SignalPlus Macro Analysis Special Edition: The Times They Are a-Changin'

Trump's second term is about to reach one hundred days, but the geopolitical situation has undergone tremendous changes compared to a few months ago. The question is no longer whether the United States will decouple from the world, but rather "how" it will decouple; and the United States' "exorbitant privilege" in the global reserve currency system is also facing substantial challenges.

Trump's second term is about to reach one hundred days, but the geopolitical situation has undergone tremendous changes compared to a few months ago. The question is no longer whether the United States will decouple from the world, but rather "how" it will decouple; and the United States' "exorbitant privilege" in the global reserve currency system is also facing substantial challenges.

Trump's second term is about to reach one hundred days, but compared to a few months ago, the geopolitical situation has undergone a dramatic change. The question is no longer whether the United States will decouple from the world, but "how" it will decouple; and the "exorbitant privilege" of the dollar as the global reserve currency system is also beginning to face substantial challenges.

The correlation between assets is breaking down, capital flows are starting to reverse, and Bitcoin has (finally) begun to show a clear divergence from stocks. The president even threatened to treat the Federal Reserve Chairman as a contestant on "The Apprentice," while large U.S. donor funds are massively selling off illiquid private equity assets at the industry's most difficult moment. Have we truly reached a critical turning point in financial history?

Dollar Safe-Haven Assets

One of the most pressing questions in the market right now—has the dollar and U.S. Treasuries lost their long-standing status as safe-haven assets? Has Trump caused irreparable structural damage to the global security and financial system established after the war?

Investors are significantly withdrawing from dollar assets, turning to euros and yen, while also selling U.S. stocks in favor of Chinese stocks. The uncertainty surrounding the end of "American exceptionalism" has caused the dollar index to fall to a three-year low, while the University of Michigan Consumer Sentiment Index has also dropped to nearly historical lows due to heightened inflation concerns.

Foreign investors' allocation to U.S. stocks has also slowed significantly, with ETF inflows nearly zero over the past three months.

At the same time, macro asset correlations are breaking down, with the yen appreciating significantly (USD/JPY ~ 140), but the Nikkei index rising instead of falling, indicating that this wave of yen appreciation is not driven by typical arbitrage unwinding but is a result of the dollar weakening.

The most important "known unknown" remains U.S. Treasuries, with the 10-year Treasury yield rising against the backdrop of a weakening dollar, stock market, and underlying economy, resembling emerging markets. While we disagree with this characterization, it is undeniable that the current financial situation in the U.S. is tightening, and bonds have not fulfilled their risk-hedging function. Before the tariff games of the Trump administration cool down, the market is unlikely to find a clear solution.

