SignalPlus Macro Analysis (20240423): The US Stock Market Awaits Corporate Earnings Data

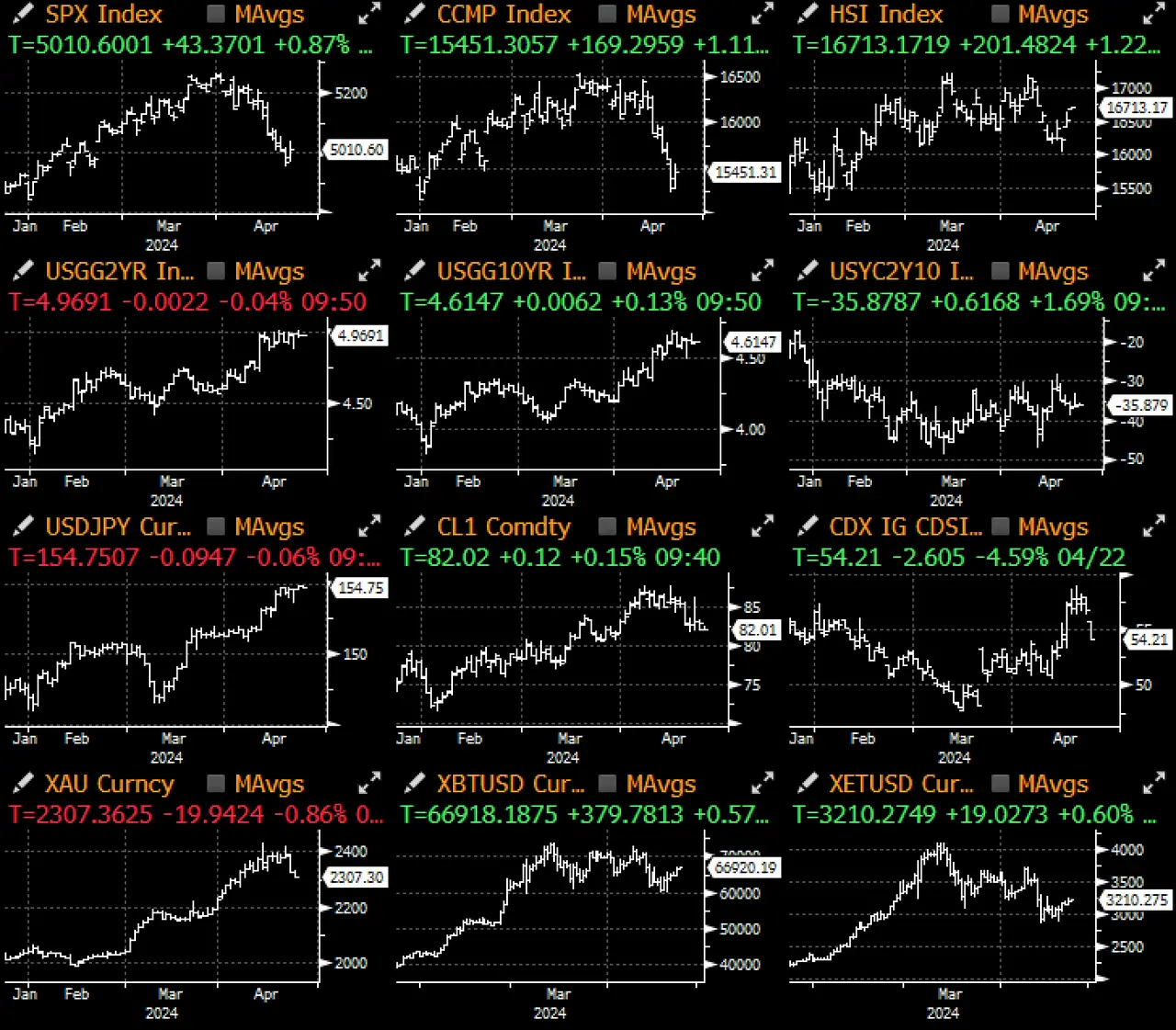

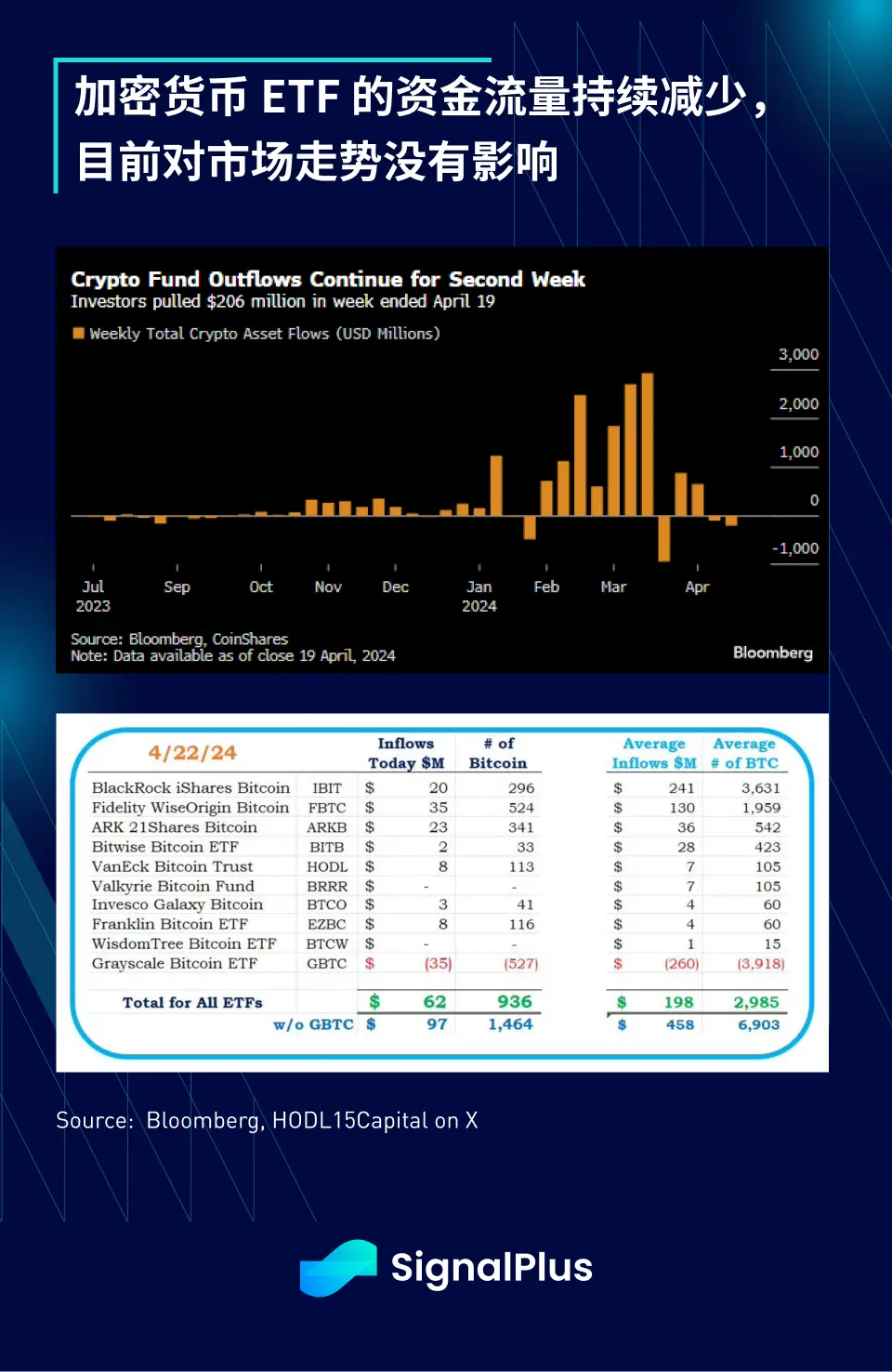

The geopolitical situation did not escalate further over the weekend, and the oversold positions led to a risk rebound, with the risk market rising across the board yesterday. In terms of cryptocurrency, based on CME futures contracts, JPM believes that BTC positions are also overweight, while ETFs have seen outflows for two consecutive weeks (albeit on a small scale).

The geopolitical situation did not escalate further over the weekend, and the oversold positions led to a risk rebound, with the risk market rising across the board yesterday. In terms of cryptocurrency, based on CME futures contracts, JPM believes that BTC positions are also overweight, while ETFs have seen outflows for two consecutive weeks (albeit on a small scale).

