Arthur Hayes: Review, Supply, and the Federal Reserve After the Ethereum Merge

Bitcoin has become a high-energy indicator of dollar liquidity. Isn't that quite sad?

Bitcoin has become a high-energy indicator of dollar liquidity. Isn't that quite sad?Author: Arthur Hayes, Co-founder of 100x

Compiled by: Wu Zhuocheng, Wu Says Blockchain

CZ: Binance Chain, US Government: Ethereum Network

Do you believe in decentralized and/or censorship-resistant networks? I expect that most Satoshi believers (who may be the majority of my readers) would answer yes.

To that, I would say: absolutely not. Many people may be enthusiastic about buying, holding, and using BNB, ETH, and/or other dApps, tokens, but most of them actually do not care about the ideology behind these technologies.

BSC is not decentralized and has never claimed to be decentralized, but that has not stopped the explosive growth of on-chain activity, nor has it affected the appeal of BNB, which is the fifth-largest token by market capitalization.

As of September 21, Lido Finance, Coinbase, and Kraken collectively control over 50% of all staked ETH on the beacon chain. This means they are the most powerful validators, and essentially, they can decide which transactions are processed. What do these three centralized entities have in common? They are all American companies or DAOs backed by American venture capitalists.

According to Crunchbase, 6 out of the 8 investors in Lido Finance are American venture capital firms or have vehicles in the Americas.

This concentration of network power in centralized entities (I should remind you that these entities are subject to US laws and regulations) does not exist under proof-of-work systems. However, network users voluntarily chose to transition to proof-of-stake and stake their ETH, thereby choosing to accept this centralization and potential future censorship. The US government did not force anyone here.

Does anyone really care? No. I am sure Vitalik would argue that there are some safeguards in place to help ensure decentralization—such as the way validators are penalized for censoring transactions. That’s a nice idea, but let’s stress-test it.

After the "upgrade" to proof-of-stake, the game theory behind incentivizing validators to reach consensus becomes trickier. I have had repeated discussions with Jonathan Bier, head of BitMEX Research, about the different penalties that potential bad actors seeking to censor transactions might face, and I quickly realized that the situation is a bit grim. In summary, the penalty system works as follows:

If less than 33% of the network refuses to validate a block, there is a way for you to slowly lose ETH. Slowly losing ETH means that validators will be penalized for reducing the stake on their nodes. If the stake falls below 16 ETH, that validating node will be removed from the network. Since you cannot unstake ETH, that capital will become dead capital.

If more than 33% of the network refuses to validate a block, there is a way to quickly lose ETH. The penalties will worsen exponentially so that dissenting validators will soon fall below the 16 ETH threshold and be kicked out of the network.

Here is a hypothesis test for your ideological commitment—given the above circumstances, if the centralized large nodes of the Ethereum network change the rules to mitigate penalties, would you support them, or would you support the resistance that blindly adheres to the censorship regime?

We saw a similar ideological test in 2016 when "The DAO" locked up a significant portion of all ETH, and almost everyone defaulted to supporting the fork protocol so that people could get their money back instead of being loyal to Ethereum's so-called "code is law" spirit.

This significant violation of Ethereum's "code is law" spirit did not even weaken the fervor of its supporters and had almost no negative impact on the network in the long run. ETH is the token that powers the network and has maintained its position as the second-largest token by market capitalization without much challenge, while Ethereum remains the most widely used blockchain network in existence (with nearly 4 times the daily transaction volume of Bitcoin).

To be fair, there are still many very successful dApps leveraging the network to seek to break the censorship regime in areas like finance. However, as dApps scale up and become significant financial players in the global ecosystem, their success may threaten entrenched interests, and if the network does not highly value censorship resistance or decentralization, these threatened parties will have countless levers to minimize them.

The pseudo-decentralization endured by users of the two most valuable "decentralized" internet computers (BSC and Ethereum) somewhat reflects the ideological sacrifices people currently make daily when using major Web2 platforms. The cost of using these platforms is not high: you either hand your data over to the US (Facebook, Google, Amazon, Microsoft, Apple, etc.) or to China (Tencent, Baidu, Weibo, Alibaba, Huawei, ByteDance, etc.). But even after realizing this grim reality, the vast majority of humanity continues to voluntarily cede their data sovereignty to governments in exchange for entertainment, online socializing, and communication capabilities.

