Bitget UEX Daily Report|Korean media's small essay collapses storage? Google included in the Dow Jones components; Micron's financial report is about to be released

Bitget UEX Daily Report

Bitget UEX Daily ReportI. Hot News

Federal Reserve Dynamics US June PMI preliminary value exceeds expectations, employment indicators weak

- Composite PMI preliminary value rises to 52.2, manufacturing PMI reaches 55.7 (a 49-month high), but the employment sub-index falls to a six-year low.

- Service sector PMI moderately rebounds to 51.3, corporate inventory procurement reaches a historical second-high. Market impact: The data reflects economic resilience but shows employment pressure, reinforcing the Federal Reserve's dual focus on inflation and the labor market, which may affect future policy path expectations.

International Commodities Strait of Hormuz reopened, Middle Eastern crude oil supply returns

- After the strait reopened, Middle Eastern crude oil accelerates into the European market, with North Sea Brent crude benchmark prices falling to a two-year low.

- Concerns over oversupply intensify, with sources in the Atlantic basin adding up. Market impact: Oil prices are under downward pressure, highlighting the direct impact of geopolitical easing on energy supply and demand, which is bearish for crude oil in the short term but alleviates inflation pressure.

Macroeconomic Policy Korean tax reform discussions trigger stock market crash, storage chip rumors exacerbate corrections

- South Korea's multi-party discussions include unrealized stock gains in comprehensive taxation, triggering a KOSPI circuit breaker, with Samsung and SK Hynix leading the decline.

- Korean media reports that SK Hynix is slowing down HBM4 expansion and shifting to general DRAM, affected by Nvidia's Rubin production cut expectations. Market impact: Policy uncertainty and industry chain rumors combine to drag down global storage and semiconductor sectors, highlighting the transmission effect of regional policies on the global tech supply chain.

II. Market Review

Commodity & Forex Performance

- Spot Gold: Approximately $4,090/ounce, -0.34%

- Spot Silver: Approximately $61/ounce, -0.33%

- WTI Crude Oil: Approximately $72.5/barrel, -0.79%

- Brent Crude Oil: Approximately $76.4/barrel, -0.87%

- US Dollar Index (DXY): 101.427 points, +0.05%

Driving Factors Analysis: The reopening of the Strait of Hormuz combined with the resumption of Middle Eastern crude oil exacerbates oversupply in the European market, with North Sea benchmark oil prices falling to low levels, putting overall pressure on oil prices. The US dollar index remains high, influenced by potential hawkish signals from the Federal Reserve and employment data, suppressing precious metal prices. Gold and silver soften amid a stronger dollar and fluctuations in risk sentiment, but geopolitical easing alleviates some safe-haven demand. Institutional views suggest that short-term supply-demand imbalances and macro policy expectations will continue to dominate correlations, with downward pressure on oil prices potentially further alleviating global inflation, while precious metals lack strong upward momentum in the short term.

Cryptocurrency Performance

- BTC: Approximately $62,866, -2.17%

- ETH: Approximately $1,667, -3.8%

- Total Cryptocurrency Market Cap: Approximately $2.24 trillion, -1.9%

- Market Liquidation Situation: Total liquidation in 24h approximately $559 million, with long positions liquidated at $493 million.

