Arthur Hayes: How will the Federal Reserve's future policies affect the path forward for Bitcoin?

Many people believe that the recent steady decline in CPI only means one thing: Powell is ready to ease monetary policy again, like in March 2020. Assuming the market thinks this is the most likely path forward, how can we expect Bitcoin to react?

Many people believe that the recent steady decline in CPI only means one thing: Powell is ready to ease monetary policy again, like in March 2020. Assuming the market thinks this is the most likely path forward, how can we expect Bitcoin to react?Author: Arthur Hayes

Compiled by: GaryMa, Wu Says Blockchain

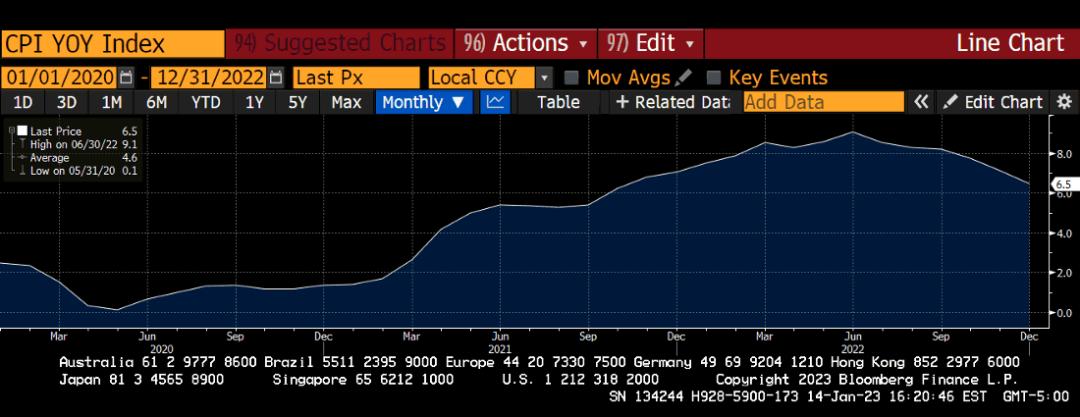

US CPI Year-on-Year Index

From the above chart, it can be seen that the inflation rate measured by the (flawed and misleading) Consumer Price Index (CPI) series released by the U.S. Bureau of Labor Statistics peaked at around 9% in mid-2022 and is now rapidly declining towards the crucial 2% level.

Many believe that the recent steady decline in CPI only means one thing: Powell is ready to ease monetary policy again, just like in March 2020. With the U.S. and possibly the entire world on the brink of recession, those prophets would say that Powell is looking for every opportunity to shift from his current quantitative tightening (QT) policy, which would bear much of the responsibility if we enter an economic downturn. With the decline in CPI, he can now point to the drop and claim that his righteous campaign to slay the inflation beast has succeeded, and he can safely turn the taps back on.

I am not so sure these predictions are correct, but we will have more discussion on that later. For now, let’s assume the market believes this is the most likely path forward; how can we expect Bitcoin to react? To model this accurately, we must remember two important things about Bitcoin.

First, Bitcoin and the broader crypto capital markets are the only markets that are truly not manipulated by central bank presidents and large global financial institutions. You might ask, "But what about the alleged misconduct of bankrupt companies like 3AC, FTX, Genesis, Celsius, etc.?" That is a fair question, but my answer is that as the crypto market prices adjusted, these companies went bankrupt, and the market quickly found a much lower liquidation price at which leverage was eliminated from the system. If similarly reckless behavior occurred in the TradFi system, authorities would try to delay market liquidation by supporting near-bankrupt entities (which they have always done), thereby damaging the economy they are supposed to protect. However, the cryptocurrency space faces severe challenges and quickly cleansed poorly managed, flawed business models, laying the groundwork for a rapid and healthy rebound.

