Besides BlackRock, what other financial giants have made moves?

Established financial institutions are actively investing in deposit tokens. Will asset tokenization trigger the next bull market?

Established financial institutions are actively investing in deposit tokens. Will asset tokenization trigger the next bull market?Author: Wang Jun, Founding Partner of Inpower

Recently, BlackRock's Bitcoin spot ETF has been receiving continuous attention from the market, and I happen to be preparing content on mainstream institutions participating in asset tokenization, so let's ride the wave~

There have already been various articles about BlackRock's Bitcoin spot ETF, so I won't repeat them here~

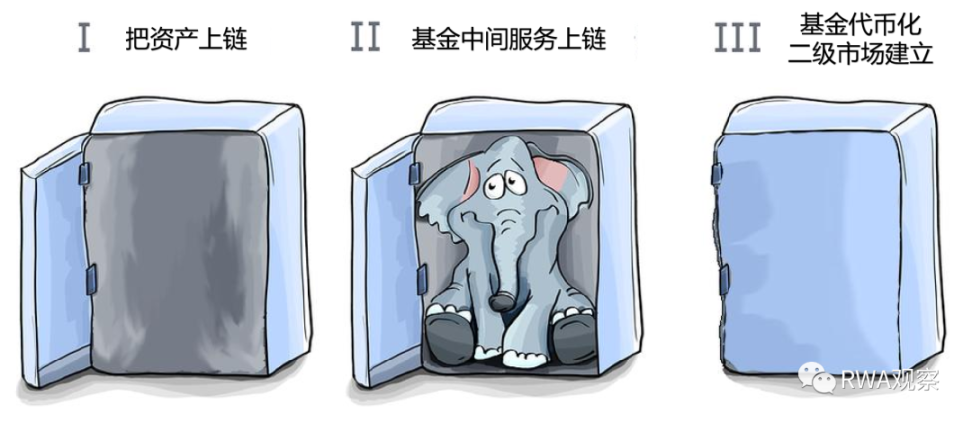

In a previous article, How many steps are needed to tokenize a fund?, I mentioned that it might involve these three steps:

- Incorporating on-chain assets under traditional fund structures

- On-chain service processes for funds

- Establishing a secondary market for fund tokenization

As a native on-chain asset, Bitcoin may pave the way for other on-chain assets (cryptocurrencies) to enter the traditional financial market after the registration of Bitcoin spot ETFs is approved.

As a giant with asset management scale reaching $10 trillion (yes, ten times the global crypto market cap), BlackRock's CEO Larry Fink publicly stated as early as last year: "The next generation of markets, the next generation of securities, is tokenized securities."

In fact, traditional finance has long been laying the groundwork for asset tokenization, which will provide a large amount of assets and funds for future markets.

01 Established Financial Institutions are Actively Developing Deposit Tokens

J.P. Morgan: We are the first on-chain service institution

J.P. Morgan started experimenting with blockchain technology internally as early as 2015, creating an asset management platform called Onyx. By now, the asset trading volume they have handled should be around $1 trillion, and even Goldman Sachs is one of their clients.

J.P. Morgan also issued a coin called JMP Coin, which is an internal deposit token based on deposits. It is expected that all banks will reference this solution in the future. However, deposit tokens still face some regulatory hurdles, so they have not been officially issued to the public yet.

Last year, J.P. Morgan also applied for a trademark for "J.P. Morgan Wallet," making it a model for the traditional financial industry.

Citigroup: Our token service is here

In mid-September this year, Citigroup launched its own token service, allowing clients to convert deposits into digital tokens (still deposit tokens).

Like J.P. Morgan, Citigroup is currently only targeting internal institutional clients, primarily addressing longstanding issues such as cross-border payments and automated trade.

Citigroup's solution may delve deeper into industry applications, partnering with international shipping giant Maersk to primarily solve their canal toll payment issues.

International shipping is quite different from paying tolls on highways; international payments may take days to settle. The tokenization solution can save a lot of time, and costs that previously required bank guarantees and letters of credit can also be eliminated.

UBS: We have created a tokenized money market fund

Just at the beginning of October this year, UBS Asset Management launched a simulated application: a tokenized money market fund based on Ethereum.

Internet users are very familiar with money market funds; the underlying product that ignited internet finance, Yu'ebao, was actually a money market fund provided by Tianhong Asset Management.

This application is directly led by UBS's tokenization platform, completing compliance under the framework in Singapore.

The token for the money market fund is roughly equivalent to a deposit token.

Various Banks: If CBDCs don't come out soon, we'll create our own deposit tokens

If the CBDCs from various sovereign institutions are delayed, traditional institutions' deposit tokens may indeed serve the role of CBDCs.

After all, in the real world, your deposits are actually recorded as money on the books of various commercial banks, not central bank M1.

Financial institution leader J.P. Morgan has calculated that the benefits of CBDCs, such as reducing settlement fees and time / lowering counterparty trading risks, can also be achieved through deposit tokens.

