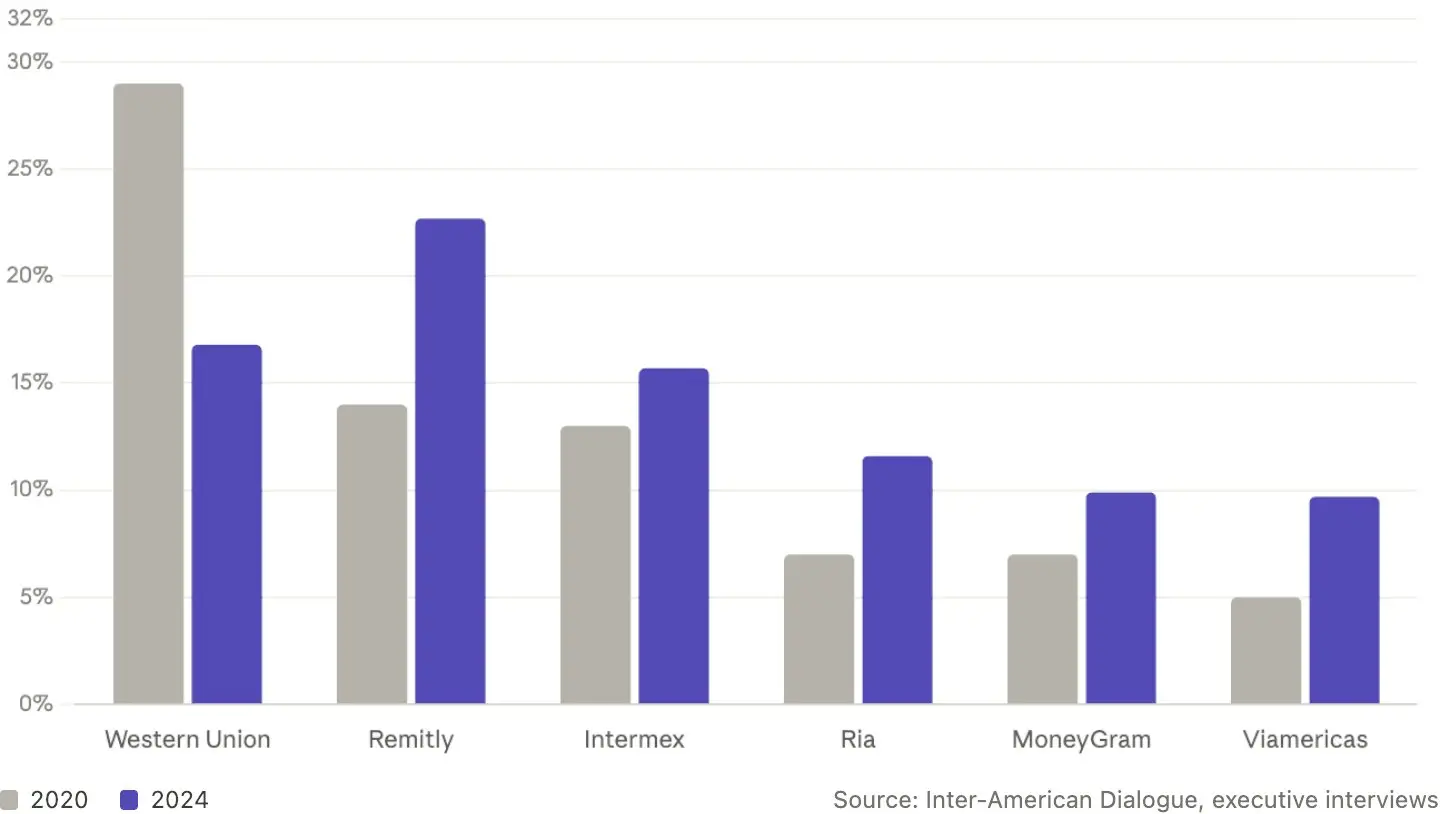

If you are unsure who is capturing the market, we can look at market share changes. In the U.S.-Latin America and Caribbean corridor (2020 → 2024):

Western Union: 29% → 16.8% (collapsing)

Remitly: 14% → 22.7% (pure digital platforms are winning)

MoneyGram: 7% → 9.9% (flat)

The trend is clear: traditional remittance operators like Western Union are losing this game, while digital-first platforms are rapidly capturing market share from traditional companies.