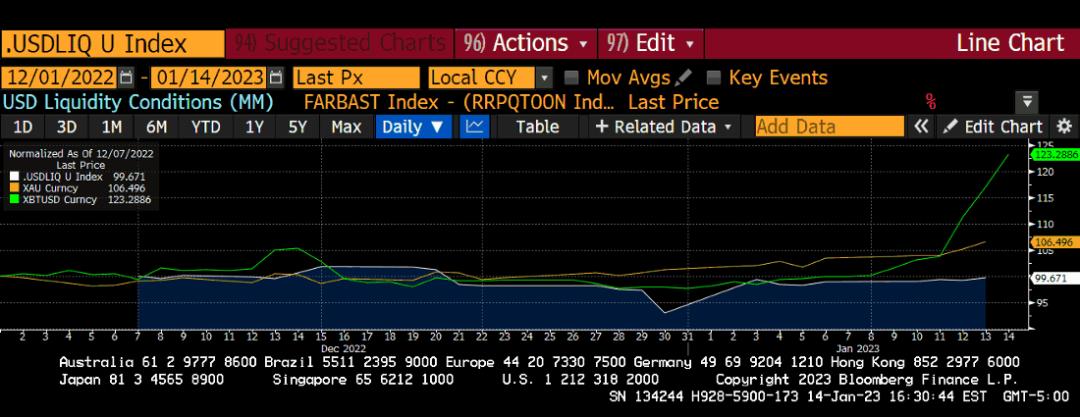

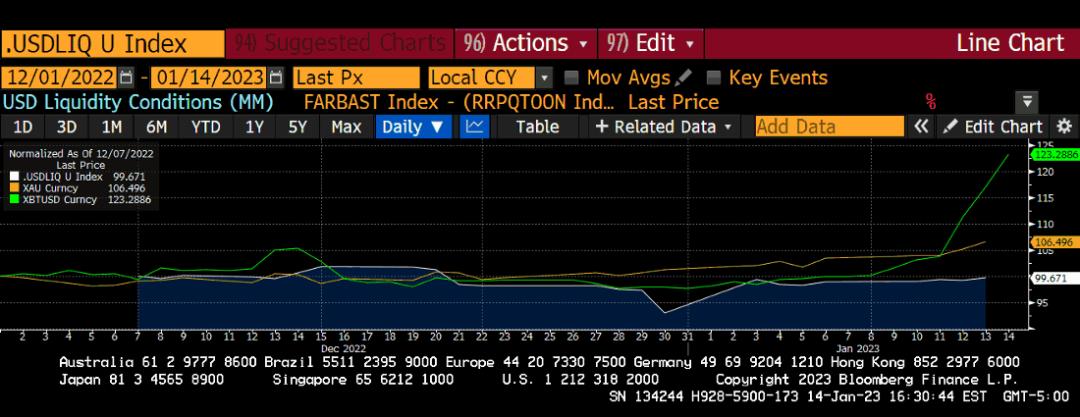

The second thing to remember about Bitcoin is that because it is a response to the profligacy of the global fiat currency system, its price largely depends on the future path of dollar global liquidity (due to the dollar being the global reserve currency). I discussed this concept and my dollar liquidity index in detail in a recent article. To this end, Bitcoin has outperformed the flat dollar liquidity index over the past two months. In my view, this indicates that the market believes the Fed's pivot is imminent.

Gold (yellow), Bitcoin (green), Dollar Liquidity Index (white), Index = 100

Looking at Bitcoin's price action, it is currently starting to rally from a low. From here, we can identify several different potential paths forward based on the actual factors driving the rebound:

Rebound Catalyst Scenario 1: Bitcoin is simply experiencing a natural rebound from a local low below $16,000.

● If this rebound is indeed just a natural bounce from a local low, I expect Bitcoin to subsequently find a new platform and move sideways until the dollar liquidity situation improves.

Rebound Catalyst Scenario 2: Bitcoin's rise is because the market is anticipating the Fed's return to printing money. If that is the case, I think two situations could arise:

● Scenario 2A: If the Fed does not implement a pivot, or if several Fed officials are not optimistic about the pivot expectations after the CPI data is "good," Bitcoin could fall back to previous lows.

● Scenario 2B: If the Fed does indeed implement a pivot, Bitcoin will continue to perform strongly, and this rebound will mark the beginning of a long-term bull market.

Clearly, we all want to believe we are heading towards Scenario 2B. That said, I think we will actually face some combination of Scenario 1 and 2A, which makes my itching "buy" finger a bit hesitant.

