Understanding DeFi Liquidity Pools: Lending, AMM, and Options Collateral

Decentralized liquidity pools are one of the key innovations of DeFi. By aggregating liquidity, they can significantly improve asset efficiency and reduce costs.

Decentralized liquidity pools are one of the key innovations of DeFi. By aggregating liquidity, they can significantly improve asset efficiency and reduce costs.This article was published on ChainNews, authored by Ryan Tian, co-founder and CFO of FinNexus

DeFi has brought revolutionary changes to financial operations, one of which is the disruptive use of liquidity pools to power financial markets. Whether liquidity pools or cash pools, these are not innovations of DeFi, but in traditional finance, such pools often imply secretive and opaque fund operations. In contrast, on the blockchain, all transactions are encoded by smart contracts, open to the public, without the need for third-party custody, and the liquidity pools are as transparent as possible. This aggregation of liquidity is economical and efficient within the decentralized finance ecosystem.

DeFi projects have various well-designed liquidity pool models suitable for different application scenarios, and more liquidity pools continue to emerge. Among them, lending pools and DEX liquidity pools are the most common, and recently, a decentralized options margin liquidity pool model has appeared with the development of DeFi.

I. Preview

The table below summarizes the main information introduced in this article.

II. Lending Pool Model

Lending pools are the first type of decentralized liquidity pool generated in DeFi, aimed at facilitating liquidity in decentralized lending markets. Unlike the peer-to-peer lending model where borrowers obtain loans directly from lenders, the lender pool acts as a unified counterparty for lending transactions, with interest rates automatically set by coded algorithms. Currently, the most famous DeFi lending pool projects in DeFi are Compound and Aave.

Compound

Compound is an open-source code money market protocol that allows users to collateralize assets for borrowing. Users deposit their assets into a liquidity pool (i.e., "market") for other users to borrow, and the interest paid by borrowers to the liquidity pool is shared among all asset providers.

When users provide assets, they receive cTokens from Compound in exchange. As interest accumulates on the provided assets, users can redeem their cTokens at a certain exchange rate. This exchange rate is determined by the interest of the underlying asset and increases over time.

In the Compound lending model, there is no distribution process for interest. Instead, by simply holding cTokens, users can automatically earn interest through changes in the exchange rate.

Aave

Aave is a decentralized non-custodial money market protocol where users can act as depositors or borrowers. Depositors provide liquidity to the market to earn passive income, while borrowers can take loans either over-collateralized or under-collateralized (flash loans).

By depositing assets into the Aave liquidity reserve pool, users can earn interest. If users have sufficient collateral in the pool, they can also borrow some assets from the pool.

All deposits in the Aave protocol have a corresponding "aToken," which is an interest-bearing token pegged 1:1 to the value of the underlying asset.

Financial Returns of the Liquidity Pool

The operation of lending pools is relatively simple. Lenders concentrate their funds into a liquidity pool for borrowers to borrow from, and the interest paid by borrowers is shared among all liquidity pool contributors. cTokens from Compound or aTokens from Aave represent shares of the liquidity pool's assets. Although the smart contracts on different platforms may adopt different interest rate mechanisms, the basic principle is similar: the higher the demand for funds in the market, the higher the interest rates.

Additionally, for example, Compound also offers mining rewards for platform governance tokens, shared by both liquidity fund borrowers and lenders to encourage user participation.

Since borrowing and lending activities are always conducted under fully collateralized conditions, lending pools are also referred to as non-loss pools, although this non-loss is relative to the borrowing base currency. (Here we assume that the code is always effective and do not consider vulnerabilities.)

Summary

In summary, lending pools aggregate liquidity with relatively low risk characteristics, which may yield lower returns compared to other pools. Based on the Lego-like interlocking characteristics of DeFi, many projects with yield tracking strategies have emerged in the market, using lending protocols as the foundational framework for their projects to build their own yield tracking structures.

