SignalPlus Macro Analysis Special Edition: Quarter End

Will the government shut down? Yes, Trump said, "Because the Democrats are crazy." Why is the White House seeking to lay off federal workers on a large scale, rather than just mandating unpaid leave? Trump responded, "Well, it's all the Democrats' fault."

"If it has to shut down, then it will shut down," Trump said on Friday. "But they are the ones causing the government shutdown."

The (semi)annual debt ceiling drama in the U.S. is playing out again, on Tuesday, September 30.

Will the government shut down? Yes, Trump said, "Because the Democrats are crazy." Why is the White House seeking to lay off federal workers on a large scale, rather than just mandating unpaid leave? Trump responded, "Well, it's all the Democrats' fault."

"If it has to shut down, then it will shut down," Trump said on Friday. "But they are the ones causing the government shutdown."

The (semi)annual debt ceiling drama in the U.S. is playing out again, on Tuesday, September 30.

Will the government shut down? Yes, Trump said, "because the Democrats are crazy." Why is the White House seeking mass layoffs of federal workers instead of just mandatory leave? Trump responded, "Well, it's all the Democrats' fault."

Will the government shut down? Yes, Trump said, "because the Democrats are crazy." Why is the White House seeking mass layoffs of federal workers instead of just mandatory leave? Trump responded, "Well, it's all the Democrats' fault."

"If it has to shut down, then it will shut down," Trump said on Friday. "But they are the ones causing the government shutdown."

The (semi)annual debt ceiling drama in the U.S. is playing out again, with no progress made before the deadline on Tuesday, September 30, to avoid a potential government shutdown. As of the writing of this article, President Trump has just agreed to a last-minute meeting with top congressional leaders on Monday, with healthcare funding still being a key point of contention.

Even in the worst-case scenario, a debt financing interruption is unlikely, but any government shutdown could delay the release of this Friday's non-farm payroll data—if the Bureau of Labor Statistics temporarily ceases operations. This would deprive the market of a key economic data point ahead of the Fed's October meeting, increasing the focus and volatility around any Fed speeches during that time.

Assuming the Bureau of Labor Statistics can remain operational, non-farm payrolls are expected to rise slightly above 100,000 in September, with an unemployment rate of around 4.3%. Asian markets may perform sluggishly as China approaches its Golden Week holiday, while quarter-end portfolio rebalancing flows may add some volatility around mid-week.

Aside from Washington's fringe policies, the market remained calm last week as the third quarter approached its close with another very strong performance. Wall Street reported that the average return of "ordinary" macro assets was about 2.5%, with gold leading the way (up about 14%). Global stock markets rose across the board, with both developed and emerging markets performing strongly, while global interest rates declined due to central banks' widespread shift to a dovish tone.

