A Review of the History of Chinese Cryptocurrency Exchanges: Rise of the Underdogs, Offshore Migration, and Compliance Reshaping

Fifteen years of tumultuous changes, a deep review of the grand evolution of Chinese cryptocurrency exchanges from their grassroots rise, the competition among giants, to global compliance, helping you understand the ups and downs of the big players and the curtain call of the industry.

Fifteen years of tumultuous changes, a deep review of the grand evolution of Chinese cryptocurrency exchanges from their grassroots rise, the competition among giants, to global compliance, helping you understand the ups and downs of the big players and the curtain call of the industry.Author: Black Mario

01 The Wilderness Begins

In the rainy season of 2011 in Shanghai, the humidity and heat were suffocating. In a less than 20 square meter residential building in Jing'an District, there wasn't even a decent sign. Two chipped computer desks and a second-hand printer were all that constituted the possessions of China's earliest cryptocurrency exchange.

Yang Linke stared at the flickering characters on the screen with a cigarette in his mouth, while Huang Xiaoyu finished the last line of matching code. These two young men, who had struggled on the fringes of the internet, had no idea that they were pushing open a door that would sweep across the globe.

At that time in China, no one took Bitcoin seriously as a business. This string of virtual code from overseas was hidden in the corners of geek forums. The story of China's cryptocurrency exchanges quietly began with these two young men, who were completely different in identity and personality.

Yang Linke was a native of Wenzhou, born in 1985. He had never followed the usual path of education. He dropped out of school in his teens to venture out, working as a network administrator in internet cafes in Wenzhou and Shanghai, surrounded by the smell of smoke, fixing machines, troubleshooting, and watching players game—this was his most authentic youth. Later, he traded virtual items and built small websites. He didn't make a lot of money, but he developed an eye for niche demands.

He didn't understand cryptography and had never been in touch with the overseas geek circle. When he first saw "Bitcoin" on a tech forum in 2010, he quickly realized that it was a virtual token that could be transferred online without any control. A simple thought popped into his mind: if someone plays, someone wants to buy and sell; if there are transactions, there must be a place to facilitate them.

At that time, there were very few over-the-counter Bitcoin transactions in China. Buyers and sellers posted on forums, transferred money privately, and manually transferred coins, which was cumbersome and dangerous, resembling the way people exchanged goods on the street before there were markets. Yang Linke saw this untouched gap, but he had no technology and no team; all he could do was find someone who could code to partner with.

The person he found was Huang Xiaoyu.

Unlike the grassroots Yang Linke, Huang Xiaoyu was a well-known tech geek in the circle, having delved into programming for many years, specializing in website development and backend construction. He was also among the first in China to understand the underlying logic of Bitcoin. He was introverted, not fond of being in the spotlight, and was obsessed with code and decentralized technology. When Yang Linke found him on the forum and bluntly said, "I'll handle operations, you write code, let's create a Bitcoin trading website together," Huang Xiaoyu agreed without hesitation.

Perhaps it was not for the sake of making big money, but for the geek's obsession that such a pioneering thing needed a trading platform of its own in China.

The two pooled together tens of thousands of yuan in startup capital, rented this residential office, had no investors, no formal employees, and no compliance procedures. During the day, they wrote code and adjusted pages, and at night, they went to forums to attract traffic, eating instant noodles when hungry and sleeping on the desk when tired. In June 2011, Bitcoin China (BTCC) officially launched, becoming China's first cryptocurrency exchange and one of the earliest trading platforms in the world.

The early BTCC website was extremely rudimentary, featuring only the simplest buy and sell orders and price curves, without even candlestick charts, allowing only Bitcoin trading. Deposits and withdrawals relied entirely on manual processes; users transferred money to Yang Linke's personal bank account, and he manually verified before adding coins for users. Withdrawals were similarly handled, with Huang Xiaoyu manually transferring coins one by one.

The first batch of users numbered only a few hundred, all programmers, geeks, and overseas students, with daily trading volumes barely reaching tens of thousands. Yang Linke later recalled that at that time, they never thought about making money; they just felt they were doing something very cool, like building the first small road in a wilderness.

Two ordinary people, one daring to dream and the other daring to act, set up the first tent of China's exchange in the wilderness.

However, this grassroots geek site remained lukewarm for two whole years after its launch, never breaking out of its small circle. Until 2013, an elite from overseas entered the scene and completely changed BTCC's fate; his name was Li Qiyuan.

Li Qiyuan's life was a world apart from Yang Linke and Huang Xiaoyu.

He studied in the United States in his early years, graduated from Stanford University, and worked in Silicon Valley tech companies and Wall Street institutions. He was familiar with overseas financial markets, media operations, and business strategies, and was a staunch believer in Bitcoin, being one of the first to introduce Bitcoin into the Chinese business circle.

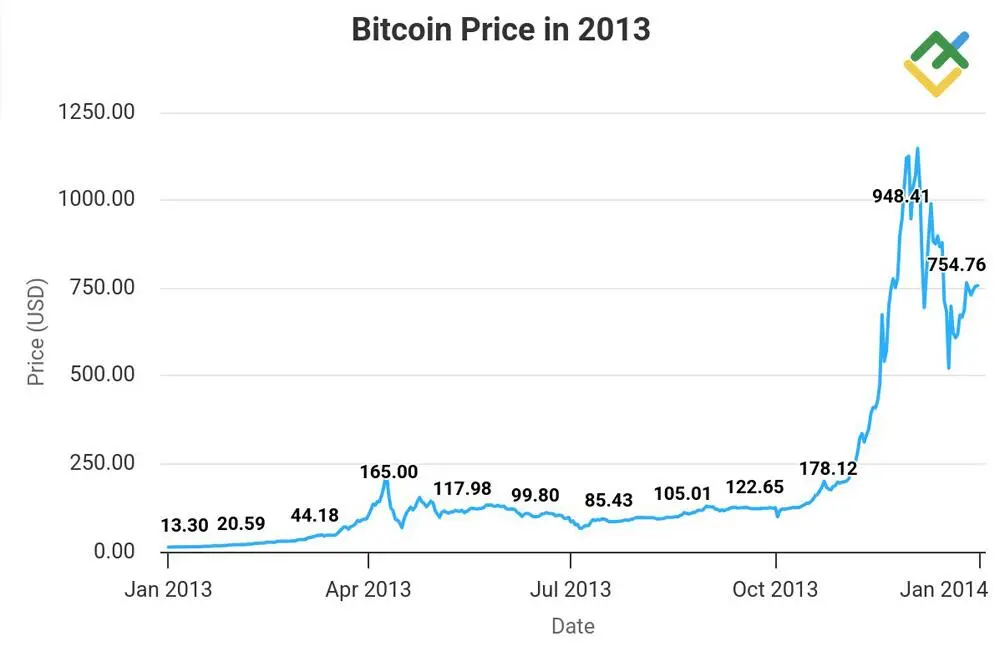

In 2013, the price of Bitcoin skyrocketed from $13 at the beginning of the year to $1,100 by the end, and the first wave of the global bull market swept in, completely unleashing demand in the Chinese market. BTCC's grassroots model could no longer support the influx of users. Li Qiyuan quickly recognized BTCC's first-mover advantage and decisively joined to lead operations, igniting a fire that turned this geeky little website into an industry benchmark.

He first ended the residential workshop model, registered a formal company, and built a complete team for technology, operations, and customer service. He also engaged domestic and foreign financial media to bring Bitcoin and BTCC into the public eye, striving to let ordinary people know about Bitcoin and Bitcoin trading. At the same time, he optimized the deposit and withdrawal processes, improved system stability, and initially established security mechanisms to accommodate the explosive growth of users.

