CPI data suggests a bull market has returned, but the options market says not to rush to pop the champagne

The 3.5% CPI data indeed provides an outlet for the current tense market sentiment. In the short term, U.S. stocks and cryptocurrencies are likely to gain a relatively calm window period thanks to this data.

The 3.5% CPI data indeed provides an outlet for the current tense market sentiment. In the short term, U.S. stocks and cryptocurrencies are likely to gain a relatively calm window period thanks to this data.Yesterday's CPI data from the United States relieved the entire risk asset market.

The annual CPI for June in the U.S. recorded 3.5%, which not only fell below the market consensus expectation of 3.8% but was also significantly lower than the previous value of 4.2%. This unexpected cooling effect almost instantly reversed the tightening panic that had previously loomed over the market. Traders quickly adjusted their pricing for the Federal Reserve's interest rate hikes within the year, the dollar weakened, and both U.S. stocks and cryptocurrencies surged in unison.

By the close, the Nasdaq index rose about 0.9%, Bitcoin rebounded from around $62,000 to near $65,000, and U.S. stock SK Hynix staged a dramatic "comeback"—soaring 27% in a single day, sweeping away the gloom of the previous two days.

A company with a market value exceeding one trillion dollars increased by 27% in one day. This is not the performance of blue-chip stocks; this is the performance of meme coins. The extreme swings in market sentiment were vividly illustrated by Hynix's candlestick chart.

While the favorable data is certainly pleasing, risk assets are likely to catch a breather in the short term. However, if we shift our perspective from candlesticks to the underlying signals in the options market, the medium to long-term risks may not have been completely eliminated by this CPI report.

1. The Federal Reserve's Stance: Single Month Data is Not Enough, "Zero Tolerance" Position Remains Unchanged

Shortly after the CPI data was released, Federal Reserve Chairman Waller made his first public appearance at a congressional hearing. The market was all ears for every word from this new chairman.

The message he conveyed was far more severe than the CPI numbers themselves.

Waller clearly stated that the Federal Reserve has a "zero tolerance" for persistently high inflation. He bluntly defined the past five years of inflation remaining above the 2% target as "the Fed's dereliction of duty" and emphasized that the judgment would not change due to a single month's improvement in CPI data.

To translate: even though a 3.5% CPI looks good, there is still a long way to go before the Federal Reserve considers its "mission accomplished."

What does this mean? It means that the market's "rate cut euphoria" may have popped the champagne too early. The Federal Reserve's decision-making framework will not undergo a fundamental shift due to one data point cooling. If inflation fluctuates in the following months, Waller's hawkish stance may re-emerge at any time. A 3.5% CPI provides the market with a breathing window, but it does not equate to a "the Fed has already turned" pass.

2. The Pressure of Inflation Has Not Been Relieved

The cooling of the CPI number is one thing; whether the underlying drivers of inflation have truly faded is another.

First, the geopolitical situation in the Middle East has heated up again. The U.S.-Iran conflict has recently escalated, with Trump announcing a renewed blockade of Iranian ports. Any risk involving disruptions to the supply from the Strait of Hormuz or Middle Eastern oil-producing countries could push oil prices higher in the short term, thereby transmitting to global inflation expectations.

Second, oil prices have remained high for a long time. WTI crude oil is currently hovering around $80 per barrel. The transmission of oil prices to CPI has a lag effect—the current $80 oil price may only gradually show its complete impact on inflation in the data for the next one to two months. In other words, while the CPI data released in July looks good, it does not guarantee that the data for August and September will also look good.

If geopolitical conflicts further push up oil prices, combined with the fading base effect, the inflation path for the second half of the year still has the potential for fluctuations.

3. What is the Options Market Saying?

The favorable CPI has driven both stock and cryptocurrency prices up, but if you look at the implied volatility structure in the options market, you will find a disturbing divergence.

