10 Counterintuitive Insights on Latin American Payments

10 conclusions about payments that contradict mainstream beliefs: crypto cards rely on high-net-worth individuals rather than retail, QR codes are replacing cards, stablecoin profits are competing to go to zero, and Latin American regulation is actually 5 years ahead of the United States.

10 conclusions about payments that contradict mainstream beliefs: crypto cards rely on high-net-worth individuals rather than retail, QR codes are replacing cards, stablecoin profits are competing to go to zero, and Latin American regulation is actually 5 years ahead of the United States.Author: Claudia, Marketing Director at Bybit

Compiled by: Jiahua, ChainCatcher

The payment rules in Latin America are being rewritten. 500 hours of field research. Things that most fintech companies haven't seen.

I spent nearly a month in Latin America with my poor Portuguese and even worse Spanish. I conducted over 500 hours of field research, flew for more than 100 hours, and talked to over 100 local users, developers, and more than 10 regulators.

The notes I brought back are different from what most payment practitioners on this platform say. Some of the content even contradicts my understanding before I set off.

In Brazil, the airline lost my suitcase. In Mexico, a wheel broke off my luggage when it came down the conveyor belt. Friends kept saying it was brave of me to travel alone as an Asian woman.

But what I really want to say is: Latin Americans are the warmest people I have ever met. Strangers helped me with directions, translations, and fixing my broken luggage. In Peru, a taxi driver waited for me for 20 minutes while I figured out which hotel I had booked. In São Paulo, a bartender drew me a map on a napkin to guide me to a meeting I was about to be late for.

Behind every story that says Latin America is "dangerous," there should be a story of a stranger helping me to the right taxi. Even when there is a language barrier, hearts connect.

Here are the things I learned, some of which I had misunderstood before this trip.

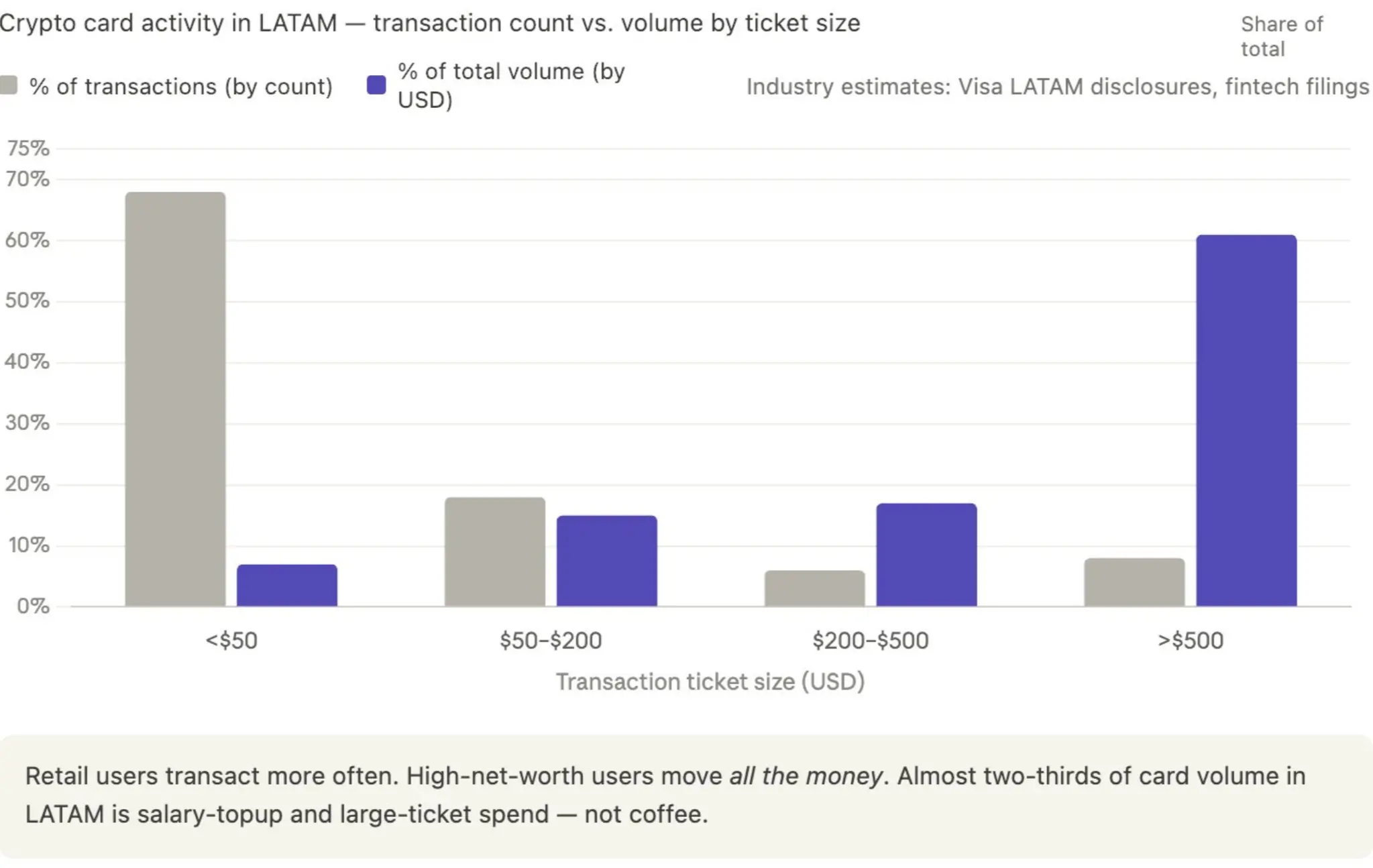

1. Do crypto cards win with cashback?

The real transaction volume of crypto cards does not come from high-frequency small purchases by retail users, but from high-net-worth clients.

The typical pattern I repeatedly saw in Brazil was: a professional receives their salary in USD or USDT (usually from multinational employers or crypto companies), loads money onto a crypto card, and when they need Brazilian Reais (BRL), they withdraw it to a local bank account via Pix.

Whether it's Kast, RedotPay, or any other crypto card, most of the transaction volume comes from this group, not from the person buying a $4 coffee with stablecoins.

Brazil received about $5 billion in personal remittances in 2024 (according to the Central Bank of Brazil), with the proportion arriving in stablecoin form rapidly increasing, as employers pay with USDC or USDT to avoid foreign exchange friction. The transaction volume of crypto cards in Latin America is highly concentrated in amounts over $500, which is typical of salary top-ups by professionals, rather than retail consumption.

