Bitget UEX Daily Report|The US and Iran will hold the next round of negotiations in Pakistan on July 11; Micron is investing $9.3 billion to expand its HBM factory in Hiroshima (July 6, 2026)

Bitget UEX Daily Report

Bitget UEX Daily Report# 1. Hot News

Federal Reserve Dynamics

Remarks by Federal Reserve Officials and Policy Expectations

- Federal Reserve Governor Waller and other officials spoke today, with the market focusing on their latest statements regarding the interest rate path; combined with recent economic data, there are still expectations for rate cuts, but the pace is cautious.

- Institutional analysis shows that easing inflation and employment data provide room for policy adjustments. Market impact: The remarks may strengthen short-term fluctuations in the dollar and affect the pricing of safe-haven assets like gold.

International Commodities

Next Round of US-Iran Negotiations and OPEC+ Dynamics

- Saudi media reported that the next round of negotiations between the US and Iran will take place on July 11 in Pakistan, discussing sanctions, frozen funds, and nuclear issues, with the Iranian delegation to be confirmed after Khamenei's funeral; OPEC+ has decided to increase production by 188,000 barrels per day in August.

- The number of vessels in the Oman route of the Strait of Hormuz has significantly decreased, with Iran tightening control, causing several ships to turn back or change course. Market impact: Geopolitical uncertainty supports short-term fluctuations in oil prices, while the increase in production may alleviate supply pressures, but actual execution is affected by shipping routes, and demand for safe-haven precious metals may remain.

Macroeconomic Policy

Bank of Korea Warns of Leverage ETF Risks

- The Bank of Korea warned that single-stock leveraged ETFs linked to Samsung and SK Hynix may exacerbate market concentration and volatility, with discussions on regulatory measures taking place today.

- Policy focus is on the unilateral flow of funds and the risk of amplifying retail investor losses. Market impact: Strengthened regulation may alleviate volatility in the semiconductor sector, but in the short term, it may affect trading enthusiasm for related stocks.

# 2. Market Review

Commodity & Forex Performance (Real-time Updates)

- Spot Gold: $4,179/oz, 24h Change +0.11%

- Spot Silver: $62.8/oz, 24h Change +0.75%

- WTI Crude Oil: $68.32/barrel, 24h Change -0.6%

- Brent Crude Oil: $71.55/barrel, 24h Change -0.35%

- US Dollar Index (DXY): 100.88 points, 24h Change +0.02%

Driving Factors Analysis: Geopolitical tensions remain the core driving force, with the prospects of US-Iran negotiations intertwined with risks of shipping disruptions in the Strait of Hormuz, leading to obstacles in tanker transportation. Despite OPEC+ announcing an increase in production, actual supply recovery is slow, resulting in narrow fluctuations in oil prices. The dollar index remains relatively stable, reflecting cautious expectations regarding Federal Reserve policy, with inflation data and employment conditions shaping market judgments on the rate cut path. Gold and silver, as safe-haven assets, benefit from uncertainty, with institutions generally believing that the short-term linkage logic leans towards risk aversion, but if negotiations make progress, commodity prices may face downward pressure. Overall, the correlation between assets shows that macro policies and geopolitical factors dominate short-term trends, and investors need to pay attention to the actual impact of shipping dynamics on energy supply.

Cryptocurrency Performance

- BTC: $63,745, +1.2%

- ETH: $1,792, +1.18%

- Total Cryptocurrency Market Cap: $2.26 trillion, 24h Change -0.55%

- Market Liquidation Situation: Total liquidation in 24h $168 million, short position liquidation $107 million

