SignalPlus Macro Analysis Special Edition: 80K

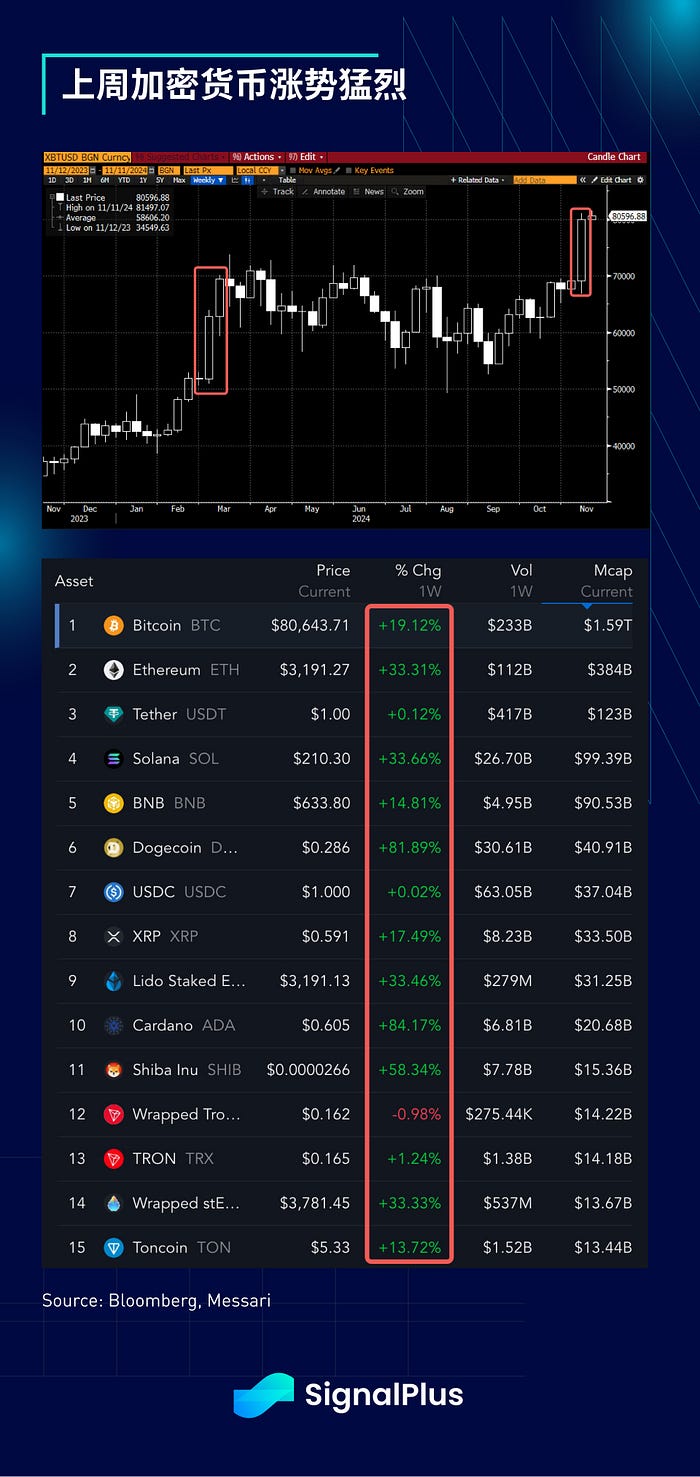

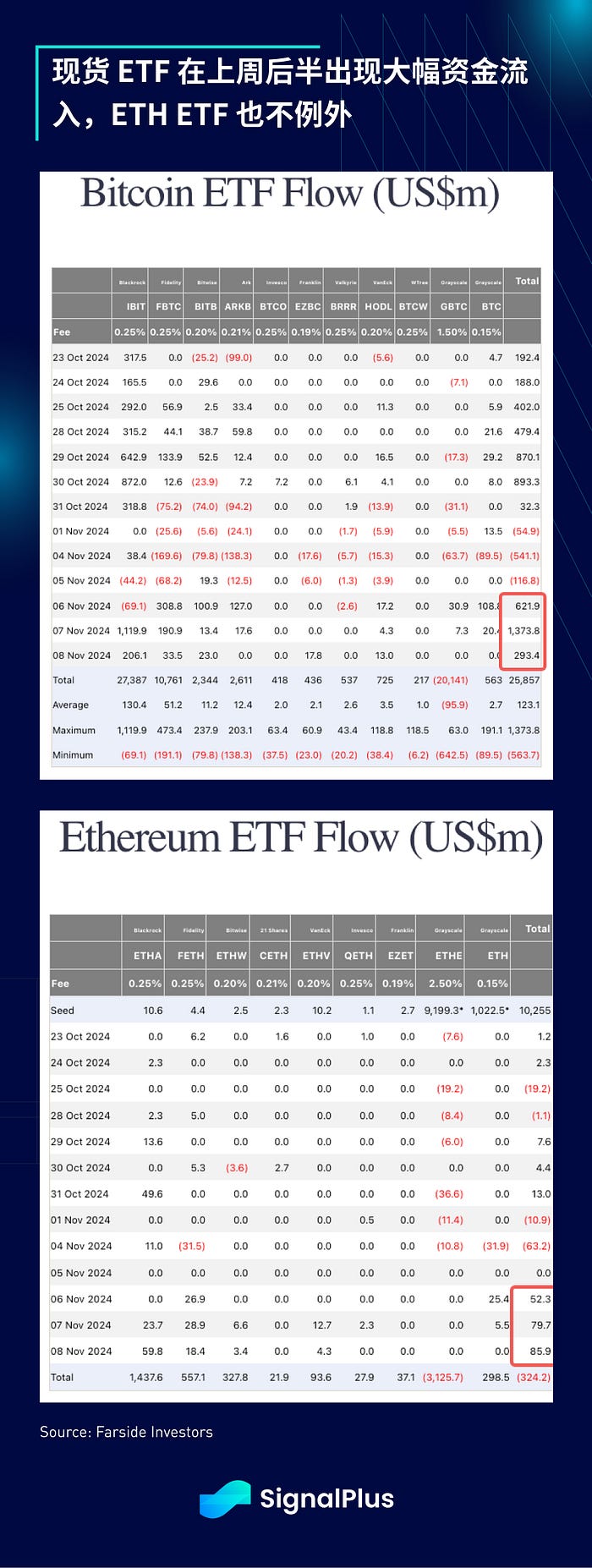

Although Trump will not officially take office for another two months after his election, the impact of his victory has already been widely reflected in geopolitics and capital markets. Cryptocurrency has once again become the focus, with BTC prices breaking through $80,000 while vote counting is still ongoing in some parts of the U.S. Last Thursday, Blackrock's BTC ETF (IBIT) set a record for single-day inflows of $1 billion, and even the ETH ETF saw its third-highest single-day inflow in history.