In 2013, BTCC reached its peak, with daily trading volumes exceeding 100 million yuan, and the user base surged, becoming the most influential exchange in China and even globally. The original iron triangle of Yang Linke, Huang Xiaoyu, and Li Qiyuan firmly established their position as pioneers of Chinese exchanges.

That period was the absolute wilderness era for Chinese cryptocurrency exchanges. There were no regulatory policies, no industry standards, no risk control requirements, and no formal payment channels. User assets were all in the founders' private accounts.

These wild years completed the industry's most essential primitive accumulation:

BTCC proved that the early business model of matching RMB + Bitcoin was feasible, expanding users from the geek circle to ordinary investors, and provided the most intuitive entrepreneurial model for later entrants.

Of course, the wild revelry eventually welcomed the first alarm bell.

In December 2013, the central bank and five ministries jointly issued a notice on "Preventing Bitcoin Risks," clearly stating for the first time that Bitcoin is not currency but a virtual commodity, while also drawing a red line prohibiting financial institutions and payment institutions from participating in related businesses, directly pointing out the fatal risks of exchanges: unregistered, poor security, vulnerable to attacks, and operators might abscond with funds.

Although this notice did not shut down exchanges, it put the first reins on the wildly growing industry.

Yang Linke understood in his heart that the days of relying on grassroots workshops and gray areas were coming to an end. Little did he know that a battle for industry dominance was already on the horizon.

In the winter of 2013, BTCC moved out of the residential building and into a formal office building. At the moment the logo lit up, the three pioneers stood by the window, their eyes filled with light.

They transformed from internet café administrators, tech geeks, and overseas elites into the first generation of founders of Chinese exchanges, completing the first step from 0 to 1 in the most straightforward way. However, they did not anticipate that soon two more radical entrepreneurs would break the pattern they had established and push Chinese exchanges to the pinnacle of the world.

Li Lin and Xu Mingxing were already sharpening their fists not far away.

02 The Rise of the Three Giants and China's Power Dominates the World

In the same year of 2013, the lights in the entrepreneurial café of Zhongguancun, Beijing, shone until late at night.

Li Lin stared at the Bitcoin candlestick chart on his computer, having just emerged from a failed group buying venture, he sensed an unprecedented opportunity. Meanwhile, a few streets away, Xu Mingxing was tapping away at code, this tech geek proficient in high-frequency trading systems was building his own trading engine.

Two young men with completely different backgrounds, ideas, and strategies focused on the Bitcoin trading track in the same year. They did not replicate BTCC's grassroots pioneering path; instead, they used mature internet strategies to break the initial pattern established by Yang Linke and Li Qiyuan, pushing Chinese cryptocurrency exchanges from a geeky small circle to the throne of global dominance.

Li Lin was from Shaoyang, Hunan, born in 1986, and was a standard veteran of internet products. He was a top student in computer science during his school years and after graduation worked at major companies like Renren and Oracle, mastering product design and user operations. In 2010, he hit the group buying trend and founded Mengmai.com, which once ranked among the top ten in the country, but ultimately fell in the smoke of the group buying war.

This failure opened his eyes: small entrepreneurs could only break through by relying on vertical tracks, urgent needs, and light asset operations.

In 2013, as Bitcoin surged from $13 to $1,000, domestic trading demand exploded. Li Lin immediately went to use BTCC, only to be left speechless by the poor experience: the page was laggy, deposits were cumbersome, and he couldn't find customer service. He instantly grasped the industry's lifeline: China lacked people to trade Bitcoin, but it needed a user-friendly, fast, and reliable trading platform.

At that time, BTCC had established a foothold thanks to its first-mover advantage but still bore the rough edges of a geek website. In September 2013, Li Lin announced the launch of Huobi, which, with its "user-friendly, free, and fast" approach, broke one million in trading volume within three months, beginning to challenge BTC China's first-mover advantage.

Li Lin's breakthrough strategy was user experience: instant deposits and withdrawals, 24-hour customer service, and a smooth page, coupled with a killer feature of free trading, directly penetrating the initial platforms that made money from transaction fees.

While Li Lin was frantically capturing the market with user experience, Xu Mingxing, who also wanted to make money in this field, took a completely opposite path.

Born in 1985, Xu Mingxing was a tech geek from Suzhou, Jiangsu. Graduating from Beijing University of Posts and Telecommunications, he had mastered distributed systems and high-concurrency architecture during college. After graduation, he joined Yahoo China, participating in the development of world-class trading systems, and later became the technical director at Douban, gaining a clear understanding of the stability of a platform with millions of users.

After encountering Bitcoin, he didn't care about the retail experience; he focused on the core barriers of trading systems. At that time, all domestic platforms' matching engines couldn't support massive trading and high-frequency quantification, leaving institutional users with nowhere to go. Xu Mingxing's goal was to create the most stable and fastest exchange in China, specifically serving institutions.

In October 2013, OKCoin officially launched, branding itself with "top technology, professional trading," competing directly with Huobi.

He personally led the team to write matching code, creating a system capable of millisecond transactions and tens of thousands of concurrent users, directly crushing BTCC's outdated architecture. Similarly focusing on quantitative and high-frequency trading, he firmly captured professional investors and institutional teams, forming a stark contrast to Li Lin's retail route.

One understood users and targeted retail; the other understood technology and catered to institutions.

Li Lin and Xu Mingxing carved out two complementary yet opposing paths to rise in the same year and on the same track.

By the end of 2013, both Huobi and OKCoin had risen, completely breaking BTCC's monopoly, and the three-legged structure of Chinese exchanges was officially formed.

At that time, BTCC held onto the golden signboard of the first-generation pioneer, relying on overseas resources and established reputation to retain old users; Huobi became the largest platform by relying on extreme user experience and aggressive operations; OKCoin monopolized the institutional and quantitative market with top-notch technology.

The three did not engage in vicious competition but instead expanded the industry pie together. With the opening of the RMB inflow channel and the standardization of trading processes, it became easier for more people to enter the cryptocurrency space, transforming exchanges from a fringe business into the most profitable entrepreneurial track at the time.

The global influence of Chinese exchanges began to emerge, while an unexpected global black swan event allowed them to take over the world.

In February 2014, the global cryptocurrency industry was rocked. The Japanese Mt. Gox exchange, which once dominated over 70% of the global Bitcoin trading volume, declared bankruptcy after being hacked and losing 850,000 Bitcoins due to internal chaos. The global cryptocurrency trading system collapsed instantly, causing panic among users, liquidity to dry up, and prices to plummet, leading to the complete failure of European and American exchanges and creating a massive vacuum in the market.

The three major platforms in China seized the opportunity to rewrite history: the RMB trading system was mature, the user base was large, and liquidity was sufficient. Huobi and OKCoin's systems were capable of accommodating the global overflow of traffic, while BTCC connected with international users through overseas resources.

In just three months, the core of global Bitcoin trading shifted from Tokyo to Beijing and Shanghai.

From 2014 to 2016, BTCC, Huobi, and OKCoin firmly occupied over 80% of the global Bitcoin trading volume, with peaks exceeding 90%. The RMB became the core currency for Bitcoin pricing, and China's trading hours, policy trends, and user sentiment directly influenced global Bitcoin prices.

Huobi's customer service was still processing orders in the early morning in Beijing, BTCC's matching system was running at high speed late at night in Shanghai, and Shenzhen's quantitative team was monitoring high-frequency trading on OKCoin, while China had become the absolute center of global cryptocurrency at that time.

These were the most glorious three years for Chinese exchanges, with no high-pressure regulation, no vicious internal competition, and no catastrophic explosions. The three giants ruled the world together, reaping enormous profits. Li Lin, Xu Mingxing, and Li Qiyuan stood at the pinnacle of the industry, becoming well-known faces in the global cryptocurrency circle.