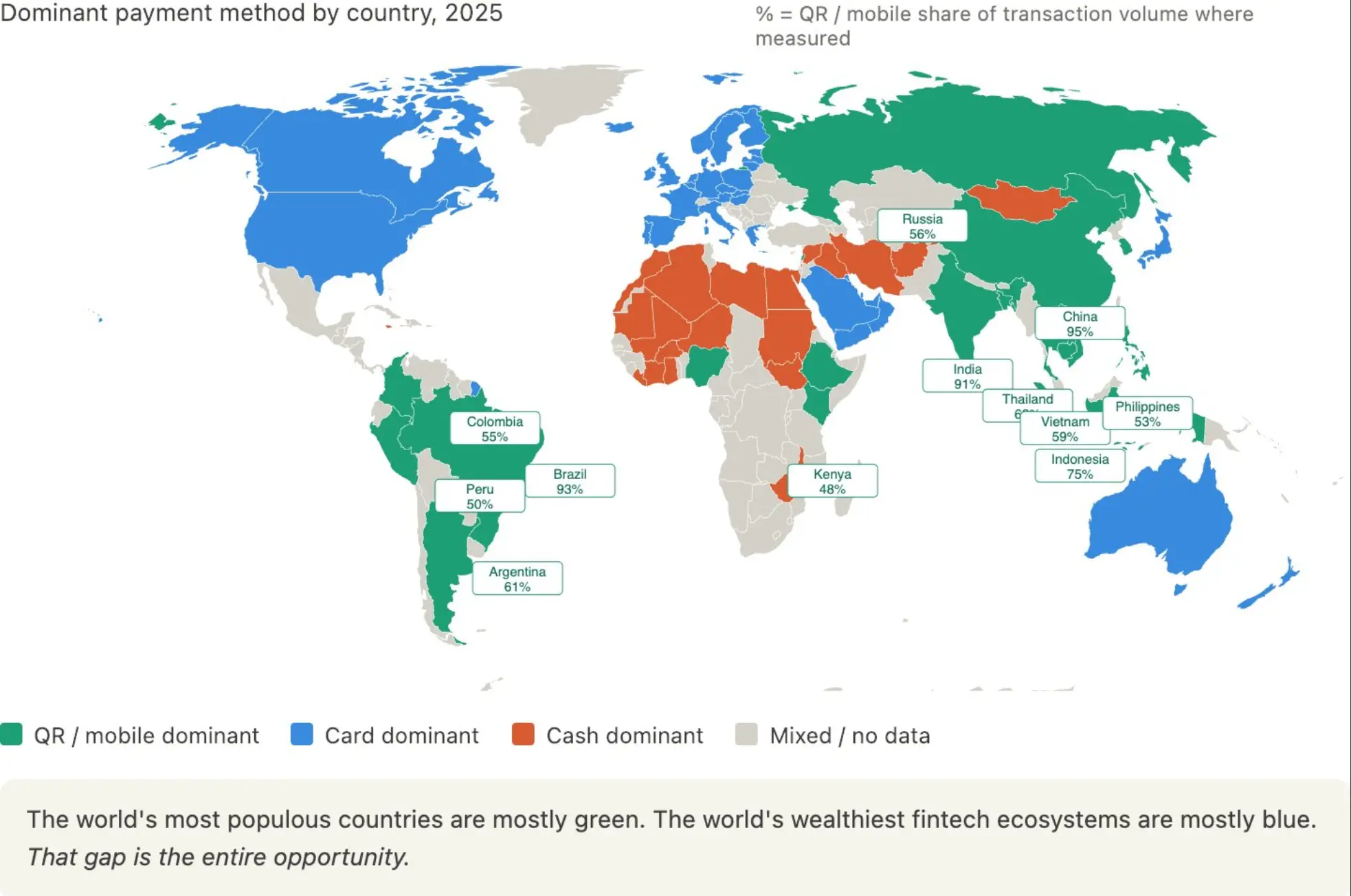

2. QR codes are set to dominate the next decade

Everyone is competing to issue cards and acquire customers. They haven't noticed the structural transformation happening underneath.

In emerging markets, QR code payments are quietly taking over the entire payment market. Brazil's Pix now processes over 6 billion transactions monthly. Argentina is filled with Mercado Pago QR codes. Peru has Yape and Plin. Mexico has CoDi. Merchants don't need POS machines, and customers don't need cards.

This is not just a Latin American story. Look at the map of the global payment landscape:

→ Brazil: 93% QR codes. Pix dominates.

→ China: 95% QR codes. Alipay and WeChat Pay have virtually eliminated cards.

→ India: 91% QR codes. UPI processes more transactions than all card organizations in the US combined.

→ Indonesia: 75%. Thailand: 62%. Argentina: 61%. Vietnam: 59%. Colombia: 55%. Philippines: 53%. Peru: 50%.

Meanwhile, the US, Canada, Western Europe, and Australia are still dominated by cards. Most of Africa and the Middle East still rely heavily on cash.

One point that most Western fintech practitioners overlook is that QR code payments have become the dominant payment method for most of the world's population. Card-dominated markets are becoming a shrinking minority, and these markets happen to be where venture capital, payment company headquarters, and most fintech Twitter users are located.

The most populous countries in the world are mostly green (QR codes), while the wealthiest fintech ecosystems are mostly blue (cards). This gap is where all the opportunities lie.