The early investors in US and Chinese Web2 giants have created generational wealth, and the same goes for ETH holders. ETH, as a financial asset—completely tethered to the US-dominated financial system and under the guise of "decentralization"—can still perform very well in the near future. The question I want to address is whether truly decentralized financial and social dApps can exist on a large scale (i.e., with hundreds of millions of users). I do not know the answer to this question, but when it becomes important to the market, I hope to have already used institutional investors as exit liquidity so that I can fully immerse myself in a truly Satoshi world.

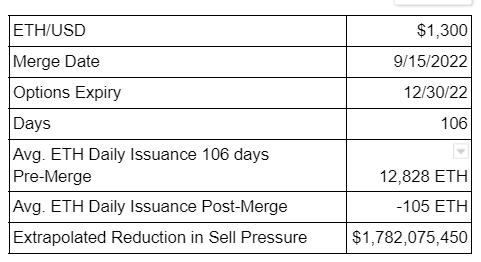

As I have said in various interviews, I believe that in the short term (i.e., the next three to six months), the only thing that matters is how the issuance of ETH per block decreases under the new Proof-of-Stake model. In the days following the merge, the ETH issuance rate averaged a drop from +13,000 ETH per day to -100 ETH.

As dollar liquidity deteriorates, the price of ETH continues to rise, but it takes time for the changes in supply and demand dynamics to permeate. Come back in a few months, and I suspect you will find that the sharp reduction in supply has created a strong and steadily rising floor for prices.

I previously wrote that I bought $3,000 worth of ETH/USD call options with a strike price of December 2022. I worry that I may not have enough time to put money into these options. Take a look at the table below.

Net ETH issuance = ETH issuance - [(average ETH gas usage / 10⁹) * number of ETH transactions].

Is eliminating nearly $2 billion in selling pressure enough to double the price three months later? If my dollar liquidity index rises, then perhaps I have a chance. But hope is not an investment strategy. I may have overestimated the impact of the supply reduction on price increases. Relative to Bitcoin, I believe ETH will continue to perform well. A more convenient trade is to buy ETH/BTC options. But I already have a spot position, and I enjoy trading.

Not Following Institutions

"The bull market can only start when institutions return," is a common viewpoint I have seen recently. The reality is that institutions are beta-chasing puppets who buy at the top and sell at the bottom, driven by their compensation incentives. Institutional fund managers and trustees are rewarded by accumulating large assets and charging management fees.

Many of these hard-working individuals are puppets because that is their compensation. However, when managing their own funds, many recognize the value of crypto assets and flock to them. As a trustee, you care about bonuses. But as the head of a household, you care more about compound returns.

In summary, those predicting that institutional investor funds will lead the next bull market are not talking about these investors' personal portfolios.

In any environment, the primary goal of any organism is survival, and fund managers are no exception. In their working lives, trustees want to survive the year to earn their next bonus. This means they will only buy cryptocurrencies in safe situations. Safety is found when prices have already risen multiple times from the bottom. When the market goes down and they lose investors' money, at least they can argue that they bought in when everyone else was buying.

So if you are waiting for institutional investors to rediscover cryptocurrencies and reignite the next bull market, then you will become a late buyer.

