AI PC War: Don't bet on factions, bet on toll booths

The core conclusion is just one sentence: In the AI PC battle, don't bet on camps, bet on toll booths; TSMC as the foundation, AMD on the offense, ARM as a small player, Intel just as a lottery, Qualcomm waiting for repricing, and Nvidia not chasing the FOMO after the news pulse.

The core conclusion is just one sentence: In the AI PC battle, don't bet on camps, bet on toll booths; TSMC as the foundation, AMD on the offense, ARM as a small player, Intel just as a lottery, Qualcomm waiting for repricing, and Nvidia not chasing the FOMO after the news pulse.Roger Lee|BIT U.S. Stock Special Analyst

With 21 years of experience in investment banking, asset management, and financial institutions, focusing on AI industry chain, U.S. stock macro liquidity, and options strategy research.

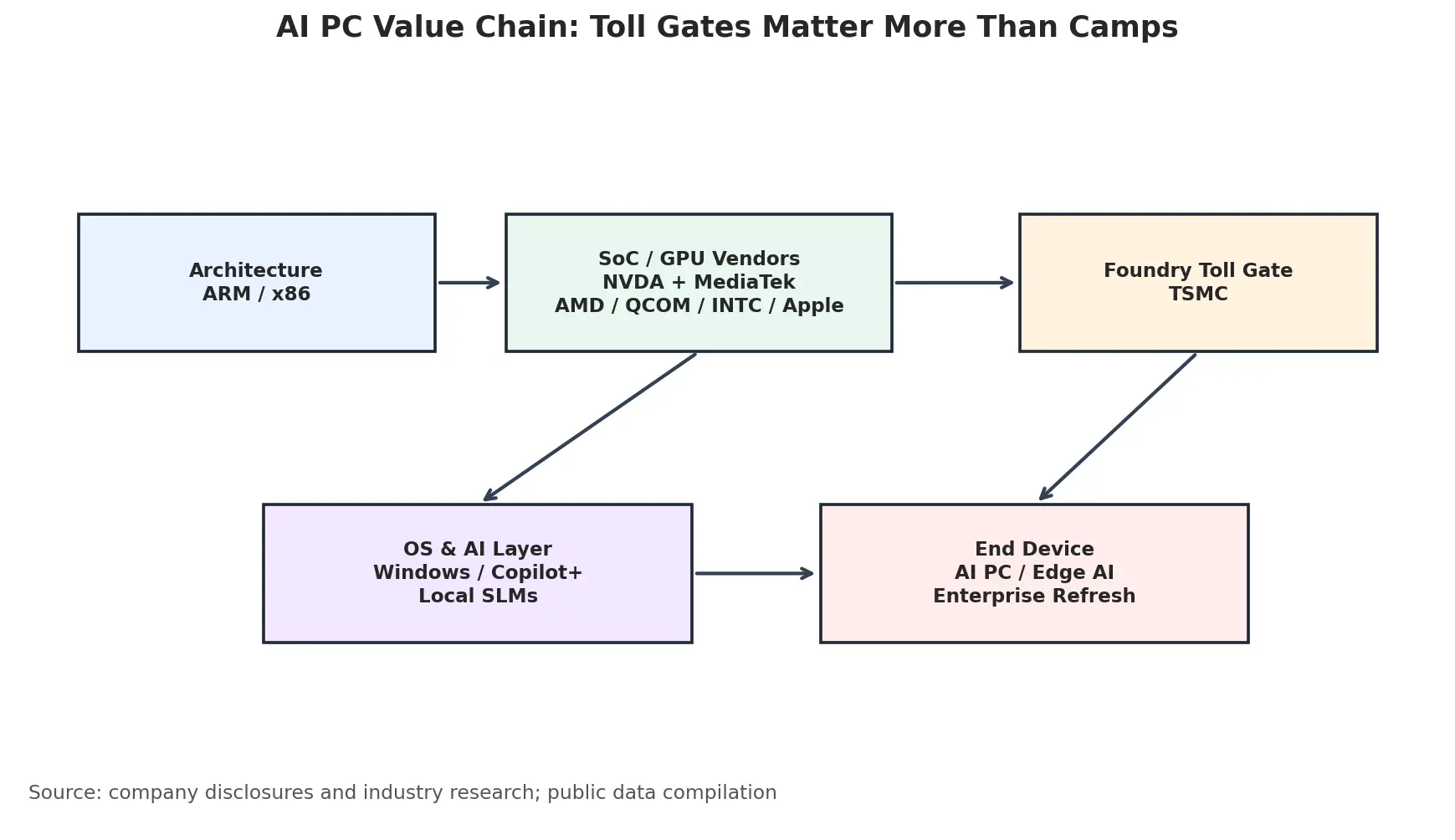

NVIDIA and MediaTek are entering the AI PC space, which on the surface appears to be just a new chip combination for consumer PCs, but essentially signifies that the AI ecosystem on the Windows side is transitioning from a single-player trial to multi-player competition. My judgment is that this war should not be simplified to a "x86 versus Arm" religious stance; what is truly worth studying is who can navigate the device replacement cycle, continuously secure gross margins, cash flow, and pricing power in the industry chain.

I view AI PCs as three layers of opportunity:

- The first layer is the advanced process toll booth; regardless of who wins, TSMC will find it easier to collect tolls.

- The second layer is the spillover of computing power and platforms; AMD and NVDA represent the offensive x86 and the extension of the GPU software stack, respectively.

- The third layer is architectural diffusion and dilemma reversal; both ARM and INTC have flexibility, but position discipline must be stricter.