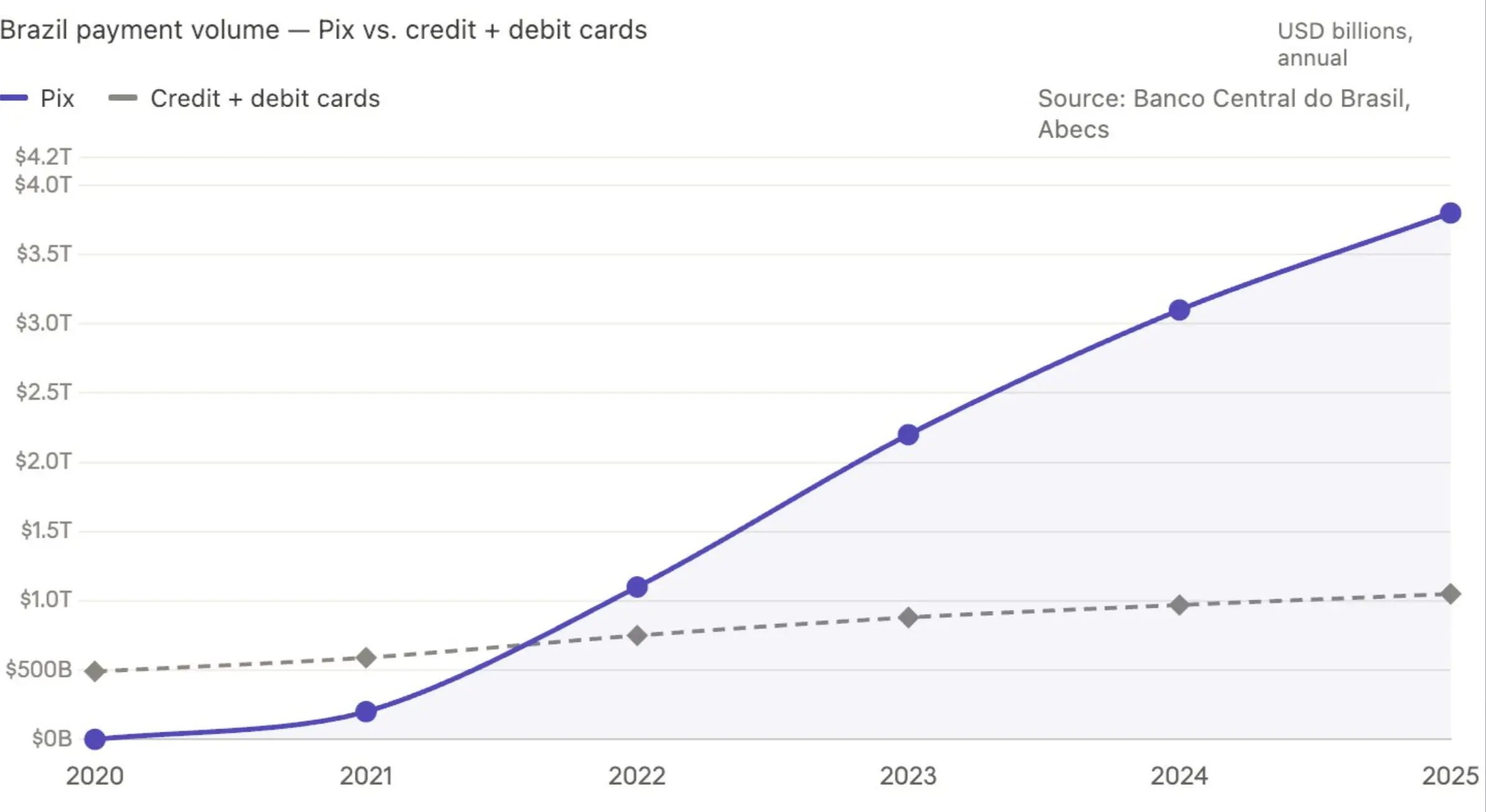

Now, let's turn our attention back to Brazil. Pix processed over $3 trillion in transactions in 2024, with about 80% of Brazilian adults using it. The transaction volume of Pix surpassed the total of credit and debit cards in 2023, and the gap is widening. Mexico's CoDi grew by 67% year-on-year in 2024. Argentina's Transferencias 3.0 doubled its transaction volume in the same year.

The logic of crypto cards assumes that the card organization tracks of Visa and Mastercard will always be the main settlement layer in emerging markets. But data shows that this is no longer the case. Moreover, the speed at which this gap is widening is faster than the speed at which card organizations can restructure themselves.

If you are still making crypto cards for emerging market users in 2026, your competitors are not other crypto cards, but payment tracks that don't need cards at all.

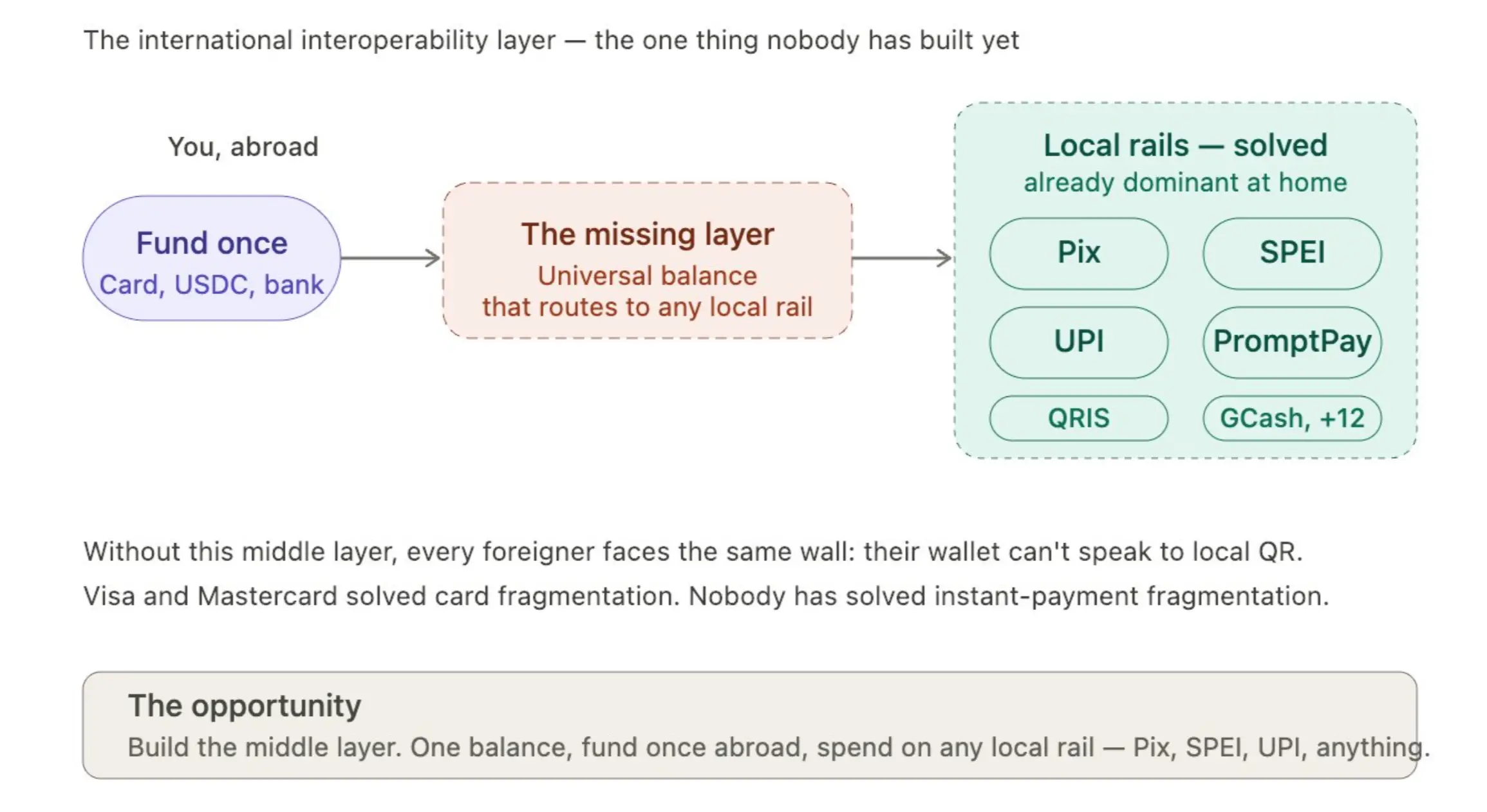

3. The biggest untapped opportunity in payments

Visa and Mastercard have unified the fragmentation of card organizations but have not solved the fragmentation problem for merchants. Not every small merchant can afford a POS machine. For a fruit stand, the cost of acquiring is simply not feasible.

QR codes and scan-to-pay solutions have solved the "last mile" within each country. Brazil's Pix, Mexico's SPEI, and Peru's Yape each dominate domestically.