While the giants dominated, small and medium platforms sprang up like mushrooms after rain, and the industry entered a prosperous period of a hundred schools of thought contending. Chinese Bitcoin exchanges focused on low fees to capture the sinking market, Bitcoin trading networks delved into spot trading, and Bter took the lead in niche coins. By 2016, the number of formal exchanges in China exceeded 30, and Bitcoin traders began to take shape from first-tier cities to small towns.

At this stage, there was only pure spot trading, and everyone thought the golden age would last forever.

But beneath the surface of prosperity, undercurrents were already surging.

The competition for users among the three giants became increasingly fierce, and pure spot trading could not satisfy their expansion ambitions; small and medium platforms began to focus on futures, leverage, and altcoins, seeking new profit points; regulatory scrutiny shifted from "defining virtual goods" to the rapidly expanding financial risks.

In 2016, Bitcoin prices steadily rose amid fluctuations. The three major exchanges sat on the throne of global trading volume, enjoying the benefits of pioneers.

However, they did not anticipate that the next phase would see a fierce internal competition surrounding futures, altcoins, and high leverage, while the regulatory knife hanging over the industry was quietly descending.

03 The Frenzied Game of Futures, Altcoins, and Leverage

In the deep winter of 2016, the Huobi office was lit all night, and the Bitcoin candlestick chart on the screen fluctuated violently due to leverage and hot money. In the corner of a 24-hour convenience store downstairs, traders with bloodshot eyes were either joyfully shouting with their phones, having just doubled their salary from a single altcoin, or crouching on the ground with their faces covered in silent tears, having just been liquidated by high leverage, losing all their savings.

This was the most frenzied time for Chinese cryptocurrency exchanges. The dividends of the spot trading track had nearly dried up, and the three giants—Huobi, OKCoin, and BTCC—tore off their gentle masks and engaged in close combat, while new players exploited loopholes in the rules and took risks.

Futures leverage, altcoin ICOs, and over-the-counter financing became three wildfires, burning the entire industry beyond recognition. Air coins ran rampant, financing sucked blood, volume was faked, and dark box operations flourished; all the evils and chaos of financial markets erupted in these two years.

It was high-leverage futures that first tore apart the industry's bottom line.

Back during the spot trading frenzy, a group of traders who had long been immersed in overseas contract markets sensed survival opportunities in the bear market. They didn't understand the technology of big firms or engage in refined operations, but they understood retail traders' gambling nature: only buying in spot trading meant only making money when prices rose, and in a bear market, one could only wait to die; with leverage and short selling, one could profit from both rising and falling prices.

In June 2013, the first domestic Bitcoin futures platform, 796, launched, bearing the label of high risk and offering up to 10x leverage, directly opening a new battlefield.

The shocking "3.21 LTC Crash" in 2014 propelled 796 to fame.

On the night of March 21, the price of Litecoin on the Huobi platform unexpectedly halved, crashing from 180 yuan to 90 yuan. There was no warning, no circuit breaker, and no risk control; millions of spot users were directly "killed," and their account funds evaporated instantly.

The platform's customer service was overwhelmed, and the office was packed with retail investors seeking redress. Some shouted angrily, while others sat down and cried. This incident made retail investors see the soft underbelly of spot trading and made 796 an overnight sensation.

In just a month, 796's trading volume surged tenfold, becoming the only winner in the bear market.

Xu Mingxing and Li Lin could no longer sit still; they knew that derivatives were the real profit machines. Huobi quickly launched BitVC futures, OKCoin rolled out a contract section overnight, and together with BTCC, they ignited a ruthless futures war.

Transaction fees were slashed from 0.1% to 0.03%, nearly free to grab users; leverage was increased from 5x to 20x, with 30x financing secretly opened to large clients; platforms quietly "manipulated" trades, delayed transactions, and targeted liquidations, silently eating away at retail investors' margins.

In May 2014, the five major platforms jointly announced a suspension of leverage business, but just a month later, high leverage was fully restarted. In the face of huge profits, no one was willing to hit the brakes.

796 became the first victim of this internal competition.

On the night of November 3, 2014, 796 suddenly collapsed across the platform, unable to log in, place orders, or withdraw funds, with users' money locked in the platform. The founding team worked overnight to fix the issues but to no avail; three days later, when they reopened, trading volume was zero, and trust collapsed. Once a leader in futures, 796 vanished in just a few weeks. The death of 796 was the clearest warning: uncontrolled high leverage was a money-sucking black hole, but by then, the market had already been swept up in gambling instincts, and no one cared about this warning.

While the futures battlefield was bloody, the altcoin and ICO track stirred up an even crazier bubble of wealth, breeding the worst chaos.

Bitcoin and Litecoin had long been monopolized by the three giants, and small platforms had no chance to break through. Former Alibaba security engineer Zhang Shousong quickly found his path—relaxing coin listing reviews and focusing on long-tail altcoins. As long as project teams paid a listing fee, JuCoin would approve them all.

In 2017, the ICO craze hit, and JuCoin went completely wild. Hundreds of altcoins flooded onto the platform, with project teams and platforms sharing profits, launching with skyrocketing prices, attracting retail investors to buy high before quietly dumping and cashing out, leaving a mess behind. Retail investors never read white papers, only listened to so-called insider information, and even dared to invest all their wealth in worthless junk coins.

JuCoin's approach allowed it to briefly top the global trading volume in 2017, serving 23 million users, becoming a wealth factory in the altcoin track and a notorious base for harvesting retail investors.

At the same time, Yunbi took the "opinion leader harvesting" to the extreme. Early Bitcoin evangelist Li Xiaolai held a 25% stake and had a million fans, making Yunbi not only the first platform in China to list Ethereum but also the preferred platform for ICO projects. In 2017, one ICO project after another launched on Yunbi, skyrocketing upon opening, with myths of hundredfold and thousandfold coins spreading across the internet.

JuCoin and Yunbi led the frenzy, while smaller platforms like Yuanbao, Bit Era, and others followed suit, flooding the market with platform tokens, altcoins, and ICO tokens. The entire market turned into a casino, with bad coins driving out good ones, and projects that genuinely focused on technology were drowned out.

The madness of futures and altcoins completely skewed the entire industry. From the three giants to small platforms, all the unspoken rules were laid bare, and the chaos was shocking.

At that time, Huobi and OKCoin fully opened financing and borrowing, allowing users to borrow 5 to 10 times their principal to trade, essentially official financing, with exorbitant interest rates; third-party companies for over-the-counter financing offered up to 50 times leverage, with daily interest rates of 1%. Borrowing 100,000 yuan meant a daily interest of 1,000 yuan, leading countless retail investors to borrow high-interest loans to trade, and when the market reversed, they were instantly buried in debt.

To seize the title of "global trading volume leader," all platforms were frantically inflating their volumes.

Bots executed trades, turning a real trading volume of 100 million into 10 billion; all orders on the order book were fake, creating a false illusion of ample liquidity, and the trading volume data reported by the media was so inflated that it was of no reference value. The open secret in the industry was that the real trading volume of Chinese exchanges was only one percent of what they claimed.

At that time, all exchanges had no third-party fund custody; users' RMB and cryptocurrencies were all held in the founders' private bank accounts and wallets. Platforms freely misappropriated user funds for trading, investment, and lavish spending. Small platforms could run away at any time, and from 2016 to 2017, over a hundred small exchanges suddenly shut down, with founders going missing and users losing all their assets. There was no regulation, no insurance, and the safety of users' assets relied entirely on the founders' conscience.