While I believe the Fed will pivot, I do not think it will happen solely because CPI is trending down. Powell has stated that he is more focused on the interaction between wage growth (U.S. hourly earnings) and core personal consumption expenditures (core PCE) rather than relying on CPI as a measure of inflation. As a side note, I believe both CPI and core PCE are not good indicators of inflation. Core personal consumption expenditures are particularly hypocritical because they exclude food and energy. The common people do not riot over the price of flat-screen TVs but over the price of bread rising by 100%. But regardless of what I think, what is important for our forecasting work is that Powell has signaled that he intends to base any decisions regarding potential policy pivots not only on CPI but also on the comparison between U.S. wage growth and core personal consumption expenditures.

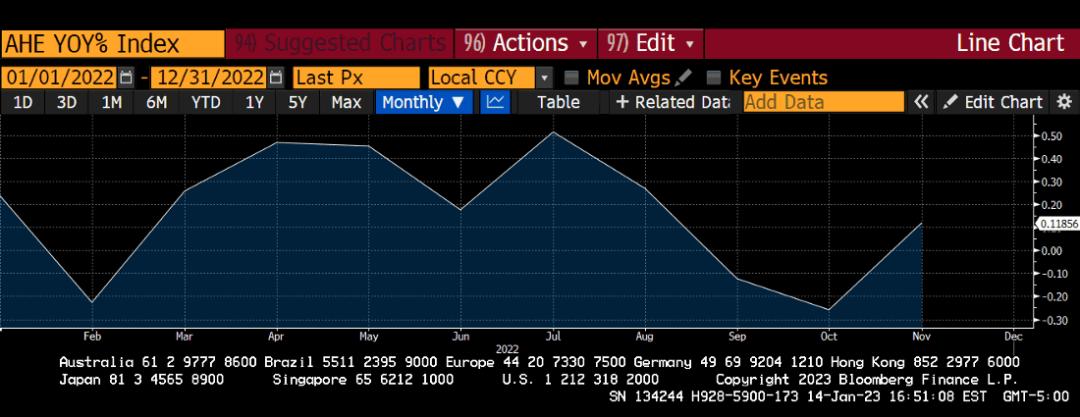

Change in U.S. Hourly Earnings Minus Change in Core PCE, Year-on-Year Percentage Change

From the above chart, it can be seen that the average wage growth in the U.S. is keeping pace with inflation. This means that while goods are becoming more expensive, people's ability to purchase these goods is actually growing at a similar rate due to wage growth. Therefore, the enhancement of purchasing power may further drive goods inflation. In other words, producers may realize that their buyers are now earning more than before and further raise prices to absorb the recent wage growth of buyers, all without worrying about stifling demand for their products. Thus, Powell actually has reason to continue raising interest rates (i.e., suppressing consumer demand to prevent further increases in goods prices). And he is likely to use it, as he has indicated that he is seeking to ensure that yields across the entire U.S. Treasury curve are above the inflation rate (which they currently are not).

U.S. Treasury Yield Curve

Core personal consumption expenditures grew by 4.7% year-on-year in December 2022. From the above curve, it can be seen that currently only the 6-month Treasury bill yields above 4.7%. Therefore, Powell has considerable room to continue raising rates. More importantly, he can continue to reduce the Fed's balance sheet, further tightening the monetary environment to the level he desires.

The significance of these last few charts and some statements is simply to indicate that the continuously declining CPI numbers are meaningless because they are inconsistent with the actual indicators Powell uses to judge whether the Fed has successfully curbed inflation. The decline in CPI may mean something, but I do not think it will meaningfully predict when the Fed will ultimately pivot.

That said, I do believe that if Powell ignores CPI data and continues to shrink the Fed's balance sheet through QT, it will lead to severe turmoil in the credit markets and force them to pivot aggressively.

Since peaking at $8.965 trillion on April 13, 2022, the Fed's balance sheet has decreased by $458 billion as of January 4, 2023. The Fed was supposed to reduce the total balance sheet by $523 billion in 2022, so they have achieved 88% of that goal. The current QT rate indicates that the balance sheet will decrease by another $100 billion per month, resulting in a further $1.2 trillion reduction in the fiscal year 2023. If withdrawing $500 billion in 2022 led to the worst bond and stock performance in centuries, imagine what would happen if double that amount were withdrawn in 2023.

