SignalPlus Macro Analysis Special Edition: Glass Half Full?

Both China and the United States are continuing to take steps towards restarting trade negotiations and easing relations. Recently, both sides have made adjustments to their trade departments and negotiators. The Chinese side stated, "The U.S. side has recently actively conveyed messages to us through relevant channels, hoping to engage in talks with us." In response, the Chinese side said, "We are currently conducting an assessment."

Both China and the United States are continuing to take steps towards restarting trade negotiations and easing relations. Recently, both sides have made adjustments to their trade departments and negotiators. The Chinese side stated, "The U.S. side has recently actively conveyed messages to us through relevant channels, hoping to engage in talks with us." In response, the Chinese side said, "We are currently conducting an assessment."

Due to a softening of the U.S. government's tough trade policy rhetoric, the SPX index ended last week with its first nine consecutive gains in over 20 years, recovering all losses since the Liberation Day crash.

Both China and the U.S. are continuing to take steps towards restarting trade negotiations and easing relations. Recently, both sides have made adjustments to their trade departments and negotiators. The Chinese side stated, "The U.S. has recently conveyed messages to us multiple times through relevant channels, hoping to talk with us." In response, the Chinese side indicated that "an evaluation is underway."

A recent Bloomberg survey shows that the market generally believes the Trump administration will ultimately respond to market changes, despite previously attempting to blame issues on Biden's legacy. The market believes the government has reached a "pain threshold" where it is willing to pause its tariff offensive.