Similarly, exchanges at that time did not have real-name authentication, and deposits relied entirely on private transfers, allowing gambling funds, dirty money, and illicit funds to be quickly laundered through exchanges. Underground banks used cryptocurrencies to transfer funds across borders, evading foreign exchange regulations. Hacker attacks were frequent; Bter's cold wallet was hacked, losing 7,170 Bitcoins, and the platform barely covered the losses; small platforms that were hacked often ran away, leaving users to bear the costs, with chaotic private key management and internal employees stealing from users being common occurrences.

In the first half of 2017, the madness of Chinese exchanges reached its peak: over 90% of global Bitcoin trading volume came from China, and ICO projects raised hundreds of millions overnight, with discussions of getting rich from trading Bitcoin everywhere.

In June 2017, the summer in Beijing was suffocatingly hot. The atmosphere in the exchanges' offices was still one of all-night revelry, with volume-inflating bots running non-stop, ICO project listing applications lining up, and the sounds of liquidation from futures being drowned out by the noise of the bull market.

No one wanted to believe that this four-year-long wild growth was about to come to an end.

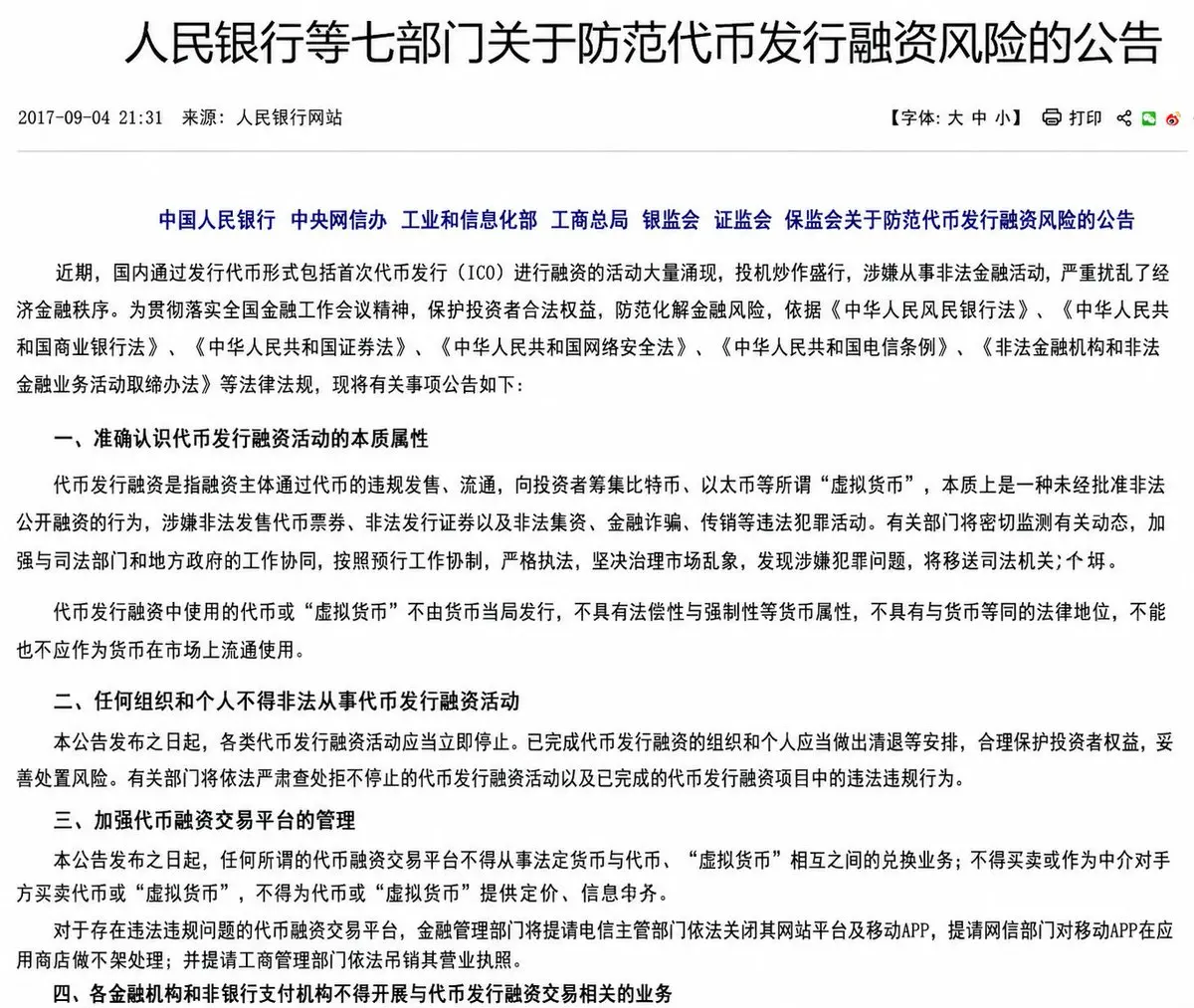

On September 4, 2017, a notice issued by seven ministries would abruptly halt all the madness, bringing the golden age of domestic exchanges to a complete end.

04 The September 4 Regulation and the First Separation from Domestic Trading

In early 2017, the Beijing branch of the central bank and the Shanghai headquarters first summoned the heads of the three major platforms—Huobi, OKCoin, and BTCC—to reiterate the core red lines of the document Yin Fa [2013] No. 289: Bitcoin is merely a virtual commodity and absolutely not legal currency; financial institutions must not engage in related businesses.

Five days later, a joint inspection team composed of the central bank and local financial bureaus officially entered the three major platforms to conduct on-site inspections. They retrieved backend trading data, checked funds flow transaction by transaction, and scrutinized every user agreement: unauthorized financial business operations, illegal financing and borrowing with amplified leverage, a complete lack of anti-money laundering systems, and user funds not being held in third-party custody…

On January 18, the central bank officially announced the inspection results and issued mandatory rectification orders: immediately halt all financing and borrowing activities, cancel zero transaction fees and restore trading fees, establish real-name authentication and anti-money laundering systems, implement third-party custody for user funds within a deadline, and eliminate false volume inflation.

This cut caused the industry to bleed instantly.

The astronomical daily trading volume of Bitcoin, which had been built on "zero fees + leverage + volume inflation," plummeted from 13.6 million coins to just 120,000 coins in a month, a drop of over 99%.

Li Lin stood in front of Huobi's big data screen, watching the line plummet vertically, chain-smoking as his fingertips grew hot; Xu Mingxing held an emergency technical meeting overnight, ordering the shutdown of all leverage interfaces, with the team working through the night to modify system codes; far away in Shanghai, Li Qiyuan quickly adjusted BTCC's business in accordance with the policies, shrinking all high-risk modules. For the first time, the entire industry felt that the regulatory knife was truly about to fall.

However, on the other side of the industry, ICO project listing applications were still lining up, the hype around altcoins showed no signs of waning, and underground financing companies changed their names to continue attracting clients.

Until 3 PM on September 4, 2017, an official announcement flooded the internet, causing the entire cryptocurrency circle to erupt.

The central bank, the Central Cyberspace Administration, the Ministry of Industry and Information Technology, the State Administration for Industry and Commerce, the China Banking Regulatory Commission, the China Securities Regulatory Commission, and the China Insurance Regulatory Commission jointly issued a notice on "Preventing Risks of Token Issuance and Financing," which was the infamous "September 4 Announcement" that sent chills down the spine of the entire industry. The announcement, based on multiple laws and regulations such as the "People's Bank Law" and the "Securities Law," used the most severe language to deliver a death sentence to domestic cryptocurrency trading.