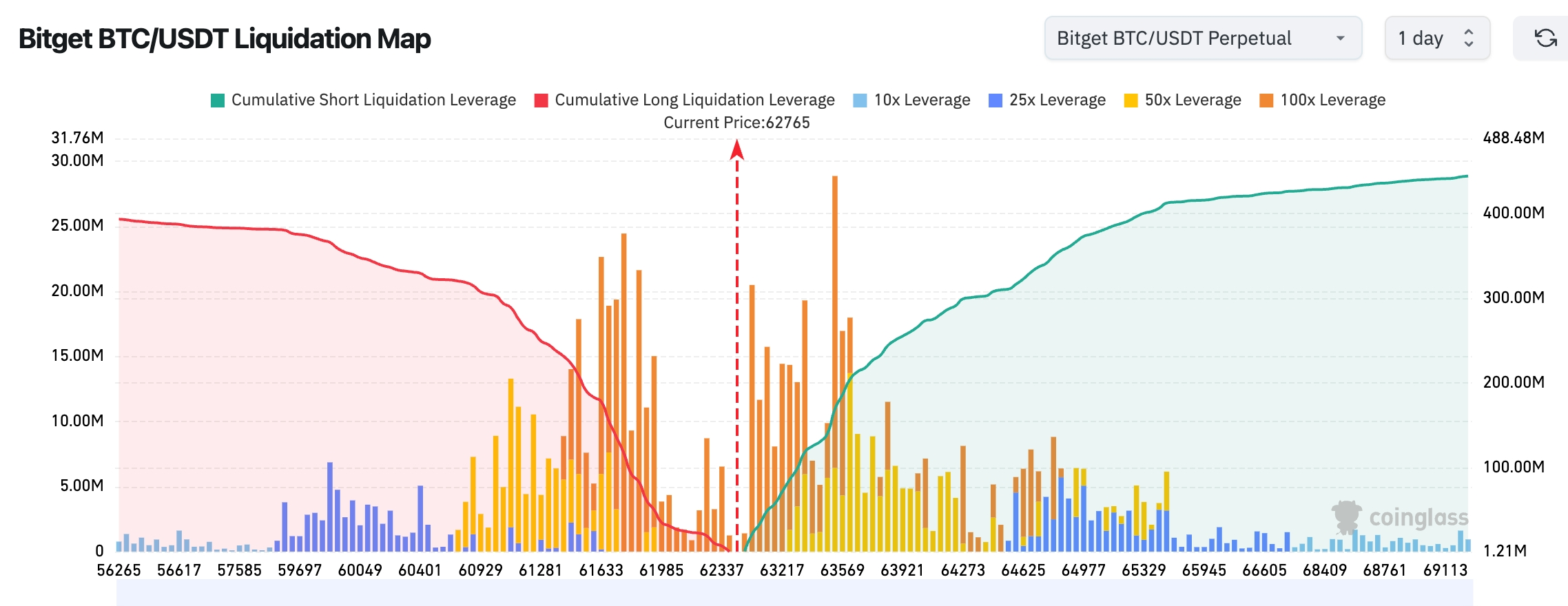

- Bitget BTC/USDT Liquidation Map: Current BTC price is approximately $62,765, with a large number of long liquidation chips concentrated in the $61,500-$62,500 range. If the price continues to pull back, it may trigger concentrated stop-losses among long positions and amplify downward volatility. There is strong short liquidation pressure in the $63,500-$65,000 range, with the highest concentration of liquidations near $63,500. If the price breaks through this area, it may trigger short squeezes and push BTC further upward.

- Spot ETF Net Inflow/Outflow: BTC spot ETF saw a net outflow of $68.3 million yesterday.

Driving Factors Analysis: The pullback in the US tech sector spills over into the crypto market, with rumors about storage chips exacerbating risk aversion. BTC/ETH are under pressure simultaneously, but BTC remains relatively stable. Liquidations are mainly from long positions, indicating that high-level holdings are under test; ETFs still show slight net inflows, indicating institutional support. Macro-wise, the strong dollar and geopolitical easing work together, testing key technical support. Institutional consensus suggests that short-term volatility is increasing, but the long-term trend of capital inflows remains unchanged, with attention on ETF dynamics and macro data guiding risk assets.

US Stock Index Performance

- Dow Jones: Closed at approximately 51,667 points (-0.09%)

- S&P 500: Closed at approximately 7,365 points (-1.44%)

- Nasdaq: Closed at approximately 25,587 points (-2.21%)

Tech Giants Dynamics

- NVDA: $200.04 (-4.13%)

- AAPL: $294.30 (-0.91%)

- MSFT: $373.94 (+1.80%)

- GOOGL: $346.13 (-0.98%)

- AMZN: $234.11 (+0.57%)

- META: $562.20 (-0.29%)

- TSLA: $381.61 (-5.79%)

Performance Summary and Driving Analysis: Tech giants are generally under pressure, with the Nasdaq showing significant pullback, mainly due to storage chip rumors and widespread declines in the semiconductor sector (Philadelphia Semiconductor Index plummeting). Google's inclusion in the Dow is more of a symbolic adjustment; individual stocks show clear differentiation, with TSLA supported by specific news, while NVDA/GOOGL are dragged down by industry chain concerns. The long-term logic of AI demand remains unchanged, but short-term high valuations and rumors amplify volatility, with the market focusing on Micron's earnings report as a catalyst.

