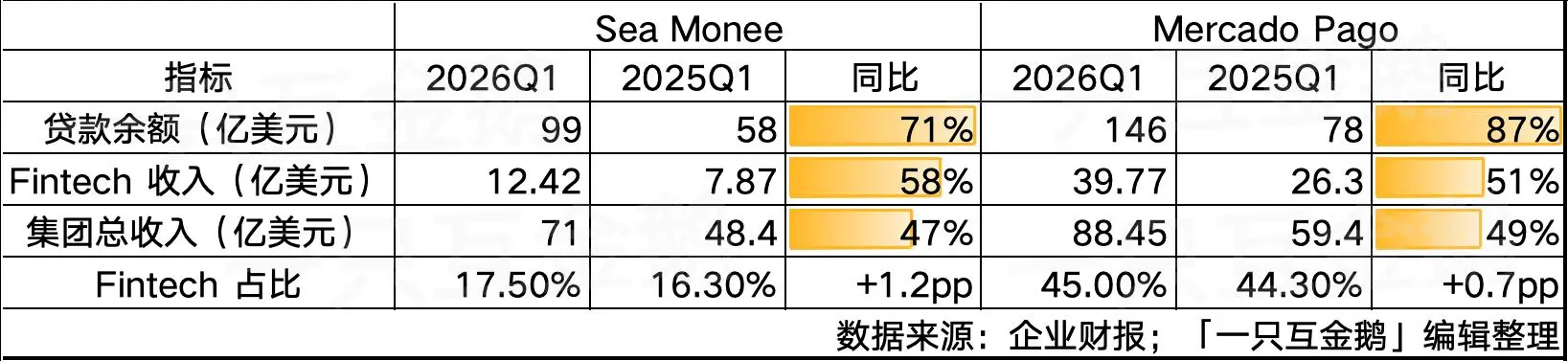

The two giants are racing in "credit": loan balances of 9.9 billion vs 14.6 billion USD, Brazil has become the main battlefield

When we see the domestic credit market growing slowly, with major lending platforms and consumer finance companies tightening their strategies and cautiously controlling volume; in stark contrast, the overseas credit sector is迎来 a period of rapid expansion.

When we see the domestic credit market growing slowly, with major lending platforms and consumer finance companies tightening their strategies and cautiously controlling volume; in stark contrast, the overseas credit sector is迎来 a period of rapid expansion.Author: Xiao Hui Ya, a Fintech Goose

When we see the slow growth of the domestic credit market, with major lending platforms and consumer finance companies tightening strategies and cautiously controlling volume; in stark contrast, the overseas credit sector is entering a rapid expansion cycle.

Especially in the Southeast Asian and Latin American markets, which are also the main choices for Chinese fintech companies going abroad.

In the past two years, "a Fintech Goose" has continuously focused on two highly representative companies in the Southeast Asian and Latin American markets------

① Monee, belonging to Sea (Shopee);

② Mercado Pago, the financial sector of Mercado.

From the Q1 financial report data this year, both companies' credit businesses continue to grow steadily and bring more momentum to the group's revenue.

As of the end of Q1 2026:

Monee's loan balance is $9.9 billion (approximately RMB 67 billion), a year-on-year increase of 71%;

Mercado Pago's loan balance reached $14.6 billion (approximately RMB 98.7 billion), a year-on-year increase of 87%.

In Q1 2026:

Monee's revenue reached $1.242 billion (approximately RMB 8.4 billion), accounting for 17.5% of Sea Group's total revenue, up from 16.3% in Q1 2025;

Mercado Pago's revenue reached $3.977 billion (approximately RMB 26.9 billion), accounting for 45% of Mercado Group's total revenue, up from 44.3% in Q1 2025.

We are not unfamiliar with the development logic of these two "e-commerce + fintech" companies. Domestic giants like Ant Group, JD.com, and ByteDance have all grown along this path.

However, the differentiated strategies of these two companies in Southeast Asia and Latin America are also highly valuable references, worthy of study by domestic fintech and internet giants going abroad.

In the following text, "a Fintech Goose" will summarize the key data and development highlights of these two giants in Q1 2026.

01 Sea Monee: Obtained Financial Credit License in Brazil in Q1

From the data, the fintech sector, which is Monee's revenue growth rate (year-on-year +57.8%), significantly exceeds that of e-commerce Shopee (+45.1%) and gaming Garena (+40.6%).