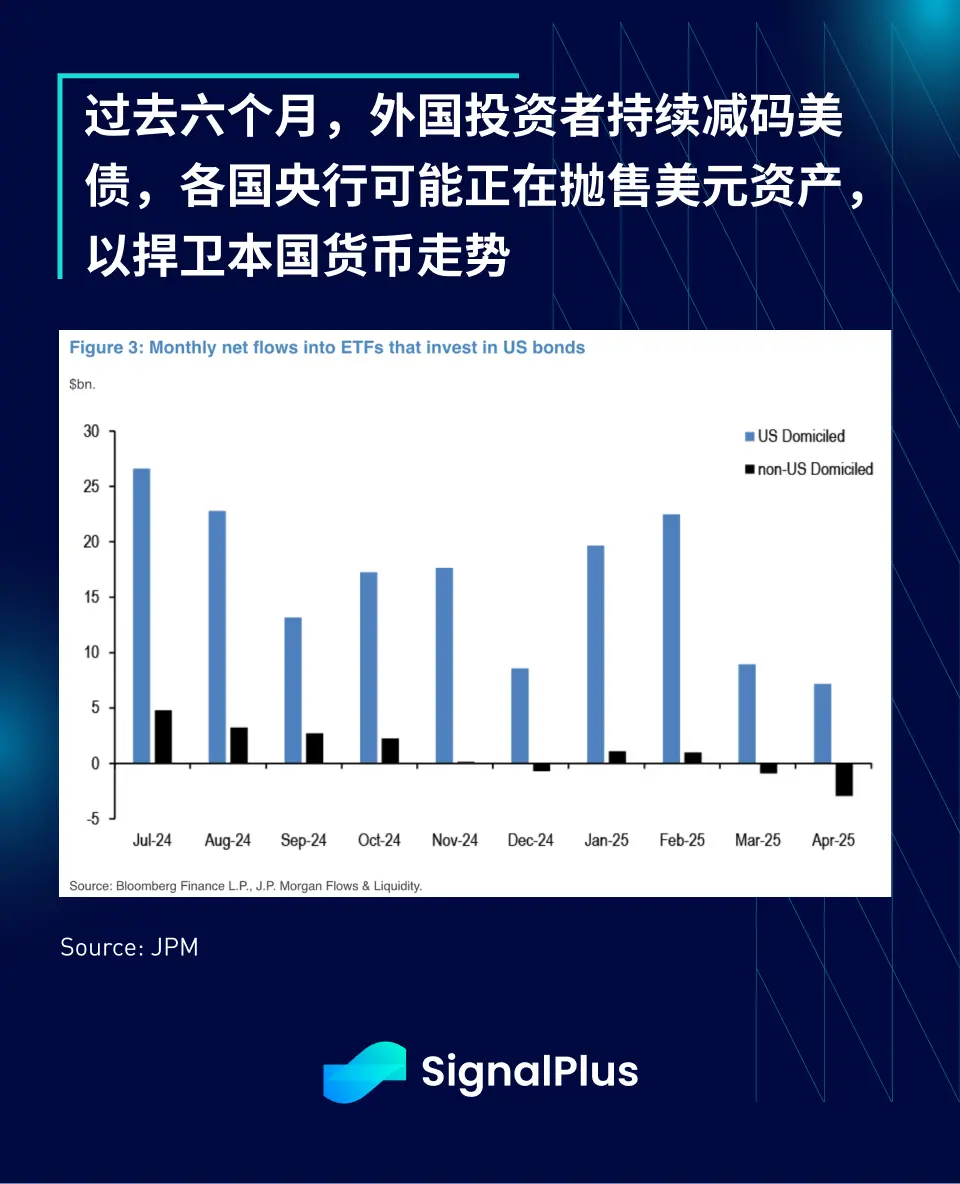

Over the past six months, foreign investors have continued to reduce their holdings of U.S. Treasuries, and central banks around the world may be selling dollar assets to defend their own currency trends.

Despite the recent significant pullback in U.S. stocks, they still have a significant premium compared to emerging markets and other international stock markets, which have made almost no progress since the global financial crisis (in terms of valuation multiples). Given that the trade war is unlikely to benefit any country completely, we do not believe that foreign markets can narrow the valuation gap with U.S. stocks solely based on their own performance. In this case, if U.S. stocks ultimately "correct downward" to narrow the valuation gap, it would mean wealth destruction, not a positive development that the market would welcome. The market should proceed with caution, as wishes coming true may not necessarily be a good thing.

Uncertainty of Trade Agreements

The tariff turmoil continues, with President Trump, as usual, oscillating between hard threats and the prospect of reaching an agreement. Last Friday, he claimed to be "very confident about reaching a trade agreement with the EU… will reach a good agreement with China… everyone is on my priority list," which temporarily boosted risk assets, but subsequent progress has been limited, as the first trade agreement remains a long way off.

We still believe that the apparent tariff numbers are less important than the "minimum tax rate" set in the preliminary agreement; more concerning is that the U.S. has yet to reach a preliminary agreement with Japan, indicating that the negotiation goals and scope may still be unclear.

However, following Chinese President Xi Jinping's visit to Southeast Asia, the U.S. is also expected to hold bilateral trade talks with Japan, South Korea, Thailand, and India during the IMF Spring Meetings this week. Reports suggest that the UK is also expected to finalize an agreement with the U.S. within three weeks. We will closely monitor whether any concrete progress can be made in the coming weeks.

"The Apprentice" Season 2

"Federal Reserve Chairman Jerome Powell is always slow and makes mistakes; yesterday he released a typical 'disaster' report… I can't wait to get him fired! The Fed should lower interest rates for the American people; that's the only thing he can do… I'm very unhappy with him; if I want him out, believe me, he will be gone soon."

-- Trump via Truth Social, April 17, 2025 "If the Federal Reserve Chairman knew what he was doing, interest rates should have been lowered long ago. He should lower rates immediately."

-- Trump at the Oval Office on April 19, 2025 "Prices are falling smoothly as I predicted, basically with almost no inflation, but if 'slowpoke' doesn't hurry up and lower rates, the economy could slow down. Europe has already lowered rates seven times. Powell is always too slow, but during the election, when helping Biden and later Kamala Harris, he was quick to lower rates."

-- Trump via Truth Social, April 21, 2025

Although the White House previously claimed it was willing to endure some economic pain to cope with the trade war, Trump has returned to his familiar script, directing his criticism at the Federal Reserve for not lowering rates faster.