Source: People's Bank of China website

Token issuance and financing were essentially unauthorized illegal public financing, suspected of illegal fundraising, financial fraud, and pyramid schemes, and were to be halted immediately; any trading platform was prohibited from engaging in any services related to the exchange of fiat currency and cryptocurrencies, token exchanges, pricing, or information intermediary services; banks and payment institutions must completely sever funding channels, and non-compliant platforms would have their websites shut down, apps removed, and licenses revoked; projects that had raised funds must refund within a specified period.

This effectively ended the business of domestic exchanges from a legal standpoint.

The moment the news broke, the entire industry fell into silence, followed by overwhelming panic.

Messages in industry groups flooded in, with cries of "It's over" and "What about the money?" filling the screen; Bitcoin and altcoins plummeted across the board, with drops exceeding 30% within minutes; the customer service systems of exchanges were instantly overwhelmed, with phone lines and online consultations filled with requests from users demanding withdrawals and refunds, the noise nearly lifting the roof.

Li Lin printed the full text of the announcement, reading it word for word, crumpling the paper in his fingers, and after half an hour of silence, he simply told his team, "Execute, strictly execute everything."

Xu Mingxing repeatedly checked the scope of the prohibitions on "fiat currency exchange" and "information intermediary," his expression serious, and immediately ordered the shutdown of all fiat trading channels and the initiation of user asset refunds;

Li Qiyuan held a global meeting overnight, making it clear that BTCC must first halt its domestic business, using the credibility of the established platform to protect the last line of defense for users.

The week following the September 4 announcement was the darkest hour for all exchanges.

An unprecedented wave of user withdrawals erupted, more terrifying than any hacker attack or market crash.

Online, withdrawal requests increased by thousands every second, with servers nearing collapse, technical staff going days without sleep, desperately keeping the channels open;

Offline, large numbers of users gathered outside the platform's office building, holding their phones and demanding immediate withdrawals, creating a tense scene;

Customer service staff were surrounded by users' accusations and complaints, apologizing with red eyes while manually reviewing each withdrawal request, their voices hoarse by the end of the day;

Financial personnel were constantly checking transfers against the wildly fluctuating bank statements, with large amounts of money in private accounts frequently triggering bank risk controls, making every step difficult.

From late September to early October, BTCC, Huobi, and OKCoin successively released final announcements, each word tightly adhering to the policy requirements of the September 4 announcement: from now on, all RMB and cryptocurrency trading businesses within the country would cease, and user asset refunds would be completed in an orderly manner.

At that moment, the core lifeline of domestic exchanges was completely severed.

From the first line of code in a Shanghai residential building in 2011 to dominating 90% of global trading volume in 2017, the golden age of Chinese cryptocurrency exchanges came to an abrupt end.

The cessation of domestic operations was not the end of the industry but a forced migration.

All platforms understood that staying in the domestic market meant a dead end; going abroad might offer a glimmer of hope.

05 Offshore Growth, Madness and Disillusionment, and Ultimate Zeroing

Three months after the September 4 announcement, domestic cryptocurrency trading was abruptly halted, but it seemed that none of the entrepreneurs who had emerged from the internet wilderness truly left the scene.

The September 4 announcement only shut down domestic RMB trading, but it did not extinguish the addiction of Chinese people to trading cryptocurrencies. The first to react were still the old rivals Li Lin and Xu Mingxing.

Li Lin cleaned up Huobi's domestic business completely and turned his attention to building Huobi.Pro in Singapore. He had always sought stability in business; whether in group buying or exchanges, he took cautious steps. This time was no different—he avoided any illegal fiat channels, only using USDT stablecoins, and did not actively block mainland users from bypassing restrictions, nor did he publicly recruit them, acting like a shopkeeper guarding his stall, just wanting to maintain stability in overseas operations. He watched as his team members changed to overseas work IDs, knowing in his heart that Huobi would never return to its golden era in Beijing's Wangjing SOHO.

In stark contrast to Li Lin's conservatism, Xu Mingxing had no intention of merely holding the fort. As soon as the September 4 document was released, he rebranded OKCoin to OKEx and dove headfirst into the futures business. Back in China, he had competed with Li Lin using technology and high-frequency trading, and now, free from domestic regulatory constraints, he fully leveraged the leverage and moved the operations center to Malta, where regulations were more relaxed. In his eyes, spot trading was no longer profitable; only derivatives and leverage could allow OKEx to surpass Huobi. The two continued their rivalry, one defending and the other attacking, neither willing to yield.

While Li Lin steadily maintained his spot trading base and Xu Mingxing gambled everything on the futures track, another tech veteran who had left OKCoin quietly laid out a comprehensive strategy that neither of the two giants had grasped.

This person was Zhao Changpeng.

In terms of background, Zhao Changpeng was a standard overseas tech expert, with a foundation far more solid than most grassroots entrepreneurs in the circle.

Born in Jiangsu in the 1970s, Zhao immigrated to Canada with his family at a young age, receiving a rigorous Western engineering education. After graduation, he worked for many years on the underlying architecture of global top financial trading systems, serving in the core trading rooms of Tokyo Securities and the Bloomberg cross-border trading systems team, honing high-concurrency, zero-lag matching technology, and thoroughly understanding the core trading logic of traditional finance, not just a wild card who switched careers halfway.

In 2014, as the cryptocurrency industry began to emerge, he saw the opportunity and returned to China to enter the field. Through He Yi's connections, he officially joined the early leading platform OKCoin as CTO, holding the core technological power of the platform.

At that time, Xu Mingxing focused on overall strategy and financial control, Zhao Changpeng handled the full-stack trading system and asset security, and He Yi coordinated market public relations. The three were tightly bound together, forming the "OK Iron Triangle," which was the most valuable and execution-driven team in the early cryptocurrency circle, effectively elevating OKCoin to a dual oligopoly position alongside Huobi.

After working together for several years, ideological rifts gradually fermented, internal power struggles and differences in direction intensified, and the iron triangle became completely disjointed. Zhao Changpeng, feeling unsettled, decided to withdraw, secretly harboring a fierce determination to reverse the situation and crush his former employer.

In 2017, as the cryptocurrency market became increasingly volatile and industry chaos began to arise, regulatory tightening signals were released in advance. While most people in the circle were still blindly increasing their domestic fiat trading and frantically harvesting short-term traffic, Zhao Changpeng accurately sensed the policy risks and decisively went all in, betting his entire fortune.

He directly sold his core properties in Shanghai, consolidating all cash flow, and without hesitation, set out to establish Binance.

Early photo of CZ founding Binance

From the very beginning, he deliberately avoided all the compliance red lines that everyone else was crowding around, not touching any domestic RMB fiat exchange channels, and only conducting pure cryptocurrency-to-cryptocurrency exchanges. From the underlying architecture and business links to the entity's location, he perfectly circumvented the regulatory prohibitions of the subsequent September 4 announcement, positioning himself in a safe zone.

By the time the September 4 policy was implemented, Huobi and OKEx were hurriedly shutting down domestic channels and hastily refunding mainland users, busy cutting off business to stabilize their operations and respond to regulatory inspections, while Binance had already prepared overseas links and opened all channels, quietly accommodating all the fleeing retail investors, funds, and traffic from the two giants.

With no past burdens, no business entanglements, and no compliance encumbrances, in just six months, Binance took off on the wave of the times, directly crushing Huobi and OKEx, which had been deeply rooted in the industry for years, and leaping to the top of the global trading volume leaderboard, transforming from a former technical executive to the new industry leader.

Li Lin watched as his former subordinate surpassed him, feeling uneasy; Xu Mingxing, seeing Binance's wild growth, could only continue to guard his own base. The three old acquaintances returned to the old pattern of a three-way standoff on the overseas battlefield.

While the giants scrambled for territory abroad, two tech-focused individuals survived in the gaps left by the giants.