1. Industry Judgment: AI PCs Entering the Shipment Verification Period from Concept

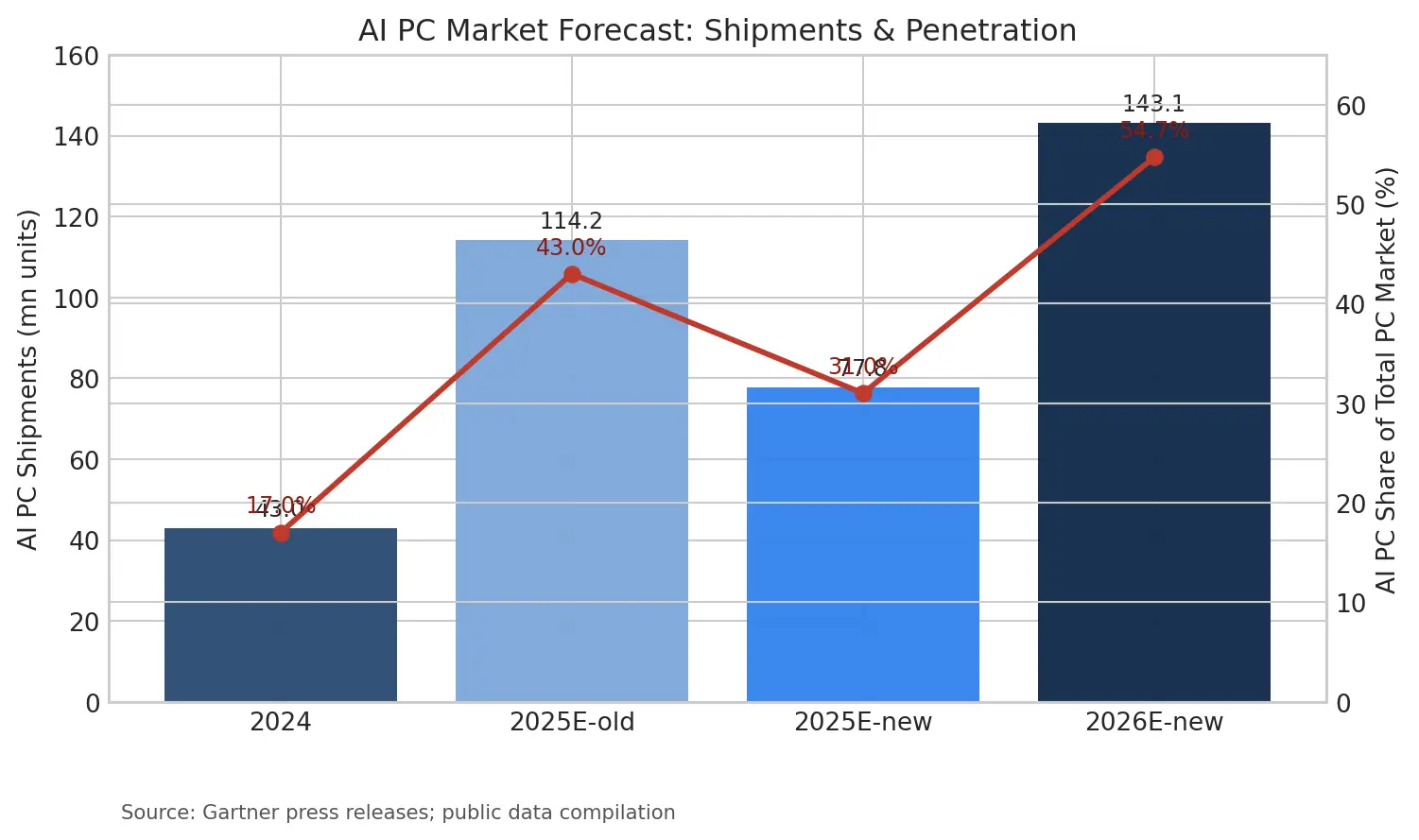

Gartner projected in 2024 that AI PC shipments will reach 114.225 million units in 2025, accounting for 43% of the PC market; after updates in 2025, influenced by tariffs and procurement rhythm disruptions, the forecast was revised down to 77.792 million units, accounting for 31%, but it is still expected to reach 143.113 million units in 2026, with a penetration rate of 54.7%. This set of data inspires me not to think of "AI PC demand being falsified," but rather that the short-term rhythm will fluctuate, while the long-term standardization direction remains unchanged.

|----------------|-------------------------------|-----------------------------| | Industry Variables | Current Changes | My Investment Interpretation | | Windows on Arm | Qualcomm's early monopoly dividends diluted by new players like NVDA/MediaTek | The single winner narrative is cooling, and the ecosystem is being repriced | | x86 Camp | AMD and Intel continue to strengthen NPU, integrated GPU, and CPU combinations | AMD is more like the offensive main line, while Intel resembles a dilemma reversal option | | Advanced Process | AI GPUs, mobile APs, and AI PC SoCs are competing for high-end capacity | TSMC remains the toll booth I value most | | Software Ecosystem | Local small models, privacy computing, and low-latency inference become selling points | Microsoft and the Windows application ecosystem determine the speed of implementation |

From an investment perspective, the real challenge for AI PCs is not "whether there is an NPU," but whether users are willing to replace their devices for a local AI experience. If the application layer only stays at meeting minutes, image generation, and simple assistants, the replacement elasticity will be lower than the market's most optimistic expectations; however, if enterprises start to deploy privacy computing, low-latency inference, and local knowledge bases as standard configurations, AI PCs will transition from a consumer electronics story to an enterprise IT upgrade story.

2. Competitive Landscape: Chipmakers Fight, TSMC Collects Tolls

The superficial narrative of AI PCs is that Arm challenges x86, but I am more concerned about where the profit pool is migrating. NVIDIA excels in GPUs and AI software stacks, AMD excels in x86 CPUs and GPU combinations, Qualcomm excels in low power and communication, and Intel excels in the existing ecosystem and enterprise channels. They each have their advantages, but the common point is clear: high-end chips cannot bypass advanced processes.