III. AMM Liquidity Pools

AMM Mechanism and AMM Pools

AMM stands for Automated Market Maker, a type of decentralized trading mechanism that relies on mathematical formulas to price assets. Unlike the order book mechanism used in traditional finance to match trades and provide liquidity, the AMM pool mechanism uses pricing algorithms in smart contracts to automatically price assets and create liquidity pools for each trading token. Projects like Balancer even allow the creation of liquidity pools that support trading multiple tokens.

AMM pools provide liquidity for asset trading in an automated manner. In other words, traders do not need to find other counterparties to sell or buy digital assets. Transaction fees are automatically distributed to all liquidity providers based on the size of their shares in the liquidity pool.

Currently, many AMM projects have emerged in the DeFi market, such as Uniswap, Sushiswap, Curve, Balancer, Bancor, Kyber, and DODO. Compared to centralized exchanges (CEX), we generally refer to these projects as AMM mechanism-driven decentralized exchanges (DEX).

Working Mechanism of AMM Pools

AMM pools provide liquidity for token trading, and the number structure of tokens in the pool changes after each transaction. Each transaction in the AMM pool incurs a transaction fee, which is distributed to liquidity participants.

Different AMM platforms adopt different mechanisms. For example, the XYK model used by Uniswap and Sushiswap is one of the most well-known AMM models. In contrast, other projects have automatic market-making mechanisms that differ from the XYK model. Curve is designed specifically for stablecoin and homogeneous coin trading, featuring low slippage algorithms; Balancer allows the use of multiple tokens in one pool while enabling users to customize the composition ratio and transaction fees of the tokens. Bancor v2.1's AMM pool provides users with a single token risk exposure option and mitigates impermanent loss risk; Kyber Network employs an open reserve architecture to establish liquidity; DODO uses a proactive market maker algorithm that allows liquidity providers to deposit only one token in the pool.

Financial Returns of the Liquidity Pool

Due to algorithmic differences across platforms, the financial returns of each platform may vary significantly. In this analysis, we will primarily examine the financial returns of the XYK automated market-making mechanism.

The main sources of income in the liquidity pool are transaction fees and mining rewards. For instance, Uniswap charges a 0.3% transaction fee, which is proportionally distributed to all liquidity providers (LPs) in the pool during transactions.

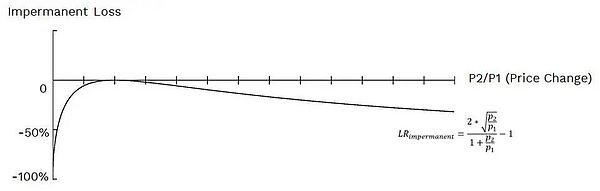

However, it is well known that AMM pools carry the risk of impermanent loss (IL).

IL refers to the losses incurred by liquidity providers in AMM liquidity pools. When liquidity providers supply liquidity to the pool, if the current price of the stored asset changes compared to the price at the time of deposit, they will incur impermanent loss. The greater the price change, the larger the loss. It is important to note that impermanent loss is relative to users who do not enter the pool and merely hold the relevant assets.

Uniswap and Sushiswap adopt the XYK model, where the deposit ratio of trading pairs in the pool is 1:1, resulting in relatively high IL risk. In contrast, Curve's model primarily targets trading with stablecoins and homogeneous coins, resulting in lower trading slippage and correspondingly lower IL risk. Other projects like Bancor and DODO also provide different solutions to address this risk.

Although Uniswap has always been the king among DEXes, the risk of impermanent loss should not be underestimated, as IL affects the financial performance of all assets within the liquidity pool.