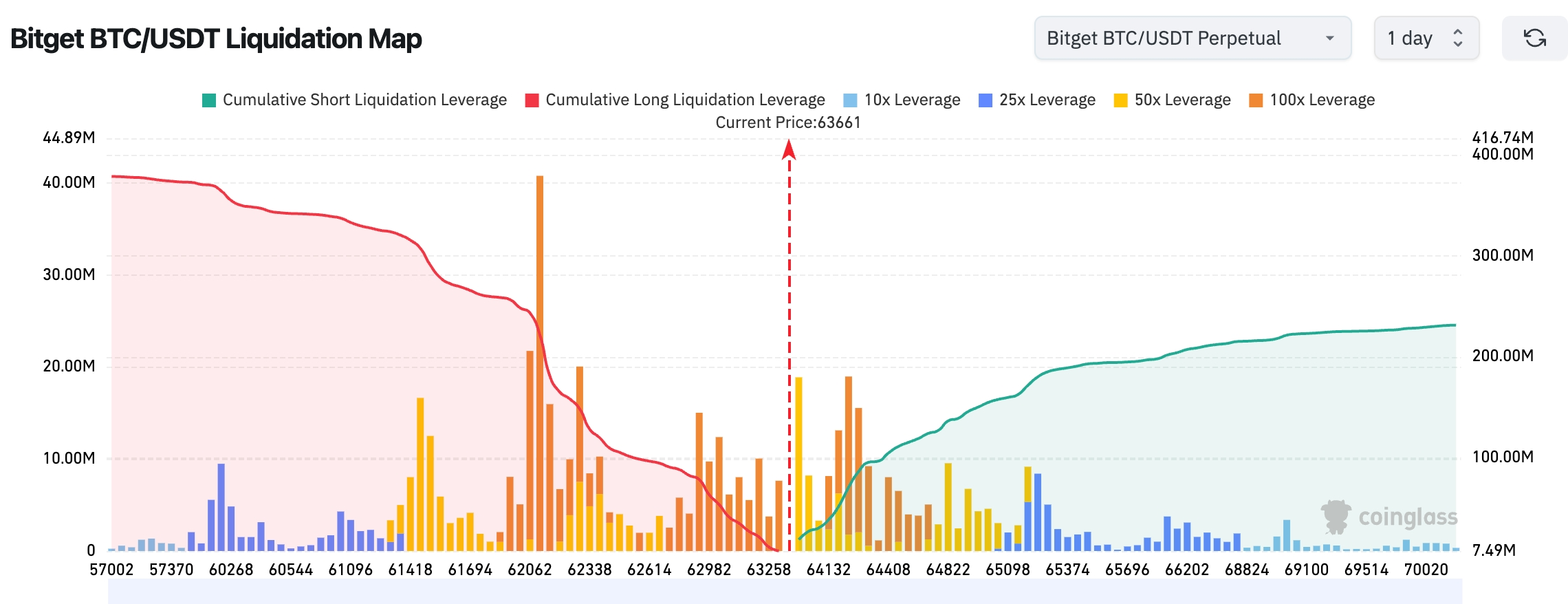

- Bitget BTC/USDT Liquidation Map: Near current price, major resistance above focuses on key integer levels, support below focuses on recent lows, leverage liquidation risk amplifies with volatility.

Driving Factors Analysis: The macro environment and geopolitical factors provide background support for the cryptocurrency market, with uncertainties surrounding US-Iran negotiations and expectations from Federal Reserve speeches driving cautious sentiment in risk assets. ETF fund flows show sustained institutional interest, while leverage liquidation data reflects market deleveraging amid volatility. Technically, BTC and ETH show mild differentiation, with BTC's dominant position solidifying while ETH is relatively lagging due to ecological events; institutional consensus believes that the trend of AI and blockchain integration and policy signals will continue to shape mid-term trends, while short-term attention should be paid to geopolitical events affecting risk appetite. Overall, the trend leans towards fluctuations, with attention to fund inflows and liquidation maps as short-term guidance.

US Stock Index Performance

- Dow Jones: 52,900.07 points, +1.14% (+594.83 points)

- S&P 500: 7,483.24 points, +0.01% (+0.01 points)

- Nasdaq: 25,832.67 points, -0.80% (-207.36 points)

Tech Giants Dynamics

- NVDA: $194.83, -1.39%

- AAPL: $308.63, +4.84%

- MSFT: $390.49, +1.62%

- GOOGL: $359.91, -0.36%

- AMZN: $242.67, +0.40%

- META: $582.90, -4.90%

- TSLA: $393.45, -7.49%

- MU: $975.56, -5.49%

- SPCX: $162.00, +2.83%

The tech sector shows significant differentiation characteristics: AAPL rebounded strongly (+4.84%), interpreted by the market as related to expectations for a foldable iPhone product; MSFT rose slightly, benefiting from ongoing AI ecosystem layouts. In contrast, TSLA (-7.49%) and META (-4.90%) showed significant pullbacks, mainly due to valuation pressures and short-term profit-taking. In the semiconductor sector, NVDA fell slightly, while MU (-5.49%) faced short-term adjustment pressure despite positive news from the Hiroshima expansion. The Micron expansion project and Samsung's DRAM price increase expectations mentioned in the Futu Daily Report further confirm the driving effect of AI demand on the storage industry chain. Overall, core AI targets show relatively strong resilience, while high valuations or event-driven stocks experience increased volatility, with significant market rotation characteristics.