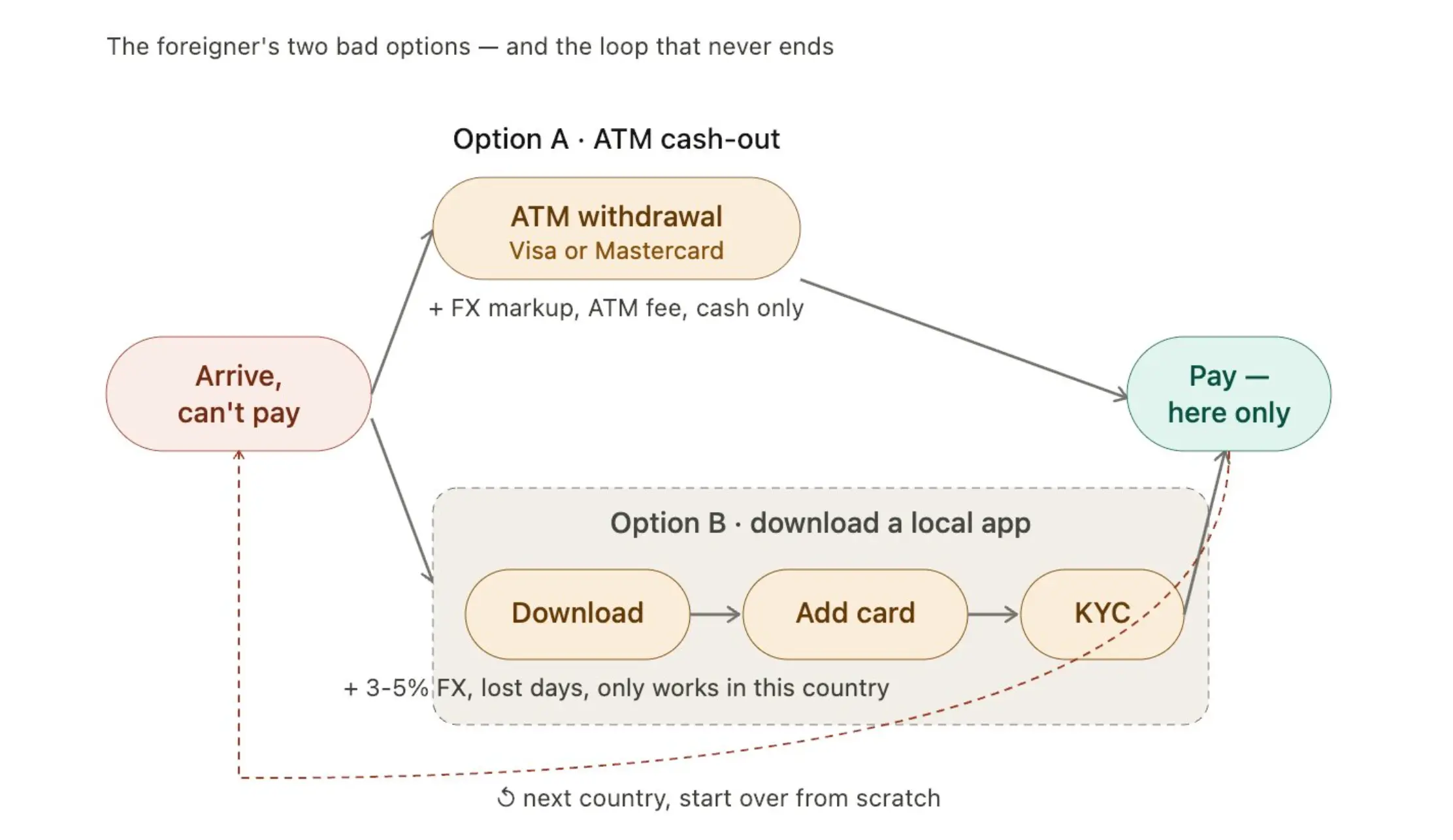

But internationally, it remains fragmented. As a foreigner, you essentially have two choices:

Choice A: Withdraw cash from an ATM using a Visa or Mastercard. The cost is foreign exchange markup and fees, and you can only pay in cash.

Choice B: Download a local app. Bind a card, complete KYC verification, with a cost of 3% to 5% in foreign exchange losses, taking several days, and usable only in that one country.

Both paths ultimately lead to the same outcome: you can only make payments in that country. Change countries, and everything is void; you have to start over.

One rainy night, sitting in a bar in Brazil as a foreigner wanting to order an espresso martini, my Pix wouldn't work. My non-Brazilian wallet couldn't communicate with the bar's POS (they could only accept local payments). The "international interoperability" layer between instant payment systems in different countries does not currently exist.

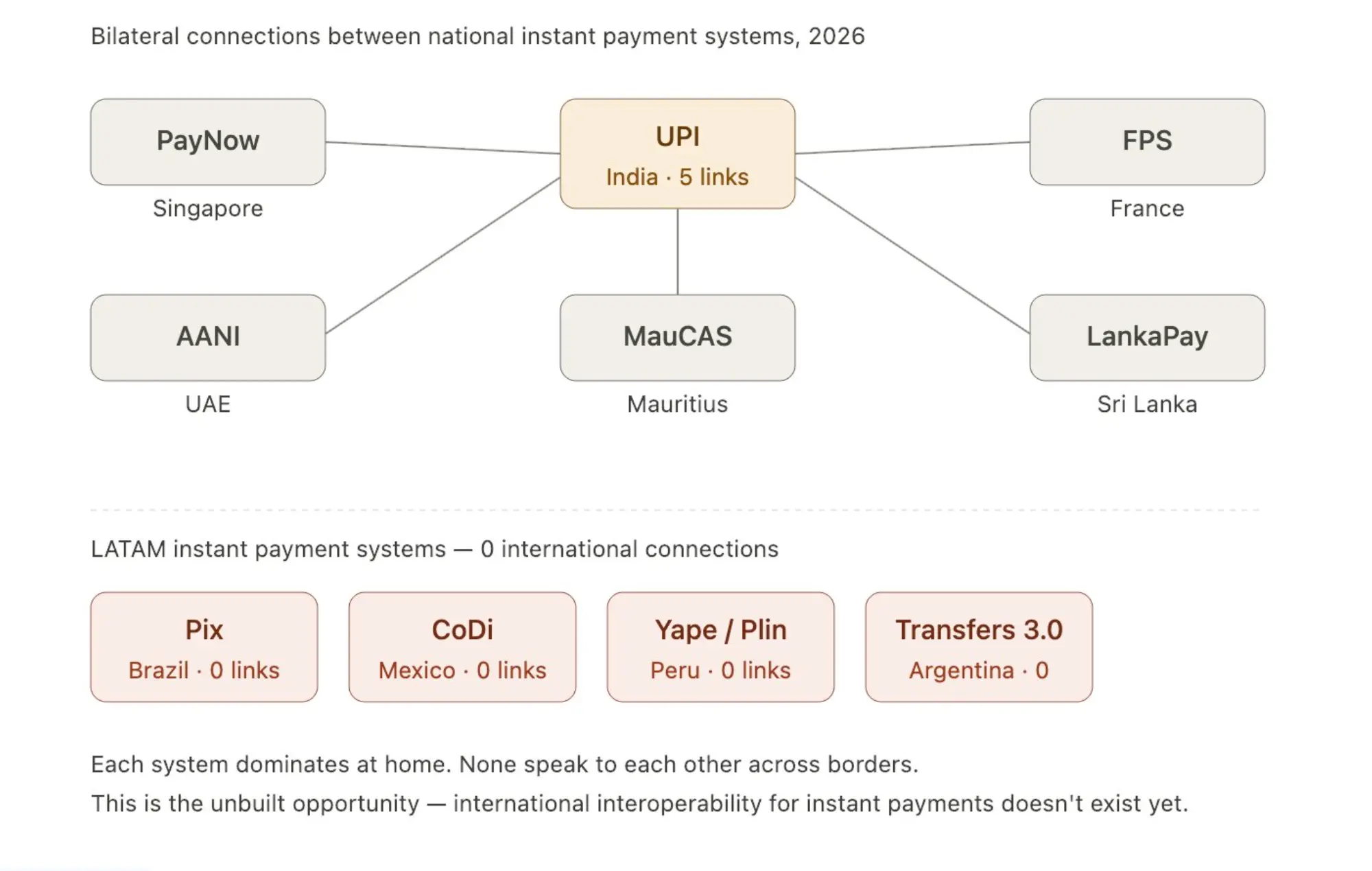

This is one of the biggest untapped opportunities in the payment sector.

India's UPI has already achieved bilateral interoperability with Singapore (PayNow), the UAE (AANI), France, Sri Lanka, and Mauritius. However, Latin America's instant payment systems are hardly connected with any international systems. The Bank for International Settlements (BIS) Nexus project is working on this, but multilateral interoperability won't be achieved until 2027.

