SignalPlus Macro Analysis: Strong U.S. Economic Data Drives Broad Stock Market Rally

Yesterday was a trading day with better risk sentiment across various asset classes. Concerns about regional banks and commercial real estate drove safe-haven buying in bonds, while strong U.S. economic data, the influx of capital at the beginning of the month, buying on dips after the FOMC meeting, and strong earnings results from Meta and Amazon collectively pushed the stock market higher.

Yesterday was a trading day with better risk sentiment across various asset classes. Concerns about regional banks and commercial real estate drove safe-haven buying in bonds, while strong U.S. economic data, the influx of capital at the beginning of the month, buying on dips after the FOMC meeting, and strong earnings results from Meta and Amazon collectively pushed the stock market higher.

Yesterday was a trading day with better risk sentiment across various asset classes. Concerns over regional banks and commercial real estate drove safe-haven buying in bonds, while strong U.S. economic data, early-month capital inflows, buying on dips after the FOMC meeting, and robust earnings results from Meta and Amazon collectively pushed the stock market higher.

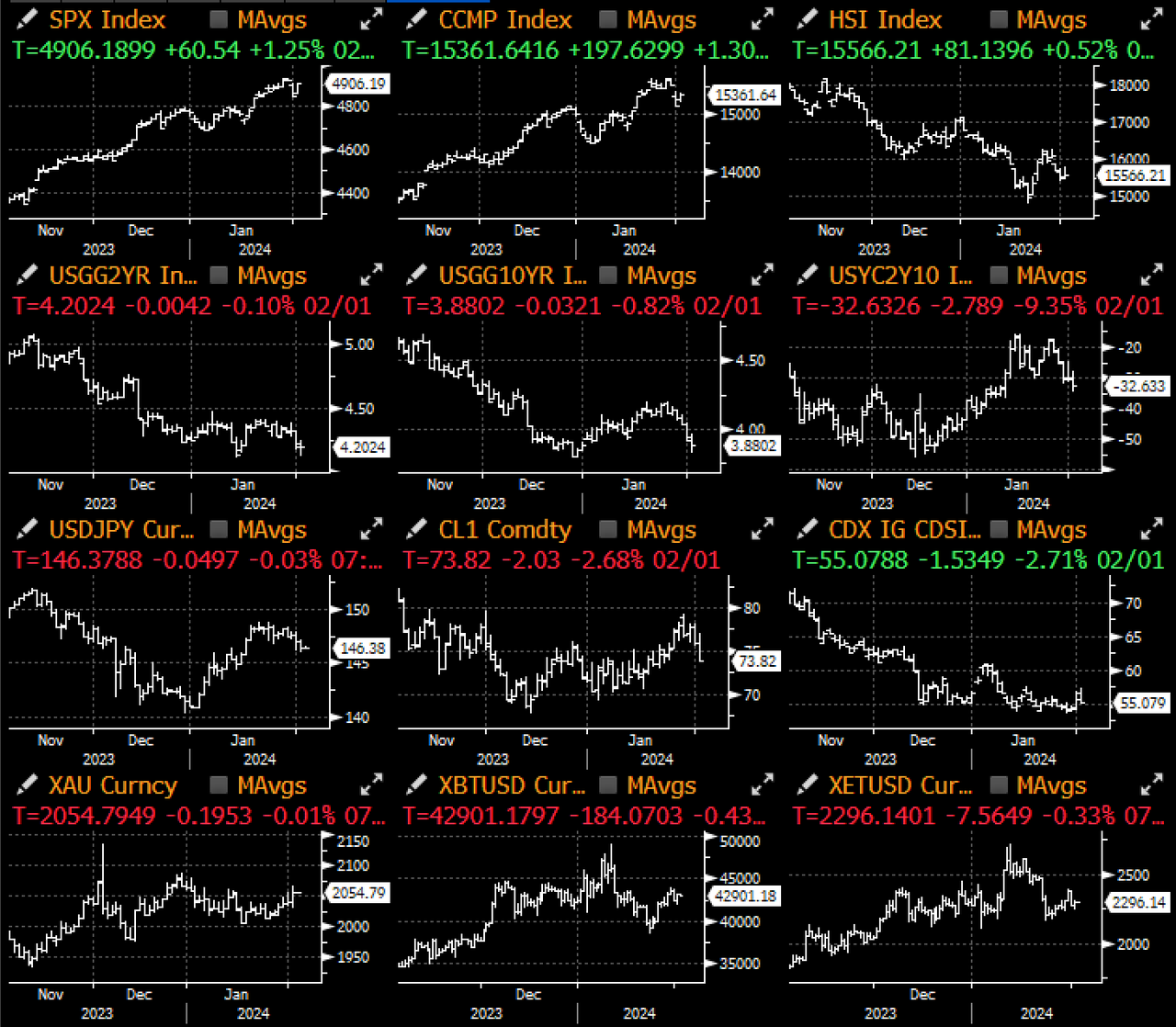

First, in the interest rate market, to address the tail risks of the regional banking crisis further spreading, there was decent buying in fixed income. Long-term rates fell 10 basis points from their peak after the FOMC meeting, with the 30-year yield currently at its lowest level this year (4.06%), while the 10-year yield is rapidly approaching the trendline support at 3.80%.

A Japanese bank reported losses due to U.S. real estate, causing some regional bank stocks to drop 7% in early trading. Meanwhile, Deutsche Bank also raised its loss reserves for U.S. commercial real estate by nearly five times, reaching about $133 million. We provide more analysis on the commercial real estate market in our "SignalPlus 2024 Macro Outlook," which interested readers should definitely check out.

On the other hand, the U.S. economy continues to remain stable, with the ISM Manufacturing Index performing strongly due to a significant jump in new orders (52.5 vs 47) and prices paid (52.9 vs 45.2), the former being the best performance since May 2022. Additionally, the Atlanta Fed's GDPNow model raised its first-quarter GDP forecast from 3.0% to 4.2% (!), while initial jobless claims also declined, providing a perfect combination of economic data that drove both bonds and stocks higher.

Non-farm payroll data will be released today, and investment banks predict that the results may exceed expectations. Citigroup's report indicates that weekly jobless claims in January were generally low, suggesting that employment data may perform strongly, while wage growth could also exceed the 2% inflation target. However, unless both of these data points significantly exceed market expectations, they are unlikely to have a major impact on market prices.

Risk warning Risk warning

Risk warning Risk warning