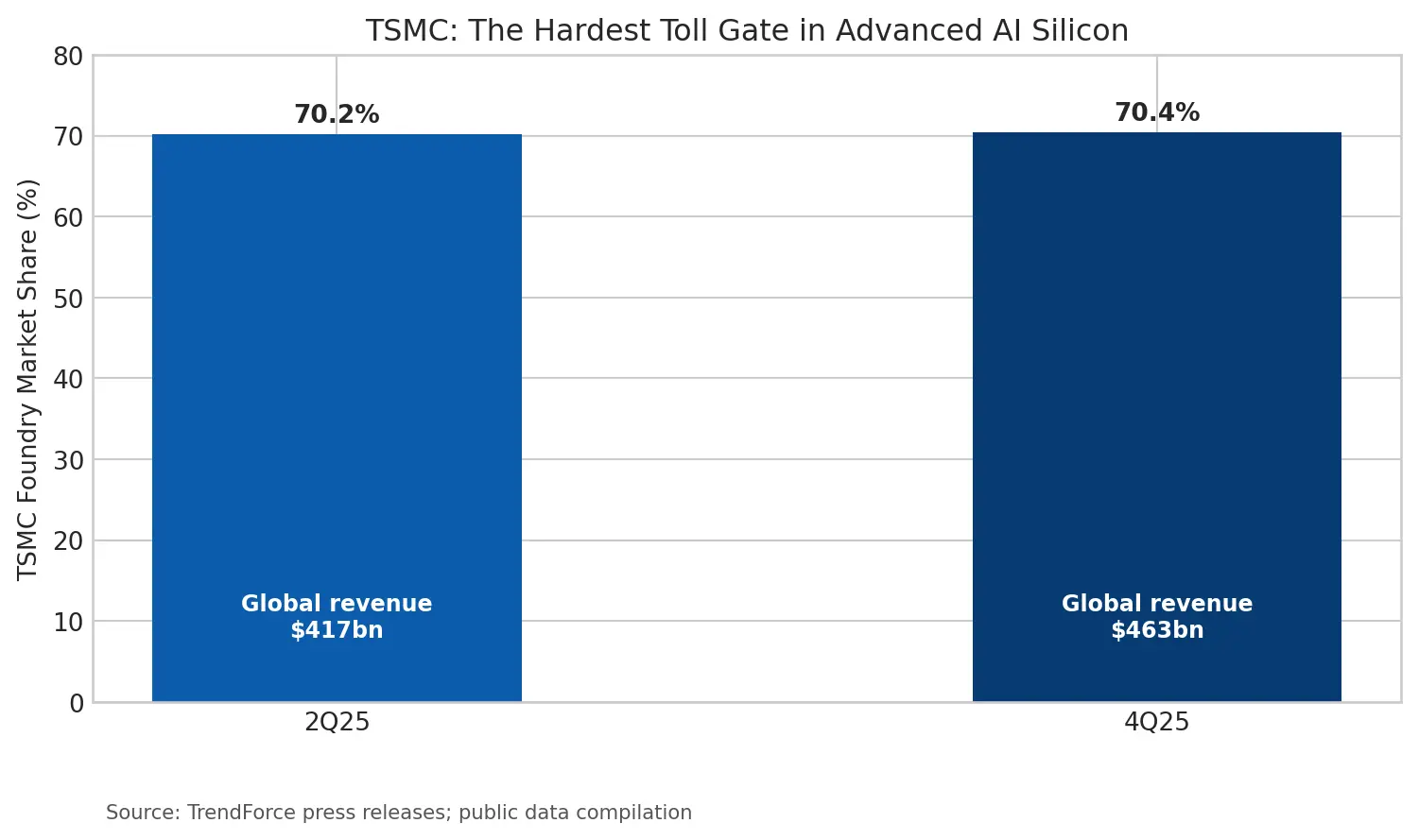

TrendForce disclosed that in Q2 2025, global foundry revenue is approximately $41.7 billion, with TSMC's share at 70.2%; in Q4 2025, global foundry revenue is approximately $46.3 billion, with TSMC's share at about 70.4%. This means that as long as AI PCs, AI servers, mobile APs, and edge AI chips continue to compete for advanced processes, TSMC is not simply a cyclical stock, but more like the toll booth entrance for the entire AI hardware era.

I do not believe that every new product launch is worth chasing, but I think that every time industry chain competition intensifies, we should ask a question in return: If the winner is still uncertain, who can charge all the winners? In the AI PC line, my answer remains advanced processes, packaging, key IP, and platform software, rather than simply betting on a single architectural slogan.