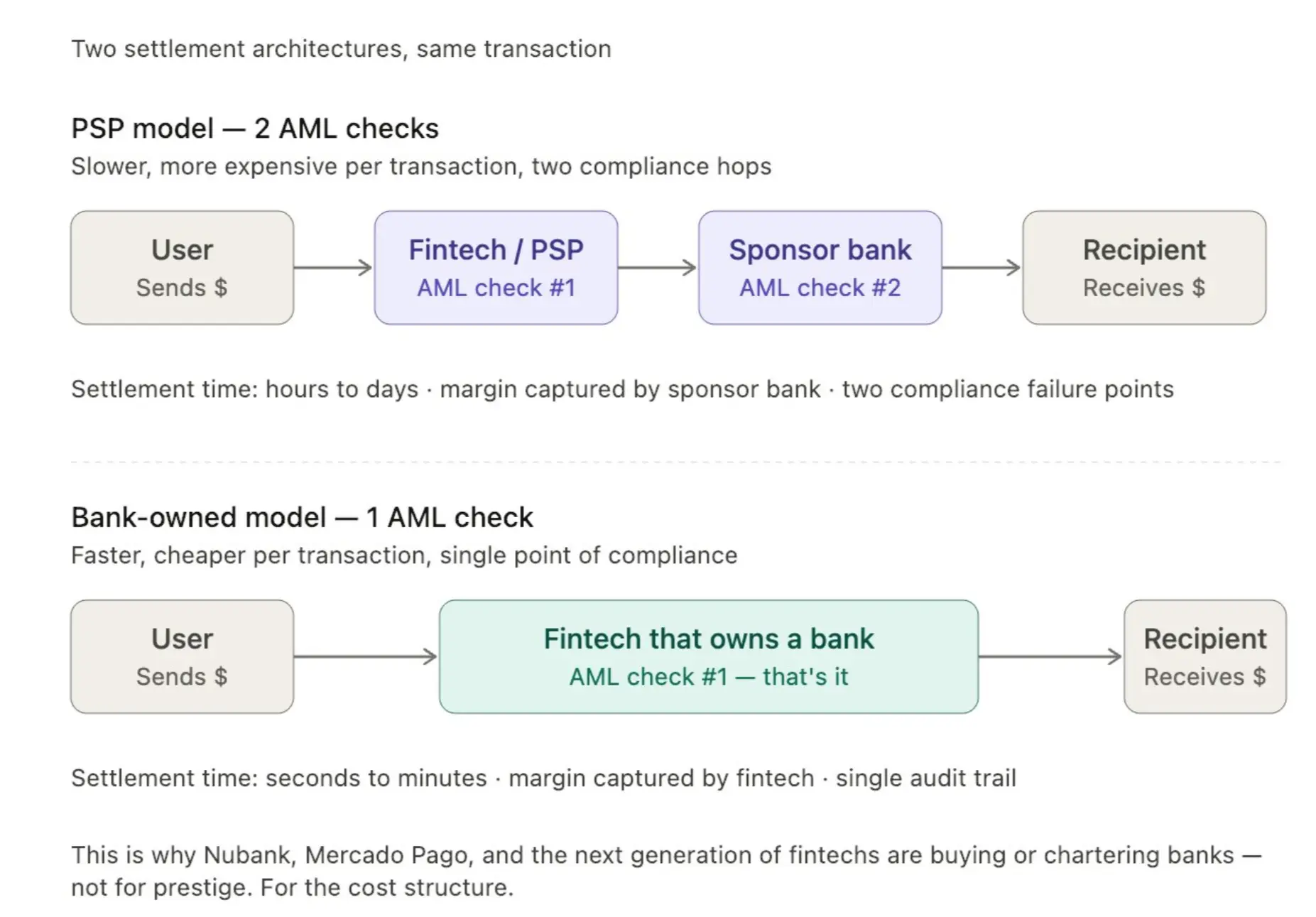

4. Payment competition is no longer about customer acquisition, but about settlement

Most companies connect with a PSP (Payment Service Provider) to handle compliance and anti-money laundering (AML) burdens. This approach works on a small scale.

But leading payment companies are now starting to acquire banks directly. Why? Because owning a bank means performing AML checks only once per transaction instead of twice. Settlements are faster, and profits are earned directly rather than rented.

So you will see Nubank's moves into banking, the wave of Brazilian fintech acquiring small banks, and several stablecoin companies quietly applying for banking licenses.

Brazil now has over 1,400 licensed payment institutions and more than 90 chartered banks. The model of "fintech with a banking license" is growing three times faster than pure PSP fintech (according to the Central Bank of Brazil 2024 data). In Mexico, just having an IFPE license is no longer enough; due to cost considerations, leading players are vying for SOFOM or full banking licenses.

5. "Latin America" is not a single market

Most companies hire a Brazilian to do "Latin America BD" or community management. This is a mistake.

The Argentine market is substantial, with real transaction volume. Moreover, due to historical, cultural, and football rivalries, Argentinians and Brazilians actually don't get along very well, sometimes calling each other "monkeys" (both ways). Each country has its own currency logic, informal economic models, diaspora groups, and histories of foreign exchange controls.

If you can't distinguish between Argentina's foreign exchange controls, Brazil's parallel exchange rates, and Mexico's freely floating pesos, you can't do payments in Latin America.

Notable data: Argentina has a population of only 46 million but over 5 million crypto users (about 11% penetration, one of the highest in the world). Argentina's parallel foreign exchange market ("blue dollar") creates a fundamentally different demand for stablecoins compared to Brazil.

Mexico's remittance flow (about $65 billion annually) is the second largest in the world but is currently being squeezed by the 1% remittance tax from the US (passed in summer 2025) and the Mexican central bank tightening the supply of US dollars.