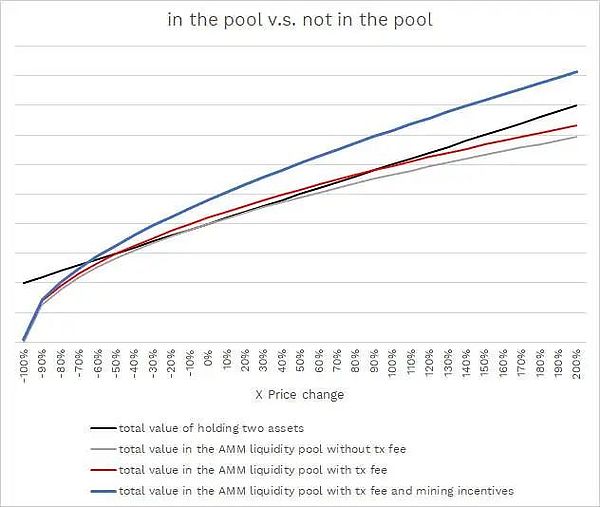

Suppose a user holds two assets of equal value, X and Y, where Y is a stablecoin. The user intends to deposit X and Y into the AMM liquidity pool at a 1:1 ratio. The black line in the diagram below represents the total asset value of holding both X and Y when the price of X changes. The gray curve shows the financial performance when the user contributes equal value of X and Y to the liquidity pool without any transaction fee rewards. It can be observed that holding the assets is more cost-effective, yielding more profit. If the user can earn some trading revenue as compensation, the gray curve will shift upward to the red curve, improving the overall return situation. However, if the price of X deviates significantly from the price at the time of collateral, the user may still incur losses compared to holding the assets without entering the pool.

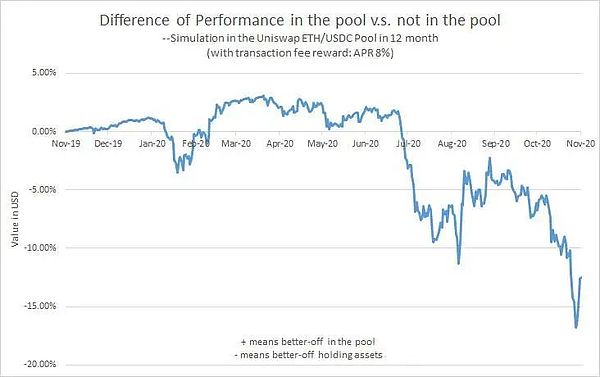

In the diagram below, we simulate the total value comparison of two different investment strategies in the ETH/USDC pool of Uniswap, which joined on November 27, 2019, and maintained for a year. Specific simulation information can be viewed by clicking this link.

Therefore, for holders of volatile assets, providing liquidity in Uniswap and Sushiswap may carry risks, and they cannot always guarantee a profit. Especially when the price of volatile tokens crashes, the AMM algorithm may even consume a significant portion of the value of stable assets in the pool. However, mining rewards can somewhat mitigate this risk, as the incentive measures can push the curve up significantly to the blue curve (assuming a 30% return rate of token X subsidized by the platform during the same period in the previous example). Nevertheless, for most projects, mining incentives remain a relatively short-term and unstable source of returns.

Summary

In conclusion, the risk differences among different AMM pool models are significant. In the XYK model adopted by Uniswap and Sushiswap, the IL risk can be substantial. However, for stablecoin trading pools, the IL risk is much lower. Meanwhile, other AMM pools are innovating algorithms to mitigate IL. Currently, many AMM projects are creating liquidity pools on DEX to enhance trading liquidity and incentivize liquidity providers with high mining rewards. At present, mining compensation is the main source of returns for most users providing liquidity.

IV. Options Margin Pools

Basic Concepts Related to Options

Options are binding contracts that allow users (as buyers) to sell or purchase the underlying asset (commodities, stocks, indices, etc.) at a predetermined price within a specified time frame. As the buyer of the options contract, the user has the right (but not the obligation) to buy or sell the underlying asset.

During the construction phase of the options contract, users must pay a certain consideration, known as the option premium, to the option seller to obtain the right to buy or sell a specific asset at the predetermined price.

Option buyers pay the option premium and only enjoy rights. Option sellers collect the option premium as compensation for granting the corresponding rights to the option holders. To ensure the performance capability of the option seller, options contracts typically require the option seller to deposit collateral to guarantee contract fulfillment.

