Bitget UEX Daily Report|US-Iran negotiations show initial setbacks, oil prices rebound; Marvell and others join the S&P 500, Samsung Hynix to list in the US; Energy Fuels receives support from the US government

Bitget UEX Daily Report

Bitget UEX Daily Report# 1. Hot News

Federal Reserve Dynamics

Deutsche Bank Shifts to Hawkish Expectations: 50 Basis Points Rate Hike in 2026

- Deutsche Bank raises its inflation forecast, expecting the Federal Reserve to hike rates twice in 2026 (totaling 50 basis points), with the federal funds rate rising to 4.1%, and does not rule out the possibility of action as early as July.

- In response to stubborn inflation and the hawkish stance of new Chair Waller, the bank reverses its previous dovish predictions, emphasizing a "longer, higher rate" environment.

- Market Impact: Traders have significantly increased the probability of a rate hike in September, short-term U.S. Treasury volatility is expected to increase, the long end of the curve is stabilizing, and interest rate-sensitive assets face repricing pressure.

International Commodities

U.S.-Iran Negotiations Start Off Poorly, Oil Prices Rebound Over 2%

- Following Trump's threat to strike Iran if Hezbollah continues to attack Israel, tensions in U.S.-Iran negotiations in Switzerland have emerged, with Iran suspending some dialogues.

- In early Asian trading, Brent crude rose over 2% to around $82.30, while WTI surpassed $78, with active trading.

- Market Impact: Geopolitical risk premiums are rising, providing short-term support for oil prices, but long-term prospects depend on negotiation progress and the situation in the Strait of Hormuz.

Macroeconomic Policy

Goldman Sachs and Other Institutions Focus on Waller's Hawkish Statements Impact on Bond Market

- In his first policy speech since taking office, Waller emphasized anti-inflation as a priority, leading the market to unexpectedly bet on an earlier rate hike.

- Goldman Sachs noted that this move would increase short-end U.S. Treasury volatility while stabilizing the long end.

- Market Impact: The fixed income market faces valuation adjustments, compounded by geopolitical factors, leading to increased uncertainty in the macro environment.

# 2. Market Review

Commodity & Forex Performance

- Spot Gold: $4187/ounce, +0.77%

- Spot Silver: $65.88/ounce, +1.53%

- WTI Crude Oil: $77.53/barrel, +2.29%

- Brent Crude Oil: $81.32/barrel, +1.77%

- Dollar Index (DXY): 100.844 points, +0.08%

Driving Factors Analysis: The renewed tensions in U.S.-Iran negotiations have reignited geopolitical concerns, driving oil prices up. Although some Gulf traffic has recovered, low inventories continue to support prices. The dollar index remains relatively stable, with hawkish signals from the Federal Reserve (such as Waller's statements and Deutsche Bank's forecasts) limiting further upside for precious metals, but inflation expectations and safe-haven demand provide bottom support. In the short term, the correlation between oil prices and gold/silver reflects the interplay of risk appetite and macro expectations; if negotiations make substantial progress, oil price pressure may increase; otherwise, volatility will persist. Institutional consensus leans towards geopolitical factors dominating the short-term oil market, while the Federal Reserve's path will influence the cross-dynamics of precious metals and the dollar.

Cryptocurrency Performance

- BTC: $63853, -0.66%

- ETH: $1728, -0.6%

- Total Cryptocurrency Market Cap: $2.27 trillion, -0.6%

- Market Liquidation Situation: Total liquidation in 24h approximately $141 million, with long positions liquidated around $97 million.