Sector Movement Observation

The semiconductor/storage sector shows significant volatility (the sector has shown clear differentiation intraday/short-term, with some stocks exhibiting outstanding elasticity under AI themes, but high base valuations and profit-taking pressures have led to overall increased volatility).

- Representative Stock: Micron Technology (MU) was boosted by positive news from the Hiroshima expansion, with the latest closing price around $975.56, with a daily change of about -5.49% (after a high-level pullback, signs of recovery appeared during the day, with active trading volume); related dynamics of SK Hynix continue to ferment, showing significant sector linkage effects.

- Driving Factors: The demand for training and inference computing power for large AI models continues to explode, directly pushing up the demand for advanced storage chips like HBM. Micron's $9.3 billion (approximately 1.5 trillion yen) Hiroshima factory expansion project has officially started, which is a key measure in its global capacity layout, with significant increases in HBM shipments expected in the second half of 2028; the Japanese Ministry of Economy, Trade and Industry provides subsidies of up to 500 billion yen, significantly lowering the capital expenditure threshold and strengthening the advantages of localizing the supply chain. Additionally, Samsung Electronics has verbally notified end customers of a 20% increase in average DRAM prices for the third quarter, reflecting good upstream inventory depletion and enhanced bargaining power, with price transmission expected to support industry gross profit recovery. SK Hynix is advancing a large-scale IPO in the US (potential scale of about $29 billion), aiming to attract global AI-focused investors and further enhance valuation anchoring and liquidity. Overall, industry capital expenditure and technological iteration are accelerating, with AI infrastructure demand becoming the core driving force, but short-term attention is still needed on valuation pressures and volatility risks brought by geopolitical factors.

# 3. In-depth Analysis of US Stocks

1. Micron Technology (MU) - Hiroshima Expansion Project

Event Overview: Micron Technology has officially launched the expansion project for its Hiroshima factory in Japan, with a total investment of approximately $9.3 billion (1.5 trillion yen), focusing on the production of high-bandwidth memory chips, including HBM. This project is an important part of its global expansion plan, aimed at meeting the strong demand for high-performance memory in the AI industry, with HBM shipments expected to start in the second half of 2028. The Japanese Ministry of Economy, Trade and Industry provides subsidies of up to 500 billion yen in support. Micron's CEO emphasized at the groundbreaking ceremony that the first batches of HBM wafers for core AI storage technology will be manufactured in Hiroshima. At the same time, storage giants like SK Hynix are also advancing their expansion plans.

Market Interpretation: Institutions generally believe that this move significantly strengthens Micron's strategic position in the AI storage supply chain. HBM, as a key component of AI accelerator processors like those from NVIDIA, currently faces severe global supply shortages. By localizing production in Japan, Micron can obtain government subsidies to reduce capital expenditures while enhancing supply chain resilience and geopolitical diversification advantages. Combined with Samsung's DRAM price increase expectations, the industry is shifting from price competition to competition based on technology and capacity barriers, increasing long-term growth certainty. However, short-term attention is still needed on the pace of HBM technology iteration and the realization of end-user demand.

Investment Insight: Focus on tracking the ongoing pull of the AI capital expenditure cycle on HBM demand, as well as the progress of Micron's project production and customer certification.

2. Apple (AAPL) - Foldable Phone Supply Outlook

Event Overview: TF International analyst Ming-Chi Kuo's latest industry survey shows that Apple's foldable iPhone is expected to assemble and ship about 7-8 million units in the second half of 2026, with only 500,000 to 1 million units shipped in the third quarter (about 10% of the total). In contrast, the inventory of iPhone 18 Pro/Pro Max during the same period is expected to reach 20-22 million units. Kuo predicts that the foldable iPhone is likely to be launched alongside other models, but the pre-order and official sale times will be later, with supply tightness expected to continue until the end of the year, similar to the launch rhythm of the iPhone X in 2017.

