June CPI is out: The thunder didn't strike, but the reversal hasn't stopped yet

The May CPI removed the "core inflation out of control, immediate rate hike in June" risk, but it did not completely stabilize the decline of the US stock market; now is not the time to fully chase the rebound, but rather to gradually position and retain the strong while waiting for the FOMC outcome.

The May CPI removed the "core inflation out of control, immediate rate hike in June" risk, but it did not completely stabilize the decline of the US stock market; now is not the time to fully chase the rebound, but rather to gradually position and retain the strong while waiting for the FOMC outcome.June CPI Released: No Explosion, But the Reversal Hasn't Stopped

Roger Lee | BIT U.S. Stock Special Analyst: With 21 years of experience in investment banking, asset management, and financial institutions, focusing on the AI industry chain, U.S. macro liquidity, and options strategy research.

Investment Summary

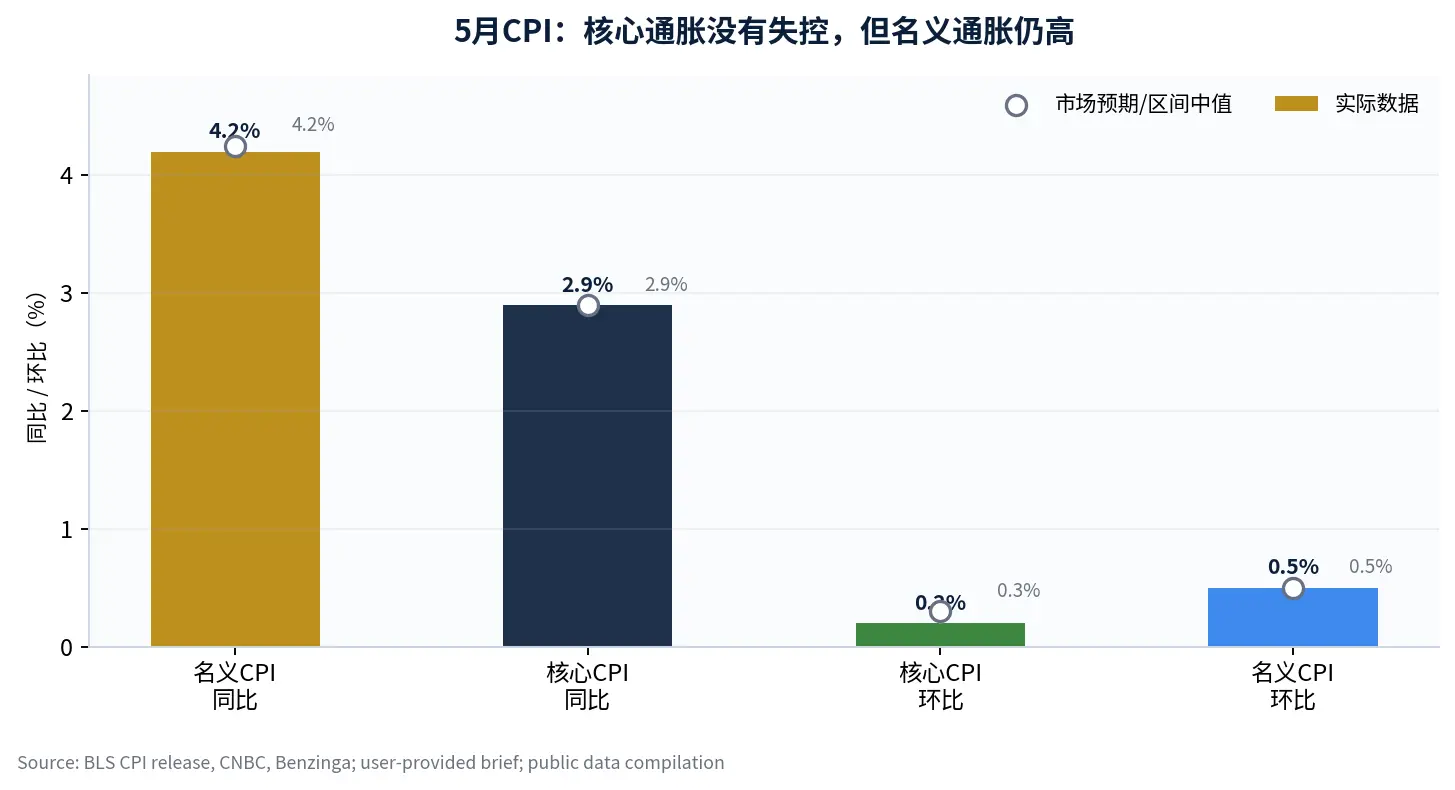

My conclusion is straightforward: The May CPI has defused the "core inflation out of control, immediate rate hike in June" bomb, but it hasn't completely stabilized the reversal in U.S. stocks; now is not the time to go all in on the rebound, but rather to use a phased approach and wait for the FOMC outcome. This statement is the core of my view on last night's market reaction. The U.S. May nominal CPI year-on-year is 4.2%, core CPI year-on-year is 2.9%, and core CPI month-on-month is only 0.2%. The data itself does not confirm the "second wave of inflation out of control"; however, the nominal CPI still reached a three-year high, and energy items and geopolitical conflicts continue to pressure the bond market in a hawkish direction, causing the market not to directly translate the positive CPI into a significant stock market rally.[1] [2]