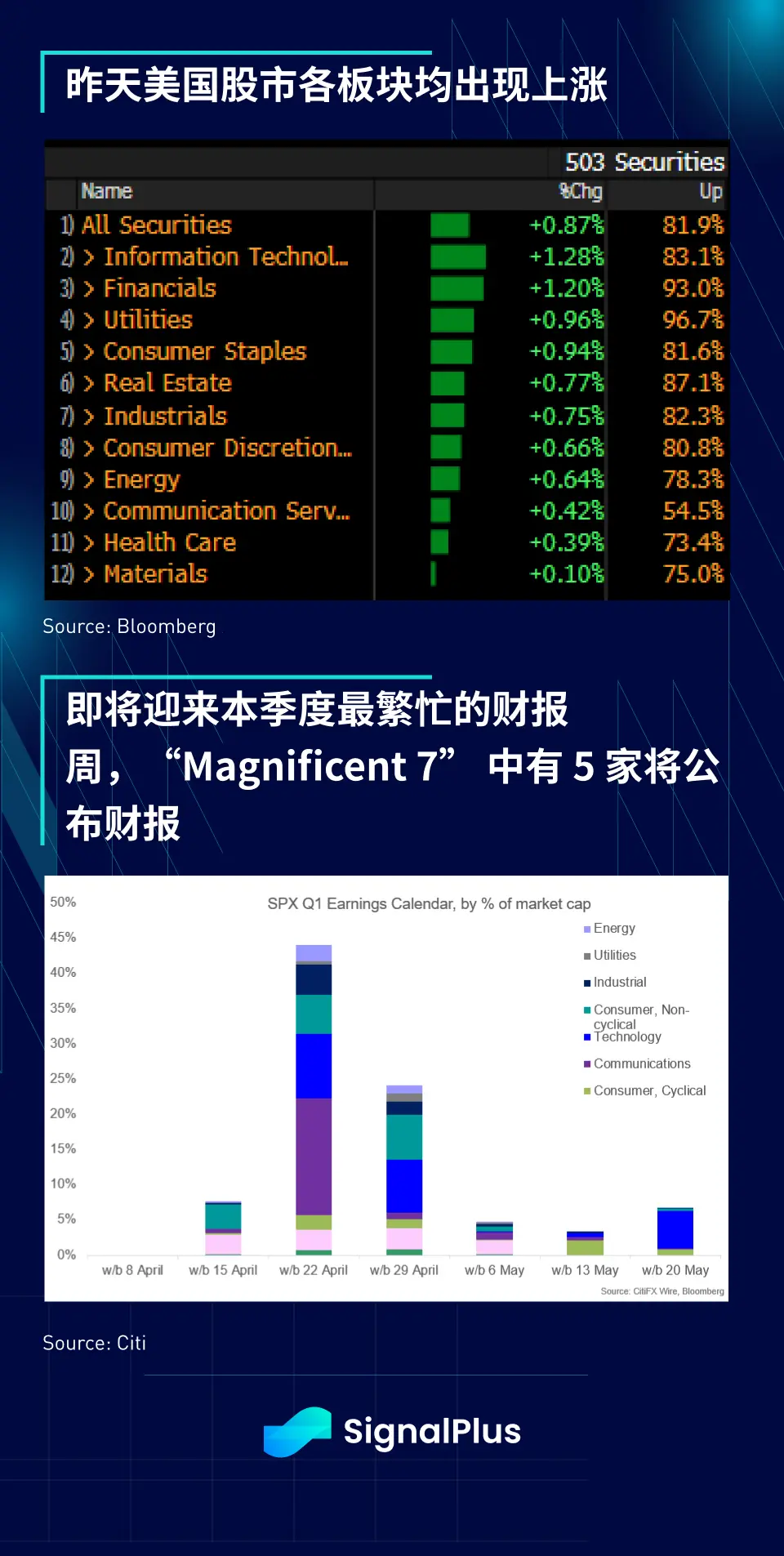

The geopolitical situation did not escalate further over the weekend, while oversold positions brought about a risk rebound, leading to a broad rise in risk markets yesterday. Ahead of Friday's PCE data, the FOMC meeting in eight days, and the busiest earnings week for SPX this quarter, fixed income investors seem to have chosen to adopt a wait-and-see attitude. Despite positive price movements, trading activity remained relatively light, with fixed income trading volume at only 60-70% of normal levels. 44% of SPX companies will announce earnings this week, including 5 from the "Magnificent 7," with Tesla reporting on Tuesday, Meta on Wednesday, and MSFT, Google, and Amazon scheduled for Thursday.