3. Target Ranking: Base Position in TSM, Offensive in AMD, Flexibility in Intel/ARM

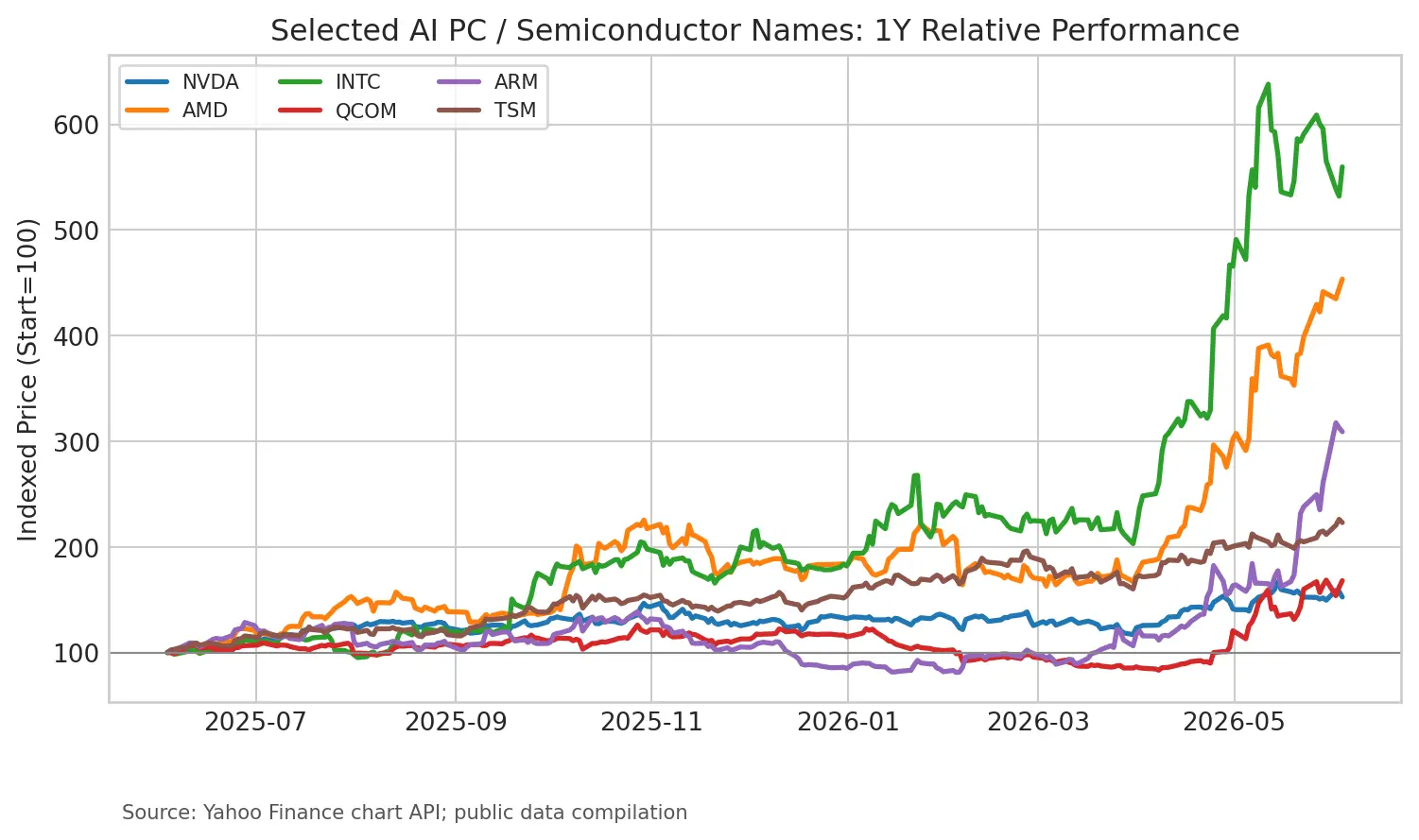

In the past year and a half, semiconductor targets have already traded ahead of AI PCs, edge AI, and computing power spillover. Yahoo Finance daily prices show that within the sample range, AMD, Intel, ARM, and TSM all have strong elasticity, but the risk-return they represent is not the same. My approach is not to buy all AI PC-related targets together, but to layer them based on certainty, valuation discipline, and industry chain position.