Bitso alone now handles about 10% of the U.S.-Mexico fund flow using stablecoin payment networks. Felix Pago has facilitated over $1 billion in USDC to SPEI transactions via WhatsApp.

The winners of the next decade will be a combination of these four: digital user experience, low cost, trust, and the underlying stablecoin payment network.

Banks Take 5%, Crypto Networks Only 2%

The average cost of sending remittances to Latin America: approximately 6.0% of the remittance amount. Most expensive: Paraguay, reaching 11.9% Cheapest: El Salvador, at 3.9% Cash transfers: average about 6.21% Digital transfers: average about 5.11%

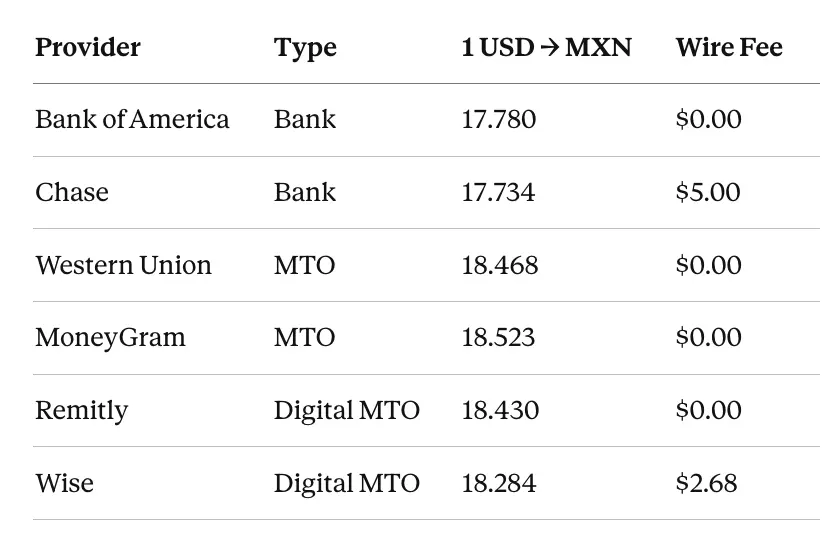

Let’s take a real snapshot of the situation from the U.S. to Mexico ($300, December 2025):

From the data, we can easily see: banks take about 3-5% profit from the exchange rate spread. Even if the fee shows as "0 dollars," banks will still extract profit from the exchange rate.

Crypto payment networks compress total costs to below 1-2%. For an immigrant sending $300 monthly, this means saving 5-8% per transaction directly sent back to their families. Accumulated over a year, this is equivalent to a month's worth of groceries.

This is the entry point. Moreover, in non-U.S. channels, this advantage is even more pronounced.

The Venezuela to Colombia corridor is the most popular intra-regional channel, estimated to reach $2.35 billion in 2021. Before accounting for the severely inflated exchange rates of traditional banks, the fees there can be as high as 1-3%.

The channels with the worst traditional cost structures are precisely where stablecoins are first disrupting. That’s why, years before any regulatory framework was introduced, Venezuela had already moved towards peer-to-peer stablecoin transactions.