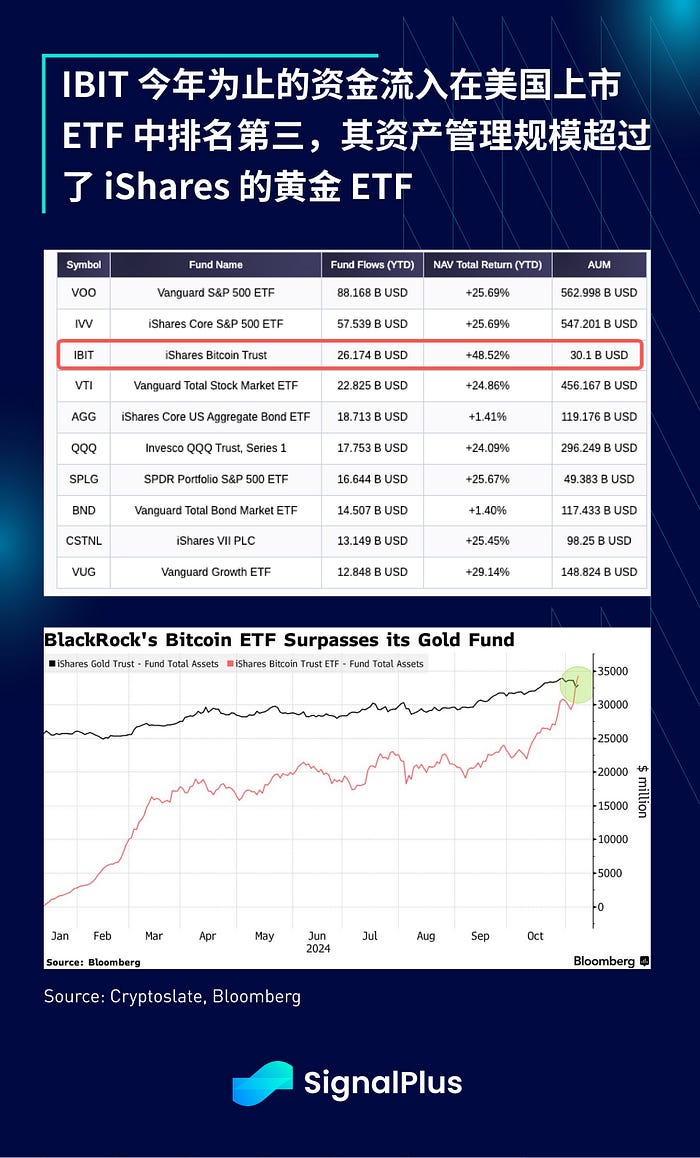

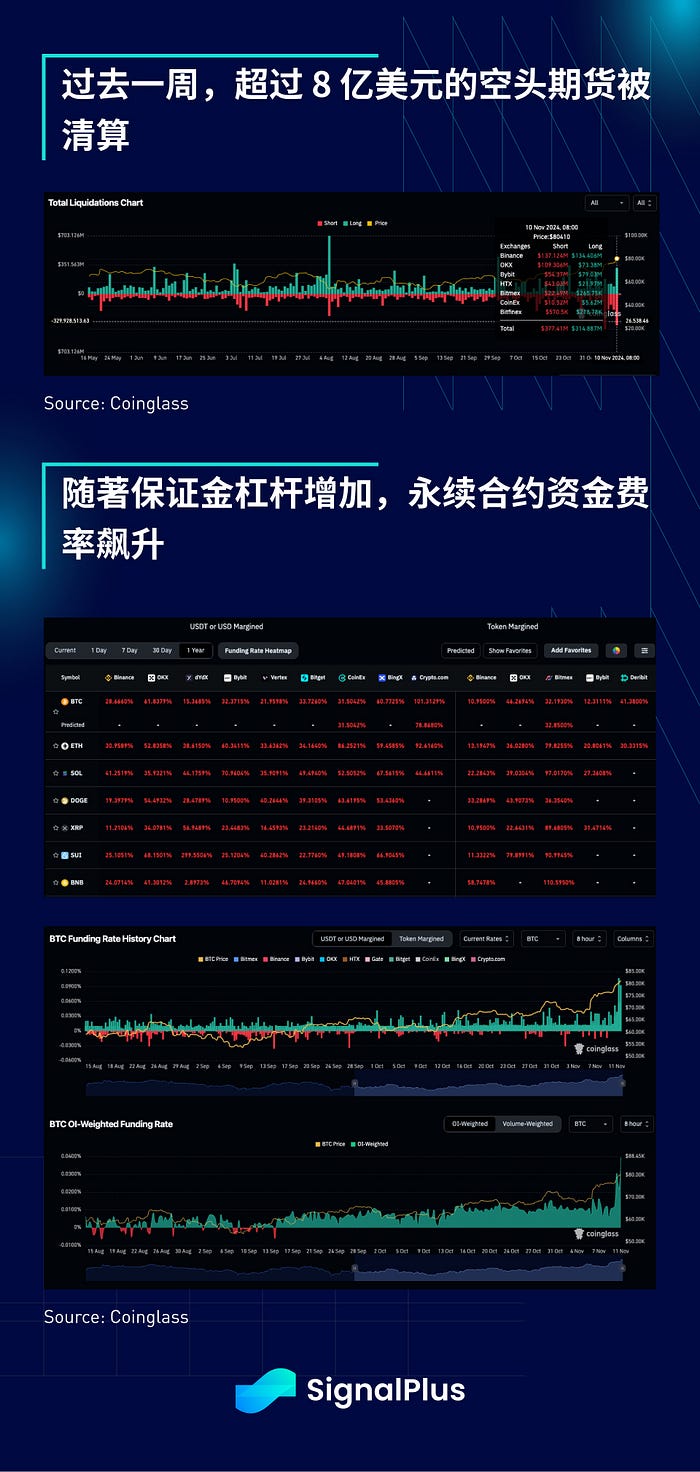

IBIT's inflows this year rank third among all U.S.-listed ETFs, with assets under management exceeding iShares' own gold ETF, surpassing $33 billion. During this surge, centralized exchanges (CEX) liquidated over $800 million in short futures positions in the past week, marking one of the largest short liquidations of the year. Meanwhile, as leveraged funds returned in large numbers, the funding rate for perpetual contracts soared to around 30%.