|--------|-----------|----------------------|-------------------------------------| | Company | Role Positioning | My Rating Preference | Core Reason | | TSM | Advanced Process Toll Booth | Strong Buy / Prefer Pullback | Not betting on architecture, benefiting from the entire industry's high-end chip capital expenditure, is the base asset I prefer to allocate long-term | | AMD | x86 Offense | Buy / Wait for Price | Participation rights in CPU, GPU, and AI PCs, suitable for offensive positions, but valuation must be disciplined | | NVDA | AI Computing Power Dominator | Hold / Do Not Chase FOMO | Strongest product power, but the emotional premium after AI PC news is not suitable for blind chasing | | QCOM | Arm PC Pioneer | Hold / Wait for Repricing | The mobile cycle, Apple risks, and the Windows competitive landscape all need market digestion | | ARM | IP Rental Platform | Buy / Small Position | Benefits from architectural diffusion, but valuation elasticity and pullback risk are also high | | INTC | Dilemma Reversal Option | Speculative Buy / Small Position | Can bet on reversal, not suitable as a core income source; position should be small, and stop-loss must be clear |

My core conclusion is simple: this is not a war where you can only buy winners, but a war where you should buy toll booths, buy platforms, and buy certainty of cash flow. If the market fully prices in emotions on the day of the news release, I would rather wait; if a pullback brings the risk-return of good companies back to a reasonable range, I will prioritize looking at TSM and AMD, followed by the flexible opportunities in ARM and Intel.

4. Risk Warning

The risks of this main line cannot be ignored:

First, AI PC applications may fall short of expectations, leading to a device replacement cycle that is not as strong as imagined.

Second, if the compatibility improvements of Windows on Arm are too slow, the narratives of Qualcomm and new entrants will be suppressed.

Third, tariffs, corporate procurement pauses, and macro uncertainties will affect PC demand.

Fourth, if there is a phase mismatch in supply and demand for advanced processes, TSMC may also experience valuation pullbacks.

Fifth, the entire AI chain's valuation is relatively high; once U.S. stock risk appetite declines, the most elastic targets often retract the fastest.

Therefore, I prefer to view AI PCs as a long-term industrial migration rather than a short-term news trade. The truly professional way to invest is not to buy slogans on the day of the release but to wait for the emotional tide to recede and then buy ecosystems, buy toll booths, and buy companies that can continuously deliver cash flow.

5. Data Source Explanation

|---------------|-------------------------|----------------------------| | Charts/Information | Main Source | Usage | | AI PC Shipment Volume and Penetration Rate | Gartner 2024 and 2025 Press Releases | Used to judge the short-term rhythm and long-term standardization trend of AI PCs | | Foundry Revenue and TSMC Share | TrendForce 2025 and 2026 Press Releases | Used to verify the logic of advanced process toll booths | | Individual Stock Price Relative Performance | Yahoo Finance chart API | Used to observe the phase market pricing of AI PCs and semiconductor-related targets | | Industry Chain Relationship Diagram | Company public disclosures, industry research, and public data compilation | Used to express the value chain relationships between architecture, chips, foundries, software, and terminals |

Data References

|----|------------------------------------|---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------| | No. | Source | Link | | 1 | Gartner: AI PC Shipment Forecast for 2025 in September 2024 | https://www.gartner.com/en/newsroom/press-releases/2024-09-25-gartner-forecasts-worldwide-shipments-of-artificial-intelligence-pcs-to-account-for-43-percent-of-all-pcs-in-2025 | | 2 | Gartner: Update on AI PC Market Share Forecast for 2025 in August 2025 | https://www.gartner.com/en/newsroom/press-releases/2025-08-28-gartner-says-artificial-intelligence-pcs-will-represent-31-percent-of-worldwide-pc-market-by-the-end-of-2025 | | 3 | TrendForce: Global Foundry Revenue and TSMC Share in Q2 2025 | https://www.trendforce.com/presscenter/news/20250901-12691.html | | 4 | TrendForce: Global Foundry Revenue and TSMC Share in Q4 2025 | https://www.trendforce.com/presscenter/news/20260312-12965.html | | 5 | Yahoo Finance: Relevant U.S. Stock Daily Price Data | https://finance.yahoo.com/ |

This report is compiled by a special analyst. The views expressed in the report represent the author's personal stance and do not represent the views of the BIT platform. This material is for reference only and does not constitute investment advice.

Risk warning

Risk warning