Gan Chun, a security expert from Ant Financial, knew he couldn't compete with Li Lin, Xu Mingxing, or Zhao Changpeng, so he simply avoided mainstream coins and focused on lesser-known altcoins, registering in Seychelles and naming the platform KuCoin. He didn't advertise or seek headlines, quietly accumulating tens of millions of users through safety and stability.

Han Lin was even more low-key, a Canadian PhD in optoelectronics who had been scammed when buying Bitcoin, and in frustration, created Bter, renaming it Gate.io after the September 4 announcement. He was one of the few down-to-earth people in the circle; when his platform was hacked and lost over 7,000 Bitcoins, he personally compensated users, and this reputation allowed him to survive steadily in the cracks between the giants.

These four individuals—each maintaining their own approach, whether conservative, aggressive, speculative, or pragmatic—thrived in the overseas exchange business. But no one expected that a tech person who had left Huobi would use an absurd model to shake the entire industry.

This person was Zhang Jian.

Zhang Jian was the former CTO of Huobi and had written the first bestselling book on blockchain in China, recognized in the circle as a technical idealist. After leaving Huobi, he wanted to pursue true technological innovation and looked down on the exchange's model of earning fees and harvesting retail investors. When the bear market arrived in 2018, Zhang Jian came up with a bold move—"Trading is Mining."

In simple terms, it meant that the transaction fees from users' trades would be returned as platform tokens, and holding platform tokens would also yield dividends. It sounded like a benefit, but in essence, it was a Ponzi scheme. However, the industry had already gone mad; within 12 days of FCoin's launch, its trading volume surpassed the combined total of Huobi, OKEx, and Binance.

Zhang Jian transformed from an industry role model to a "disruptor" overnight, but he knew very well that this bubble would eventually burst.

Indeed, less than two years later, FCoin collapsed. Over 7,000 Bitcoins could not be redeemed, and Zhang Jian disappeared overnight, leaving hundreds of thousands of users with nothing. The once-idealistic technologist became the biggest fraudster in the circle, and this farce became the most glaring scar of the gray industry over the past four years.

FCoin collapsed, but the industry's madness did not diminish.

In mainland China, related businesses did not completely disappear but gradually shifted to more concealed and decentralized gray areas.

Mining had formed a considerable scale in places like Sichuan, Yunnan, and Inner Mongolia, with many mining machines relying on cheap electricity to operate continuously. China's computing power once occupied a significant share of the global market. However, behind the rapid expansion, issues such as energy consumption, local regulatory arbitrage, and compliance with electricity usage began to accumulate.

At the same time, over-the-counter trading involving USDT quietly spread among the public. WeChat, Alipay, and bank transfers became alternative channels for many users to enter and exit the cryptocurrency market. This maintained market liquidity to some extent but inevitably became a part of illegal activities, such as fraud, gambling, and capital flight, making it difficult to regulate.

2019 was a golden period for the development of exchanges in China.

After several rounds of bull and bear markets, the industry discourse power was firmly held by the three major players, collectively referred to as the HBO Iron Triangle, with Huobi, Binance, and OKEx dividing over 80% of the effective traffic in the Chinese-speaking world, crushing both the spot and futures tracks, while second-tier platforms struggled to compete directly, and third-tier small exchanges could only run alongside.

Binance pioneered the IEO model with Launchpad, with the initial release of the BTT token doubling in value, igniting a wave of enthusiasm for new projects across the internet, followed by quality projects stepping in, steadily capturing the first round of traffic dividends; in July, it launched perpetual contracts, exerting dual pressure on both spot and derivatives, maintaining over 30% of global trading volume throughout the year, and emerging as a dark horse to claim the top spot.

Huobi closely followed the trend by launching Huobi Prime to synchronize with IEOs, maintaining a solid second position in the industry.

OKEx launched OK Jumpstart as a differentiated counterpart to IEOs, standing shoulder to shoulder with Huobi to maintain its second-tier base. The three often copied each other in daily operations, with new product launches, promotional activities, and product models being highly similar, leading Chinese retail investors to migrate back and forth across platforms.

IEOs were the absolute traffic password of 2019, becoming the universal tool for platforms to increase revenue, boost trading volumes, and attract new users. Project teams bypassed the cumbersome private fundraising processes and directly connected with leading exchanges for compliant listings, allowing users to participate in lotteries for new projects by staking platform tokens, while platforms steadily profited from listing service fees and secondary market transaction fees, resulting in a short-term win-win frenzy for all three parties.

Amid the heightened excitement, retail investors' FOMO emotions reached a peak, and platform tokens collectively experienced a doubling trend, with valuations across the industry rising. However, hidden dangers lurked behind the revelry, as many projects with no qualifications took the opportunity to mix in and raise funds, leading to market crashes and frequent collective rights protection incidents, laying a solid foundation for subsequent global regulatory crackdowns.

The top players clustered together to compete for core profits, while second- and third-tier platforms avoided direct confrontations, all opting for differentiated strategies to quietly profit.

Platforms like KuCoin, Gate.io, BitMax, ZB, LBank, Bibox, CoinEx, Bitforex, EXX, CoinBene, MXC, BiKi, Hotbit, BigONE, DigiFinex, and BitZ also shared in the dividends, each playing their part to divide the remaining scattered traffic.

Overall, 2019 was the last wild revelry feast for cryptocurrency exchanges.

With clear hierarchies, vibrant gameplay, abundant traffic, and frequent stories of getting rich, the three HBO giants monopolized the core profits of the entire industry, while second-tier platforms developed quietly through differentiation, and third-tier small exchanges survived by following trends.

It was also during this phase that the image of the cryptocurrency industry in China began to rapidly diverge: on one side were the enormous business opportunities brought by mining, trading, and global liquidity; on the other side were the social risks brought by regulatory blind spots, gray funds, and the spread of scams. The industry was not denied overnight but gradually accumulated reasons for strong regulatory rectification amid long-term disorder.

Everyone knew that these gray days would eventually come to an end.

First, regulatory authorities shut down over-the-counter trading channels for Alipay and WeChat, then cleared out mining sites in Inner Mongolia and Sichuan, and finally cut off all channels for exchanges to bypass restrictions.