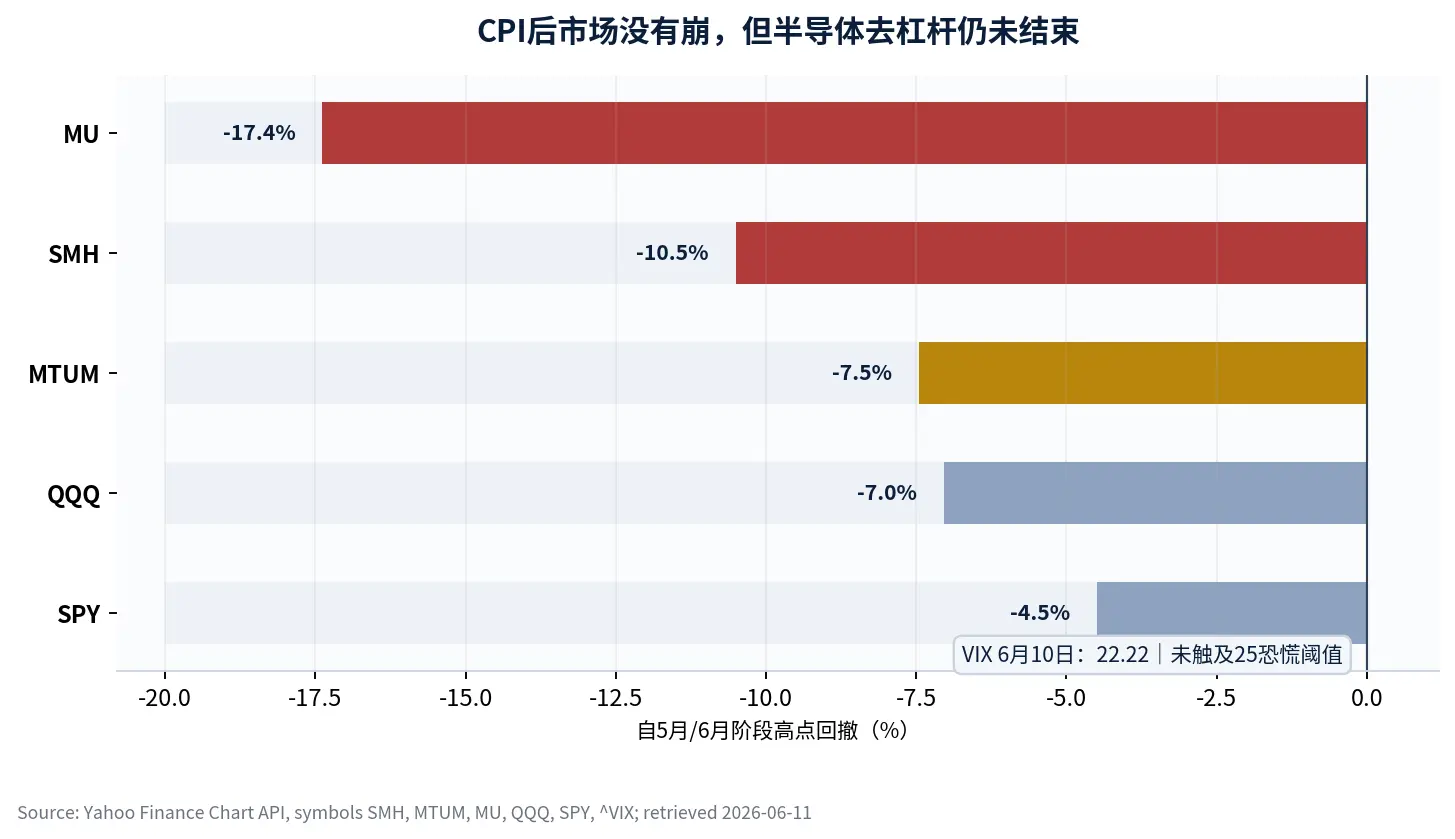

I believe the current market is not about "buying blindly after all bad news is out," but rather "extreme tail risks are decreasing, but crowded trades are still actively reducing risk." SMH has retreated about 10.5% from its recent high, MU has retreated about 17.4%, MTUM has retreated about 7.5%, and VIX closed at 22.22, still not breaking the panic threshold of 25, indicating that the market is not experiencing a systemic crash, but rather that semiconductors and high Beta sectors are still deleveraging.[5]

1. Fact Judgment: CPI Didn't Explode, But Why Didn't the Market Rise

The key to the U.S. May CPI is not the nominal year-on-year figure itself, but whether core inflation is widely spreading to the service sector. The original text mentions that the nominal CPI year-on-year is 4.2%, core CPI year-on-year is 2.9%, core CPI month-on-month is 0.2%, and nominal CPI month-on-month is 0.5%. Public reports and official data indicate that energy prices are one of the core drivers of nominal inflation, while the core CPI month-on-month being below the market expectation of 0.3% means that the worst-case scenario of "oil price shocks fully spreading to the service sector" has not occurred temporarily.[1] [3]

|---------|------|-------------|---------------------------| | Indicator | Actual Data | Market Expectation/Background | My Interpretation | | Nominal CPI YoY | 4.2% | 4.2%---4.3% | High levels still pressure valuations, but not exceeding the most pessimistic expectations | | Core CPI YoY | 2.9% | Basically in line with expectations | Core inflation does not provide sufficient reason for an immediate rate hike in June | | Core CPI MoM | 0.2% | 0.3% | Pressure from service diffusion is lower than market concerns, which is the most important easing point of this data | | Nominal CPI MoM | 0.5% | 0.5% | Energy shocks exist, but no larger surprises occurred |