It can be seen that the revenue share of the fintech sector Monee continues to increase within the entire Sea (Sea Group).

Specific data for the fintech sector:

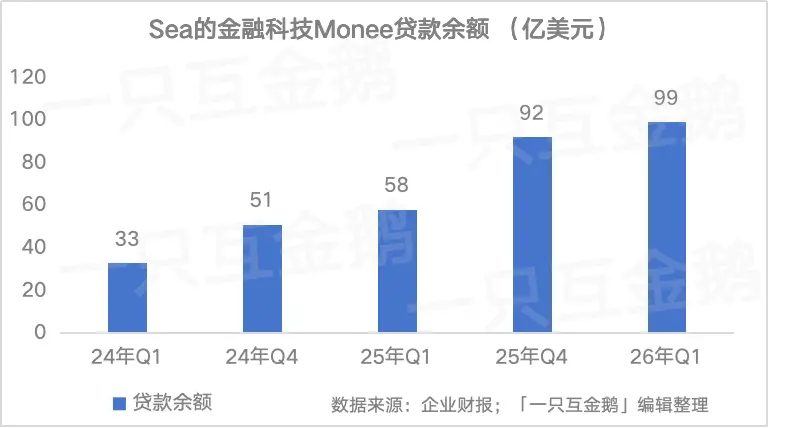

(1) Loan Balance

In two years, the loan balance increased from $3.3 billion to $9.9 billion, expanding to three times the original size.

In two years, the loan balance increased from $3.3 billion to $9.9 billion, expanding to three times the original size.

Each quarter, the loan balance has maintained high double-digit growth.

In the investor conference call, management mentioned that generally, Q1 is usually a low season for consumption, but this year Q1, Sea Monee's loan balance still achieved a +7.5% quarter-on-quarter growth.

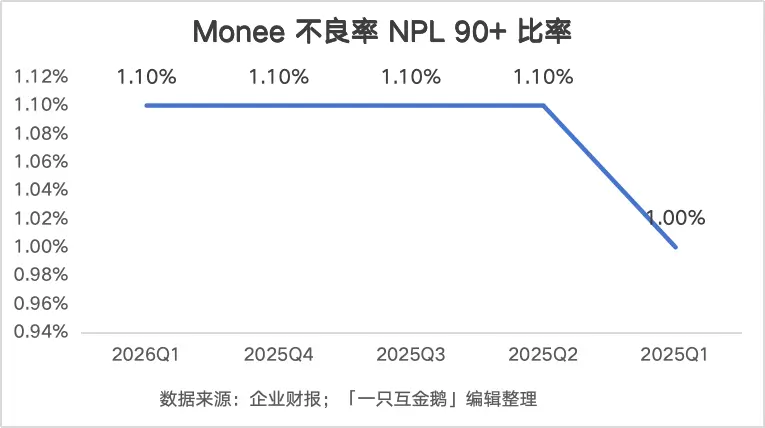

(2) Risk Performance:

With a loan scale growth of 71% within a year, the 90-day delinquency rate only slightly increased from 1.0% to 1.1%, remaining stable at 1.1% for four consecutive quarters.

The delinquency rate remains stable, which to some extent indicates that its risk model has withstood the test under rapid credit scale growth.

Important note on the delinquency rate metric: The NPL 90+ ratio's denominator includes the total loan principal of "on-book + off-book."

The financial report provides a specific explanation:

Off-book mainly refers to channeling arrangements, where partner financial institutions lend on the Sea platform.

(3) Three Growth Paths for Credit Business

Sea clearly outlined three growth paths for Monee's credit business during the conference call:

Path One: Deepen Existing User Relationships

As understanding of user repayment behavior deepens, gradually release more credit limits. This is reflected in the average loan balance increasing from $200 to $250 (+25%) (approximately RMB 1,670).

Path Two: Acquire High-Quality New Users

Launch special activities targeting customer segments with better risk scores and stronger purchasing power, attracting these users with competitive pricing, higher limits, and longer repayment terms.

Management clearly stated, "Early signs show success."

Path Three: Expand Credit Scenarios Outside the Shopee Ecosystem (Off-Shopee)

This is the most imaginative growth direction.