Overview of Cryptocurrency Stock Derivatives

24H Total Transaction Volume: $23.338 billion (+49.76%)

Total Open Interest: $5.023 billion (-6.82%)

24H Total Liquidation: $49.498 million

Proportion: Transaction Volume 13.02%, Open Interest 4.73%, Liquidation 8.85%

Sector Open Interest Performance (Main Sectors)

Technology: $2.606 billion

Finance: $158 million

Consumer: $81.46 million

Industrial: $30.26 million

Biotechnology: $14.93 million

Trend Observation: The technology sector still holds an absolute dominant position, but overall market open interest has decreased by 6.82%, indicating signs of profit-taking or declining risk appetite amid active trading.

Market Heatmap (Open Interest Focus)

Top Asset Open Interest Rankings (in hundreds of millions):

SPCX: $675 million ------ Currently the largest open interest scale

MU: $451 million

SKHX: $396 million

SNDK: $289 million

NVDA: $220 million

INTC: $167 million

MRVL: $147 million

GOOGL: $109 million

CRCL: $102 million

MSFT: $97 million

MSTR: $86 million

TSLA: $81 million

BZ: $65 million

In terms of capital flow, SPCX, GOOGL, MSFT, NBIS, and other targets show signs of increased positions; MU, SKHX, SNDK, NVDA, INTC, MRVL, CRCL, MSTR, and other targets show reductions or capital outflows.

Sector Activity Observation Semiconductor/Storage Sector significantly declines (Philadelphia Semiconductor Index falls about 7-8%)

- Representative Stocks: Micron Technology (MU), SanDisk (WDC), etc., fall over 13%, with SK Hynix (related ADR) leading the decline, ARM, Qualcomm, Western Digital, Applied Materials, etc., fall by more than 7-10%, Nvidia (NVDA) falls about 4%, AMD falls over 5%.

- Driving Factors: Multiple negative factors amplify market concerns. First, a policy document discussed by South Korean multi-party lawmakers to include unrealized stock gains in the comprehensive tax system directly triggers a KOSPI circuit breaker, with major stocks like Samsung Electronics and SK Hynix plummeting, raising market fears that this policy, if advanced, will dampen enthusiasm for high-valuation tech investments. Second, Korean media reports that SK Hynix is slowing down the pace of HBM4 mass production expansion and shifting resources to general DRAM, mainly due to continued downward adjustments in Nvidia's next-generation Rubin platform production forecasts. This "small essay" was quickly reprinted by international media such as Bloomberg and CNBC, with traders pointing to uncertainties in the demand outlook for high-end AI storage.

In-Depth Analysis: HBM, as a core bottleneck resource for AI training and inference, was previously expected to support high growth and margin expansion for storage giants due to supply tightness. However, signals of slowed expansion combined with adjustments in Nvidia's demand guidance have raised widespread doubts about whether the peak of AI capital expenditure in the second half of 2026 will arrive early or slow down. This industry chain transmission effect not only impacts the storage sector but also spills over to the entire semiconductor ecosystem, leading to concentrated profit-taking in high-valuation AI hardware stocks. In the short term, the sector's valuation is under significant pressure; in the medium term, if upcoming earnings reports from Micron and others can provide positive guidance (such as increased HBM market share or healthy inventory), it may alleviate some pessimistic sentiment, but geopolitical policy uncertainties and the macro interest rate environment will still constrain the rebound strength. Investors need to closely track actual shipment data from the supply chain and capital expenditure plans from major clients to distinguish between cyclical fluctuations and structural opportunities.

III. In-Depth Analysis of US Stocks

1. Alphabet (GOOGL) - Included in Dow Components Event Overview: S&P Dow Jones Indices officially announced that Google's parent company Alphabet Class A shares (GOOGL) will be included in the Dow Jones Industrial Average (Dow), replacing long-time member Verizon Communications. This adjustment also involves changes to other indices, including Honeywell Aerospace being included in the S&P 500 while remaining in the Dow, and IES and Toast being replaced in the S&P MidCap Index. Alphabet had previously completed a 1-for-20 stock split in 2022, significantly reducing the risk of high stock prices distorting the index's price-weighted mechanism. Market Interpretation: Several institutions point out that this inclusion is not only a technical adjustment of the index but also profoundly reflects the structural shift in the US corporate landscape from traditional telecommunications to tech giants. As a price-weighted index, the weight of Alphabet will be lower than its market capitalization-weighted influence in the S&P 500 or Nasdaq 100; the scale of passive funds tracking the Dow is relatively limited, and the actual impact of capital rebalancing is expected to be moderate, mainly symbolic. However, it marks that the blue-chip index has finally fully embraced the leaders of the AI and digital economy era. Investment Insight: The short-term market reaction may be relatively muted, with a focus on capital flow and sector sentiment; in the long term, it helps enhance Alphabet's attractiveness in allocation among traditional investors, strengthening the tech weight in blue-chip portfolios, suggesting tracking its valuation expansion potential in conjunction with AI search and cloud business growth.