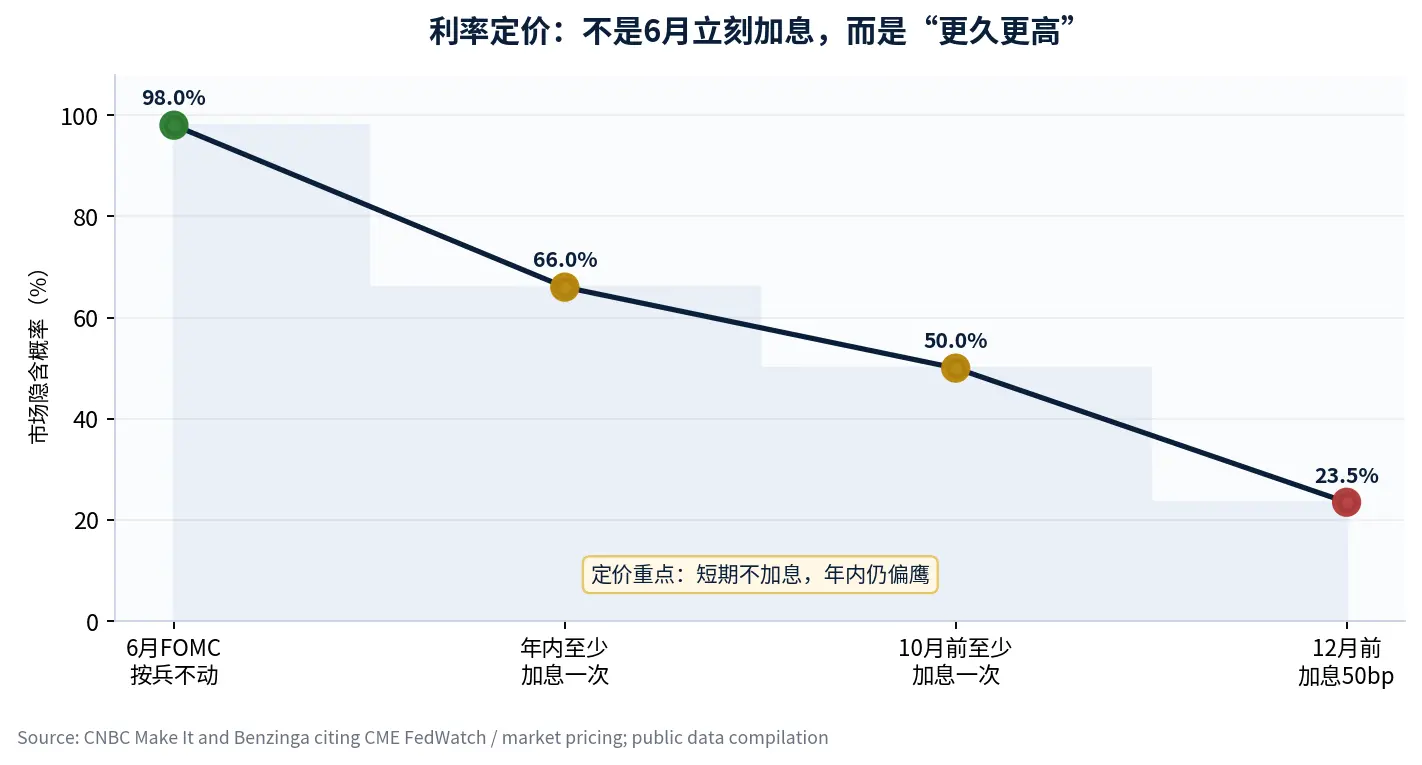

The market did not rise significantly because the stock market and bond market are looking at different things. The stock market sees that core inflation is not out of control, and the main line of AI profits has not been falsified by macro data; the bond market sees that nominal inflation is still high, oil prices and geopolitical conflicts are uncertain, and the probability of another rate hike this year has risen again. CNBC and Benzinga's reports on CME FedWatch and market pricing show that the probability of the June FOMC remaining unchanged is close to 98%, but the probability of at least one rate hike this year is about 66%, which reflects the pricing split of "no hike in the short term, higher in the long term." [2] [4]

2. Bond-Stock Split: The Real Pressure Comes from "Longer and Higher"

The implication of this CPI is not "immediate rate hike," but rather "the imagination of rate cuts continues to be suppressed." If core CPI month-on-month were significantly higher than expected, the market would directly trade for a rate hike in June or July; now this extreme scenario has been ruled out, but high nominal CPI, oil price shocks, and employment resilience still make the bond market unwilling to bet on easing prematurely. This does not harm tech stocks in terms of immediate falsification at the fundamental level, but rather constrains the discount rate on the valuation side.