Among them, the SPayLater loans outside Shopee in Thailand and Indonesia exceeded 20% of the SPayLater portfolio by the end of Q1.

It is worth noting that strong growth in high-value categories (such as electronics and two-wheelers) was seen in Indonesia, where installment credit plays an important role in purchases of these categories.

(4) Brazil Market, Bright Growth

In Q1 2026, the Brazilian market became Sea's fastest-growing market.

Whether in the e-commerce Shopee sector or the fintech Monee, there are highlights:

Shopee Brazil:

Q1 is the fastest-growing market while remaining profitable;

GMV growth exceeds the market average, driven by active buyer numbers, purchase frequency, and average order value;

Delivery timeliness improved by more than one day year-on-year;

Three new fulfillment centers were established, bringing the total to five;

ShopeeMall GMV more than doubled year-on-year, accounting for about 15% of Brazil's GMV;

Launched the ShopeeVIP membership program in Brazil in April (over 10 million members in Asia).

Brazil Fintech (Monee Brazil):

The product that merged SPayLater + cash loan limits launched last year highly aligns with Brazilian consumers' credit usage habits, driving strong growth in user numbers and repurchase rates.

In Q1 2026, the loan scale in Brazil exceeded $1 billion, a year-on-year increase of 250%, becoming the fourth market with a loan scale exceeding $1 billion.

"A Fintech Goose" note: The other three markets exceeding $1 billion are Indonesia, Thailand, and Malaysia.

The penetration rate of SPayLater GMV in Brazil is only about 10%, far lower than in mature markets, indicating significant development potential;

The per capita loan balance in Brazil doubled year-on-year, with extremely strong user stickiness.

A key highlight is------obtaining a key license!

In Q1 2026, Sea was approved for the SCFI license in Brazil (Sociedade de Crédito, Financiamento e Investimento), also known as the Brazilian financial credit license.

Obtaining this license can broaden the range of financial services offered in Brazil, laying a compliance foundation for more diversified credit business in the future. This is a key milestone.

02 Mercado: Q1 Credit Business Revenue in Brazil is $1.124 Billion (approximately RMB 8 Billion)

Next, let's look at Mercado.

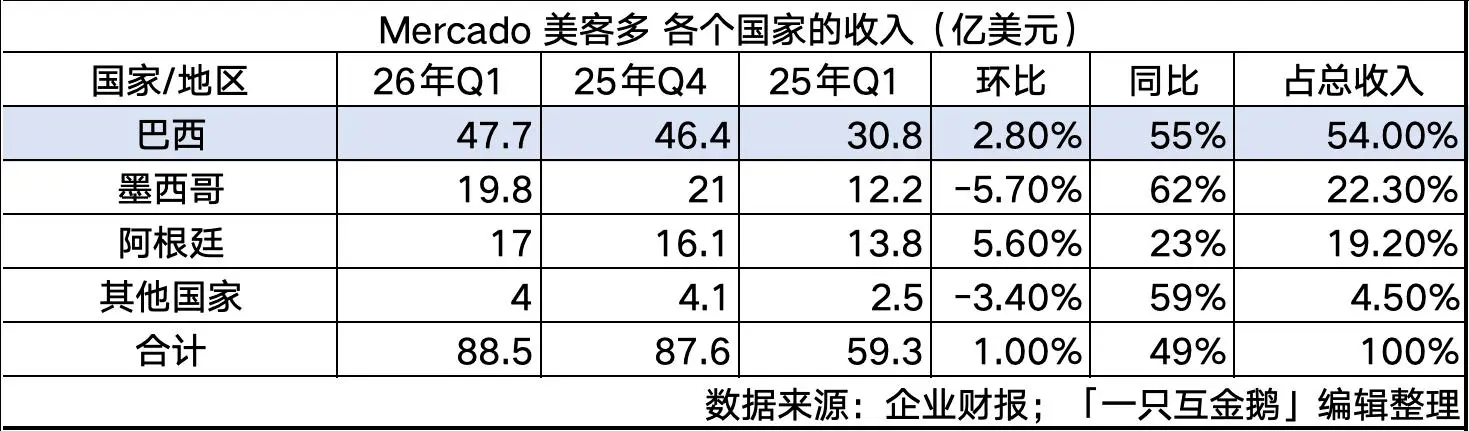

Like Sea, Brazil is also a very important part of Mercado's operations in all its countries.