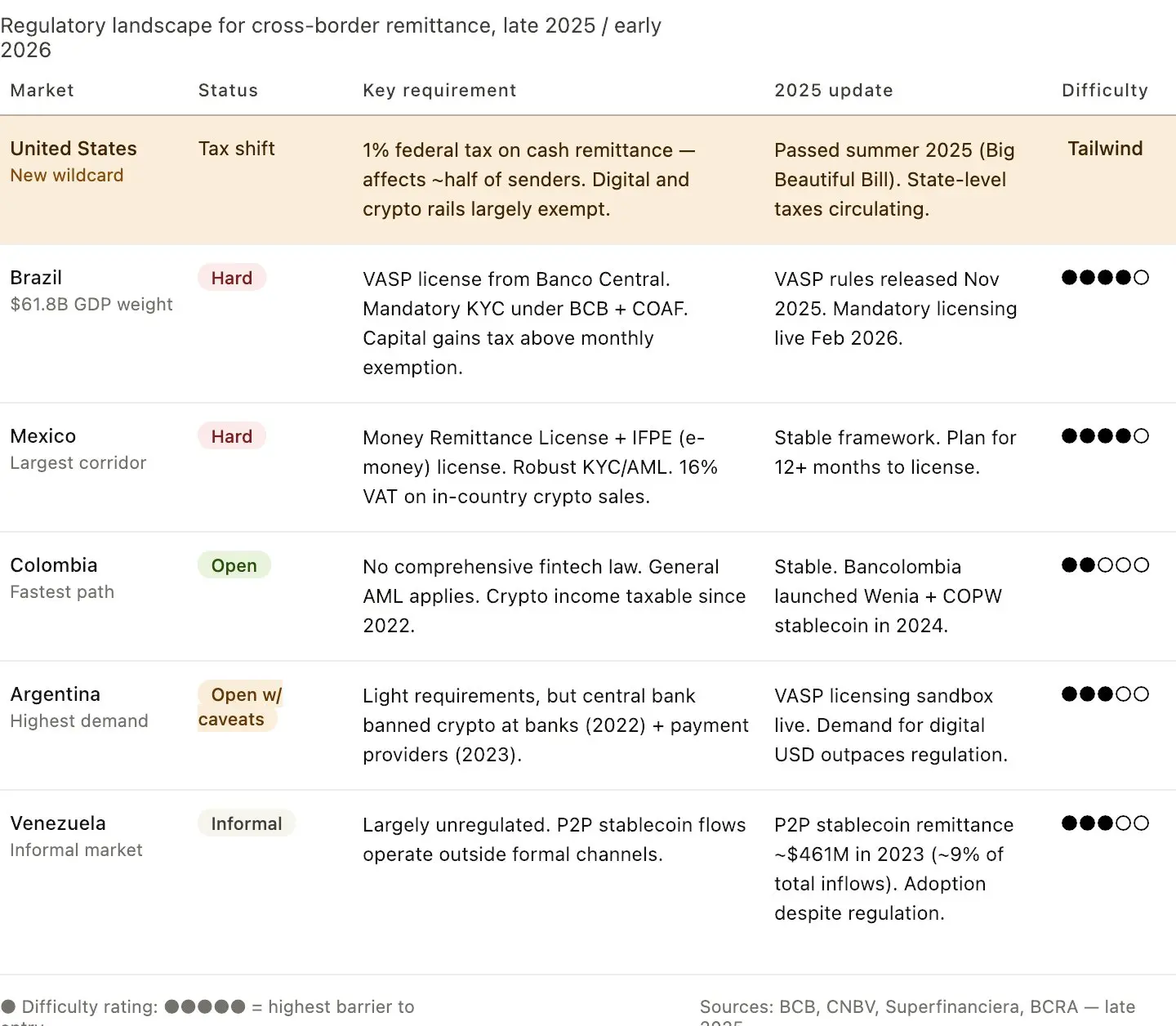

The Same Continent, Five Sets of Regulatory Rules

Most business plans for "Latin American expansion" treat the region as a single country. But it is not. The regulatory landscape is the biggest reason most fintech companies fail to expand here. Moreover, as of 2025, a new variable that most people have not accounted for has emerged.

The biggest change on this map is not in Latin America, but in the United States.

A 1% federal tax on cash remittances, part of the "Big Beautiful Bill," was passed in the summer of 2025, affecting about half of remitters. Digital and crypto payment network transfers are largely exempt.

This is the biggest regulatory boon for the stablecoin remittance industry granted by U.S. policy in a decade. Proposals for states to increase their own taxes are also circulating. The ongoing migration from cash to digital has just received a forced acceleration.