|---------|--------------|----------------------------| | Pricing Variable | Current Signal | Impact on Tech Stocks | | June FOMC | High probability of remaining unchanged | Immediate rate hike tail risk decreases, favorable for short-term sentiment recovery | | Probability of Rate Hike This Year | Market pricing about 66% | Long-term valuations still under pressure, rebound space limited | | Oil Prices and Geopolitical Conflicts | Still the biggest external variable | If oil prices remain high for a long time, nominal CPI will continue to constrain the Fed | | Waller's Statement | June 18 is a key window | If only verbal hawkishness, the market can recover; if pointing to substantial rate hikes, need to reduce leverage |

My judgment is that the bond-stock split will not end in one day. The stock market can rebound due to core CPI being lower than expected, but if the 10-year U.S. Treasury yield continues to rise, or if the Fed communication turns "another rate hike" from a risk scenario into a baseline scenario, high valuation tech stocks will still be repeatedly pressured on valuations. Therefore, before the FOMC, the positive CPI should not be interpreted as "immediately going all in."

3. Semiconductor Hedge: Surge in Hedge Demand Indicates Reversal Still Unstable

The original text mentions that the inflow of SOXS funds and the increase in SMH put options transactions are the most important micro signals in the market after this CPI. My understanding is: institutions are not selling all AI assets, but are using the rebound to lock in downside risks. In other words, they acknowledge that the CPI has defused one bomb, but do not believe that the crowded positions in semiconductors have been completely cleaned out.