Looking at the Q1 2026 financial report, if we break down revenue by country:

Brazil contributed more than half of the revenue, accounting for 54% of total revenue;

Mexico is the fastest-growing market, with revenue increasing by +62% year-on-year;

Argentina has a relatively moderate growth rate, with revenue increasing by +23% year-on-year, but considering Argentina's inflation and currency depreciation, the actual local currency growth rate is very high;

Other countries, including Chile, Colombia, and Peru, have a smaller overall scale, accounting for only 4.5% in total.

If we look at the business segments, in Q1 2026, the e-commerce segment saw a slight quarter-on-quarter decline (seasonal low), but the Fintech sector grew against the trend with a +4.1% quarter-on-quarter increase.

Interestingly, when further breaking down the fintech sector, credit income has surpassed financial services income for the first time, becoming the largest engine of Fintech.

That is: the credit business supports its overall performance.

In previous articles, "a Fintech Goose" has detailed Mercado's credit business.

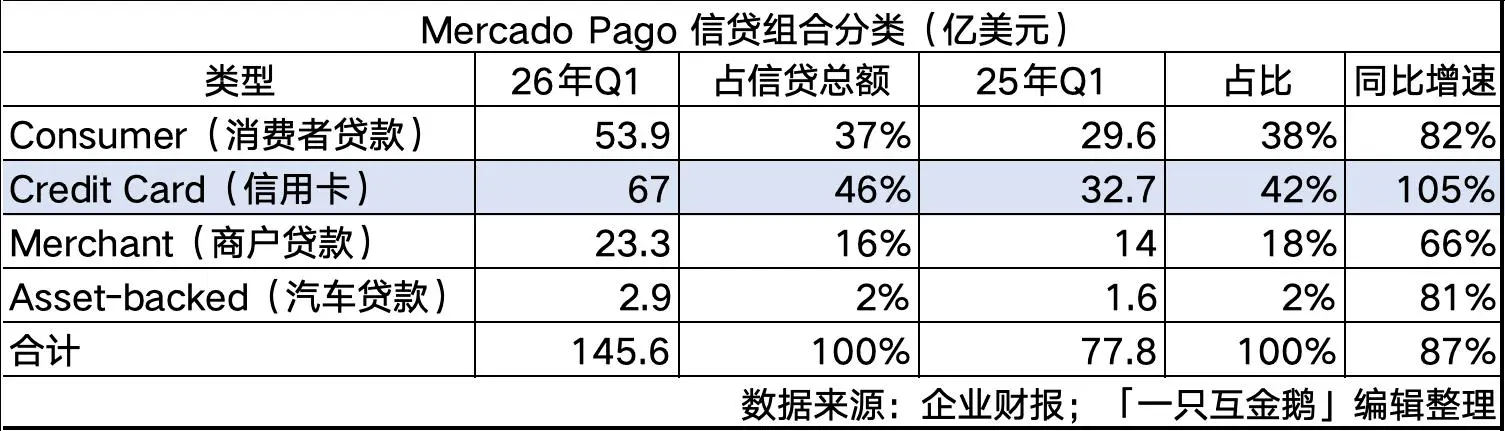

This includes:

① Consumer loans; ② Credit card business; ③ Merchant loans; ④ Auto loans.

Looking at the Q1 2026 data:

The loan scale of the credit card business has seen significant growth (+105%), and its scale share has reached 46%, dominating the majority.

Regardless of the country, credit cards are a business with a very long investment-return cycle.

In the Latin American region, the initial costs of issuing credit cards are extremely high, with zero annual fees + a maximum of 40 days interest-free + up to 18 months interest-free installments, along with substantial subsidies for customer acquisition. The costs required are very high.

Additionally, Brazilian users are accustomed to interest-free installments, so it takes a long time for users to transition from "taking advantage" to "generating interest income."

(1) Strategic Significance of Credit Cards

In the investor conference call, management repeatedly mentioned the strategic significance of the credit card business.

They even described it with a phrase: "Investing in credit cards is as important to Mercado Pago as launching a self-built logistics network was to e-commerce platforms ten years ago."

Summarizing several key points of Mercado's credit card business:

Issuance volume: 2.7 million new cards issued in Q1, with credit card TPV increasing by 90% year-on-year, and MAU increasing by 68% year-on-year.