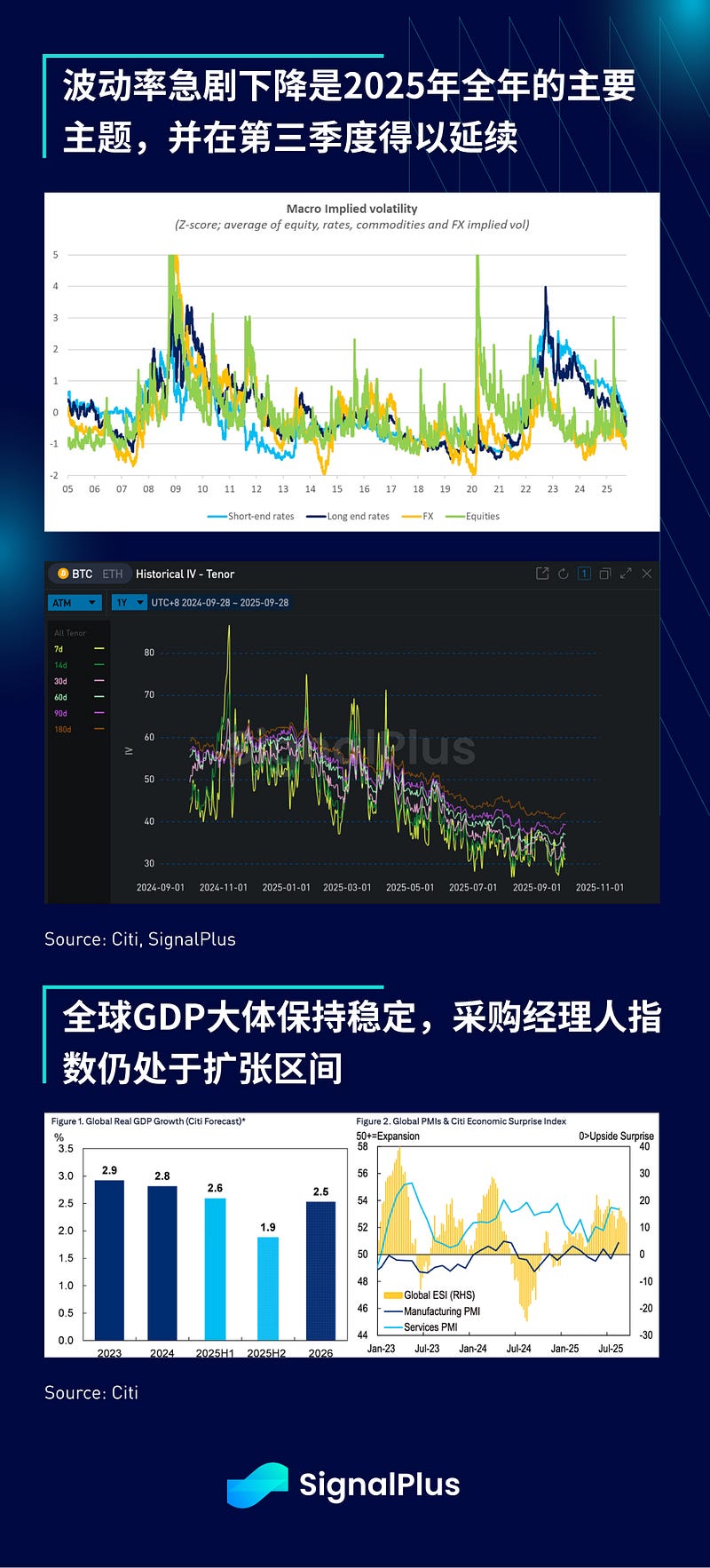

Another major theme of this quarter has been the decline in implied volatility, reflected across various sectors including stocks, interest rates, foreign exchange, and even Bitcoin. This is primarily due to a significant drop in actual volatility, driven by the Fed's accommodative policies, stable global GDP, a lack of significant tariff pass-through effects in CPI readings, and a recent easing of geopolitical tensions and tariffs.

The reduction in volatility has directly led to rising stock valuations and narrowing credit spreads, which is an inconvenient reality for those who may have missed the rally in risk assets.

As the U.S. fiscal year ends in late September, according to Citigroup research, the actual fiscal deficit this time is roughly in line with the Congressional Budget Office's estimate ($1.99 trillion vs $1.978 trillion). This actually means the deficit is $310 billion lower than in 2024 and is the lowest absolute deficit level since 2021. While its long-term impact remains uncertain, U.S. tariff policies have significantly improved fiscal conditions, expected to have generated $3 trillion in revenue over the past decade, helping to reduce projected deficits over the next two years.

In response, the dollar experienced one of its strongest weekly performances since midsummer, thanks to resilient U.S. data and a sharp repricing of front-end yields over the past week. The dollar's persistent net short positions could push this squeeze further into the fourth quarter, especially if the Fed's dovish rhetoric weakens even slightly, or if the stock market experiences a downturn, potentially triggering safe-haven inflows.

The situation in cryptocurrencies last week was far less optimistic, as the industry lost $300 billion in market capitalization due to a rapid deleveraging of several large altcoins (ETH -10%, Solana -13%). Over $3 billion was liquidated in a single day last Monday, leading to nearly $1 billion in weekly outflows from BTC and ETH ETFs.

Interestingly, Bitcoin's implied volatility remains low, as the market still does not seek any downside protection, possibly due to the dominance of long-only DAT holders. Given Ethereum's actual volatility, its volatility has risen, causing its volatility gap relative to Bitcoin to reach the highest level since 2019.

Despite the price sell-off, the fundamental backdrop for cryptocurrencies remains positive. Reports indicate that Tether is negotiating with a group of strategic investors (including Ark) to raise about $2 billion at a $50 billion valuation; while Kraken, having just completed its latest funding round, is reportedly seeking new funding at a $20 billion valuation.

Our inclination remains similar to the past week, leaning towards a more defensive posture given extreme valuations and challenging seasonal factors. Holdings in U.S. stock ETFs have surged to their highest levels since 2022, seemingly pricing in all the positive news about the economy, moderate inflation, and a dovish Fed.

However, as always, please do your own research, and have a great holiday in the region! Good luck and happy trading.

Risk warning Risk warning

Risk warning Risk warning

Popular articles