The market's response to the injection and withdrawal of funds is asymmetric. Therefore, I expect the law of unintended consequences to bite the Fed in the ass as it continues to withdraw liquidity. I also believe Powell instinctively understands this because, despite his very aggressive QT, it would take many years at the current pace to fully reverse the amount of money printed since the onset of the pandemic. From mid-March 2020 to mid-April 2022, the Fed printed $4.653 trillion. At a rate of $100 billion per month, it would take about 4 years to fully return to pre-pandemic Fed balance sheet levels.

If the Fed truly wants to reverse monetary growth, it should directly sell MBS and U.S. Treasuries rather than merely stopping the reinvestment of maturing bonds. Powell could speed up the process, but he has not, indicating that he knows the market cannot bear the Fed selling its assets. But I still believe he has overestimated the market's ability to cope with the Fed's continued passive participation. The MBS and Treasury markets need the Fed's liquidity, and if QT continues to grow at the same pace, these markets and all other fixed-income markets that derive valuations and pricing from these benchmarks will soon find themselves in a painful world.

Fed Pivot Scenario Analysis

In my view, two things could prompt the Fed to pivot:

Powell believes that the decline in the CPI index confirms that the Fed has done enough and can pause rate hikes at some point in the near future, potentially stopping QT and cutting rates if a mild recession occurs in the second half of 2023. Monetary policy typically has a lag of 12 to 24 months, so Powell seeing a downward trend in CPI could lead him to believe that inflation will continue to return to the 2% holy grail in the near future based on what has happened over the past year. As I outlined above, I think this scenario is unlikely because I do not believe Powell uses CPI as a measure of inflation, but it is not impossible.

Certain parts of the U.S. credit market collapse, leading to a financial collapse involving a wide range of financial assets. In response similar to March 2020, the Fed holds an emergency press conference, stops QT, significantly cuts rates, and restarts quantitative easing by buying bonds again.

In Scenario 1, I expect risk asset prices to rise slowly. We will not return to the lows of 2022, and it will be a pleasant environment for fund managers. Just sit back and watch the base effects of CPI work their magic, mechanically lowering the overall data. The U.S. economy will find itself in a generally stable position, but nothing very bad will happen. Even if a mild recession occurs, it will not be as severe as what we saw during the March to April 2020 period or the 2008 global financial crisis. This is the preferred scenario because it means you can start buying now before the economy improves and inflation remains low.

In Scenario 2, risk asset prices plummet. As the glue of the dollar-based global financial system dissolves, bonds, stocks, and every cryptocurrency under the sun will be tarnished. Imagine U.S. 10-year Treasury yields doubling from 3.5% to 7%, the S&P 500 dropping below 3000, and the Nasdaq 100 falling below 8000, with Bitcoin trading at $15,000 or lower. Like a deer caught in headlights, I expect Sir Powell to mount his horse and lead the money-printing army to the rescue. This scenario is less than ideal because it means that everyone buying risk assets now will face significant performance declines. 2023 could be just as bad as 2022 before the Fed pivots.

My guess is Scenario 2.

Why is Gold Rising?

Gold (yellow), Bitcoin (green), Dollar Liquidity Index (white), Index = 100

The most reasonable rebuttal to my basic assumption of Scenario 2 is that gold is also rising alongside Bitcoin. Gold is a more liquid and reliable anti-fragile asset, serving a similar purpose as a hedge against the fiat currency system. Therefore, at first glance, you might reasonably speculate that gold's recent rise further proves that the market believes the Fed will adjust its policy in the near future. This is a reasonable inference, but I suspect that gold's rise is entirely due to another reason. Therefore, it is important not to conflate the rise of gold and Bitcoin as a joint confirmation of the Fed's impending pivot. Let me explain.

Gold is a sovereign currency because, at the end of the day, nation-states can always settle trade in goods and energy with gold. This is why every central bank has a certain amount of gold on its balance sheet.

Since every central bank holds a certain amount of gold, when a country's currency must depreciate to maintain global competitiveness, central banks always resort to devaluing gold. A recent example is the U.S. devaluing the dollar against gold in 1933 and 1971. This is why I have allocated a significant amount of physical gold and gold miners in my portfolio. Investing alongside central banks is always better than going against them.

