Does cryptocurrency, regarded as legal property, involve tax issues?

Although the existing tax laws do not have specific regulations regarding cryptocurrencies, strictly speaking, the transfer of cryptocurrencies involves tax issues.

Although the existing tax laws do not have specific regulations regarding cryptocurrencies, strictly speaking, the transfer of cryptocurrencies involves tax issues.Original Title: "Do Cryptocurrencies as Legal Property Need to be Taxed in Mainland China?"

Written by: TaxDAO

On September 1, the People's Court Daily published an article titled "Identification of the Property Attributes of Virtual Currency and Issues Related to the Disposal of Involved Assets," which analyzes the criminal law attributes of virtual currencies such as Bitcoin. It concludes that Bitcoin and other virtual currencies have economic attributes and can be classified as property. Current regulations clearly define Bitcoin and other virtual currencies as virtual goods, and administrative legal policies do not comprehensively prohibit virtual currency transactions. Under the existing legal and policy framework, virtual currencies held by relevant entities in China still constitute legal property and are protected by law.

Do individuals need to pay taxes on the gains from transferring cryptocurrencies?

Regarding the tax issues of virtual currencies such as Bitcoin, major countries or regions internationally have issued relevant tax regulations that stipulate tax matters related to the holding and transfer of Bitcoin and other virtual currencies. For example, U.S. tax law stipulates that individuals must pay personal income tax on the capital gains from transferring Bitcoin, with tax rates varying based on the holding period. In Japan, individuals are taxed on the income from transferring Bitcoin and other virtual currencies as miscellaneous income.

In China, on one hand, current policies classify activities related to virtual currencies as illegal financial activities, posing legal risks for any legal entities, non-legal entities, and individuals participating in virtual currency investment and trading activities. On the other hand, there are currently no specific regulations regarding the tax implications of gains from transferring Bitcoin and other virtual currencies. This has led to many misunderstandings among practitioners, who believe that gains from transferring Bitcoin do not involve tax issues and do not require tax payment.

However, first, current regulations in China do not prohibit individuals from holding Bitcoin and other cryptocurrencies. As stated in the article published by the People's Court Daily at the beginning of this text, according to the existing legal framework, virtual currencies held by individuals are considered legal property and are protected by law. Secondly, the absence of specific regulations regarding Bitcoin and other virtual currencies in current tax law does not imply that gains from transferring Bitcoin do not involve tax. On the contrary, existing tax laws in China already address the tax implications of gains from transferring Bitcoin and other cryptocurrencies.

How does the tax bureau obtain information on individuals' cryptocurrency transfers?

Currently, the tax bureau in mainland China may obtain information on individuals' cryptocurrency transfers through centralized cryptocurrency exchanges and service providers, information exchanged through CRS, information provided by on-chain transaction tracking technology teams, and information from public security departments.

What tax items may be involved when individuals transfer cryptocurrencies?

According to current tax law in China, income generated from individuals transferring Bitcoin and other virtual currencies may involve the payment of personal income tax.

Currently, existing regulations in China define Bitcoin and other virtual currencies as specific virtual goods, and virtual currencies held by individuals are considered personal property. When gains from transfers occur, they are subject to personal income tax and should be calculated and paid according to the property transfer income category.