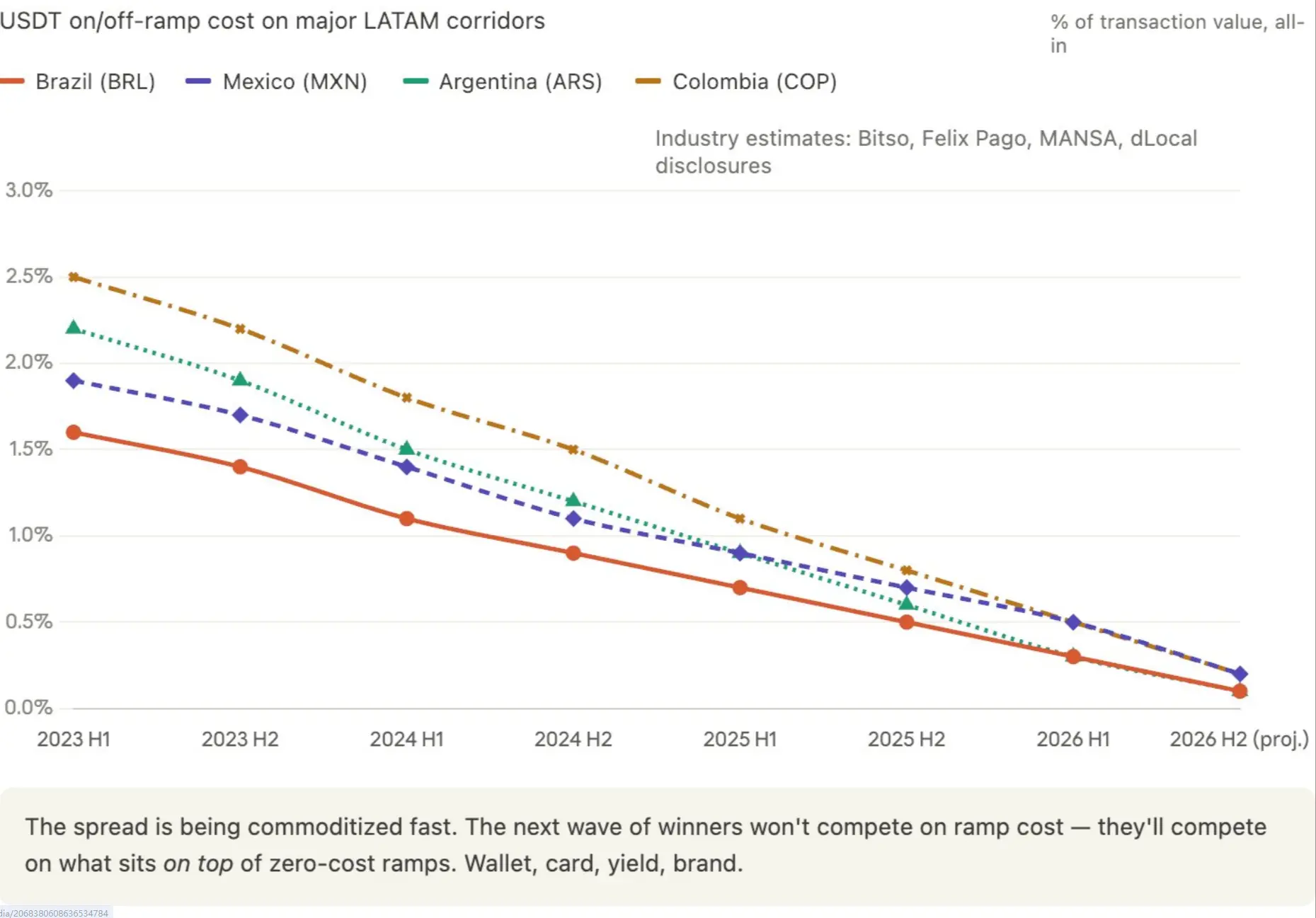

6. New banks are turning to foreign exchange

The stablecoin conference held in Mexico City this year was essentially a remittance and foreign exchange conference. Money from different countries is flowing across borders, and this flow is being commoditized, turning into a price war.

Profit margins are approaching zero. My prediction is that within the next 6 to 12 months, the exchange cost between USD and USDT will drop to zero along major corridors in Latin America. Companies that hope to profit from interest rate spreads will find themselves squeezed by infrastructure players who treat exchanges as a loss leader to drive larger products.

From July 2023 to June 2024, the transaction volume of stablecoins in Latin America is about $415 billion (according to Chainalysis), with approximately 71% of Latin American institutions using stablecoins for cross-border payments (according to Fireblocks 2025 data).

The cost of cross-border stablecoin transfers has dropped from 1.5% to 2% in 2023 to 0.3% to 0.8% in 2025. Cost compression is accelerating, with Bitso, Felix Pago, and a dozen smaller players racing to drive the spread to zero.

7. Cross-border expansion is the new direction

The classic payment advice is: choose a remittance corridor and master it. Build relationships, obtain licenses, lock in merchants, and become the default option.

This advice is becoming obsolete. Venture capitalists now tell me that payments have become difficult to invest in due to excessive localization. Every company is deeply rooted in one country, taking local profits, but then can't expand out. They become kings of a corridor but cannot be invested in as a cross-regional brand.

The next generation of payment companies needs to have brand recognition internationally from day one, and their tech stack must be able to scale across borders. This represents a generational shift in fintech regarding what constitutes "good."

Stripe's valuation of over $90 billion comes from cross-corridor expansion, not just depth within a single corridor.

Nubank's expansion into Mexico, Colombia, and now targeting Argentina has unlocked its valuation through this multi-country strategy, not just its deepening in Brazil.

DollarAPP has also recently begun entering the Brazilian market. Between 2024 and 2025, most of the financing in Latin American fintech that has seen valuation downgrades from venture capital has been poured into companies that only operate in a single country.

8. Brazil and Mexico are already a red ocean

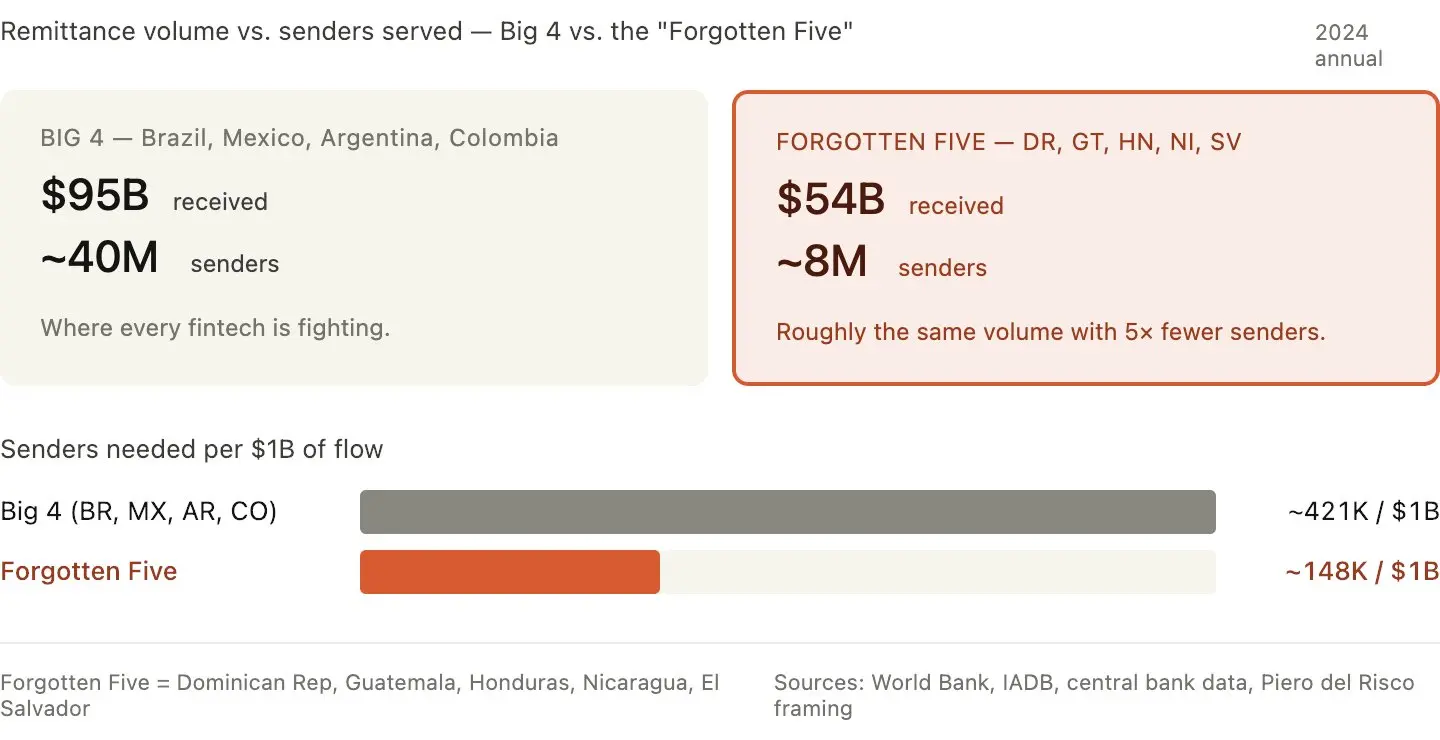

I discussed the "forgotten five countries" with Piero del Risco.