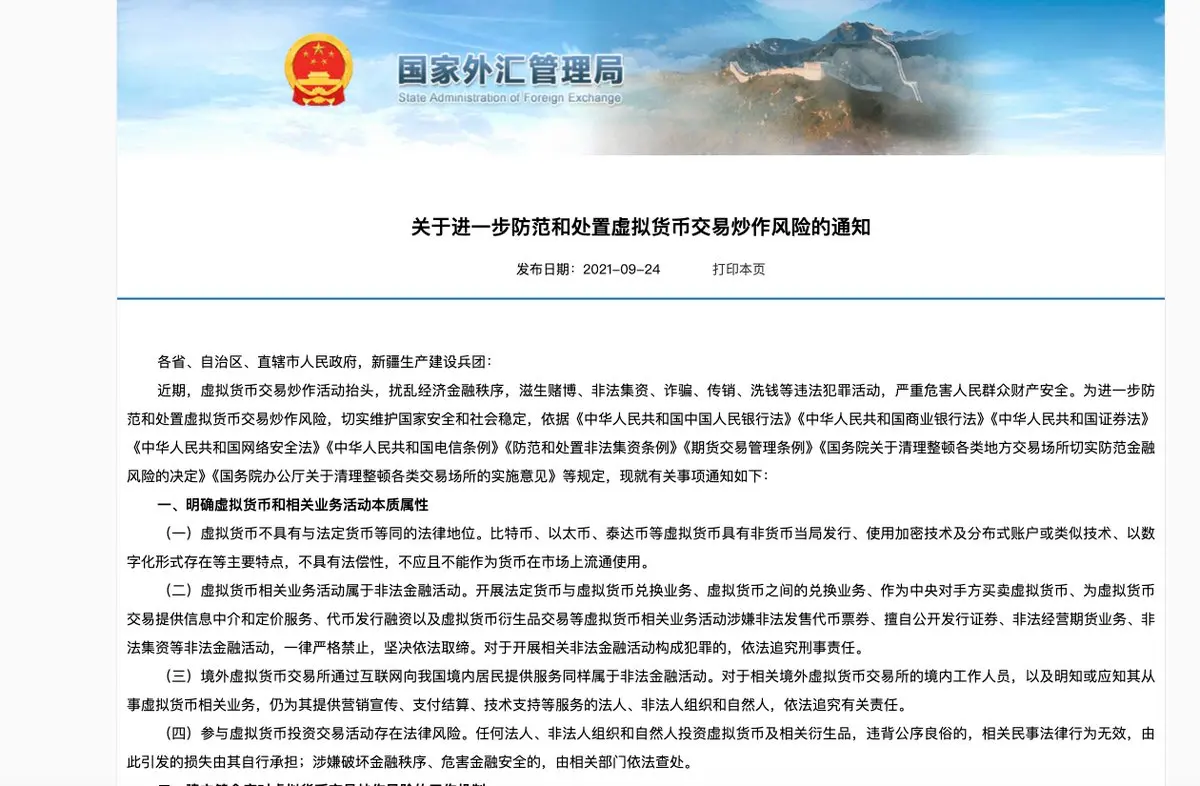

Until September 24, 2021, when a notice from ten departments came down, directly declaring that all cryptocurrency-related businesses in the mainland were illegal financial activities; providing services to mainland users from overseas platforms was also illegal.

Source: https://www.safe.gov.cn/safe/2021/0924/19915.html

This time, no one dared to take chances.

Li Lin's Huobi completely refunded mainland users; Xu Mingxing shut down OKEx's mainland IP, completely turning towards Europe; Zhao Changpeng cut off Binance's channels for bypassing restrictions, abandoning the largest hidden pool of traffic; Gan Chun and Han Lin also obediently restricted mainland users, saying goodbye to the gray business. The remaining mid-tier and long-tail small exchanges that relied on the Chinese market essentially disappeared in this round of strangulation.

The mainland market, which once accounted for 90% of global trading volume, was completely zeroed out.

06 The Disintegration of Giants, Selling Off and Leaving the Market, and the New Global Compliance Landscape

With the arrival of the September 24, 2021, document, all cryptocurrency-related businesses were categorized as non-compliant financial activities; overseas platforms were prohibited from directing mainland users to open accounts, and domestic merchants and individuals were no longer allowed to provide payment, community, or technical support to exchanges, and even mining computing power was completely cleared out. In short, the local native cryptocurrency ecosystem was halted on the spot.

Overnight, the paths of the three giants began to diverge in three different directions.

Before the policy tightened, Huobi relied on its early entry and established reputation to maintain a steady spot market, with a continuous flow of retail investors and stable transaction fees, avoiding the risks of high-risk contracts and the chaos of listing obscure coins.

However, after the new regulations were implemented, its advantages were completely wiped out, and troubles followed one after another:

It was impossible to obtain licenses in Europe and the U.S., Southeast Asian regulators frequently conducted interviews, and cross-border users were often limited in flow and IP. Renting overseas venues, hiring local teams, and employing compliance lawyers cost money like water, yet the platform's daily active users and trading volume continued to decline. Huobi's once-stable operational base suddenly faced multiple leaks, with compliance risks looming ahead and the reluctance to give up years of market foundation.

Li Lin saw through it all and understood the situation clearly. In the early years, with relaxed regulations, he could do business steadily through connections and flexible traffic guidance.

After 2021, it was all about hard regulations: user fund custody, on-site office registration, fund traceability risk control, and compliance endorsements for executives—missing any one of these would not hold up.

He had enough local connections but lacked the foundation for overseas compliance and cross-border political and business resources. On one side were increasingly strict regulatory pressures, and on the other were rising operational costs, along with the unclear risks of joint liability. After much thought, the optimal solution was clear: while the platform still had valuation, he should gracefully exit, avoiding the subsequent storms of the industry.

In 2022, coinciding with a bear market, the entire industry's assets shrank, and exchange valuations fell, creating a window for stable handovers at low points. Li Lin discreetly connected with Hong Kong capital, following formal institutional acquisition processes, publicly disclosing that the acquirer was Hong Kong's About Capital Management; subsequently, Sun Yuchen joined the global advisory board and became one of the most critical public figures in terms of brand, operations, and ecosystem.

By October of that year, all the handover procedures were completed. Li Lin cleared all his shares, resigned from all positions, and cleanly distanced himself from Huobi. On the surface, it appeared that the founding figure of the first generation had successfully retired, but in reality, it was a precise timing to cash out and hedge against the bear market, securing his assets. From that moment on, the ironclad industry structure established by the old three giants cracked open, and the curtain on the industry's compliance reshuffle was officially raised.

Li Lin turned his back on the platform, no longer involved in any trivial matters, and laid the groundwork for the establishment of a new Huobi, focusing on compliance agency services.

Sun Yuchen took over the operational authority, avoiding the old paths, gradually adjusting the platform's original operational rhythm to align with the actual needs of the offshore circle, quietly rewriting the originally stable competitive ecology of Chinese exchanges.

After taking over, Sun Yuchen's first task was to adjust the brand's external name, reducing local recognition to facilitate registration in various countries.

First, it was temporarily renamed "Huobi," lowering the old platform's recognition in the mainland and adapting to the basic compliance standards of multiple countries; by September 2023, during the TOKEN2049 conference in Singapore, when global industry figures gathered and traffic peaked, it was officially announced that the name would be changed to HTX.

TOKEN2049 / HTX DAO x TRON Afterparty scene

While leveraging the user base accumulated over many years, it also linked its own TRON ecosystem, smoothly transitioning through the platform's ten-year operational nodes, quietly completing the brand upgrade, and synchronously filling in the compliance disclosures for overseas operations.

After streamlining the brand, the platform adjusted its operational strategies to align with retail investors' actual trading preferences, increasing the variety of high-liquidity trading products, moderately relaxing the trading tiers for derivatives, and introducing a batch of compliant small and unique coins, quickly boosting trading volume and stabilizing its industry ranking. At the same time, it refined the operations of various communities, maintaining different needs of existing users, inviting experienced industry figures from overseas to form an external advisory team, and ensuring that the external compliance facade was solid and effective.

Short-term trading data visibly warmed up, but the platform's underlying security risk control and full-chain fund custody systems had not yet been upgraded in sync, leaving room for optimization in fund dispatching and real trading volume management. Behind the bustling traffic lay hidden pressures for long-term operations.

In fact, some minor issues left over from the equity handover began to surface.

In 2025, Li Lin and Sun Yuchen communicated publicly several rounds regarding the reconciliation of funds before and after the handover, position transitions, and the transfer of ecosystem tokens.

Both sides discussed their respective responsibilities, rationally sorting out the gaps in existing funds, the progress of margin replenishment, and the compliance flow of tokens, and handled all the handover issues in accordance with regulations.

Meanwhile, from 2023 to 2025, market fluctuations were significant, with some users reporting experiences of system lag, price fluctuations, and inconsistent order matching speeds during extreme market conditions. The platform was continuously optimizing its backend operational capabilities. Industry technical personnel flowed normally, and backend service efficiency was steadily iterated and adjusted. By 2026, HTX focused on deepening its existing user base in the Chinese-speaking world, steadily maintaining its own segmented market and operating smoothly without incidents.