Once you see this map, a wise phased strategy for expansion in Latin America becomes evident:

First, Colombia and Argentina: faster paths, lighter regulatory intervention.

Simultaneously advancing in Brazil and Mexico, entering through licensed local partners: slower speed but defensive.

Entering Venezuela through peer-to-peer stablecoin networks: demand is already naturally occurring, go to where the demand is.

A common mistake in most expansion plans is starting with Brazil because "it is the largest." Brazil is the largest but also the most difficult. First, capture the easier markets to build practical experience in local payment networks, then enter Brazil with real licensed partners.

Do not underestimate the influence from the U.S. This 1% tax is the kind of policy change that quietly redraws the map.

Within 12 months, the proportion of remittances conducted through cash channels will plummet. By then, those who control digital and crypto payment networks will capture a brand new market that is vastly different from today.

What Does a Winning Tech Stack Look Like?

After six months of observation from various angles, here is the technology architecture that can win:

Local payment network integration: Pix (Brazil), SPEI (Mexico), PSE (Colombia), CVU/CBU (Argentina).

Scalable stablecoin liquidity: USDT and USDC, deep order books, minimal spreads, and fast conversion to local currencies (Brazilian Real/Mexican Peso/Argentine Peso/Colombian Peso). This is a basic threshold, not a moat.

Card layer: Because recipients usually want to spend these dollars, not just receive them. Adding a card on top of stablecoin balances can turn remittance products into everyday financial products.

This is the direction of Visa and Bridge's stablecoin card layout, Nubank integrating USDC, and a wave of regional card and fintech collaborations.Value-added/yield layer: For the portion of remittances held rather than spent by recipients. Offering a 4-6% yield on USDC outperforms all local savings accounts in the region. This is a part that almost no one can integrate well.

Trust and a minimalist experience: One-time KYC verification, using local languages, and an interface that a 55-year-old can easily use. The product that wins in the end is not the one with the most features, but the simplest one.

So we can see the closed loop here: Deposit → Remittance → Recipient holds USDC or exchanges it for local currency through local payment networks → Spend via card or earn balance yield.

This is something banks cannot do (they do not have stablecoin payment networks). Traditional remittance operators cannot do it (they do not have wallet/card technology stacks). Pure crypto exchanges cannot do it (they do not have local payment integration). And pure digital banks cannot do it (they do not have cross-border crypto liquidity).

Companies preparing to seize this opportunity are coming from all directions and converging in the middle. Whoever first pieces together the complete architecture will win the daily balance.

Trust is Ten Times More Important Than Technology

First, stop treating Latin America as a single market. Brazil, Mexico, Argentina, Colombia, each country requires different licenses, different payment networks, different stablecoins, and different marketing strategies.

The companies that win here operate technology stacks tailored to specific countries, not regionally. Treating "Latin American expansion" as a single project on the roadmap signals that this team has not done their homework.

Second, the adoption of stablecoins has already happened. The debate about "whether users will hold digital dollars" is over; they are already holding them in large amounts, regardless of whether your product exists.

The remaining question is where they put their balances: exchanges, wallets, digital banks, or accounts linked to cards. Products that can capture daily balances will win users. Everything else is just a fleeting transaction.

Third, the bottleneck is trust, not technology. The key to unlocking crypto payment networks in retail remittances is a brand that even the recipient's mother trusts.

This is a marketing issue, not an engineering issue. Most fintech companies in this space are over-engineered and under-marketed. Local faces, local languages, and local community partnerships will always outperform better technology.

In fact, Latin America is not "the next big opportunity." It is currently the largest opportunity in the stablecoin-driven cross-border payment space, having quietly developed for two years while everyone has been focused on the U.S.

The fintech companies that will win the next decade in this region will be those that combine local payment networks, stablecoin liquidity, trust, and a closed-loop economy (remittance → holding → spending → earning).

Most teams pitching Latin American businesses I have seen possess only one or two of these elements. Very few can have them all.

That is where the gap lies. And that is where the opportunity is.

Risk warning

Risk warning