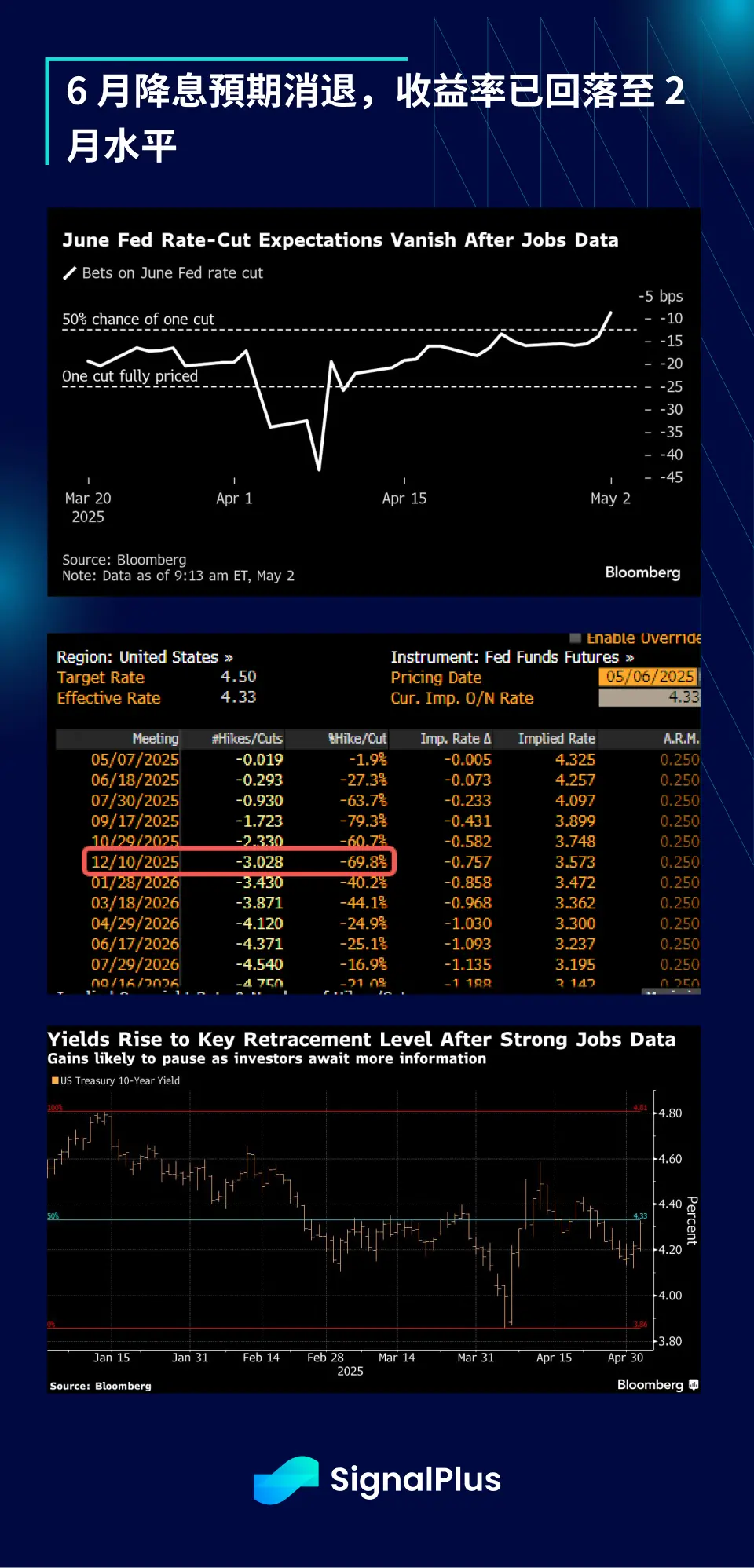

In addition to positive signals on trade, the non-farm payroll report released last Friday was unexpectedly strong, further boosting market risk appetite and concluding a week of robust economic data, indicating that despite negative sentiment in the market, the fundamentals of the U.S. economy remain solid. In April, 177,000 new jobs were added, and the unemployment rate held steady at 4.2%, temporarily alleviating concerns about an impending economic recession. However, the true impact of tariff policies may not be reflected until the data for May and June is available.

Furthermore, based on the average drawdown levels during past economic slowdowns, the implied probability of a recession from the current stock market rebound is only about 8%, significantly lower than estimates from economists or levels implied by the fixed income market.

In the fixed income market, the yield curve has flattened and has returned to levels seen in February, with the market expecting only about a 30% chance of a rate cut in June, and only about three rate cuts expected for the entire year.

On the other hand, recent actual inflation data has continued to decline, coupled with positive signals from multiple central banks regarding maintaining U.S. Treasury positions, restoring normalcy to the U.S. bond market.

In the cryptocurrency space, overall volatility has been low over the past week, with prices remaining flat. Although BTC briefly recovered to the 96k level, it subsequently faced short-term profit-taking pressure. The volatility curve has flattened, indicating a lack of clear direction in the market, while actual volatility has fallen to a year-to-date low.

If there are no significant macro asset movements, we expect cryptocurrency prices to continue consolidating in the short term, with a potential bias towards bullishness in the medium term.

Over the past two weeks, although the scale has been small, ETF inflows have continued to be positive, with cumulative net inflows nearly exceeding the early highs of the first quarter.

Looking ahead, with the SPX successfully recovering losses after Liberation Day, the "easy" part of the rebound has been achieved, and prices have re-entered a technical resistance area. Historically, "bear market" rebounds (if this counts as one) are the most unstable and irrational for observers. However, this rapid rebound has also triggered some positive divergence signals, which may push prices back to January's highs.

We expect this week's FOMC meeting will not have a significant impact on the market, and there is currently no clear directional judgment; price movements may be as unpredictable as flipping a coin. Ultimately, it will return to the performance of corporate profit growth, which will further depend on economic realities and the subsequent impact of tariffs.

So far, the situation looks good, with first-quarter profit growth expected to approach a year-on-year increase of 13%, nearly double the expectations at the beginning of the earnings season, and it will be the second consecutive quarter of double-digit growth.

If a choice must be made, we believe the market's "pain trade" still leans towards further price increases, as most observers remain fixated on the notion that tariffs are "a done deal, irreversible." However, it is important to note that the "dead cat bounce" in a bear market should not be underestimated!

Risk warning Risk warning

Risk warning Risk warning