While HTX steadily adjusted its operational rhythm and refined its community reputation, Xu Mingxing, who relied on contract technology to dominate, had already seen the industry's trends clearly.

He predicted that global regulation would only become stricter year by year, so he gradually reduced his public appearances, delegating the responsibilities of daily operations to professional teams, while quietly retreating to the background, only controlling core strategies and risk management.

After the full-scale withdrawal in 2021, OKEx, relying on its well-developed contract trading system and long-term partnerships with leading quantitative institutions, maintained a steady flow of basic transactions without experiencing operational turmoil or funding chain tensions.

However, the broader environment never eased; cross-border leverage controls became increasingly detailed, and compliance checks on trading grew more frequent, with overseas regulatory inquiries arriving every few days, requiring the closure of various user experience complaints and cooperation with local inspections. While the apparent revenue looked stable, the pressure of compliance hung over their heads at all times, fearing that any misstep could lead to business restrictions or cross-border penalties.

Xu Mingxing was well aware that the days of making wild profits from contracts were over. Moving forward, the industry would not compete on aggressive strategies but on compliance licenses, robust risk control, and institutional networks. Continuing to stand in the spotlight would only increase personal liability risks.

To isolate risks and simplify governance, he actively faded from public view, entrusting daily operations to a professional team while splitting multiple layers of offshore operational entities, delegating the cumbersome and responsible tasks of compliance connections, user operations, and fund reconciliations.

On January 18, 2022, OKEx officially rebranded to OKX, laying out plans for a full Web3 ecosystem and expanding on-chain custody services, breaking free from the single exchange framework while downplaying its early contract label and organizing historical compliance records to reduce the risks of cross-border traceability.

Once a fierce competitor alongside Li Lin, the early warrior quietly faded into the background, and OKX transformed into a professional compliance platform, becoming the second pillar of the old three giants, landing steadily.

After stepping back and delegating authority, OKX directly adopted a pragmatic approach, concentrating all manpower and resources on two tasks: obtaining compliance licenses globally and focusing on serving large institutional clients.

Starting in 2023, OKX accelerated its global compliance transformation, establishing local teams and compliance qualifications in markets like the Middle East and Southeast Asia, gradually transitioning from an early offshore trading platform to a globally licensed operator across multiple regions.

In 2025, OKX made significant progress in European compliance, obtaining a MiCA license in Malta in January and beginning to expand services to the European Economic Area through a passporting mechanism; in February of the same year, OKX reached a settlement with the U.S. Department of Justice regarding historical compliance issues, paying over $504 million in fines to address historical shortcomings in anti-money laundering, KYC, and cross-border operations.

Subsequently, OKX continued to strengthen its proof of reserves, fund transparency, and anti-money laundering risk control systems, with the platform's image gradually shifting from a "contract technology exchange" to a mainstream trading platform emphasizing compliance, custody, institutional services, and global licenses.

By 2026, OKX secured minority equity investment from ICE, the parent company of the New York Stock Exchange, with a corresponding valuation of about $25 billion. This not only indicated that traditional financial infrastructure was beginning to engage more deeply with the cryptocurrency trading system but also further reinforced OKX's signal of aligning with mainstream financial markets.

After three years of low-key development, OKX steadily captured the stable funds flowing out of Binance and the cautious users diverted from HTX, quietly securing its position as the second largest globally, becoming a genuine hidden winner in the circle.

While some cashed out and left, others remained behind the scenes to maintain order, and the industry landscape subtly shifted.

Only Zhao Changpeng, who had once raced to the top of the industry, faced the layered encirclement of global regulators, and the once-dominant scale of Binance returned to a normal pace of development.

During the years when Binance was at its peak, it relied on a lightweight offshore distributed operation without a fixed headquarters, absorbing global retail traffic without regional restrictions, consistently leading the industry in trading volume.

In the early years, while competing for territory and scale, it prioritized spreading traffic across the network and expanding its global customer base, gradually improving its compliance system and localized risk controls to align with the industry's early rough development pace. But regulatory agencies began to turn their attention to Binance.

The liquidity crisis at FTX in November 2022 may have been one of the triggers.

Before the crisis escalated, CZ had already sensed the risks, reducing his stake in FTX for compliance reasons and subsequently disclosing his plans for adjusting his holdings. Coinciding with FTT's own weak liquidity, this triggered a concentrated withdrawal from the market, temporarily impacting FTX's financial base. Binance then expressed intentions to acquire FTX but rationally terminated the cooperation after a quick due diligence process.

SBF was also found to have stolen billions from customers due to FTX's inability to repay user funds, constituting a serious fraud crime, facing long-term imprisonment.

The collapse of FTX also drew global regulatory scrutiny towards the compliance checks of leading platforms.

As the aftershocks of FTX had not yet dissipated, in March 2023, several overseas crypto cooperative banks experienced liquidity adjustments: Silvergate orderly liquidated its operations, Signature Bank was managed by local financial authorities, and Silicon Valley Bank slightly interacted with the flow of funds in the crypto circle. Traditional banks tightened their cooperation limits with cryptocurrencies, leading to a rational return of liquidity across the industry, with regulatory inspections intensifying and becoming routine.

With multiple historical compliance tasks piling up alongside industry fluctuations, in November 2023, Binance and Zhao Changpeng reached a compliance agreement with the U.S. Department of Justice: the platform would pay $4.3 billion for compliance rectification, closing the loop on historical issues related to anti-money laundering, cross-border compliance, and localized operations.

CZ was also sentenced to four months in prison for violating U.S. anti-money laundering regulations and personally paid a $50 million fine. After his release, the former CEO CZ focused on the overall compliance strategy, with his decision-making power in the industry returning to a stable norm.

Real scene of Zhao Changpeng outside the U.S. court in 2024

After the rectification, CZ completely reined in his expansion ambitions, no longer blindly seeking to acquire territory, focusing instead on maintaining stability and deepening compliance. He orderly tightened high-risk derivatives businesses, optimized cross-border fund flow controls, and split multiple regional independent compliance entities, shedding assets with high public sentiment and compliance risks.

In 2025, with Trump's rise to power, the industry's direction shifted dramatically. The Trump family launched the WLFI crypto ecosystem, issuing a USD1 compliant stablecoin pegged to U.S. Treasury reserves; in May of the same year, the Abu Dhabi-based investment institution MGX used the WLFI USD1 stablecoin to complete a $2 billion investment arrangement with Binance, significantly deepening the binding between Binance and Middle Eastern capital and the stablecoin ecosystem.

Moreover, in October 2025, CZ was granted compliance amnesty for past compliance-related issues, signaling that the industry had officially entered a new phase of political and business collaboration.

As the three giants adjusted and stabilized, the compliance users and market shares that were freed up flowed to second-tier platforms that had long been low-key and compliant, and a new stable pattern was formed, closing the window for grassroots cross-border entries and overnight overtakes in the industry.

KuCoin, led by Gan Chun, had not engaged in close battles with the giants for years, steadily focusing on overseas niche coins that met genuine demand, and had successfully weathered several bull and bear cycles during adjustments and user risk diversions from leading platforms.

Gate.io, under Han Lin's leadership, relied on its early reputation for full compensation for stolen Bitcoins to maintain stability, successfully enduring multiple rounds of bear market storms and fluctuations from small and medium platforms, firmly holding onto a group of stable high-net-worth users.

The chaotic wilderness came to an end, and the era of wild fighting concluded. The cryptocurrency industry officially entered a stable conclusion characterized by strong regulation, professionalism, and globalization, and all the stories of the first-generation cryptocurrency entrepreneurs came to rest.

Risk warning

Risk warning