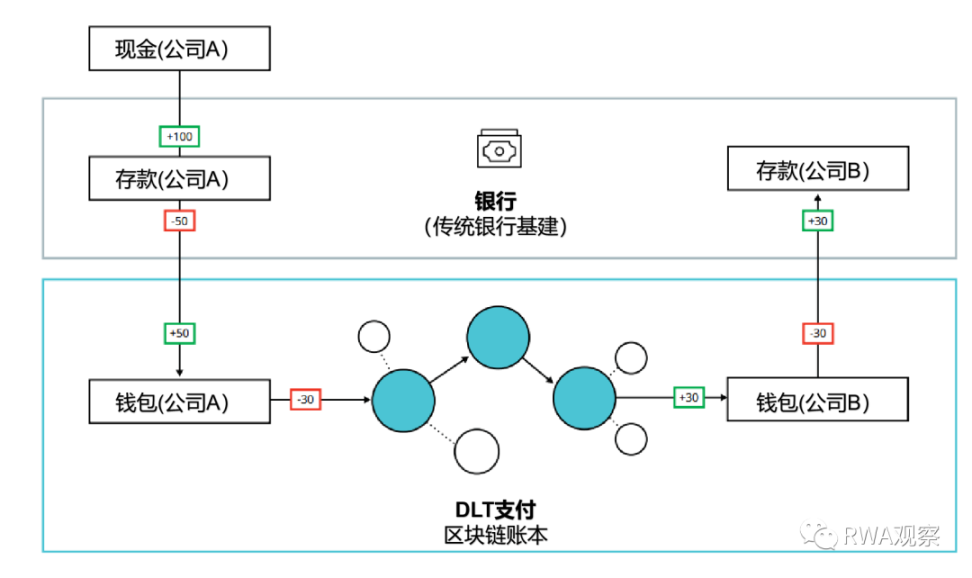

The general process is as follows:

As you can see, there seems to be a significant missing link in the middle DLT payment process.

That's right, currently most banks' deposit tokens are only used within their own networks.

To achieve direct settlement between deposit tokens from different banks, the participation of other giants is still needed.

02 Settlement Solutions are Emerging

Federal Reserve: Come settle on our network?

In July this year, the esteemed Federal Reserve (actually the New York Innovation Center under the Federal Reserve) personally proposed a concept plan for a Regulated Liability Network (RLN).

This plan aims to achieve real-time cross-border settlement of various assets within the compliance framework in the United States.

With the Federal Reserve personally involved, many other institutions are sure to follow, including:

SWIFT, BNY Mellon, Citigroup, Hang Seng, Mastercard, PNC Bank, TD Bank, Truist Bank, US Bank, and Wells Fargo.

SWIFT: Keep using us, I can become a node

Traditional banks must use SWIFT to achieve cross-border settlements.

Cryptocurrencies often threaten to disrupt SWIFT.

Of course, SWIFT won't just sit back and do nothing.

At the end of August, SWIFT launched a project that allows it to remain a core node in the future transfer of tokenized assets between banks.

In this project, SWIFT has also brought in several partners, some of which overlap with the Federal Reserve:

ANZ (Australia and New Zealand Banking Group), BNP Paribas, BNY Mellon, Citigroup, two European clearing giants Clearstream/Euroclear, Raiffeisen Bank, Six Digital Exchange (SDX), and DTCC (the US Securities Depository and Clearing Corporation, the same one involved with BlackRock today).

Chainlink: Use my cross-chain solution

In the plan proposed by SWIFT, each bank will have its own private chain for original asset tokenization (which large institutions are indeed doing), and then use Chainlink to provide an enterprise abstraction layer (the recently famous CCIP) to map assets across chains to Ethereum's Sepolia network.

If this solution is widely adopted, who might be the biggest winner?

03 Don't Expect Traditional Exchanges to Act Soon

Nasdaq: My custody solution is on hold

While other financial institutions are ramping up their efforts, Nasdaq announced in July that its digital asset custody solution is on hold.

This solution was proposed by Nasdaq back in 2018, and the official reason for the pause is "regulatory uncertainty."

Meanwhile, various Bitcoin spot ETF applications have adopted Coinbase's partnership solution. However, considering that both Coinbase and the subsequent ETFs are landing on Nasdaq, it may indeed be a matter of avoiding conflict.

London Stock Exchange: I'm still in discussions

The London Stock Exchange has also stated that it is preparing a new digital asset trading market, which will be built on blockchain technology and operate as a separate entity from the London Stock Exchange.

As for the current progress, they are still in discussions with the UK government and regulatory authorities.

Hong Kong Stock Exchange: I'm keeping up~

Hong Kong has actually been quite proactive in following up on policies.

As early as the end of 2022, it opened up cryptocurrency ETFs, with Southern Eastern listing Bitcoin futures ETFs and Ethereum futures ETFs. However, these futures ETFs are essentially based on futures contracts from the Chicago Mercantile Exchange.

After the US launches spot ETFs, it is highly likely that Hong Kong will follow suit.

04 Will Asset Tokenization Ignite the Next Bull Market?

These are all established institutions from traditional finance, aware of the importance of fully compliant asset tokenization (some institutions are even part of the regulatory framework).

In the context of finance, any asset can be tokenized.

However, based on current trends, deposit tokenization may be the closest to large-scale application of substantial real-world assets (and regulatory and legislative bodies actually cannot provide effective measures to stop this process).

The attitude of the US legislative bodies has also begun to shift positively; recently, PayPal launched a stablecoin and received support from the House Financial Services Committee. If J.P. Morgan's deposit token solution also gets the green light, the on-chain assets could grow exponentially.

Risk warning Risk warning

Risk warning Risk warning

Popular articles