From the captured market data, SMH has retreated about 10.5% from its recent high as of June 10, MU has retreated about 17.4%, while MTUM has retreated about 7.5%, QQQ about 7.0%, and SPY about 4.5%, with VIX closing at 22.22.[5] This set of data indicates two things. First, the deleveraging within semiconductors is significantly deeper than the overall market; second, VIX not breaking 25 indicates that the market has not yet entered a phase of indiscriminate panic selling. For me, this is not "total destruction," but it is also not "the reversal has stabilized."

|------|--------|---------------|-------------------| | Asset | Phase Retreat | Signal Meaning | My Action | | MU | -17.4% | High Beta storage leader volatility amplified | Not chasing the rebound, waiting for FOMC and earnings expectations to stabilize | | SMH | -10.5% | Semiconductor main line is still deleveraging | Core positions should not be easily discarded, but new positions should be added in batches | | MTUM | -7.5% | Momentum assets' retreat has not yet turned panic | The market is still reducing risk, not completely clearing out | | QQQ | -7.0% | Tech index is under pressure but not in systemic collapse | Waiting for confirmation from bond yields and Fed communication | | SPY | -4.5% | The overall market's retreat is mild | Risks are concentrated in high valuations and crowded directions |

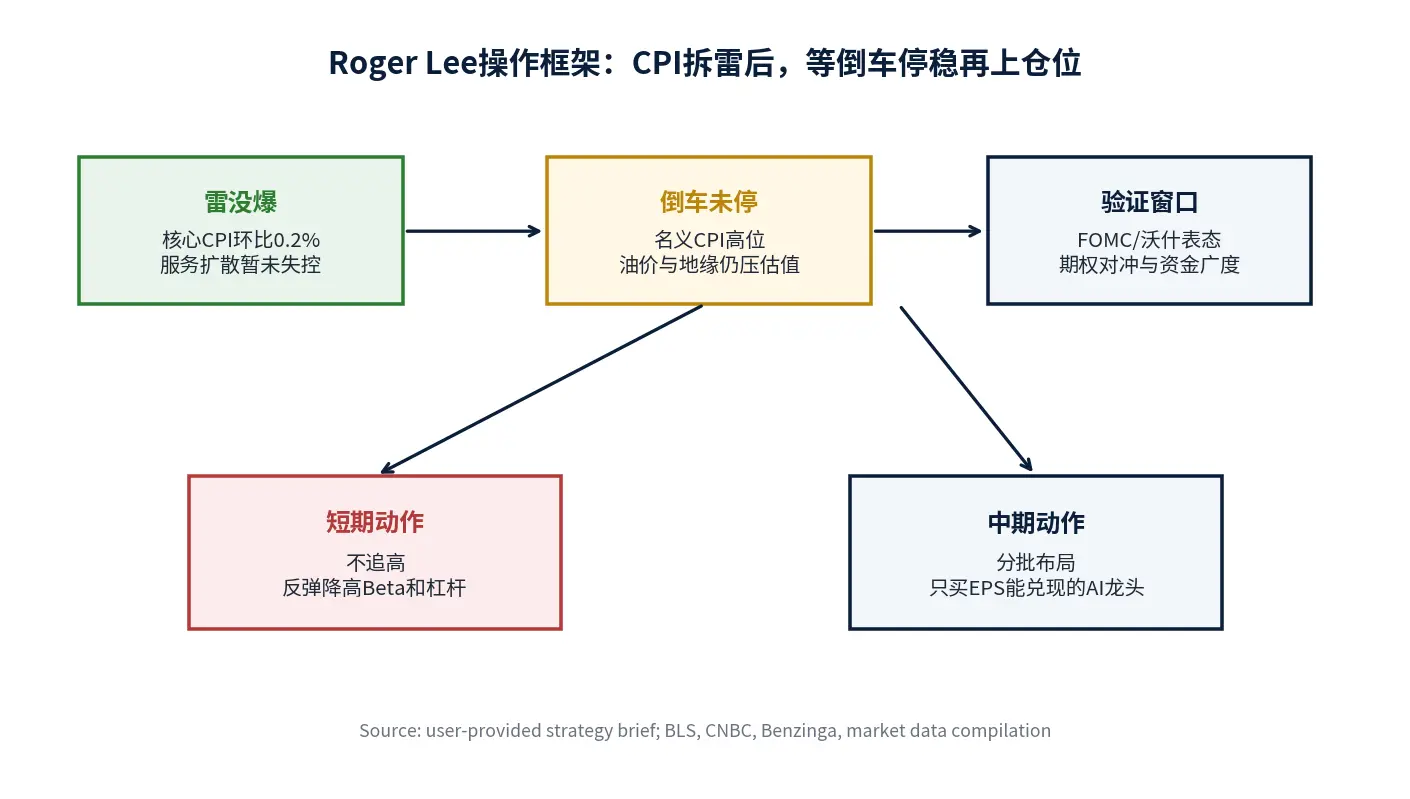

4. Operational Framework: Don't Chase Highs in the Short Term, Buy EPS in Batches in the Mid Term

I divide the next two weeks into two phases. The first phase is before the FOMC meeting, with the core task being to preserve capital and reduce noise. Since the market breadth has not shown significant recovery, and VIX has not hit panic extremes, I will not directly leverage up just because the CPI is slightly better than expected. I will reduce high Beta, high leverage semiconductor and concept tech stocks during the rebound, especially those without orders, without gross margin support, relying solely on valuation expansion.

The second phase is after the FOMC and Waller's statement, with the core task being phased positioning. The original text mentions that if investors can tolerate a market retreat of about 3%---4%, the current market has gradually entered a phased positioning range. I agree with this judgment, but the premise is to only buy AI leaders with EPS evidence, rather than buying all tech stocks that have fallen. The previous report has emphasized that the true terminator of the tech rally is industry competition and EPS falsification, not the Fed adding 25bp; after this CPI release, this framework has not changed.[6]

|-----------|-----------|----------------------|-----------------------| | Time Window | Operational Principle | Conditions for Increasing Positions | Conditions for Reducing Positions | | Before FOMC | Don't chase highs, reduce leverage | Core assets drop sharply to support zones, and interest rates do not continue to rise | Semiconductor rebounds with low volume, SOXS/put options continue to amplify | | Waller's Statement on June 18 | Wait for policy tone confirmation | Only verbal hawkishness, not pointing