2. Cerebras Systems - Stock Plummets Over 10% After Earnings Report Event Overview: AI chip startup Cerebras Systems released its Q1 FY2026 results, with revenue reaching $194.3 million, a 94% year-on-year increase, but a loss of $0.22 per share. After the earnings announcement, the stock price fell sharply by over 10%, continuing the overall weakness in the semiconductor sector. Market Interpretation: As a "challenger to Nvidia," Cerebras demonstrates innovative advantages in wafer-scale engine technology, but high growth accompanied by ongoing losses raises investor concerns about the path to profitability and cash burn rate. Combined with rumors of SK Hynix slowing HBM production expansion and adjustments in Nvidia's Rubin expectations, the short-term demand outlook for the entire AI hardware ecosystem is questioned, amplifying systemic correction pressure in the sector. Investment Insight: Competition in AI infrastructure is entering a heated stage, and short-term profit fluctuations are normal; investors who are optimistic about its technological barriers and vertical integration capabilities can gradually position themselves during corrections, but must closely monitor subsequent improvements in gross margins and progress with major clients to avoid high valuation risks.

3. SpaceX - Plans to Issue $25 Billion in Bonds Event Overview: SpaceX has launched its first public bond issuance plan, aiming to raise $25 billion, with bond terms ranging from 5 to 30 years. This move aims to test fixed-income investors' confidence in its ambitious plans for rocket manufacturing, Starlink, and AI-related projects, currently attracting nearly $90 billion in subscription orders. Market Interpretation: Investment bankers believe this is an important indicator for SpaceX's future financing transactions. Despite the current pullback in tech stocks and pressure from the interest rate environment, strong subscriptions show that investors still have confidence in the long-term growth potential of Musk's businesses, especially the scaling of Starlink and potential synergies with AI data centers. Banks hope to establish a good market impression to pave the way for future refinancing. Investment Insight: A successful bond issuance will further solidify the company's valuation foundation and optimize its capital structure; investors should pay attention to potential strategic synergies with Tesla (such as merger discussions) and the cash flow support of Starlink for the overall group, suitable for long-term aerospace and emerging technology themes.

4. Micron Technology (MU) - Key Focus Ahead of Earnings Report Event Overview: Storage chip giant Micron Technology (MU) will announce its latest quarterly results after the US market closes, with the market highly focused on its HBM and DRAM business performance under AI demand, as well as inventory reduction and gross margin recovery. The sector has already seen significant pullbacks due to rumors of SK Hynix slowing production expansion. Market Interpretation: Institutions generally expect that as a key player in the memory sector, Micron's performance will directly test the real strength of AI capital expenditures. Against the backdrop of tight supply for high-bandwidth memory (HBM), if guidance is optimistic or inventory improves, it will alleviate market concerns about the peak of storage demand; conversely, it may further suppress semiconductor valuations. Analysts emphasize the need to distinguish between cyclical recovery and the contributions of AI structural growth. Investment Insight: The earnings report will become a short-term catalyst for the sector, suggesting attention to HBM market share increases and gross margin guidance; for investors optimistic about the memory cycle's upward trend, the current pullback may provide a strategic entry window, but macro and geopolitical variables should be monitored for interference.

5. Microsoft (MSFT) - Wisconsin Data Center Commences Operations Event Overview: Microsoft announced that its first data center in Mount Pleasant, Wisconsin, is now fully operational, currently employing nearly 550 full-time staff, and plans to invest $4.7 billion in large-scale projects in the state between 2024 and 2028. This facility completed equipment onboarding in April this year and is an important milestone in Microsoft's AI and cloud infrastructure expansion. Market Interpretation: Institutions believe this move highlights Microsoft's heavy investment in AI infrastructure, forming a closed loop with Azure cloud services and OpenAI collaboration. The operation of the data center will enhance computing power supply capacity, supporting enterprise-level AI demand growth, but during the high investment period, attention must still be paid to capital return rates and energy cost pressures. Overall, it aligns with the trend of tech giants' AI capital expenditures. Investment Insight: Long-term positive for accelerating cloud and AI business revenue, suggesting tracking subsequent utilization rates and revenue conversion efficiency; as a defensive tech giant, MSFT provides relative stability amid sector volatility, suitable for core holding allocation.

