RWA in the Eyes of the Federal Reserve: Tokenization and Financial Stability

This article aims to provide a background on asset tokenization and discuss the potential benefits as well as the risks to financial stability.

This article aims to provide a background on asset tokenization and discuss the potential benefits as well as the risks to financial stability.Author: Will 阿望, Web3 小律

In a working paper on tokenization published by the Federal Reserve on September 8, it stated that tokenization is a new and rapidly growing financial innovation in the crypto market, analyzed from the perspectives of scale, advantages, and risks. It first introduces the concept of tokenization, which refers to the process of creating a digital representation (crypto tokens) for non-crypto assets (underlying assets). In this process, tokenization establishes a link between the crypto asset ecosystem and the traditional financial system. When sufficiently scaled, tokenized assets may transfer the risk of extreme volatility from the crypto market to the underlying asset market of traditional finance.

The following is a compilation of this 29-page paper to help everyone further understand RWA and tokenization, underlying assets and crypto assets, regulation and financial stability. Borrowing a phrase from the principal: "Any financial technology comes with inherent risks, and the deep integration of regulatory technology with RWA and DeFi will be an important focus area for the development and iteration of crypto technology in the future."

This is another RWA research report following previous compilations of Binance (Tokenization of Real World Assets RWA, Bridging TradFi and DeFi), Citigroup (The Next Billion Users and Trillion Dollar Value of Blockchain, Money, Tokens, and Games), and our own RWA Research Report: In-depth Analysis of Current RWA Implementation Paths and Future RWA-Fi Prospects. Below, enjoy:

1. What is Tokenization

"Tokenization" refers to the process of linking the value of underlying assets (Reference Assets) with the value of crypto tokens. Strictly speaking, tokenization allows token holders to have legal rights to dispose of the underlying assets. So far, most tokenization projects in the market have been initiated by small VC-backed crypto companies, while traditional financial institutions such as Santander Bank, Franklin Templeton, and JPMorgan have also announced their tokenization pilot projects related to crypto assets.

Like stablecoins, tokenization can have different characteristics due to varying design schemes. Generally, tokenization typically includes the following five features: (1) based on blockchain; (2) ownership of underlying assets; (3) a mechanism to capture the value of underlying assets; (4) a method for storing/custody of assets; (5) a redemption mechanism for tokens/underlying assets. Overall, tokenization connects the crypto market with the market of underlying assets, and the design of tokenization schemes will differentiate various tokens and impact traditional financial markets to varying degrees.

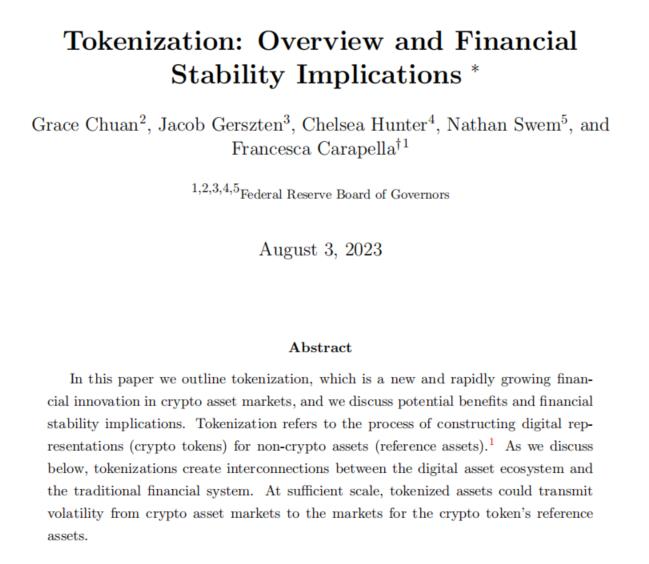

The first factor to consider in the design of tokenization schemes is the underlying blockchain, which is used for the issuance, storage, and trading of tokens. Some projects issue tokens on permissioned private blockchains, while others issue on permissionless public blockchains. Permissioned blockchains are typically controlled by a centralized entity that approves selected participants to enter a private ecosystem. In contrast, issuing tokens on permissionless blockchains (such as Bitcoin, Ethereum, Solana, etc.) allows for broader public participation with fewer restrictions, but the issuer has less control over the tokens. Tokens on permissionless blockchains can also be integrated into decentralized finance (DeFi) protocols, such as decentralized exchanges. Examples of project tokens issued on permissioned and permissionless blockchains can be seen in Figure 1.

Another consideration is the underlying assets of the tokens. Underlying assets can be classified into various categories, such as on-chain assets and off-chain assets, intangible assets and tangible assets, etc. Off-chain underlying assets are independent of the crypto market and can be tangible (such as real estate and commodities) or intangible (such as intellectual property and traditional financial securities). The tokenization of off-chain/underlying assets typically involves an off-chain agency, such as a bank, to assess the value of the underlying assets and provide custody services. The tokenization of on-chain/crypto assets requires the inclusion of smart contracts to provide custody and asset assessment for the crypto assets.