to substantial rate hikes | Clearly hinting at multiple rate hikes this year or an extremely hawkish dot plot | | End of June to July | Focus on EPS and earnings guidance | Cloud capital expenditures, AI orders, gross margins continue to stabilize | Order downgrades, gross margin declines, EPS upward revisions stop | | Mid-term Allocation | Phased positioning in core leaders | Can tolerate 3%---4% index fluctuations and keep enough cash | Full positions at once, chasing high Beta, ignoring oil price variables |

5. My Investment Interpretation: The Bomb Has Been Defused, But Cash Shouldn't Be Spent Too Quickly

My operational strategy is clear: the CPI has given the market a breather, but I will not misinterpret this breath as a trend that has accelerated again. For the AI core assets already held, I will not easily exit due to the fluctuations after the CPI; but for new positions, I will phase in, set limits, and wait for confirmation. Priority for positions will be given to AI infrastructure chains with high order visibility, stable gross margins, and good cash flow, especially those directly benefiting from cloud capital expenditures.

For high Beta and purely narrative varieties, I will continue to reduce positions during the rebound. Quantum, aerospace, and small chip stocks lacking a path to profit realization will find it difficult to continue expanding valuations in an environment of "high interest rates lasting longer." Once the market shifts from "talking about long-term potential" back to "looking at current EPS," these stocks will be the first to be sold.

|------|----------------|--------------|---------------------| | Portfolio Level | What I Will Keep | What I Will Reduce | Why | | Core Holdings | AI infrastructure leaders with EPS still being revised upwards | None | Industry trends remain, volatility does not equal falsification | | Satellite Holdings | High elasticity stocks with orders and customer validation | High Beta stocks with overly rapid valuation expansion | Retain elasticity, but control net exposure | | Defensive Holdings | Cash, short-term bonds, dividend stabilizers | Overcrowded defensive rebounds | Used to wait for buying points after a 3%---4% retreat | | Hedging Tools | Index protection, sector options | Naked chasing of SOXS and other high-loss tools | Hedging is insurance, not directional gambling |

6. Conclusion: The Reversal Hasn't Stopped, Don't Unbuckle Your Seatbelt Too Early

The final conclusion returns to the first sentence: The May CPI has defused the "immediate rate hike" bomb, but has not defused the "longer and higher" valuation pressure; currently, it is the beginning of a phased positioning window, not a starting gun to rush in all at once. If Waller's statement on June 18 is merely verbal hawkishness, core inflation continues to remain controllable, and AI EPS and orders are not downgraded, I will treat this round of retreat as a mid-term positioning opportunity. Conversely, if oil prices continue to rise, the dot plot becomes more hawkish, and semiconductor hedge demand does not decrease but increases, I will continue to keep positions within a tolerable range of fluctuations.