Cross-selling flywheel: A large number of credit card users were previously just platform buyers, and now they have become active Fintech users.

Ecosystem effect: Credit cards enhance platform conversion rates, individual user GMV, and cross-ecosystem transaction volume.

Five-year investment in Brazil: Brazil's credit card has been invested in for five years, with old batches maturing as expected, gradually offsetting the dilution effect of new batches.

Acceleration in Mexico: Credit card issuance in Mexico is accelerating, with an attractive payback period.

New starting point in Argentina: Credit cards were just launched in Argentina in August-September last year, with early performance similar to Brazil's initial stage.

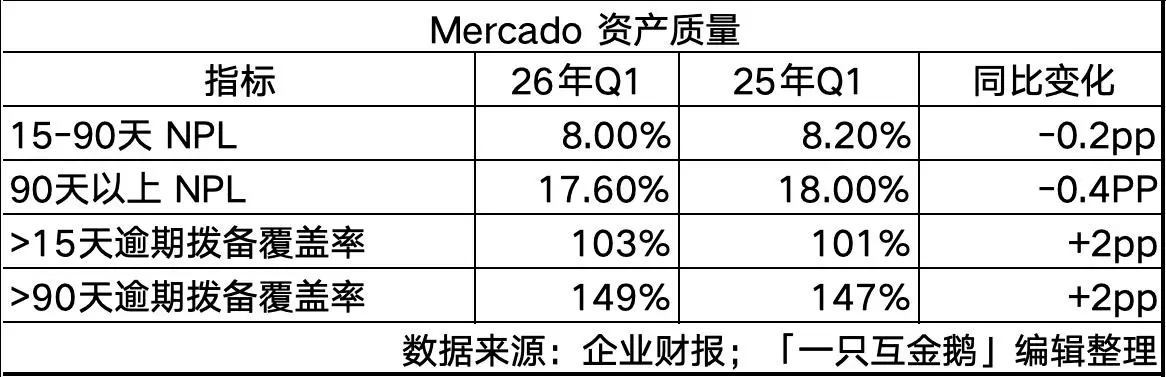

(2) Credit Risk Performance

With a credit portfolio growth of 87%, the delinquency rate has decreased year-on-year, and provisions for severely overdue loans are over 1.5 times, increasing the risk buffer.

With a credit portfolio growth of 87%, the delinquency rate has decreased year-on-year, and provisions for severely overdue loans are over 1.5 times, increasing the risk buffer.

It is particularly noted that a delinquency rate exceeding 17% is alarming, but local loan business interest rates are also higher than in our country.

According to Mercado's NIMAL and public information from the Brazilian market:

Personal Loans annual interest rate is 146%;

Payroll Loans annual interest rate is 28% (secured, lowest rate);

Credit card revolving interest annual interest rate is 451% (Brazilian Central Bank, March 2026).