The final factor to consider is the redemption mechanism. Similar to some stablecoins, issuers allow token holders to redeem their tokens for the underlying assets. This redemption mechanism connects the crypto market with the underlying asset market. Additionally, tokenized assets can also be traded in secondary markets, such as centralized crypto exchanges and DeFi exchanges. While some security tokens involving other on-chain debts or shares do not include a redemption mechanism, they still grant token holders some other rights, such as cash flow disposal rights related to their underlying assets.

2. Current Market Size of Tokenization and Categories of Tokenized Assets

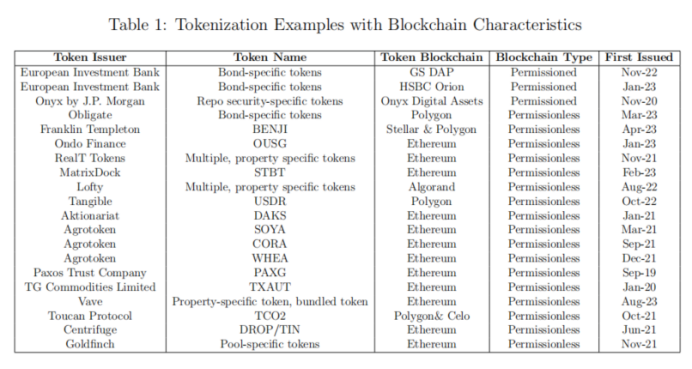

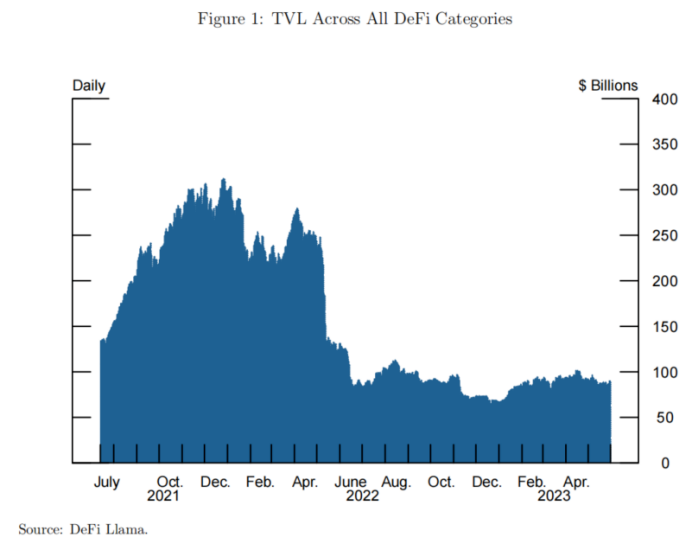

According to publicly available information, we estimate that as of May 2023, the market size of tokenization on permissionless blockchains is $2.15 billion. These assets are typically issued by DeFi protocols like Centrifuge and traditional financial companies like Paxos. Due to the differences in tokenization schemes, there is no unified standard, making it difficult to obtain a comprehensive set of data. Therefore, we will use the publicly available data from the DeFiLlama platform to demonstrate the robust development of tokenization in DeFi. As shown in Table 1, since June 2022, the total value locked (TVL) in the entire DeFi market has remained relatively stable, while Table 2 shows that since July 2021, the TVL of the real-world assets (RWA) asset class has been continuously growing compared to similar assets or the entire DeFi market. Many new tokenization projects have been recently announced, encompassing various categories of underlying assets, such as agricultural products, gold, precious metals, real estate, and other financial assets.

A recent typical tokenization project involves agricultural products SOYA, CORA, and WHEA, which reference soybeans, corn, and wheat, respectively. This project was a pilot program initiated by Santander Bank and crypto company Agrotoken in Argentina in March 2022. By embedding the right of recourse for the underlying assets in the tokens and building the infrastructure to verify and process transactions and redemptions, Santander Bank can accept these tokens as collateral for loans. Santander Bank and Agrotoken have expressed their intention to promote commodity tokenization schemes in larger markets, such as Brazil and the United States, in the future.

Another category of tokenized underlying assets includes gold and real estate. As of May 2023, the market size of tokenized gold is approximately $1 billion. Two types of tokenized gold account for 99% of the market share, namely Pax Gold (PAXG) issued by Paxos Trust Company and Tether Gold (XAUt) issued by TG Commodities Limited. Both issuers set one token unit equivalent to one ounce of gold, stored according to standards set by the London Bullion Market Association (LBMA). PAXG can be redeemed for an equivalent amount of USD, while XAUt can be redeemed through the issuer by selling on the Swiss gold market. Overall, the two models are fundamentally similar, with values corresponding to gold futures.