Harsh Correlation

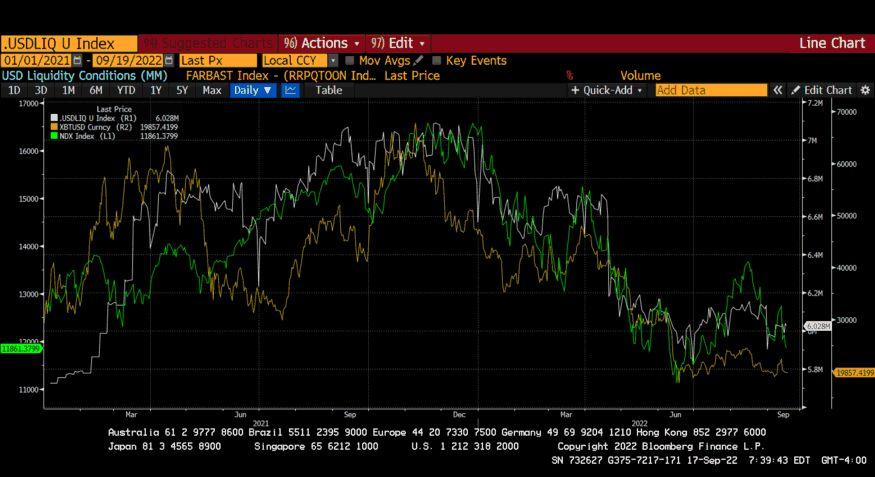

Bitcoin has become a high-energy indicator of dollar liquidity; isn't that sad? The correlation of crypto assets with the Nasdaq 100 index, composed of large US tech companies, isn't that a helpless situation? I thought crypto assets should be the people's money, negatively correlated with the TradFi system.

These are the sentiments of many market analysts immersed in how the TradFi market operates. Many of these analysts fully believe that the Federal Reserve and its central bankers will continue to raise short-term interest rates for the foreseeable future. Given that these actions remove credit from the system, these strategists are bearish on long-term tech stocks and therefore very bearish on the future price of crypto assets.

Bitcoin Price = Dollar Liquidity + Technology

The state of dollar liquidity will do its best, which is the price driver most people are concerned about. However, censorship-resistant technology does not receive enough trust. Until these attributes are proven valuable, it will continue to lack trust.

These technological characteristics cannot be a priori, primarily due to the way we think about the future; we tend to reference the recent past to predict the future. For most humans living in economically developed countries, recent history has been "correct" from a financial services perspective, and fiat currencies and their accompanying financial systems are effective.

As I pointed out in my recent article "For the War," recent history is one of economic peace between two major blocs (the US/EU and Eurasia/Russia/China). If your passport is Russian, your dollars, euros, pounds, etc., are no longer yours. And Russia now only allows fuel purchases in rubles, gold, or currencies of "friendly" countries. The global financial and energy systems are Balkanizing, leading to fierce inflation. In this context, a global currency operated and owned by humans has infinite value. At that time, Bitcoin technology will show its true value and support the right side of the aforementioned value proposition.

Financial analysts completely disregard this part because they are human. You cannot value it until it has value, so in any model, it is assigned a zero value. Therefore, while I completely agree that in the near future, Bitcoin's price will remain aligned with dollar liquidity, I expect that as this economic war intensifies, the value of Bitcoin technology will begin to be recognized.

Incremental

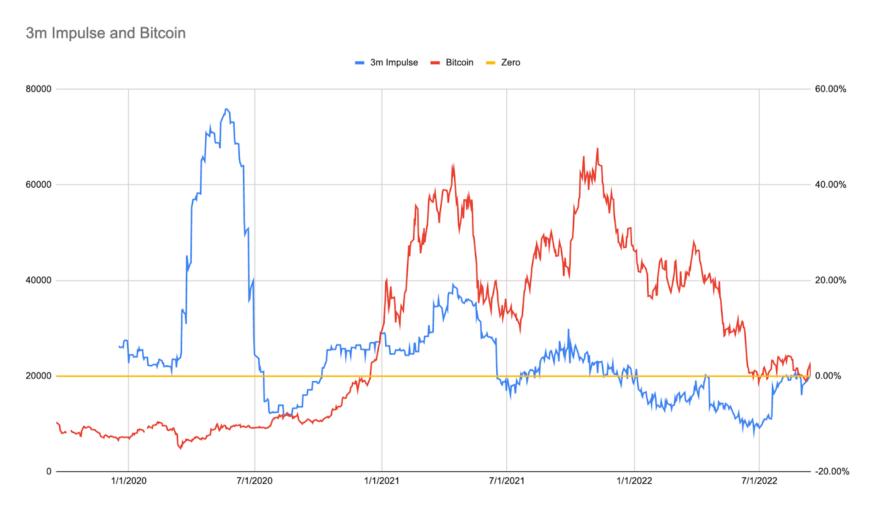

While the dollar liquidity index explains Bitcoin's recent movements well, it has no predictive power. If we want to predict what might happen to Bitcoin's price in the future, we care about the liquidity situation today relative to recent conditions.