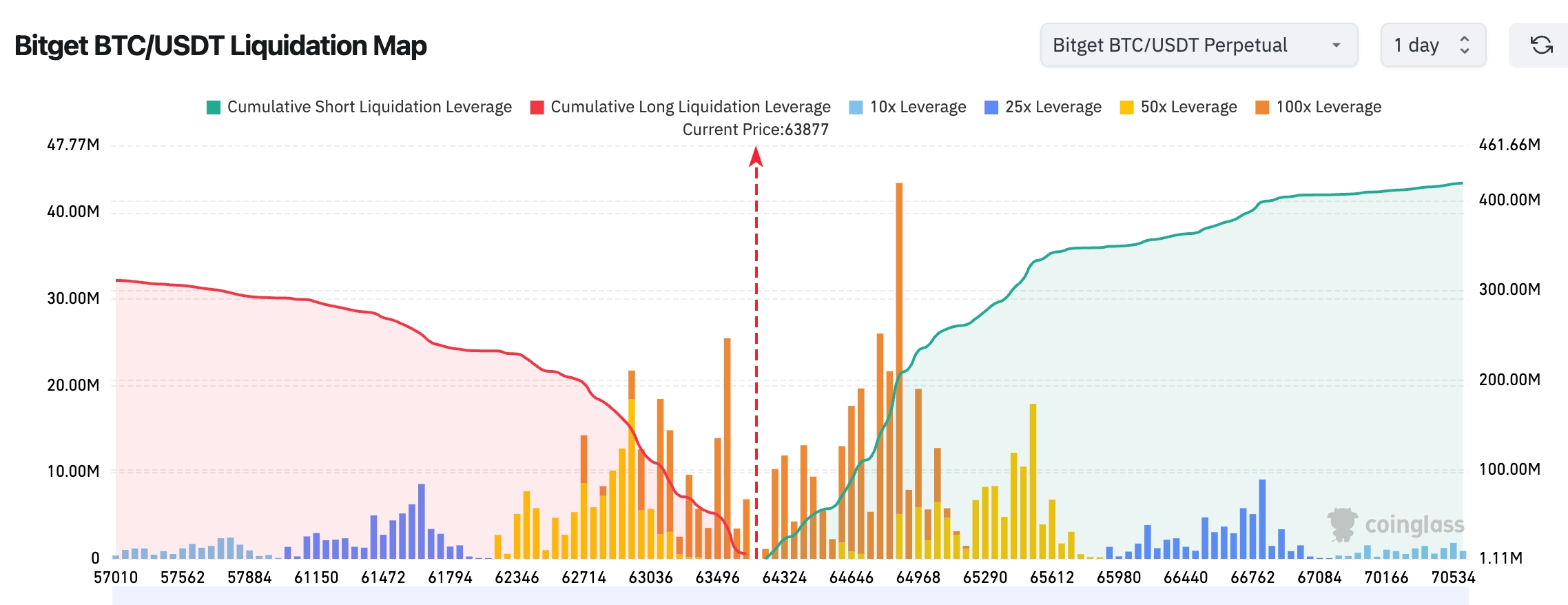

- Bitget BTC/USDT Liquidation Map: Current BTC price around $63,877, with a significant number of short liquidation positions clustered above $64,500-65,500, indicating stronger liquidation pressure than below, with a potential for upward liquidity sweep in the short term. The main long liquidation zone is concentrated around $62,700-63,200; if this area is lost, the market may face further downward pressure.

Driving Factors Analysis: Geopolitical tensions and hawkish expectations from the Federal Reserve jointly suppress risk assets, with BTC/ETH under pressure in the short term, but total market cap remains resilient. Leverage liquidation is mainly concentrated in long positions, reflecting market caution towards increased volatility. ETF fund flows show net outflows, indicating institutional short-term caution. Technically, BTC is oscillating near key support, while ETH is lagging. The macro environment (oil price rebound, U.S. Treasury yields) forms a hedge against AI narratives, with institutional views suggesting that short-term trends depend on negotiation progress and Federal Reserve signals, while long-term ETF inflows and computing power demand remain positive factors. The divergence between BTC and ETH may continue, with attention on rebound potential after leverage reduction.

U.S. Stock Index Performance

- Dow Jones: Approximately 51564.7 points, +0.14%

- S&P 500: 7500.58 points, +1.08%

- Nasdaq: 26517.93 points, +1.91%

Tech Giants Dynamics

- NVDA: $210.69, +2.95%

- AAPL: $297.20, +0.70%

- MSFT: $399.14, +2.15%

- GOOGL: $368.03, +1.17%

- AMZN: $243.15, -0.51%

- META: $577.22, +1.67%

- TSLA: $398.50, +0.55%

Performance Summary and Driving Analysis: The tech sector overall strengthened, with the semiconductor index soaring over 6%, and chip stocks collectively reaching new highs. Traditional manufacturers like Intel and AI leaders like Nvidia show clear divergence: the former benefits from advanced packaging, glass substrates, and long-term roadmap restructuring, while the latter dominates computing power demand. Amazon is negotiating the sale of custom chips like Trainium, and Google/Broadcom are replicating Nvidia's financing model, indicating that competition in AI infrastructure is evolving from single suppliers to multi-party closed loops. Valuation pressures and company-specific events (such as SpaceX bond issuance, Meta data center agreements) lead to stock disparities, but the overall trend remains driven by AI commercialization, though caution is warranted regarding macro tightening signals.