Compared to commodities like agricultural products and gold, real estate as an underlying asset faces challenges such as difficulty in standardization, weak liquidity, difficulty in valuation, and more complex legal and tax issues. These pose significant challenges to real estate tokenization. Real Token Inc. (RealT) is a real estate tokenization project that collects residential properties and tokenizes their equity. Each property is independently held by a limited liability company (LLC), and the property itself is not tokenized; rather, the shares of the LLC are tokenized, allowing different investors to co-own each property. This project primarily provides international investors with a way to invest in U.S. real estate, with rental income as a return. As of September 2022, RealT has tokenized 970 properties, with a total value of $52 million.

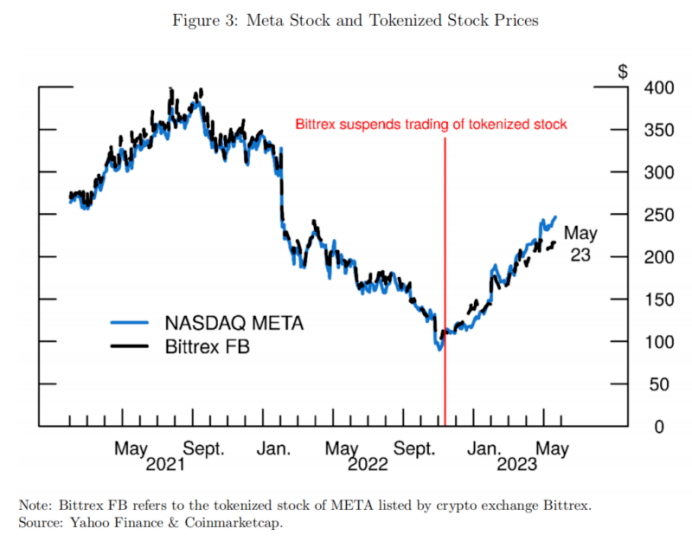

The tokenization of financial assets involves underlying assets such as securities, bonds, and ETFs. Unlike directly holding securities, the price of tokenized securities may differ from the price of the securities themselves, partly because tokens can be traded 24/7, and partly due to the programmability of tokens and their composability with DeFi, which can provide different liquidity for the tokens. We illustrate the differences in prices and trading volumes of META securities and MEAT corresponding to security tokens (based on Bittrex FB) through Tables 3 and 4.

Tokenization can occur on traditional compliant exchanges or directly issue tokens on the blockchain. Akionariat, based in Switzerland, provides tokenization services for Swiss companies. U.S. publicly traded companies like Amazon (AMZN), Tesla (TSLA), and Apple (AAPL) currently or previously have tokenized securities traded on Bittrex and FTX.

Earlier in 2023, Ondo Finance issued tokenized funds, with the underlying assets being ETFs of U.S. Treasuries and corporate bonds. The shares of these tokenized funds represent shares in their corresponding ETFs. Additionally, Ondo Finance holds a small portion of stablecoins as liquidity reserves. Ondo Finance acts as the manager of the tokenized funds, Clear Street serves as the broker and custodian for the funds, and Coinbase acts as the custodian for the stablecoins.

3. Potential Benefits of Tokenization

Tokenization can bring numerous benefits, including allowing investors to enter markets that were previously difficult to access due to high investment thresholds. For example, tokenized real estate can allow investors to purchase a small share of a specific commercial building or residence, which differs from real estate investment trusts (REITs) that invest in a portfolio of properties.

The programmability of tokens and the ability to utilize smart contracts allow for additional functionalities to be embedded in the tokens, which may also benefit the market for underlying assets. For instance, liquidity saving mechanisms can be applied during the token settlement process, which are difficult to implement in the real world. These characteristics of blockchain may lower the entry barriers for a wide range of investors, making the market more competitive and liquid, as well as improving price discovery.

Tokenization may also facilitate lending by using tokens as collateral, as discussed in the case of tokenized agricultural products, where directly using agricultural products as collateral can be costly or difficult to implement. Furthermore, the settlement of tokenized assets is generally more convenient compared to real-world underlying assets or financial assets. Traditional securities settlement systems, such as Fedwire Securities Services and the Depository Trust and Clearing Corporation (DTCC), typically settle transactions on a gross or net basis over the entire settlement cycle, usually one business day after the transaction.

ETFs are the financial instruments most similar to tokenized assets, and existing empirical evidence may suggest that tokenization can also improve the liquidity of underlying asset markets. Academic literature on ETFs demonstrates a strong positive correlation between ETF liquidity and the liquidity of underlying assets, finding that additional trading activity in ETFs leads to higher information exchange/liquidity of the underlying assets. For tokens, a mechanism similar to that of ETFs means that greater liquidity of tokens in the crypto market may be more beneficial for the price discovery of underlying assets.