While we agree that lowering long-term interest rates in a relaxed financial situation is indeed wise, urging the Federal Reserve to cut rates seems unhelpful against the backdrop of a weakening dollar and inflation driven by rising import costs.

The market seems to agree with this view, as the SPX index fell 2% on Monday, while yields rose again, indicating that market participants clearly do not agree with the latest threatening rhetoric.

On the other hand, Federal Reserve Chairman Powell remains calm and professional in response to the situation, firmly upholding the independence of the Federal Reserve:

"The independence of the Federal Reserve is widely understood and supported in Washington and Congress."

"People can say whatever they want; that's fine. But our decisions are completely free from political or other external influences."

-- Powell at the Economic Club of Chicago, April 17, 2025

Nonetheless, concerns about an economic slowdown are intensifying, with the interest rate market pricing in far more rate cuts this year than the Federal Reserve's forecast (4 vs 2). In this context, we believe it is unwise for the president to continue pressuring the Federal Reserve, but looking back over the past two months, more outrageous statements have been heard.

Economic Slowdown Imminent

From certain indicators, the current uncertainty in economic policy has reached an all-time high, even surpassing the early days of the pandemic. This uncertainty has led to a significant decline in business outlook, with the New York Fed's manufacturing survey showing that business activity expectations have dropped to their lowest level in over a decade.

Sub-indicators also show similar trends. Forward-looking shipping and capital expenditure indicators have plummeted, while payment prices have risen significantly. Meanwhile, corporate earnings have continued to be downgraded, with earnings growth facing compression, casting a shadow over the stock market.

Poison Pill

Although the market is accustomed to listening to officials' statements, the so-called "Trump 2.0 trade" has so far been a disaster, with most policy narratives ultimately leading to significant losses. A picture is worth a thousand words:

Once bitten, twice shy. The market is unlikely to easily accept Trump's statements in the near future.

Brave or Cannon Fodder?

While hedge funds are busy deleveraging and reducing risk due to significant losses in 2025, retail investors are doing the opposite, with record inflows into leveraged Nasdaq ETFs over the past two weeks.

There is ample evidence that, over the past five years, retail and passive funds have significantly outperformed active funds and professional fund managers. Will history repeat itself again, even though it seems doubtful at the moment?

As retail investors ramp up, a considerable number of companies have lowered their earnings expectations, and the market depth (liquidity) of the SPX index is nearing historical lows.

Gold Shines Again

The recent surge in gold prices has almost completely made up for the lag of the past decade, with spot prices rising about 150% since the beginning of 2024, as investors seek a capital safe haven in this topsy-turvy world, leading to a vertical rise in gold prices.

Ironically, President Trump recently made a poignant comment on social media: "Those who own gold can set the rules," possibly referring to his negotiation strategy, further pushing spot gold prices above $3,400 to new highs.

Additionally, data shows that this wave of gold price increases mainly occurred during Asian trading hours, indicating possible inflows from official or central bank funds shifting from the dollar to other safe-haven assets. Compared to the past, the decoupling phenomenon of the dollar seems more pronounced.

BTC Narrative Restart - No Longer Just Nasdaq, But Not Yet Gold

Decoupling from the dollar may bring BTC back into the market's focus as a long-term bullish narrative for a store of value. Although we have criticized BTC over the past year for increasingly resembling a high-leverage version of the Nasdaq index, it has recently begun to show signs of decoupling from the stock market. Last week, while U.S. stocks performed poorly overall, BTC prices still approached the $90,000 range.

Of course, we cannot be overly optimistic. Year-to-date, BTC's performance still lags significantly behind spot gold, so for now, it can only be said that it is gradually evolving into a hybrid of gold and leveraged Nasdaq, but this development is already better than the positioning of "the beautified version of TQQQ."

JPM data shows that recent gold futures positions have increased significantly, while BTC's capital flows have stagnated. To truly realize BTC's potential as a safe-haven asset, the market still needs to observe whether capital will flow back in.

Minor Impact from U.S. Donor Funds

In addition to issuing threats internationally, the Trump administration has recently been at odds with U.S. donor funds domestically, particularly represented by Harvard, which may negatively impact market liquidity.

Reports indicate that Yale University's endowment fund will sell about $6 billion in private equity positions, coinciding with a difficult phase for the private market, which is experiencing historically low liquidity and weak investment returns.

Non-U.S. observers may not realize the scale and importance of the U.S. donor fund system, which has traditionally been one of the most influential "permanent" holders in the capital markets. Will the ongoing political struggle lead to a slowdown in their investments or even change their capital allocation structure? Dealing with the Trump administration is never boring. Times are indeed changing…

Wishing everyone successful trading this week!

Risk warning Risk warning

Risk warning Risk warning