"Think about it: the Dominican Republic, Guatemala, Honduras, Nicaragua, and El Salvador together receive about $60 billion in remittances, which is roughly equal to the total of Brazil, Mexico, Argentina, and other major markets. But there are only 8 million remittance senders serving these 'forgotten five countries,' while there are 40 million serving the larger markets. We move upstream in the US as project managers, thus creating a regulatory moat, providing banking services to remittance senders at the top of the funnel, while mastering the payment tracks in each country downstream."

It's not just these five countries; there are a few other small nations with a small but concentrated group of remittance senders that receive as much money as the entire "big" market. Everyone is fighting over Brazil and Mexico, but almost no one is seriously building infrastructure for Guatemala or Honduras. The competition density here is five times lower for the same transaction volume.

There are also a few overlooked corridors I am keeping an eye on:

Colombia → Europe (Spain, Italy, Netherlands)

Argentina → Bolivia (small scale but extremely concentrated)

Venezuela → Colombia (the largest non-US Latin American corridor)

Guatemala is expected to receive $20.3 billion in remittances in 2024 (15% of GDP). Other countries: Honduras $9.7 billion, El Salvador $8.6 billion, Nicaragua $4.8 billion, Dominican Republic $10.2 billion. The total is $53.6 billion, accounting for about 33% of all remittances in Latin America. Their combined population is less than a quarter of Brazil and Mexico, yet there is almost no fintech competition.

The cost of each remittance in the "forgotten five countries" is also higher (6.5% to 8%, while the Latin American average is 6%), meaning there is more profit margin to capture.

9. Marketing budgets should be spent in the right places

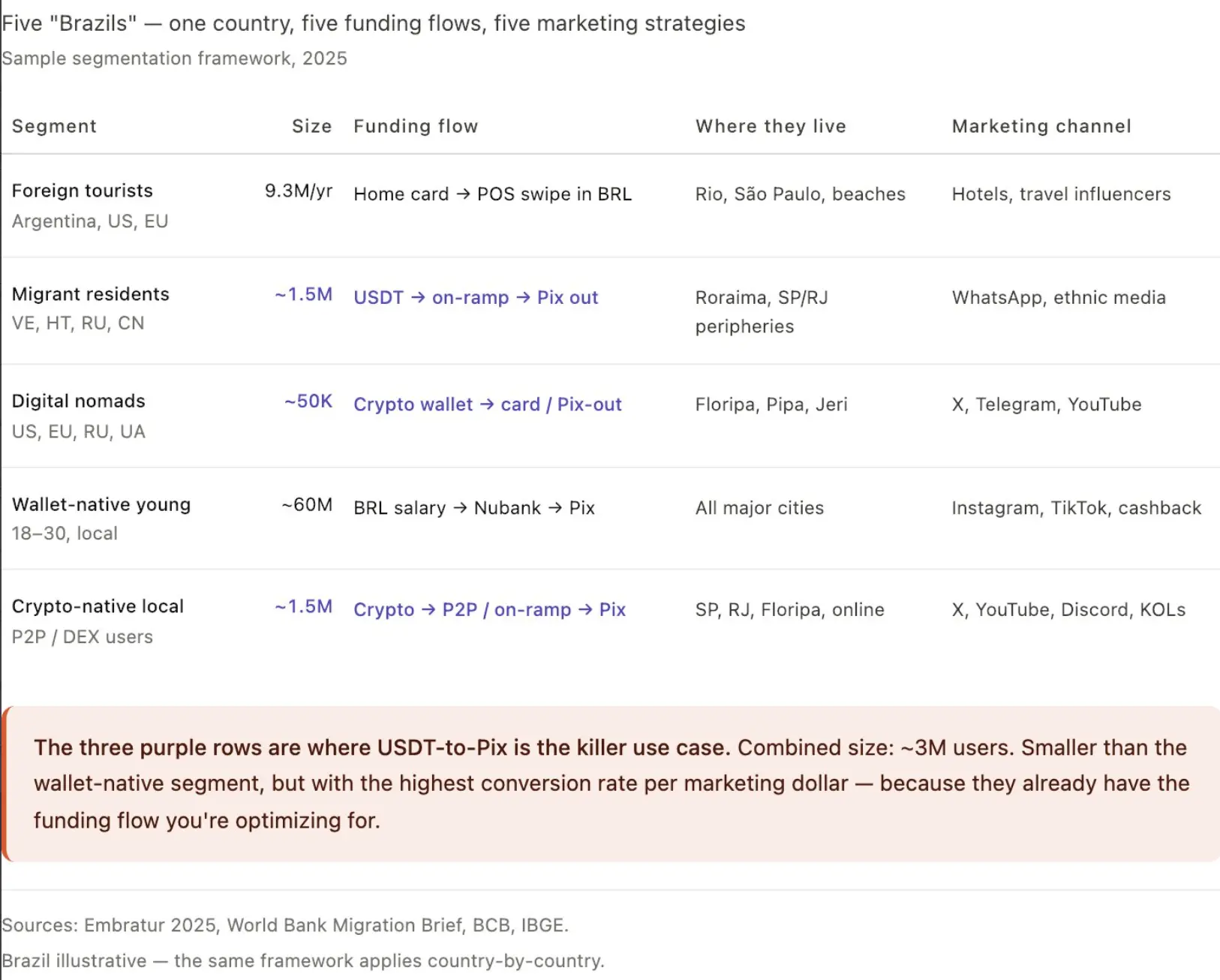

Take Brazil as an example.

Every fintech company promoting "Brazil" treats it as a single user group. It is not. This country has at least five different funding flow segments, each corresponding to different products, messaging, and payment tracks. If you can't sketch out the funding flows of your users on a napkin, you are wasting your marketing budget on the wrong people.

Here are the five segments I sketched out in the field:

Segment 1: Foreign tourists. In 2025, there will be 9.3 million, with total spending of $7.9 billion (about $847 per person).

Main sources: 3.4 million from Argentina (price-sensitive, love the beach), 800,000 from Chile (high value), 760,000 from the US (high spending), followed by Paraguay, Uruguay, France, Portugal, and Germany.

Their funding flow is: home country debit or credit card → swipe at POS in Brazil. They never directly handle BRL.

Effective marketing entry points: airport transfers, comparing foreign exchange savings with their home banks, and one-click payments at attractions with no fees.

Segment 2: Long-term foreign residents without Brazilian bank accounts. Venezuelans (79% of Brazil's immigrant population), Haitians, Bolivians, Russians, Chinese, and Syrians, totaling about 1.5 million immigrants. Among them, 62% are already using digital wallets instead of traditional accounts.

Their funding flow is: international USDT or USD income → exchange → Pix transfer out for BRL consumption. This is the highest value group for native stablecoin products, with USDT to Pix being their killer use case. Zero education cost, direct conversion.

Segment 3: Digital nomads. Concentrated in Florianópolis, Rio, São Paulo, Pipa, and Jericoacoara. Mainly Americans, Europeans, Russians, and Ukrainians. Their income comes from abroad, usually in USDT or BTC. They refuse to open Brazilian bank accounts due to bureaucratic hassles.

Funding flow: crypto wallet → swipe or Pix transfer out for rent, restaurants, Uber, phone bills. They are not sensitive to foreign exchange prices but are extremely sensitive to experience. As long as the operation can be simplified, they will switch service providers.

Segment 4: Young digital wallet natives in Brazil. They have "accounts," but they are with Nubank, Mercado Pago, PicPay, RecargaPay, not Itaú or Bradesco. They don't see themselves as bank customers but as app users.