Market Interpretation: The market views this as an important signal of Apple's hardware innovation cycle. The foldable form factor is expected to open up new growth spaces; although initial shipment volumes are limited, it can solidify Apple's differentiated positioning in the high-end market. Supply chain validation and inventory rhythm will be key observation indicators, with initial supply tightness potentially reinforcing product scarcity and brand premium.

Investment Insight: Pay attention to how Apple's product strategy details reshape hardware cycle expectations, as well as the actual progress of supply chain validation and inventory data.

3. SK Hynix - US Listing Plan

Event Overview: SK Hynix plans to conduct an IPO in the US with a scale of about $29 billion, which could become one of the largest foreign company IPOs in history, aiming to attract global AI investors. The underwriting fee is about 0.5%, and the issuance scale can reach up to 2.5% of the issued shares. This move primarily targets international investors who cannot directly enter the Korean market, providing a convenient channel to participate in pure AI memory targets.

Market Interpretation: Institutions believe that in the current AI boom context, the timing of the US listing is favorable, as it can enhance the company's liquidity and valuation attractiveness while directly connecting with the largest scale of AI capital globally. Institutional investors holding Micron stock indicate that the market is in a period of extreme enthusiasm for chip stocks, and this move will help SK Hynix gain broader capital support in the AI memory cycle.

Investment Insight: The connection to the global capital market will further strengthen semiconductor AI theme investment opportunities, and it is recommended to continuously monitor the final issuance scale and subscription enthusiasm.

4. Tesla (TSLA) - Employee AI Spending Restrictions

Event Overview: An internal memo from Tesla shows that starting July 6, employees will have a weekly spending limit of $200 on AI tools, with any excess requiring management approval. This move aims to balance the promotion of AI applications with cost control, and employee use of xAI's Grok model will not count against the limit.

Market Interpretation: The market interprets this as a signal that Tesla is shifting from "broad deployment" to "precise control" in its AI investments. On one hand, it reflects the company's emphasis on the actual efficiency of AI tool usage, while on the other hand, it shows that during the rapid expansion of AI applications, token-based costs have begun to exert pressure on operations. Institutions believe that this move may temporarily affect the speed of some AI experiments, but in the long term, it will help concentrate resources on core projects, aligning with Tesla's AI strategic direction in robotics and autonomous driving.

Investment Insight: Monitor the effects of Tesla's AI cost control measures on internal efficiency improvements, as well as changes in resource allocation between xAI and its own AI models.

5. NVIDIA (NVDA) - Core Beneficiary of HBM Demand

Event Overview: With the expansion of Micron in Hiroshima, SK Hynix's capacity increase, and Samsung's DRAM price hikes, NVIDIA, as a global leader in AI accelerators, has become the most direct beneficiary of HBM demand in the storage industry chain. Multiple institutions predict that the HBM market size will grow significantly by 2026, with NVIDIA's supply locking and technical cooperation deepening in the HBM3E/HBM4 era.

Market Interpretation: Institutional views suggest that HBM has become the "new oil" of AI infrastructure, and Micron and SK Hynix's capacity expansions are essentially serving core customers like NVIDIA. By deeply binding with storage manufacturers, NVIDIA can not only ensure the supply of key components but also maintain a leading advantage in the technology roadmap. Although short-term stock prices are influenced by overall tech sector volatility, the long-term trend of AI capital expenditure remains unchanged, and its core position in the AI ecosystem remains solid.

Investment Insight: Focus on tracking the actual expansion progress of the HBM supply chain and the demand realization of NVIDIA's next-generation platforms (such as Rubin), paying attention to its pricing power and ecosystem control in the AI stack.

# 4. Market & Project Dynamics

- Garrett Jin, the agent for "1011 Insider Whale," pointed out in an analysis that there has been a significant change in market structure this week, with funds within the AI industry chain being redistributed. Signs of a peak in the storage chip market are emerging, with Micron's stock price encountering resistance and retreating around $1,250, despite better-than-expected earnings reports. The stock price is still declining in volume, showing typical characteristics of "weakening after good news is priced in." Similarly, SK Hynix and Samsung Electronics in the Korean market are also weakening, with data showing that over the past two months, foreign capital has withdrawn more than 100 trillion won (about $65 billion) from the Korean stock market. The real direction of fund support is not in small and mid-cap AI concept stocks but in core cloud computing giants represented by Google, Microsoft, and Amazon.