IV. Cryptocurrency Project Dynamics

Ben Slavin, global ETF head at Bank of New York Mellon (BNY), stated that asset managers are accelerating the advancement of tokenized ETF plans, driven mainly by investor demand and the "FOMO" sentiment of fearing to miss early opportunities in blockchain finance.

The US House of Representatives passed housing legislation with a vote of 358 to 32, which includes a temporary ban on central bank digital currencies (CBDC) lasting until 2030. The bill has now been sent to President Trump for signing. Previously, the US Senate passed a housing bill that includes a four-year ban on the Federal Reserve's CBDC.

Opinion: Trump's latest executive order may accelerate the development of post-quantum cryptography, benefiting the cryptocurrency industry.

CryptoQuant suggests that Strategy should pause Bitcoin purchases and prioritize rebuilding cash reserves. It recommends that Strategy should halt coin purchases until cash reserves and dividends are restored, and establish a systematic timing model to avoid the market impression of "always buying at local highs," while also formulating a reduction framework in the future bull market to realize profits, reduce leverage, and reserve cash for downturn cycles. Moreno emphasizes that Strategy currently holds unrealized losses of about $10.6 billion in Bitcoin, and forced sales would massively realize losses and harm shareholder value; the company could convey its ability to fulfill obligations by increasing dividend rates or issuing MSTR stock.

SpaceX is preparing for its first bond issuance, planning to raise $25 billion; this move aims to test fixed-income investors' confidence in Elon Musk's ambitious plans for the company's future.

The Ethereum Foundation (EF) announced the completion of organizational restructuring, reducing its workforce by about 20%, with 54 employees leaving, and establishing five major business clusters: protocol layer, access layer, user layer, community layer, and institutional layer.

V. Today's Market Calendar

Data Release Schedule

|-------|----|----------------|-----| | 01:50 | Japan | BoJ Monetary Policy Meeting Summary | ⭐⭐⭐ | | 10:00 | US | New Home Sales (May) | ⭐⭐⭐ | | 10:00 | US | Leading Economic Indicators (May) | ⭐⭐ |

Important Event Forecast

June 24 (Wednesday)

- US Economic Data: May new home sales, leading indicators, etc.

- US Stock Earnings: Micron Technology (MU) heavy earnings report after hours (leading storage chip company, key verification of AI server HBM demand); Trip.com Group (TCOM), etc.★★★★

- Other Highlights: Nvidia (NVDA) shareholder meeting (9:00 AM Pacific Time, focusing on Blackwell and Vera architecture capacity ramp-up, AI infrastructure outlook).

June 25 (Thursday)

- US Economic Data: May PCE Price Index (the Federal Reserve's preferred inflation indicator, core PCE expected to rise 0.3% month-on-month); Q1 GDP final value (expected to remain at 1.6%); durable goods orders, initial jobless claims, etc. (data-intensive day).★★★★

- US Stock Earnings: Blackberry (BB) earnings before market opens.

June 26 (Friday)

- US Economic Data: University of Michigan Consumer Sentiment Index final value; Federal Reserve officials' speeches (Williams, Kashkari, etc.).

Institutional Views: Well-known investment bank analysts believe that although the Nasdaq was pressured by semiconductor pullbacks yesterday, the Dow remains relatively resilient, reflecting market support for non-tech blue chips. The easing of tensions between the US and Iran is favorable for energy stability, with oil prices declining in the short term but long-term demand still present. The cryptocurrency market fluctuates with risk assets, with slight inflows into ETFs providing a buffer. Overall, the long-term narrative of AI remains unchanged, with analysts raising the S&P target to the 8000+ point range, suggesting attention to earnings season catalysts and macro data validating valuation pressures. High-valuation sectors are experiencing increased short-term volatility, but institutions still see structural opportunities in tech and crypto.

Disclaimer: The above content is compiled by AI search, with human verification for publication, and is not intended as any investment advice. The data in the text may inevitably contain deviations; please refer to real-time market data.

Risk warning

Risk warning