Overview of Cryptocurrency Stock Derivatives

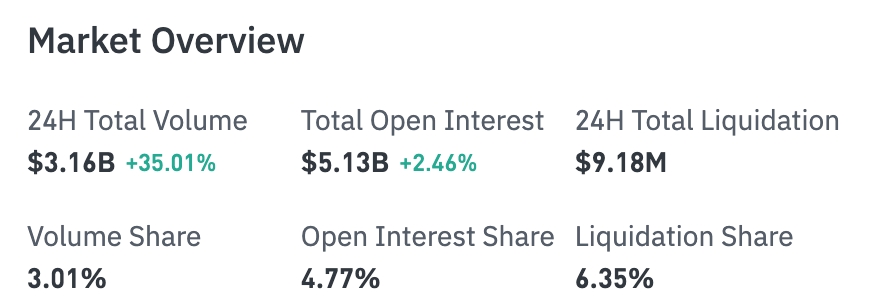

24H Total Trading Volume: $3.16 billion (+35.01%)

Total Open Interest: $5.13 billion (+2.46%)

24H Total Liquidation: $9.18 million

Proportion: Trading Volume 3.01%, Open Interest 4.77%, Liquidation 6.35%

Sector Positioning Performance (Major Sectors)

Technology: $2.64 billion

Finance: $169 million

Consumer: $70.34 million

Industrial: $30.95 million

Biotechnology: $17.3 million

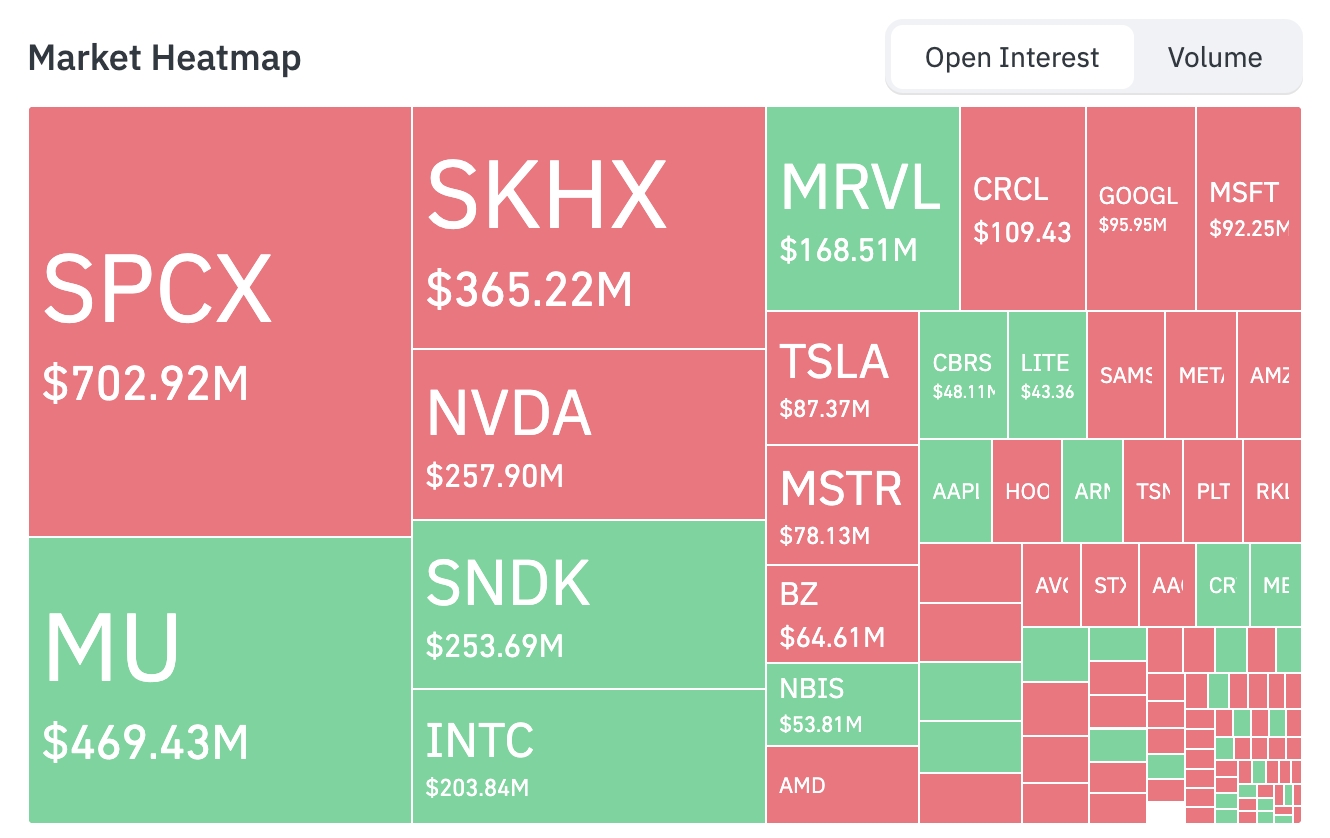

Market Heat Map (Positioning Focus)

Top Asset Position Rankings (in $100 million):

SPCX: $703 million

MU: $469 million

SKHX: $365 million

NVDA: $258 million

SNDK: $254 million

INTC: $204 million

MRVL: $169 million

CRCL: $109 million

GOOGL: $96 million

MSFT: $92 million

TSLA: $87 million

MSTR: $78 million

In terms of fund flows, MU, MRVL, SNDK, INTC, and other semiconductor-related assets have seen increased positions, while SPCX, SKHX, NVDA, TSLA, MSTR, AMD, GOOGL, and MSFT have shown signs of position reduction.

Sector Movement Observation

Semiconductor Sector Rises Over 6%

- Representative Stocks: SanDisk rises over 11%, Intel rises over 10%, Micron Technology rises over 8%, TSMC/Qualcomm rise over 6%, NXP/Broadcom/Western Digital/Applied Materials/AMD rise over 4%, ASML rises over 3%, Nvidia rises 2.95%. Multiple stocks hit closing historical highs.

- Driving Factors: The demand for AI inference is rapidly shifting from model training to commercial implementation, with the computing power gap far exceeding supply. Bernstein senior analyst Rasgon states this is the first "real chip supercycle" of his career—semiconductor industry revenue has jumped from over $800 billion last year to a target of $1.3 trillion this year. Capacity bottlenecks are spreading from GPUs to HBM high-bandwidth memory, semiconductor equipment, power supply, and even custom ASIC chip areas. Nvidia GPUs and custom chips from Broadcom are expected to coexist in this incremental market long-term, jointly addressing massive computing power demand. Amid geopolitical macro uncertainty, AI as a "certain" growth mainline further highlights the influx of funds into the entire semiconductor industry chain.