Additionally, despite weak on-chain activity, inflows from traditional finance have become a stable support factor. The market capitalization of stablecoins has steadily rebounded this year, approaching the historical highs of 2022. Further inflows into stablecoins should provide more margin funds, and as prices continue to rebound, leverage is expected to remain elevated.

From a political perspective, considering that the incoming government is more inclined to support cryptocurrency legislation, the industry is increasingly optimistic about the emergence of a more favorable regulatory framework for cryptocurrencies in the future.

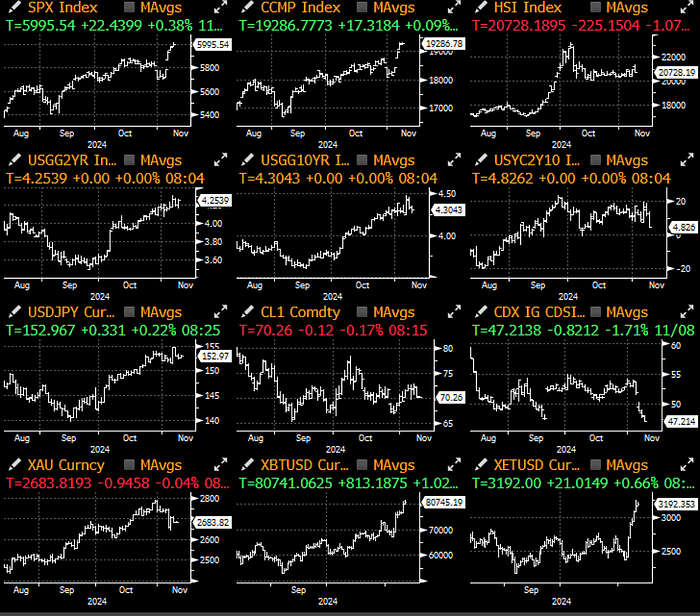

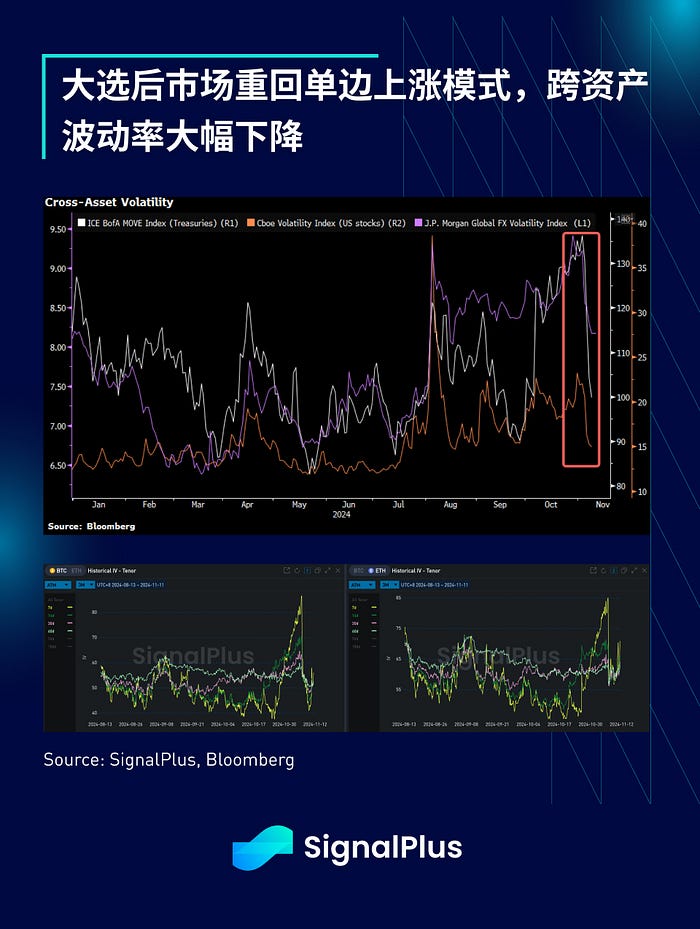

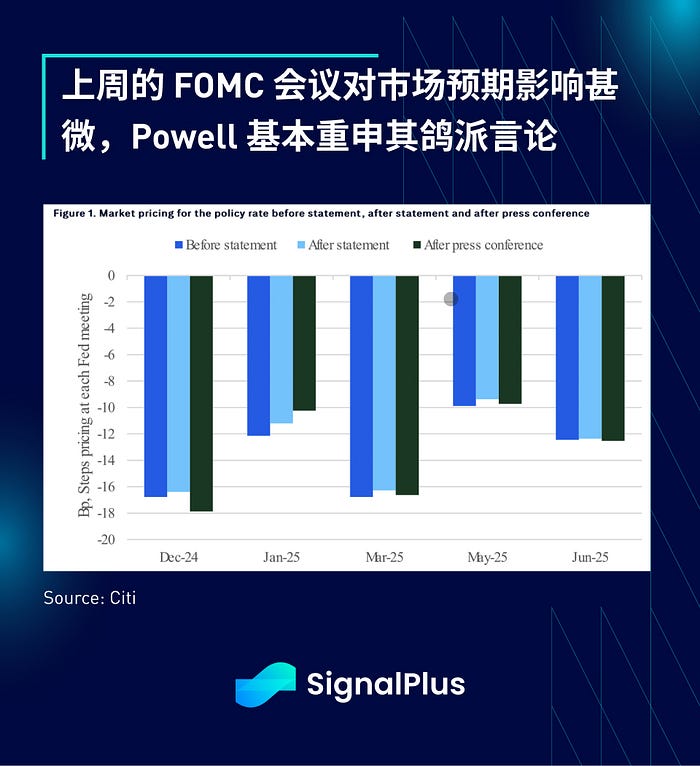

Returning to the macro market, the U.S. stock market has ignored the disappointment of China's stimulus policies and continues to reach new highs, while the fixed income market remains stable due to the dovish stance from last Thursday's FOMC