I (and many others) have written extensively about how the world will accelerate its de-dollarization in the coming years following several key geopolitical events (such as the U.S. freezing "assets" held by Russia in the Western financial system). I expect that producers of cheap labor and natural resources around the world will eventually realize that if they anger the U.S. government, they may face the same fate as Russia, making it pointless to store wealth in U.S. Treasuries. This makes gold the most obvious and attractive investment destination.

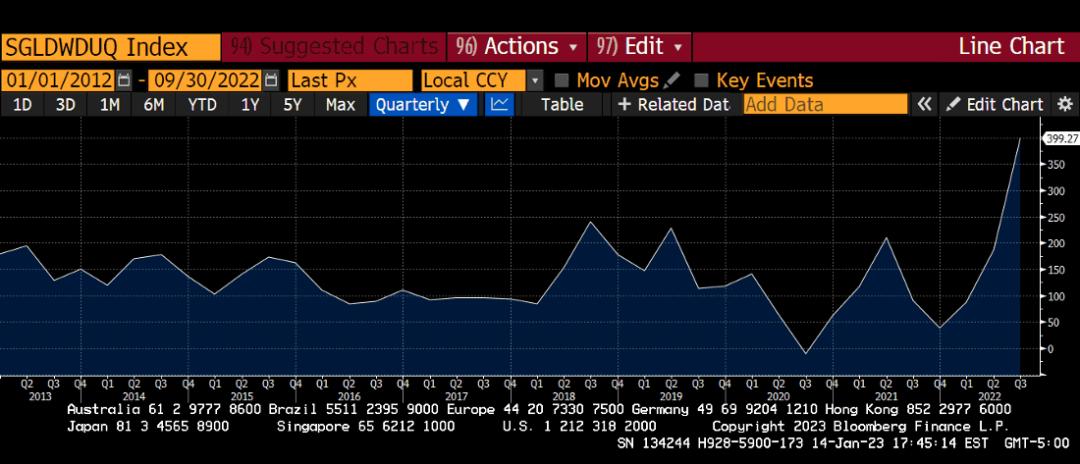

These data support the view that governments are turning to the historically established sovereign reserve currency, gold, to store wealth. The following chart traces back ten years and depicts the net purchases of gold by central banks. As you can see, we set a historical high in the third quarter of 2022.

Net Purchases of Gold by Central Banks (Metric Tons)

The peak of cheap energy has arrived, and many heads of state are aware of this. They instinctively know, like most people, that gold has better purchasing power in terms of energy (crude oil) than currencies like the dollar.