Market Implications: This movement is not only a short-term emotional release but also reflects the deepening of the AI capital expenditure cycle and supply chain restructuring. In the short term, it benefits related equipment, materials, and foundry segments, while in the medium to long term, it will test companies' execution capabilities and yield ramp-up abilities. Investors should pay attention to the potential impact of the Federal Reserve's policy path on capital expenditure rhythms and opportunities among diversified suppliers beyond Nvidia.

# 3. In-Depth Analysis of U.S. Stocks

1. Intel (INTC) - CEO Sets Long-Term Ambitious Goals

Event Overview: Intel's new CEO Lip-Bu Tan systematically elaborated on the strategic vision in a podcast interview, clearly stating the ambition to achieve a tenfold return within 5-10 years. The company is systematically restructuring its technology roadmap through advanced packaging technologies like EMIB, innovations in glass substrates, and cutting-edge materials such as synthetic diamonds to break through traditional silicon-based physical limits. The explosion of Agentic AI is significantly driving a recovery in CPU demand; the foundry business focuses on improving process yields and rebuilding customer trust, while collaborating with Musk's projects to advance initiatives like Terafab. The market expects Intel to enter a true potential release period after 2030, with its differentiated positioning in data centers and AI edge computing gradually being realized. Market Interpretation: Institutions generally recognize this systematic transformation path, believing it not only aligns with the current trend of AI computing power shifting from training to inference but also builds a long-term moat through material and packaging innovations. Analysts are focused on its potential in the GPU/CPU hybrid ecosystem, especially in seeking niche breakthroughs under Nvidia's dominant landscape. Despite facing execution risks and competitive pressures in the short term, long-term growth catalysts are clear. Investment Insight: In the short term, closely track improvements in process yields and the progress of the Terafab collaboration; in the long term, Intel's differentiated positioning in AI infrastructure is worth strategic allocation, suitable for investors optimistic about the semiconductor cycle recovery.