Garrett Jin believes that the logic behind this round of fund migration is the "Token Optimization Trend": As more simple tasks are handled by low-cost models, value will gradually concentrate in the cloud service layer rather than the foundational model layer, which constitutes the core moat of super-large cloud vendors.

Yesterday, Strategy founder Michael Saylor released information related to Bitcoin Tracker again. According to previous patterns, Strategy always discloses information about increasing Bitcoin holdings the day after relevant news is released.

Bitcoin News cited analyst @gaah_im, reporting that the Bitcoin miner cycle pressure composite index has fallen to a new low for 2026, entering a historically "undervalued" range. This index combines the Puell Multiple and the inverse miner capitulation index, which measure miner income and cost dynamics, respectively. Their synchronous signals have historically been strong indicators of Bitcoin cycle bottoms. Previous occurrences of this composite index collapsing simultaneously appeared near major Bitcoin bottoms in 2015, 2018, 2020, 2022, and 2024. The only previous instance of this composite index reaching 0.00 was during the capitulation period in 2015, when Bitcoin fell from about $300 to $160 within a week. The reoccurrence of similar behavior in 2026 marks that miner pressure has again reached a historically rare level.

Data shows that the proportion of meme coins in the market capitalization of altcoins has dropped to 3.7%, the lowest level since February 2024, with the number of holders also reaching a three-year low. This ratio exceeded 10% in November 2024 and has since continued to decline.

CryptoQuant analyst Darkfost pointed out that the Bitcoin Sharpe ratio has once again reached an extreme negative value, slightly rebounding after falling below -20. The Sharpe ratio is used to measure the relationship between investment risk and return, with negative values indicating higher risk relative to current returns, which corresponds with Bitcoin's third consecutive quarterly decline (latest quarterly drop of 16.1%).

Historically, such extremely pessimistic periods often last for several weeks to months and correspond to a new bottom-building phase, followed by a price restart. Analysts indicate that the data suggests we are approaching this phase, but it should be noted that this observation belongs to a long-term time frame.

- This week, SK Hynix's $29 billion IPO in the US could become the largest foreign company IPO in history, but this is not just about raising funds. More critically, it aims to compete in the hottest area of the current global stock market, namely the memory chips used for AI computing. Daniel Morgan, senior portfolio manager at Synovus Trust, which holds Micron stock, stated that the market is in a period of extreme enthusiasm for chip stocks, and now is a good time for US investors to participate in their stock. Zhou Di, portfolio manager at Thornburg Investment Management, which holds SK Hynix stock, stated that this issuance targets investors who currently cannot enter the Korean stock market. SK Hynix's listing on NASDAQ provides investors with a direct and frictionless opportunity to participate in one of the most attractive pure targets in the AI memory cycle.

# 5. Today's Market Calendar

Data Release Schedule

|-------|----|----------------|------| | 21:45 | US | June S&P Global Services PMI Final | ⭐⭐⭐ | | 22:00 | US | June ISM Non-Manufacturing PMI | ⭐⭐⭐⭐ |

Important Event Forecast

- Remarks by Federal Reserve Governor Waller and others: 23:00 - Focus on interest rates and economic outlook.

- Discussion on Regulation of Single Stock Leveraged ETFs in Korea: Today - Focus on reviewing the impact of market volatility.

Institutional Views:

Well-known investment bank analysts generally believe that the current market is in an environment where geopolitical risks and policy expectations are intertwined. Progress in US-Iran negotiations may alleviate some energy supply concerns, but tensions in the Strait of Hormuz still support oil and gold prices. In the US stock market, the tech sector continues to show differentiation, with AI-driven expansion investments boosting the long-term outlook for semiconductors, while signals of leveraged product regulation may impact emerging market volatility. The cryptocurrency market remains resilient under the support of ETF inflows and macro signals, with institutions recommending attention to data releases and officials' remarks as guidance for risk appetite, maintaining a neutral and cautious allocation overall, prioritizing defensive and high-certainty growth assets. Short-term volatility may increase, but the long-term outlook is positive for AI and energy transition themes.

Disclaimer: The above content is compiled by AI search, with human verification for publication, and should not be considered as any investment advice. The data in the text may inevitably contain deviations, please refer to real-time market data.

Risk warning

Risk warning