4. Impact of Tokenization on Financial Stability

The market size of tokenization below one billion dollars is relatively small compared to the entire crypto market or traditional financial market, and does not pose an overall financial stability issue. However, if the tokenization market continues to grow in quantity and scale, it may pose financial stability risks to both the crypto market and the traditional financial system.

In the long term, the redemption mechanisms established between the crypto asset ecosystem and the traditional financial system involved in tokenization may have potential implications for financial stability. For example, at sufficient scale, an emergency sell-off of tokenized assets may impact traditional financial markets, as price discrepancies in the crypto market provide market participants with opportunities to redeem tokenized assets for underlying assets to arbitrage. Therefore, a mechanism may be needed to address the value transmission between the two markets mentioned above.

Additionally, the lack of liquidity in underlying assets may pose problems for tokenized assets. Examples may include real estate or other illiquid underlying assets. This issue has also been discussed in the academic literature on ETFs, where there is a strong correlation between the liquidity, price discovery, and volatility of underlying assets in ETFs.

Another financial stability risk is the issuers of tokenized assets themselves. Tokenized assets with redemption options may encounter similar issues to those faced by asset-backed stablecoins, such as Tether. Any uncertainty regarding the underlying assets (especially a lack of disclosure and information asymmetry regarding the issuer) may increase investors' incentives to redeem underlying assets, leading to sell-offs of tokenized assets.

This liquidity transmission may also be exacerbated by the characteristics of the crypto market. Crypto exchanges allow crypto assets to be traded continuously 24/7, while most underlying asset markets are only open during business hours. The mismatch in trading hours may have unpredictable effects on investors or institutions in special circumstances.

For example, issuers of tokenized assets with redemption options may face sell-offs of tokens over the weekend, as the underlying assets are held off-chain and traditional markets are closed for trading on weekends, preventing redeeming parties from quickly obtaining the underlying assets. This situation may further deteriorate, as the decline in the value of tokenized assets may threaten the solvency of institutions holding significant portions of these assets on their balance sheets. Furthermore, even if institutions can obtain liquidity from traditional markets, they may find it difficult to inject liquidity during the closure of traditional markets.

Therefore, a large-scale sell-off of tokenized assets may rapidly reduce the market value of institutions holding these assets and issuers, affecting their borrowing capacity and, consequently, their ability to repay debts. Another example may relate to the automatic margin call mechanisms of DeFi exchanges, which trigger liquidation or redemption requirements for tokens, potentially having unpredictable effects on the underlying asset market.

As tokenization technology and the market for tokenized assets develop, tokenized assets themselves may become underlying assets. Given that the prices of crypto assets are more volatile than those of similar underlying assets in the real world, the price fluctuations of such tokenized assets may transmit to traditional financial markets.

As the market size of tokenized assets continues to expand, traditional financial institutions may participate in various ways, either by directly holding tokenized assets or by holding tokenized assets as collateral. Examples in this regard may include Santander Bank providing loans to farmers using tokenized agricultural products as collateral. As mentioned earlier, we have also seen cases like Ondo Finance tokenizing U.S. government money market funds.

Moreover, although it is essentially similar to JPMorgan's initial use of money market fund (MMF) equity as collateral for repurchase and securities lending transactions, Ondo Finance's initiative may have more far-reaching implications for traditional financial markets. Ondo Finance's tokens are deployed on the public blockchain Ethereum, rather than on the institution's own private permissioned blockchain, meaning Ondo Finance cannot control how users and DeFi protocols interact. As of May 2023, Ondo Finance's tokenized funds account for 32% of the entire tokenized asset market. According to DeFiLlama, Ondo Finance is the largest tokenized project in this category, and its token OUSG can also be used as collateral for the lending protocol Flux Finance.

Finally, similar to the role of asset securitization, tokenization may package higher-risk or illiquid underlying assets into safe and easily tradable assets, potentially bringing higher leverage and risk-taking. Once risks are exposed, these assets could trigger systemic events.

5. Conclusion

This article aims to provide a background on asset tokenization and discuss the potential benefits and financial stability risks it may bring. Currently, the scale of asset tokenization is very small, but tokenization projects involving various types of underlying assets are being developed, indicating that asset tokenization may occupy a larger portion of the crypto ecosystem in the future. Among the benefits that tokenization may bring, the most prominent is the reduction of barriers to entry into markets that were previously inaccessible and the improvement of liquidity in such markets. The financial stability risks brought about by asset tokenization mainly manifest in the interconnections created between tokenized assets in the crypto ecosystem and the traditional financial system, which may transmit risks from one financial system to another.

Risk warning

Risk warning Risk warning

Risk warning

Popular articles