In traditional finance, theoretically, option sellers bear unlimited potential risk. However, option sellers are usually professional institutional participants who can significantly reduce their risk through more complex hedging tools. Additionally, professional traders and market makers provide order book liquidity for different options trading pairs.

However, if we move these options contracts to the blockchain for decentralized management in the form of smart contracts, some issues may arise. For example, the lack of professional decentralized hedging tools can make it difficult for sellers to participate in trading and diversify risks, while on-chain order book liquidity is often expensive and inefficient.

Decentralized Liquidity Pools

Decentralized options projects represented by Hegic and FinNexus aggregate seller funds in the form of collateral pools to provide liquidity for options trading, which is a significant innovation in DeFi.

In traditional finance, the existence of options agreements typically takes the form of peer-to-peer bilateral contracts. However, Hegic and FinNexus's on-chain options contracts innovatively adopt a pool model, concentrating liquidity in collateral liquidity pools. These liquidity pools serve as a unified counterparty for all options with different terms while providing sufficient collateral for options fulfillment. Risks and option premiums are fairly shared among all liquidity providers based on their shares, so no individual user is at high risk, and all participants can share the profits.

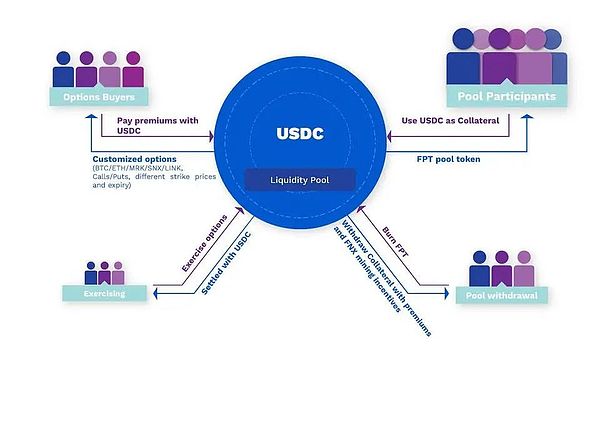

For example, the USDC liquidity pool of FinNexus operates as follows:

Financial Returns of Options Margin Pools

Measuring the financial performance of options collateral asset pools is different from the two models introduced earlier and is relatively complex.

The options in the options collateral pool are closely related to probabilities, and the famous Black-Scholes (BS) options pricing model is based on probability theory. From a mathematical statistics perspective, if the option pricing is reasonable, option sellers are generally more likely to win. However, in practical scenarios, individual cases are usually more complex. Options collateral pools provide liquidity for options trading and act as sellers of various terms of options; this pool model is akin to a fund that sells options. The reliability and stability of the financial returns of options collateral pools may take months or even longer to manifest. Nevertheless, there are still some methods to test the financial status of the pool.

It is well known that crypto assets like BTC and ETH are highly volatile. Therefore, it is reasonable to understand that options may be more favorable to holders, meaning that option holders are more likely to benefit since they only enjoy rights without obligations, and the losses for option holders are limited to the option premium itself.

Is this really the case?

Before starting the mathematical analysis, we must recognize that volatility is an important parameter in options pricing. Options for highly volatile assets are more expensive, and this volatility parameter can be measured by the implied volatility in the BS options pricing model. In the following analysis, we will use historical average volatility to price options.

First, we calculate the average volatility of BTC options from March 29, 2017, to November 26, 2019, covering 1-day, 2-day, 3-day, 7-day, 15-day, and 30-day volatilities.

Second, using the above volatilities, we calculate the prices of ATM options for each expiration date from November 27, 2019, to November 27, 2020, over the past year.

Third, assuming the pool sells an equal number of put and call options, we can derive the profit and loss for sellers on each expiration date during the same period.

Finally, referencing the trading volume on Deribit, we can assign different weights to options with different expiration dates, thereby deriving the average expected APR and maximum drawdown for the options collateral pool.

For detailed calculation information, please click this link.