meeting. Furthermore, as the market is expected to maintain a risk-on mode before the end of the year, the cross-asset volatility of macro assets has significantly decreased. On the other hand, with BTC breaking through $80,000, the volatility of BTC and ETH has slightly rebounded, and $100,000 call options have once again entered the market spotlight.

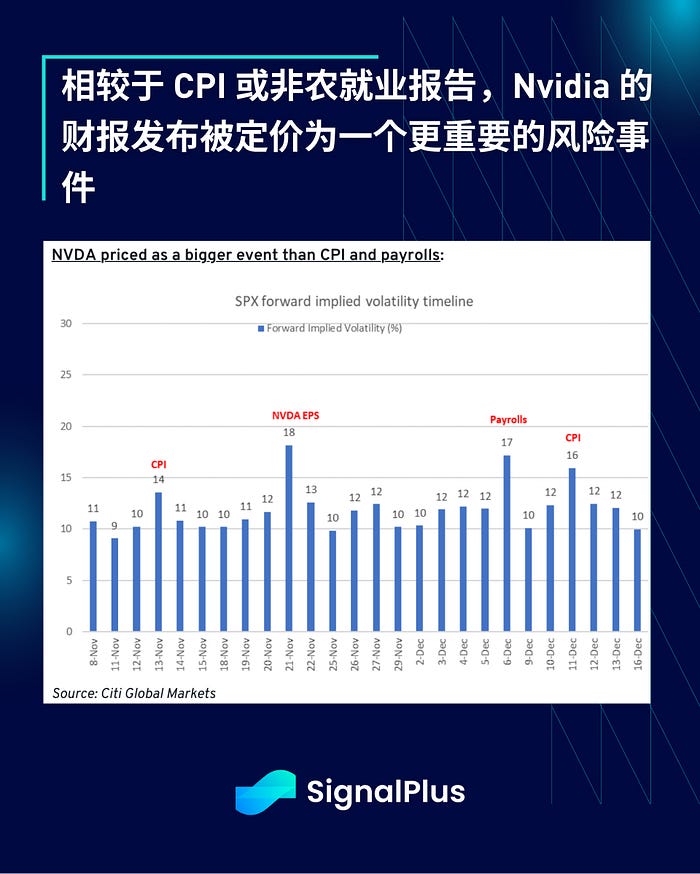

This week will see the release of CPI data, and aside from that, there are not many other important macroeconomic data points this month. Interestingly, market pricing reflects that Nvidia's earnings report is considered a more significant risk event compared to the CPI or non-farm payroll reports, indicating that the market has more confidence in the Federal Reserve's stance and that there are no obvious negative catalysts in the market environment.

So, enjoy the party while it lasts, but still maintain cautious risk management. Good luck to everyone!

Risk warning Risk warning

Risk warning Risk warning

Popular articles