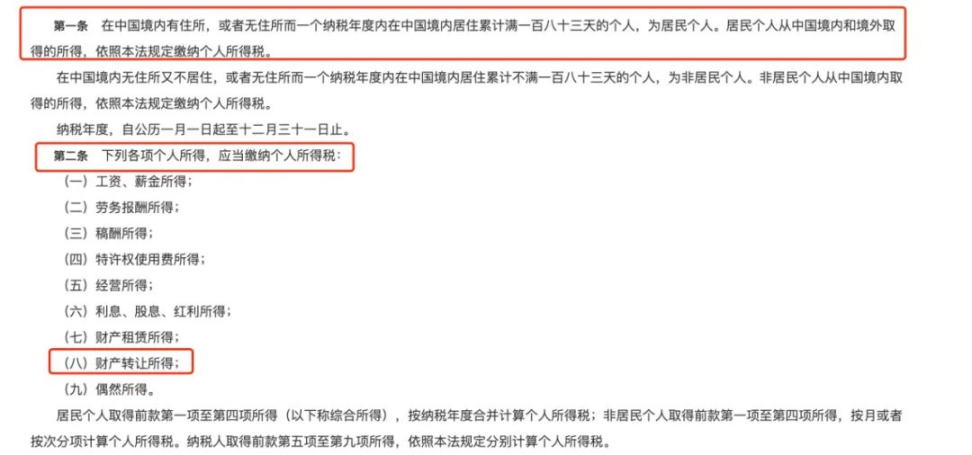

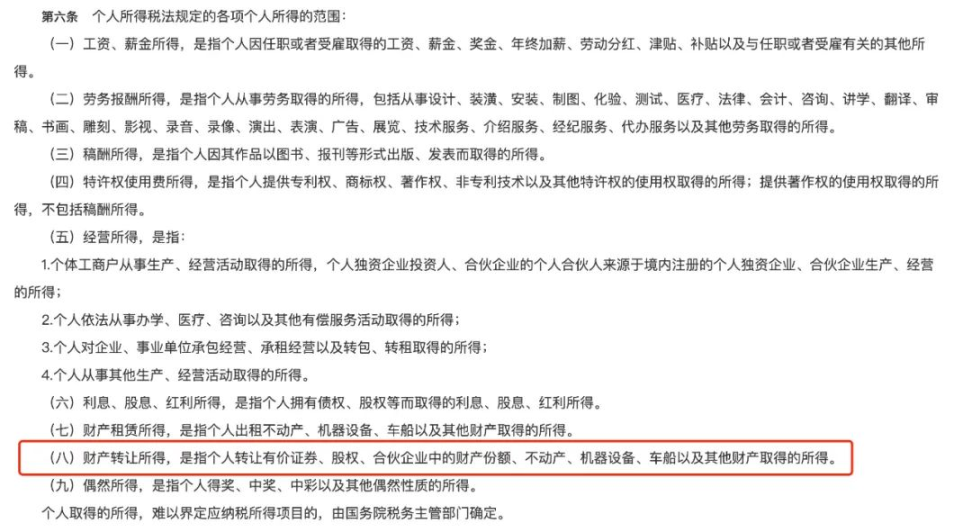

According to the "Individual Income Tax Law of the People's Republic of China," "Article 1: Residents' personal income obtained from within and outside China shall pay individual income tax in accordance with this law," and "Article 2: The following personal income items shall pay individual income tax: …; (8) income from property transfers," and the "Implementation Regulations of the Individual Income Tax Law of the People's Republic of China," "Article 6: The scope of personal income as stipulated in the Individual Income Tax Law includes: …; (8) income from property transfers refers to income obtained by individuals from transferring valuable securities, equity, shares in partnerships, real estate, machinery and equipment, vehicles, and other properties."

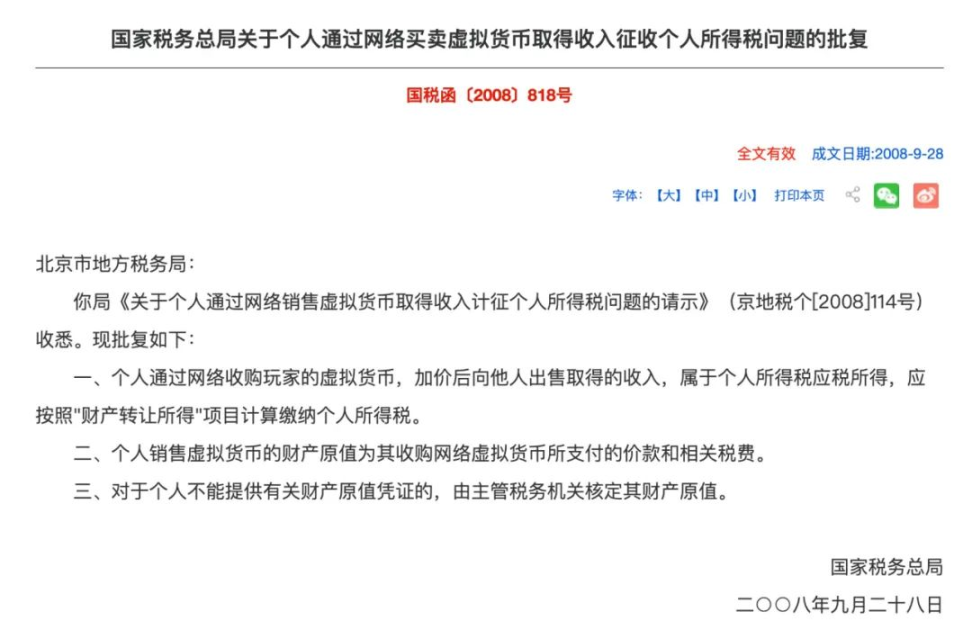

Previously, the State Administration of Taxation had issued a special reply regarding the collection of personal income tax on virtual currency transactions. According to the provisions of the State Tax Letter [2008] No. 818: Income obtained by individuals through the online purchase of virtual currency from players and reselling it at a markup is considered taxable income for personal income tax and should be calculated and paid under the "property transfer income" category.

Although this regulation primarily targets virtual currencies such as game coins and Q coins, which are different from blockchain-based virtual currencies like Bitcoin, under existing Chinese law, both types of virtual currencies are essentially classified as virtual goods. Therefore, this regulation has certain reference value for the personal income tax implications of transferring Bitcoin and other virtual currencies.

What happens if taxes are not paid on gains from cryptocurrency transfers?

Taxes owed should be paid at the time the income is received. If taxes are not declared and paid on time, when the tax bureau conducts an audit, not only will the owed taxes need to be repaid, but also late fees at a daily rate of 0.05% and related penalties will apply. Engaging in tax evasion may also involve corresponding criminal liability. The costs of addressing these issues afterward can be extremely high.

How should individuals consider tax matters when they have gains from transferring cryptocurrency?

If individuals have gains from transferring cryptocurrency, they can consider tax matters from the perspective of their personal tax residency status, potential tax types, tax amounts, and available tax incentives.

However, tax-related regulations are quite complex, and the tax matters themselves are quite specialized. Additionally, the calculation of gains from transferring Bitcoin and other cryptocurrencies is complicated, making tax matters related to cryptocurrency transfers even more complex and uncertain. Therefore, if individuals are involved in gains from transferring Bitcoin and other cryptocurrencies, it is advisable to communicate in advance with tax professionals or institutions to understand whether relevant tax matters are involved, and if so, how to declare and pay taxes in practice, and to plan ahead. This can help avoid unnecessary tax risks or costs due to failure to declare taxes in a timely manner or creating tax obligations in multiple locations, leading to delayed tax payments or the need to pay taxes multiple times.

Risk warning

Risk warning Risk warning

Risk warning