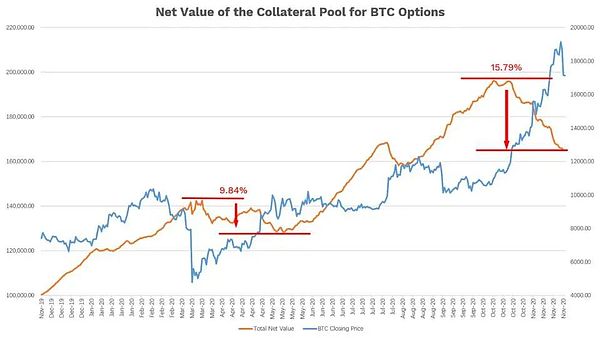

In the above chart, the red curve represents the calculated volatility of the net value of the options collateral pool measured in USD, while the blue curve represents the price of BTC.

In the long run, despite experiencing drawdowns, the liquidity pool as a collective option seller is more likely to be profitable. Over the past 12 months, assuming the collateral in the pool has been fully utilized, the net value of the pool has increased by over 60%, indicating a 60% APR return. If the average utilization rate of the collateral is 50%, then the APR could be 30%, with correspondingly smaller drawdowns.

From the above chart, it can be seen that if the unilateral volatility of BTC prices lasts for a long time, the pool will incur losses, especially during the periods from March to May 2020 and from October to November.

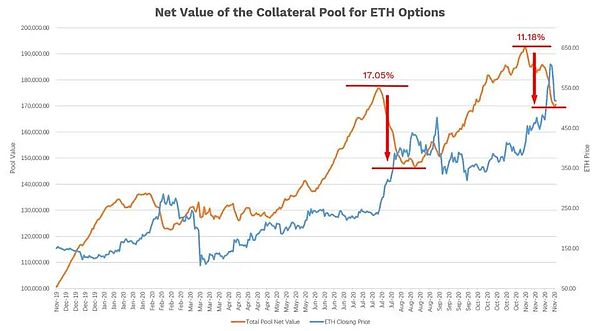

Using the same calculation method, we can simulate the financial returns of the Ethereum options pool over the past 12 months, as shown below. Specific simulation information can be viewed by clicking this link.

Summary

Options collateral pools differ from lending pools and AMM liquidity pools. Options collateral pools provide liquidity and collateral for options, earning option premiums as returns and bearing the risk of option payouts as a cost. If the market price of the underlying asset experiences unilateral changes, losses may occur. However, in the long run, price changes are more beneficial than detrimental for liquidity providers, allowing them to profit.

V. Other Liquidity Pools

In addition to the three types of pool models introduced above, the DeFi market also has other types of liquidity pools, such as the gunpowder pools of YFI, YFII, and Harvest, as well as locked pools used for voting, mining, or enhancing yields, including CRV, Hegic, etc. The returns from these liquidity pools can be measured in different base currencies and can create differentiated risk-return combinations through various strategies. For example, gunpowder pools currently mostly adopt a no-loss mining investment strategy based on base currencies, achieving this by aggregating mining and selling mining returns. As decentralized financial tools continue to combine, gunpowder pools are also developing liquidity pools with more complex investment strategies. Some platforms also have mechanisms where locking platform tokens for mining can accelerate other mining returns, and locking platform tokens can also earn transaction fees as returns while having voting rights in platform decisions.

VI. Conclusion

Decentralized liquidity pools are one of the greatest innovations in decentralized finance. Through decentralized liquidity pools, all liquidity is efficiently aggregated, maximizing asset efficiency while reducing costs. At the same time, blockchain technology ensures the openness and transparency of liquidity pools, free from censorship. Meanwhile, the continuous emergence of DeFi projects and models provides users with increasingly diverse liquidity aggregation solutions, offering more choices for users with different risk preferences. Despite the growing richness of DeFi products, users should carefully study the similarities and differences among various platforms, understand the characteristics of each liquidity pool, and then invest to avoid unnecessary losses.

Risk warning

Risk warning Risk warning

Risk warning