In summary: The CPI has given the market a breather, but the reversal hasn't stabilized yet. Don't rush to go all in; phased positioning and keeping enough cash to cope with potential 3%---4% fluctuations is the way to survive right now.

Risk Warning

This report is for research discussion only and does not constitute any profit commitment or individual stock trading advice. The three categories of risks that need to be tracked most closely are: First, if oil prices and geopolitical conflicts continue to push up nominal inflation, U.S. Treasury yields may rise again, thereby pressuring high valuation tech stocks; Second, if the FOMC dot plot and officials' statements turn clearly hawkish, the market's discount for "longer and higher" will continue to deepen; Third, if the AI chain shows order slowdowns, gross margin downgrades, or EPS upward revisions stop, the semiconductor rebound will shift from valuation repair to fundamental verification failure.

|---------|------------------------|--------------------| | Risk Variable | Observation Signal | Response Principle | | Oil Prices and Nominal Inflation | Energy items continue to push CPI, 10-year U.S. Treasury yields rise | Reduce high Beta exposure, retain cash for confirmation | | Fed Communication | Dot plot or official speeches indicate more rate hikes | Don't chase rebounds, wait for interest rate shocks to release | | AI Fundamentals | Orders, gross margins, EPS guidance downgrades | Go weak and keep strong, only retain leaders with strong realization capabilities | | Crowded Trades | Semiconductor put options, SOXS funds continue to amplify | Control positions, avoid going all in at once |

Data Sources and Citation Notes

The macro data, market prices, and news background in this report are sourced from publicly verifiable sources and are listed in the footnotes and References of the charts. CPI-related metrics refer to official releases from the BLS and mainstream financial media reports, market retreats and VIX data are organized using Yahoo Finance's public chart data interface, interest rate pricing and policy expectations refer to public reports from CNBC, Benzinga, etc., and external macro background references supplement Reuters.

|----------|-------------------------------|-------------------------------| | Chart/Data Item | Usage Metrics | Main Sources | | Actual vs. Expected CPI | Nominal CPI, Core CPI YoY/MoM and Market Expectations | BLS, CNBC, Benzinga, Morningstar | | Risk Asset Retreat Chart | SMH, MTUM, MU, QQQ, SPY phase high point retreats and VIX | Yahoo Finance public Chart API | | Interest Rate Pricing Path | June FOMC, Probability of Rate Hikes This Year, Pricing for Rate Hikes Before October/December | CNBC Make It, Benzinga reports on market pricing | | Operational Framework | User strategy brief and public macro, market data cross-organization | User-provided materials, BLS, CNBC, Benzinga |

References

U.S. Bureau of Labor Statistics, Consumer Price Index --- May 2026. https://www.bls.gov/news.release/cpi.htm

CNBC, CPI inflation report May 2026, June 10, 2026. https://www.cnbc.com/2026/06/10/cpi-inflation-report-may-2026.html

Morningstar, May CPI Forecasts Show Continued Lofty Inflation. https://www.morningstar.com/economy/may-cpi-forecasts-show-continued-lofty-inflation

CNBC Make It, Rate hikes are back on the table amid rising prices, June 10, 2026. https://www.cnbc.com/2026/06/10/interest-rates-may-stay-higherwhat-it-means-for-your-money.html

Yahoo Finance Chart API, daily prices for SMH, MTUM, MU, QQQ, SPY and ^VIX, retrieved June 11, 2026. https://finance.yahoo.com/

Roger Lee Research, Rate hikes are not the killer of tech, EPS is: Weakening and strengthening strategy after the AI main line's big drop, June 8, 2026.

Benzinga, Hottest Inflation In Over 3 Years: Is The Fed Ready To Hike Interest Rates?, June 10, 2026. https://www.benzinga.com/markets/economic-data/26/06/53128579/may-cpi-reactions-fed-hold-inflation-4-2

Reuters, Gold inches higher as oil falls, US rate-hike fears cap gains, June 9, 2026. https://www.reuters.com/world/india/gold-extends-falls-rising-treasury-yields-2026-06-09/

This report is compiled by a special analyst. The views expressed in the report represent the author's personal stance and do not reflect the views of the BIT platform. This material is for reference only and does not constitute investment advice.

Risk warning

Risk warning