As always, forecasting is an art, not a science. Through curve fitting, I made assumptions about time. In this case, I want a less volatile increment but also one that moves quickly to account for Bitcoin's rapidly changing nature. I established a 3-month index. The components of this index are updated weekly (Federal Reserve balance sheet and Treasury total accounts) and updated daily on business days (reverse repo overnight interest and standing repo facility balances). The US typically has 252 trading days in a year, so if I want a 3-month impulse, that is 63 trading days.

Simply put, if the increment is positive, I go long Bitcoin; if the increment is negative, I go short or stay out of Bitcoin.

This simple statement does not benefit traders much. As traders, we care about turning points. In November 2021, the increment was positive—that is, dollar liquidity increased compared to the previous three months—but it was the market's peak. If the increment is rising but the rate of increase is slowing, we want to exit long positions and possibly short. If the impulse is declining but the rate of decline is slowing, we want to exit short positions and possibly go long.

The current situation is turbulent. From November 2021 to July 2022, the state of dollar liquidity tightened significantly. The chart clearly shows a drop of $3 million, along with a corresponding drop in Bitcoin's price. In recent weeks, this impulse has been cut to around 0%.

From the perspective of dollar liquidity, the Federal Reserve is committed to reducing the size of its balance sheet for the remainder of this year, and the US Treasury is issuing a large amount of debt to fund the government. Both actions remove liquidity from the system. This should lead to a decline in the impulse and cause Bitcoin to drop to test its June low of $17,500.

The mitigating factor is that all this liquidity tightening will disrupt financial markets in the US and around the world. A dollar-based, highly leveraged global economy cannot survive at the current level of activity with significantly reduced dollar liquidity. My guess is that there will be some issues with how the US Treasury market operates. The Federal Reserve, the Treasury, US domestic banks, and large foreign holders like Japan and China are all selling bonds. Who will buy all these bonds at yields far below government inflation indicators? If the Federal Reserve and the Treasury want to ensure that the US Treasury market, the most important market in the global financial system, remains intact, they may have to abandon their plans to significantly remove dollars from the system. Politics is a passive activity, so we may have to see the US Treasury market collapse before it changes direction.

There are rumors that the "strengthening the dollar" policy being pursued by the Federal Reserve and the Treasury may be reversed during the G20 showdown in Bali on November 15-16. The EU, as an anti-Russian/Chinese spearhead, cannot survive when they now have to import more liquefied natural gas tankers, strengthening the dollar. This event also takes place after the US midterm elections, so the political will to "combat" inflation may fade faster than TerraUSD.

The Federal Reserve has not changed its quantitative tightening or short-term interest rate policies as I suggested in my previous articles. However, I never said I believed the Federal Reserve would make adjustments before the midterm elections.

As we observe the fluctuations of the dollar liquidity index and its incremental changes, the Bitcoin price that bulls should be concerned about is $17,500. The most likely course of action is to retest that low. Whether this line can hold depends entirely on the trajectory of the dollar liquidity index's increment.

On ETH, we are just a week away from the merge. It seems the network is running smoothly, which is good. The technology is challenging, and it seems congratulations are in order for the Ethereum core developers for completing this incredible feat. As expected, the number of ETH is decreasing by nearly 13,000 each day.

Since I wrote two bullish articles about ETH, the price has capitulated. I still believe that the structural reduction in ETH supply will certainly lead to outperformance relative to Bitcoin—but if the Federal Reserve and the Treasury continue their plans to reduce dollar liquidity, I have no confidence in ETH reaching five figures by the end of the year. What frustrates me is that my December options will be worthless when they expire.

That said, am I lightening my positions in ETH and ERC-20 altcoins in my portfolio? Absolutely not! Because I hold spot, I do not have to worry about time and cost. Clearly, there is an opportunity cost in holding short-term US Treasuries compared to holding fiat, but I have allocated a portion of my overall portfolio to it. I am also long on interest rates through a series of exotic derivatives. In the crypto market, waiting is worthwhile, and I can structurally remain patient.

Risk warning

Risk warning Risk warning

Risk warning