2. Amazon (AMZN) - Expanding Custom AI Chip Sales

Event Overview: Amazon is actively negotiating the sale of its custom AI accelerator chips like Trainium to external companies, aiming to further weaken Nvidia's absolute dominance in the AI chip market. AWS AI business head Peter DeSantis stated that AI infrastructure is evolving rapidly, with the third-generation Trainium accelerators nearly sold out and strong market demand for the fourth-generation products. The company hopes to leverage its internal scale advantages to expand its custom chip business from in-house use to external sales, building a more complete AI supply chain loop. Market Interpretation: This expansion is seen as a direct replication and challenge to Nvidia's "script," with the market assessing it as reshaping the cloud service and AI hardware supply chain landscape. Institutional views suggest that Amazon, with its massive data center demand and financing capabilities, is likely to accelerate the industry's transition from "Nvidia's monopoly" to multi-supplier competition, but it also faces challenges in technology iteration speed and ecosystem compatibility. Investment Insight: Pay attention to Amazon's diversification potential in the AI ecosystem; intensified competition may reshape industry profit distribution; investors can view it as a long-term opportunity for the integration of cloud and hardware advantages.

3. SpaceX - Plans for Large-Scale Bond Issuance

Event Overview: After completing a record IPO, SpaceX plans to initiate an investor conference call as early as this week to issue at least $20 billion in investment-grade dollar bonds to refinance a $20 billion bridge loan maturing in 2027. This bridge loan was jointly provided by Bank of America, Citigroup, JPMorgan, Goldman Sachs, and Morgan Stanley, which will also lead the bond underwriting. The related plan may still be adjusted, but it reflects the company's proactive management of capital structure optimization. Market Interpretation: Institutions view this as a key step for SpaceX to transition from high-cost bridge financing to stable long-term investment-grade debt, reflecting its strong growth prospects and debt management capabilities. A successful bond issuance will lower financial costs and provide more flexible funding support for future expansions (such as Starship, satellite networks), with investors focusing on its cash flow stability and valuation support. Investment Insight: The successful bond issuance will significantly enhance financial flexibility, benefiting long-term valuations; suitable for long-term investors focused on aerospace and high-growth technology infrastructure.

4. Energy Fuels (UUUU) - U.S. Government Supports Rare Earth Projects

Event Overview: The U.S. government signed a $725 million conditional loan agreement with Energy Fuels to support domestic rare earth separation and processing capacity construction, aiming to reduce reliance on external supply chains. This agreement aims to strengthen domestic critical mineral autonomy, and following the news, Energy Fuels' stock price rose over 8% on Thursday. Market Interpretation: Institutions believe this move is an important step in the U.S. supply chain security strategy, with the demand for rare earths as critical materials for AI, electric vehicles, and defense continuing to grow, Energy Fuels is expected to benefit from policy dividends and long-term contracts. Investment Insight: In the short term, focus on the progress of the loan agreement and project execution; in the long term, positive on structural opportunities brought by the expansion of domestic rare earth production capacity in the U.S., suitable for investors focused on commodities and national security themes.

5. Meta Platforms (META) - Data Center AI Computing Power Agreement

Event Overview: Meta has reached a new agreement with data center developer Crusoe to purchase a total of approximately 1.6 gigawatts of computing power across two data centers to support AI infrastructure expansion. Previously, Crusoe had signed contracts for a capacity of 4.9 gigawatts, with a total project pipeline exceeding 40 gigawatts. Market Interpretation: Institutions view this as a continuation of Meta's large-scale AI investment, demonstrating its proactive layout in computing power acquisition, which helps strengthen content recommendation, advertising algorithms, and Llama model training capabilities, maintaining a leading position in the competitive AI race. Investment Insight: Pay attention to the efficiency of AI capital expenditure conversion; in the long term, Meta's synergistic advantages in the integration of social and AI fields are worth noting, suitable for investors optimistic about digital advertising and generative AI growth.