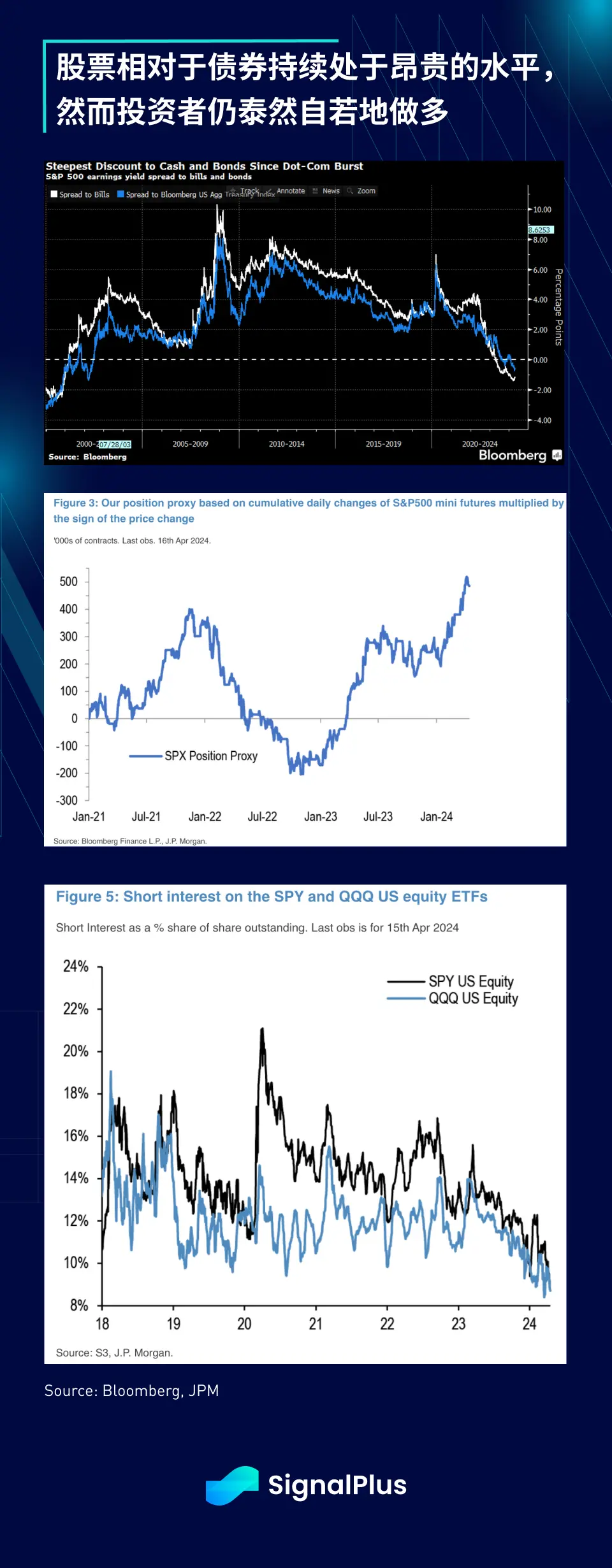

With last week's bond sell-off, stocks remain at a historically expensive level relative to fixed income (based on implied yields). Nevertheless, Wall Street believes that investors still feel comfortable going long, with long position indicators reaching a four-year high, while the short ratio for SPX/Nasdaq will hit a nearly ten-year low.

However, last week's negative price movements have caused some technical damage to stocks, with SPX futures breaking below the 55-day moving average and more than 5% away from the next 200-day moving average support level. From a weekly perspective, the slow stochastic indicator has turned negative and is accelerating downward, while the SPX monthly candlestick may form a bearish engulfing pattern at record highs, warranting caution during earnings season.

In the cryptocurrency space, based on CME futures contracts, JPM believes that BTC positions are also overly heavy, while ETFs have seen outflows for two consecutive weeks (albeit on a small scale), with mainstream momentum clearly weakening. On Monday, inflows slightly rebounded to +$62 million, but had no impact on the market; we will continue to closely monitor market developments.

Risk warning Risk warning

Risk warning Risk warning

Popular articles