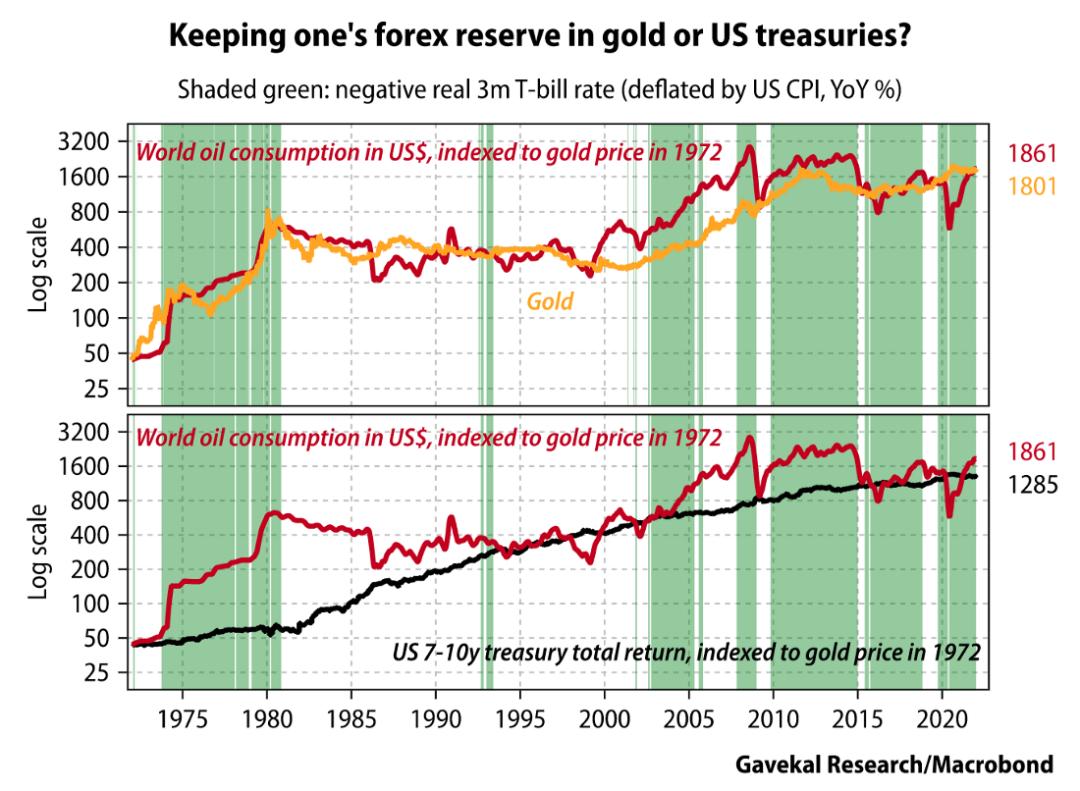

This excellent chart from Gavekal Research clearly shows that gold is a better store of energy than U.S. Treasuries.

In my view, this data indicates that the rise in gold prices is more due to real physical demand rather than because central banks around the world believe the Fed will pivot. Of course, at least part of it is due to expectations that the Fed's monetary policy may ease in the near future, but I do not believe these expectations are the driving force behind it.

Trading Preparation

What if I am wrong, and Scenario 1 of good economy and low inflation occurs?

That means I have missed the opportunity to rebound from the bottom, and Bitcoin is unlikely to turn back as it relentlessly moves towards historical highs. If this is true, rate hikes may occur in two phases. In the first phase, savvy speculators will get ahead of the actual shift in Fed policy. During this phase, Bitcoin could easily trade between $30,000 and $40,000, as the current price is severely depressed by the bearish sentiment following FTX. The next phase would take us to $69,000 or higher, but it can only begin after a significant injection of dollars into the crypto capital markets. Such an injection would require at least a pause in rate hikes and QT.

If I am wrong, I would be happy to miss the initial opportunity to rebound from the bottom. I am already long, so I will benefit regardless. However, the dollars I hold in the form of short-term Treasury bills would suddenly perform poorly, and I would need to reallocate those funds into Bitcoin to maximize my investment returns. However, before I give up the bonds I bought at a 5% yield, I want to have a high degree of confidence that the bull market has returned. 5% is clearly below the inflation rate, but it is better than a 20% drop because I mis-timed the market and bought risk assets too early in the next cycle.

When they really decide to pivot, the Fed will clearly communicate in advance that they will abandon tightening monetary policy. The Fed told us at the end of 2021 that they would pivot to combat inflation by restricting the money supply and raising rates. They stuck to it and began doing so in March 2022, and anyone who did not believe them was slaughtered. Therefore, the same thing is likely to happen in the other direction, meaning the Fed will tell us when to stop, and if you do not believe them, you will miss the subsequent surge.

Since the Fed has not yet signaled a pivot, I can wait. I believe the first priority is to preserve capital, and the second is to grow. I would rather buy into a market that has already rebounded 100%+ from the lows after the Fed communicates a pivot than buy into a market that has rebounded 100%+ from the lows without a pivot and then suffers a 50%+ correction due to poor macro fundamentals.

If I am right and the catastrophic Scenario 2 occurs (i.e., a global financial collapse), then I will have another opportunity to buy the dip. I will know the market may have bottomed because the collapse that occurs when the system temporarily fails will either hold the previous low of $15,800 or it will not. What level it ultimately reaches downward does not matter because I know the Fed will subsequently act to print money to avoid another financial collapse, which in turn will mark the bottom for all risk assets. Then I will get another scenario similar to March 2020, ramping up my purchases of cryptocurrencies.

Risk warning

Risk warning Risk warning

Risk warning