SK Hynix: Recent IV Far Higher Than Long-Term

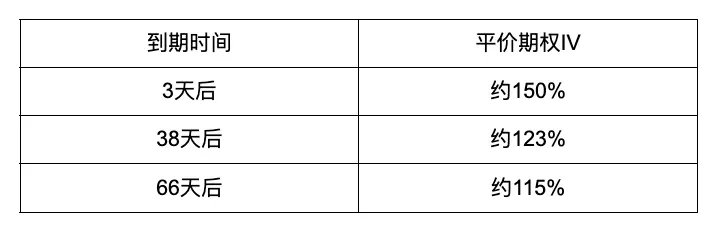

The implied volatility (IV) of Hynix's current options has surged to around 181%—an extreme and almost crazy number, typically seen only in highly speculative small stocks or on the eve of major events.

More critically is the term structure: the IV of near-term options is significantly higher than that of long-term options. The specific data is as follows:

What does this "near high, far low" term structure mean?

It means that the options market is pricing a judgment with real money: Hynix is likely to be impacted by certain news in the short term (within days to a couple of weeks), leading to significant price volatility. However, from a medium to long-term perspective, there is a lack of further driving force to sustain the rise in stock prices.

The recent high IV reflects "event risk"—it could be earnings reports, macro data, or geopolitical upheaval. The decline in long-term IV indicates that options traders believe these shocks are short-term and non-trend-based. In the medium to long term, Hynix's stock price seems to lack upward momentum.

Bitcoin Options: The Same Script

The options structure for Bitcoin also shows an almost identical pattern.

Although the favorable CPI pushed BTC prices from $62,000 to $65,000, the response from the options market was quite restrained:

Near-term options IV: Slightly increased to about 35%

Long-term options IV: Maintained at 32%-33%, showing almost no improvement

What does this mean? It means that options traders believe the upward potential for BTC is catalyzed by the CPI data in the short term, but from a medium to long-term perspective, the market does not see Bitcoin having the momentum for a sustained significant breakthrough. The low long-term IV reflects a lack of strong directional judgment on the mid-term trend.

4. In Conclusion: Short-Term Relief, Medium to Long-Term Caution

Overall, the 3.5% CPI data indeed provides a release valve for the currently tense market sentiment. In the short term, U.S. stocks and cryptocurrencies are likely to gain a relatively calm window thanks to this data.

However, from a medium to long-term perspective, several key variables have not been resolved:

The Federal Reserve's "zero tolerance" stance has not changed; single month data is insufficient to make it relent.

Geopolitical conflicts and high oil prices remain potential catalysts for a resurgence of inflation.

The term structure in the options market indicates high volatility risk in the short term, but insufficient upward driving force in the medium to long term.

Short-term relief is possible, but medium to long-term risks have not truly been alleviated.

For investors looking to position themselves in the current environment, the BIT brokerage platform offers a toolbox for two-way operations:

Financing to go long: If you believe the CPI cooling trend will continue and risk assets still have room for recovery—BIT provides interest-free intraday financing and interest-free financing within a $20,000 limit overnight.

Margin trading to go short: If you believe market sentiment is overly optimistic and the rebound of chip stocks and cryptocurrencies is unsustainable—BIT's margin trading function offers a limited-time $0 fee rate (until July 31), allowing you to explore bearish directions at low cost.

While the CPI data brings short-term relief, do not forget to leave a retreat route for medium to long-term uncertainties.

Disclaimer: This article is written by an external author and represents the author's personal views, not the official position of BIT. BIT has not independently verified the data and analysis in this article and does not constitute investment advice or solicitation. Margin trading involves leverage and short-selling mechanisms, which may lead to losses exceeding the principal and carries the risk of forced liquidation. Promotional rates are only valid during the activity period, specific to what is displayed in the BIT App, and may be adjusted after the activity ends. U.S. stock investment access must comply with qualifications and regulations of the jurisdiction. Past performance does not guarantee future returns; please make prudent decisions after fully understanding the risks.

Risk warning

Risk warning