# 4. Market & Project Dynamics

Institutional reports indicate that Bitcoin has held the low point of $59,200 after multiple tests and rebounded 3.54% this week to close at $65,655. This round of increase is more due to the exhaustion of selling pressure rather than new demand, as previously open futures contracts have significantly retreated from May highs, with short-term holders selling at a loss, and exchange balances dropping to a seven-year low, indicating that the market has entered a phase of deleveraging and pressure release. Short-term holders are still generally in a floating loss state of about 17%-19%, with potential selling pressure remaining heavy above. Currently, Bitcoin is trapped between two key ranges: support around $54,000 and resistance near $68,000 from short-term holders, presenting a structure of "selling pressure paused but buying not confirmed."

Cryptocurrency mining company Ionic Digital released a mining and operations update report for May 2026, disclosing a mining output of 24.77 BTC, a month-on-month increase of 21.1%, with no Bitcoin sold during the same period and maintaining a zero-debt status, increasing total holdings to 2861 BTC.

10x Research analysis points out that BlackRock's Bitcoin Enhanced Yield Exchange-Traded Fund (BITA) may have strategic design flaws, as its method of generating income through selling call options may lead investors to underperform against spot Bitcoin in most market environments, potentially failing to achieve ideal absolute returns.

Data: Tokens such as H, XPL, and SAHARA are set to unlock large amounts this week, with H unlocking approximately $54.8 million in value.

Yesterday, Michael Saylor, founder and executive chairman of Bitcoin treasury company Strategy, released further information related to Bitcoin Tracker. According to previous patterns, Strategy always discloses information about increasing Bitcoin holdings the day after relevant news is released.

# 5. Market Calendar

June 23 (Monday)

Index Adjustments Take Effect

- MRVL (Marvell Technology) joins the S&P 500 Index

- FLEX (Flex) joins the S&P 500 Index

- ALAB (Astera Labs) joins the Nasdaq 100 Index

- CRWV (CoreWeave) joins the Nasdaq 100 Index

- NBIS (Nebius) joins the Nasdaq 100 Index

- RKLB (Rocket Lab) joins the Nasdaq 100 Index

- TER (Teradyne) joins the Nasdaq 100 Index

June 24 (Tuesday)

U.S. Stock Earnings Reports

- FDX (FedEx) announces earnings after hours

June 25 (Wednesday)

U.S. Stock Earnings Reports

- MU (Micron Technology) announces earnings after hours

- Market expects EPS: $20.7

- Market expects revenue: $35.56 billion

- TCOM (Trip.com) announces earnings after hours

June 26 (Thursday)

U.S. Macroeconomic Data

- U.S. May PCE Price Index

- U.S. Q1 GDP Final Value

- U.S. Initial Jobless Claims

Important Events

- NVDA (NVIDIA) holds the 2026 Annual Shareholders Meeting

- Progress on Blackwell chip capacity

- Progress on Vera architecture chip

- Progress on AI ecosystem commercialization

- Capital return plan

June 27 (Friday)

U.S. Macroeconomic Data

- U.S. June University of Michigan Consumer Sentiment Index Final Value

To Watch (Specific Times Not Yet Confirmed)

OpenAI

- GPT-5.6 series models may be released next week

- Mini version

- Standard version

- Pro version

SK Hynix

- SEC may approve ADR listing application as early as the week of June 22

- Likely to list in the U.S. as early as August

Institutional Views:

Well-known investment bank analysts generally believe that the short-term market is dominated by uncertainties in U.S.-Iran negotiations and hawkish signals from the Federal Reserve, with oil prices receiving geopolitical support but overall risk assets under pressure. Deutsche Bank and others raising rate hike expectations reinforce the narrative of "higher for longer," which is bearish for precious metals and growth stocks; Goldman Sachs focuses on bond market volatility transmission. The tech and AI sectors show significant divergence, with the semiconductor supercycle logic still recognized, but valuation and competitive risks need to be heeded. The deleveraging in the crypto market provides potential rebound space, while ETF outflows reflect cautious sentiment. Overall, institutions recommend focusing on data validation and negotiation progress, maintaining a neutral to cautious allocation, prioritizing defense against geopolitical and policy risks.

Disclaimer: The above content is compiled by AI search, with human verification for publication, and does not constitute any investment advice. Data in the text may inevitably contain deviations; please refer to real-time market data.

Risk warning

Risk warning