Funding flow: BRL salary → digital wallet → used everywhere with Pix. Crypto exposure is increasing, but core processes are fully localized. Marketing entry points are: cashback, earnings, convenience, rather than "stablecoin tracks."

Segment 5: Crypto-native Brazilians. Holding USDT or BTC, often using P2P. Funding flow: crypto balance → P2P or exchange → Pix → consumption. Brazil has over 1.5 million active crypto users. This is the easiest group to convert, but also the smallest.

Most fintechs make a mistake here: they create one product, run one marketing campaign, and target the entire "Brazil." As a result, customer acquisition costs are absurdly high because segments 1, 2, 3, 4, and 5 require completely different customer acquisition channels, completely different messaging, and completely different funding tracks.

A Russian YouTube ad targeting digital nomads in Florianópolis and a Portuguese Instagram ad targeting young Brazilians in São Paulo have vastly different conversion rates. WhatsApp groups for Venezuelan immigrants in Roraima perform completely differently from collaborations with American travel influencers targeting tourists.

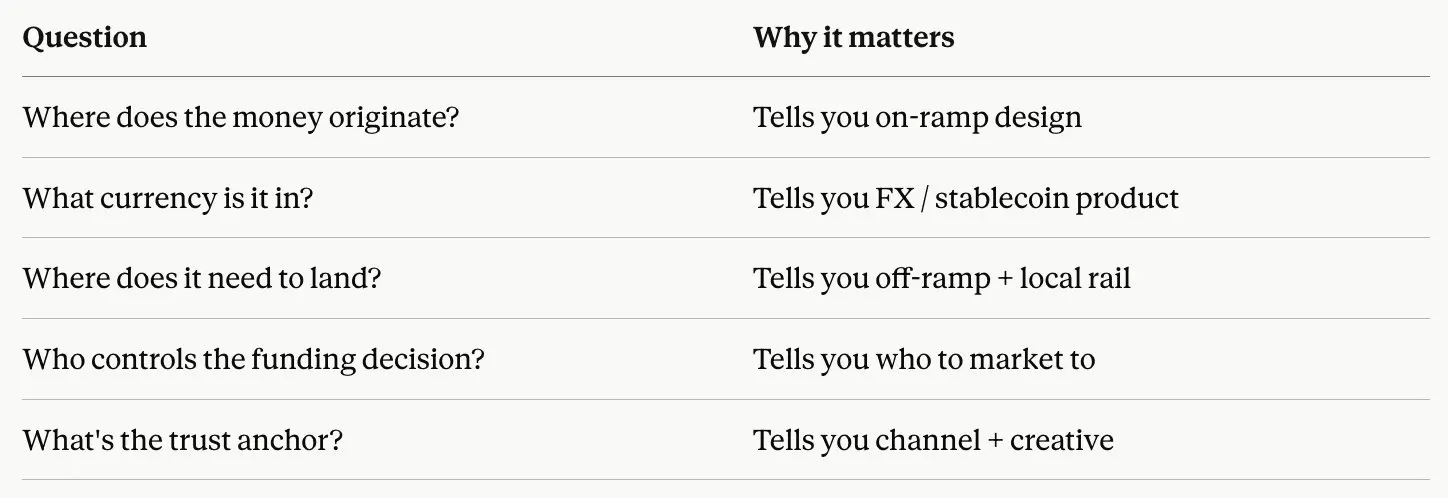

After sketching out these groups, the framework I would use in any Latin American country is:

If you can't answer these five questions for each priority group, you are not ready to spend your marketing budget. What you should do is more user research.

The same logic applies to every Latin American country.

The example of Brazil can be directly applied to Mexico (remittance senders from the US, Mexican professionals, cross-border SMEs between the US and Mexico, crypto-native youth, rural populations without bank accounts), and it can also be applied to Argentina (blue dollar holders, professionals with dollarized salaries, crypto-native traders, MercadoPago users, tourism arbitrageurs), as well as every market in the region.

Don't ask, "Should I enter Brazil?"

Ask, "Which of these five Brazils am I targeting?"

This is the only question that can turn Latin American expansion into an investment-worthy endeavor rather than a bottomless pit.

10. In terms of regulation, Latin America is five years ahead of the US

Throughout the journey, I spoke with over 10 regulators. The biggest surprise was their lack of concern about stablecoins, P2P tracks, and the interchange between crypto and fiat.

The Western narrative about Latin American regulation is "fragmented, slow, and backward." But in the field, the situation is quite the opposite. The US is lagging behind.

Brazil. The Central Bank developed Pix in 18 months and made it free on the payment side, something the Federal Reserve is still studying. The regulatory framework for crypto is now set: resolutions 519, 520, and 521 will be published in November 2025 and will take effect on February 2, 2026. The hard deadline for existing Virtual Asset Service Providers (VASP) to apply for authorization is October 30, 2026.

After that, every institution regulated by the Central Bank of Brazil, including every Brazilian bank, every payment processor, and every Pix service provider, will be prohibited from conducting virtual asset business with unlicensed counterparties. Read that sentence again.

This deadline is not "you need a license," but "if you don't have a license, every Brazilian bank that partners with you is legally required to cut ties with you." As of the time of writing, there are only about four months left.

Mexico. Mexico passed the Fintech Law in 2018, while the US still does not have a federal fintech law by 2026. The IFPE and remittance license framework from the Central Bank of Mexico is specifically designed for cross-border digital fund flows. The US just passed a 1% federal remittance tax in summer 2025 (the "Big and Beautiful Act"). Mexican regulators noticed this earlier than US fintech practitioners. Several told me they are adjusting their licensing strategies to accommodate funds that will bypass US cash channels.

Colombia. The Financial Superintendence approved Bancolombia's COPW peso stablecoin in 2024, which is an end-to-end regulated commercial bank stablecoin. The Federal Reserve has yet to approve any US bank stablecoin.

Argentina. Although the Central Bank prohibited banks from dealing with crypto in 2022, the new VASP licensing sandbox (launching in 2025) is more lenient than New York's BitLicense. Argentine regulators directly told me: "We can't stop dollarization; we can only make it safer." This level of candor is something most US regulators would not exhibit in public.

Costa Rica and Paraguay. Both countries are running stablecoin remittance sandboxes, and their licensing paths are clearer than those of over 30 US states.

What surprised me the most about this part is that Latin American regulators do not want to slow down the adoption of stablecoins. Several proactively asked me, "How can we make it safer for citizens?" rather than asking, "How can we stop it?"

This is not a regulatory environment that is "behind" the US. This is a regulatory environment that is ahead of the US; they have moved past the existential debate that the US is still entangled in.

If you are doing cross-border business in Latin America and are still waiting for "regulatory clarity," then you have misread the situation. Clarity has long been established.

What is vague is the end of the corridor on the US side.

In fact, most of these views contradict my understanding before the trip.

The most impactful for me was point 6; I thought stablecoins were a structurally high-profit business when I went to Latin America. The reality I saw on the ground, however, is that they are competing to reach zero.

The winner will not be the one that does the best in exchange channels, but the one that excels in the next layer (wallets, cards, earnings, branding) above the exchange.

To every taxi driver, bartender, bank manager, and regulator willing to take the time to explain things to a foreigner with poor Spanish and worse Portuguese.

The wheel on my suitcase will eventually be fixed.

But the lessons learned on this trip will not be worn down.

Risk warning

Risk warning