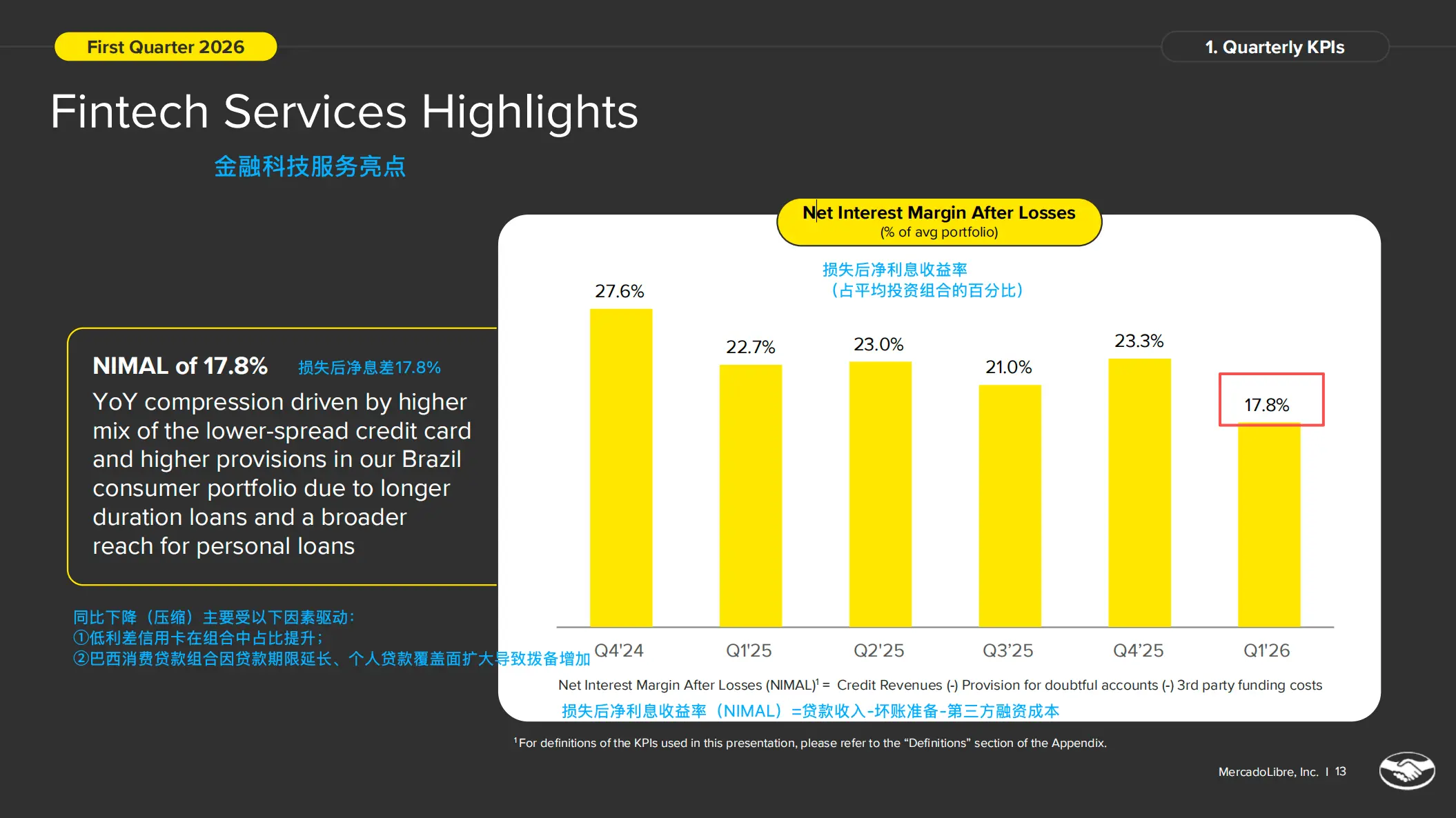

(3) Net Interest Margin Still Strong

Screenshot source: Mercado investor report (click image for a larger view)

Mercado's net interest margin remains strong.

Although it decreased from 22.7% in Q1 2025 to 17.8% in Q1 2026, a decline of 4.9 percentage points, it is still at an extremely high level.

It is worth noting that domestically, for example, China Merchants Bank's NIM in Q1 2026 was only 1.83%; WeBank, known as the "profit king" among domestic private banks, had an NIM of only 4.19% in 2025 (before provisions).

Moreover, Mercado's data metric is even stricter.

Mercado NIMAL = credit income - bad debt provisions - funding costs, that is: net interest margin after deducting bad debts

Domestic banks' NIM = (interest income - interest expenses) / interest-earning assets, that is: before deducting bad debts

Mercado's investor conference call mentioned: NIMAL decreased by 4.9 percentage points year-on-year, mainly due to:

Increased proportion of credit cards (2/3 of the compression comes from this factor): Initial NIMAL for credit cards is lower because full expected loss provisions need to be accounted for when issuing cards;

Extended loan terms and expanded coverage for Brazilian consumer loans (1/3 of the compression): Terms extended from 5 months to 8 months, reaching more credit segment users.

It is noteworthy that each sub-portfolio remains profitable. The consumer loan portfolio still maintains double-digit profit margins, and merchant loans have the highest interest spread. Credit cards operate on a "loss first, profit later" model, and the old batches of Brazilian credit cards have already started to become profitable.

(4) Brazil Market, the Biggest Surprise

Management expressed unexpected joy and importance regarding the Brazilian market in the shareholder letter:

"Twenty-six years after launch, Mercado Libre is growing at startup rates across all of our major markets. Nowhere is this more evident than in Brazil, our largest and most established market, where growth is not just fast -- it is accelerating."

Translation: After 26 years of establishment, Mercado Libre is growing at startup rates, most notably in Brazil------growth is not only fast but also accelerating.

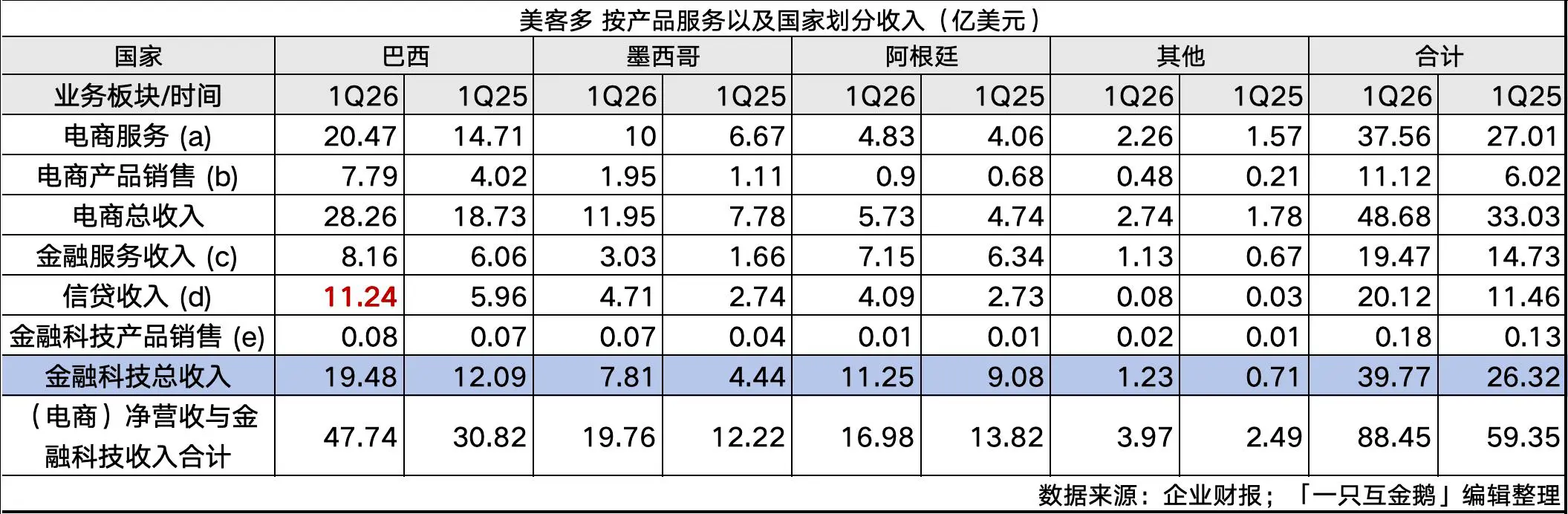

Mercado's e-commerce revenue in Q1 2026 was $2.826 billion, a year-on-year increase of 51%.

Specifically, in Q1, e-commerce GMV grew by 38% year-on-year, the number of items sold increased by 56% year-on-year, and the number of active buyers grew by 32% year-on-year.

All this growth mainly stems from the decision made in 2025 to lower the free shipping threshold, which management called "one of the most important decisions of 2025"------the free shipping threshold was reduced to R$19 (Brazilian Real) (approximately RMB 25.49), greatly lowering the psychological barrier for first-time purchases.

Now looking at the fintech sector------

The fintech sector in Brazil contributed $1.948 billion in revenue in Q1 2026, accounting for 22.0% of the group's total revenue;

Among them, the credit portion's revenue was $1.124 billion (approximately RMB 7.6 billion), accounting for 12.7% of the group's total revenue. Last year's Q1 revenue for this segment was $596 million, which means a year-on-year increase of 89%.

Currently, Brazil's credit business is undoubtedly an important growth engine for Mercado.

The credit income from one market already accounts for nearly one-eighth of Mercado's total global revenue.

How to say, although Sea and Mercado are both betting on Brazil, with growth rates often doubling, it is indeed a highly attractive market.

However, this rapid growth seems to belong only to the giants, while other fintech players------

Without e-commerce transaction scene data, without a payment closed loop to nurture users, it is extremely difficult to do credit in Brazil. Additionally, the local tax system is particularly complex, making it hard for general players to establish a foothold, and it is not highly recommended.

Risk warning

Risk warning