Bitget UEX Daily Report|The third-in-command of the Federal Reserve signals a steady policy; SanDisk and Micron lead the AI sector, but US stocks show divergence; PCE inflation exceeds expectations, raising policy uncertainty

Bitget UEX Daily Report

Bitget UEX Daily Report# 1. Hot News

Federal Reserve Dynamics

New York Fed President Williams: Current monetary policy stance is appropriate, and it is an undeniable fact that inflation is significantly above 2%

- Williams stated that tariffs, energy prices, and AI investments are the main drivers of current inflation, expecting inflation to drop to around 3.5% by the end of 2026 and return to the 2% target by 2028; the unemployment rate will fall back to 4%.

- He emphasized that the current interest rate level is sufficient to help inflation return to the target, but significant risks still exist, and policy needs to remain flexible.

- Market Impact: Strengthened expectations for the Fed to "maintain higher rates for a longer time," short-term pressure on rate cut bets, the dollar index remains strong, and risk assets face certain pressure.

International Commodities

Iran and the dynamics related to the Strait of Hormuz continue to ferment, testing the US-Iran ceasefire agreement

- Iran is expected to earn about $40 billion annually from the Strait of Hormuz and has proposed joint charging with neighboring countries; at the same time, the Iranian Revolutionary Guard attacked a Singapore-flagged cargo ship near the strait, testing the implementation of the ceasefire agreement.

- Background of the event: Previous Middle East conflicts raised energy prices, which in turn pushed up US inflation; progress in the ceasefire had previously caused oil prices to retreat, but this incident shows the fragility of the agreement.

- Market Impact: Short-term oil prices are under pressure and retreating, but geopolitical uncertainty still provides support for the energy market, while safe-haven assets like gold are temporarily dragged down by a stronger dollar.

Macroeconomic Policy

US May PCE Price Index year-on-year rose to 4.1%, the first time exceeding 4% since April 2023

- Core drivers include rising energy prices due to the Middle East conflict and the prior impact of Trump's tariff policy; Q1 GDP final value was revised up to 2.1%, but the downward revision of private domestic purchasing power shows weak consumption momentum.

- Institutions predict that the US unemployment rate may rise to 4.7% by the end of the year, with hiring becoming cautious.

- Market Impact: Inflation stickiness exceeded expectations, combined with statements from Fed officials, leading to further convergence of market expectations for the number of Fed rate cuts this year, supporting the dollar and US Treasury yields.

# 2. Market Review

Commodity & Forex Performance

- Spot Gold: $4,021/ounce, -0.14%

- Spot Silver: $57.40/ounce, -0.72%

- WTI Crude Oil: $71.70/barrel, -0.33%

- Brent Crude Oil: $75.20/barrel, -0.4%

- Dollar Index (DXY): 101.51, -0.02%

Driving Factors Analysis: The dollar index remains strong around 101.5, driven by signals from Fed officials of "higher rates for longer" and sticky US inflation data. Gold and silver are under pressure and retreating amid a stronger dollar and fluctuations in risk appetite, but geopolitical uncertainty in the Middle East still provides some safe-haven support. Oil prices have slightly retreated under the intertwining of US-Iran ceasefire progress and Strait of Hormuz events, with market expectations for supply recovery heating up, but the fragility of the agreement limits the downside. In the short term, the dollar's movement and the Fed's policy path remain core variables for precious metals and energy prices. Institutions generally believe that if inflation data continues to exceed expectations, precious metals may maintain range-bound fluctuations, while oil prices need to pay attention to geopolitical developments and OPEC+ dynamics.

Cryptocurrency Performance

- BTC: $59,595, -2%

- ETH: $1,565, +3.25%

- Total Cryptocurrency Market Cap: $2.14 trillion, -1.4%

- Market Liquidation Situation: Total liquidation in 24h approximately $887 million, long positions liquidation approximately $691 million

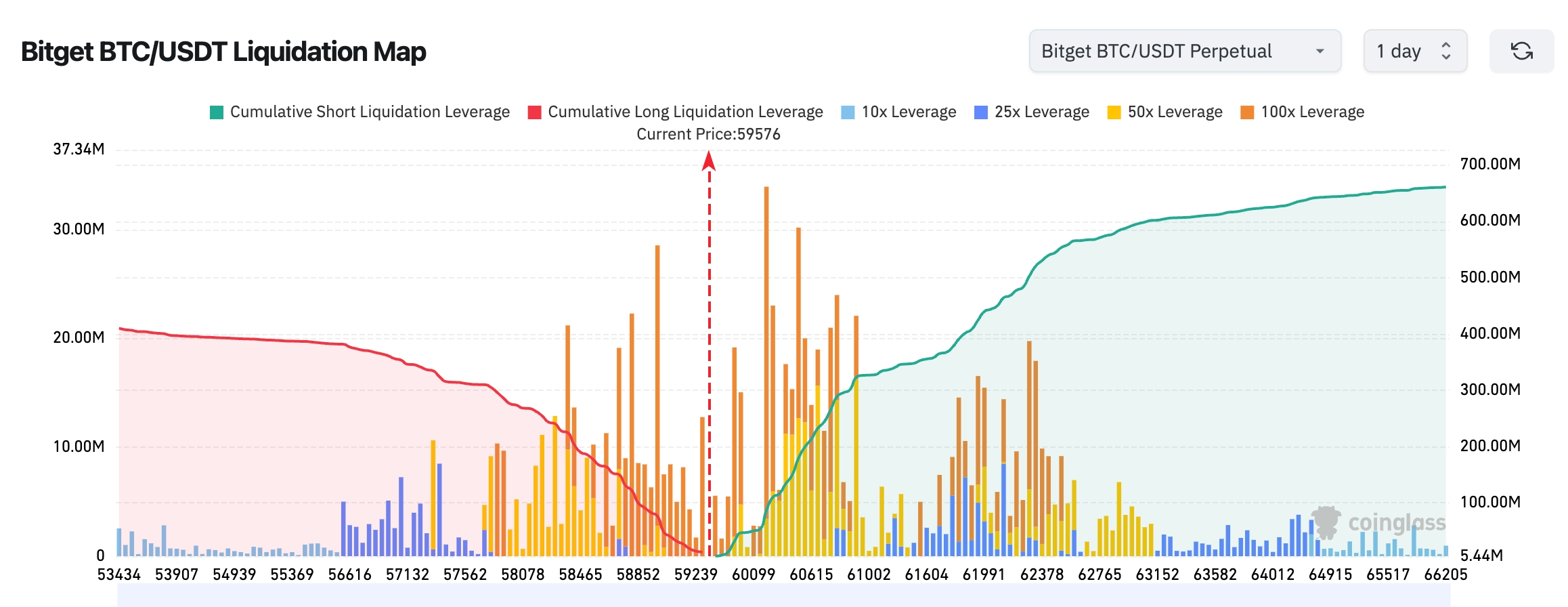

- Bitget BTC/USDT Liquidation Map: Current BTC price approximately $59,576, with a large number of long liquidation points clustered in the range of $58,500-$59,300; if it falls below key support, it may trigger a chain reaction of long stop-losses, accelerating the decline. The upper range of $60,000-$62,500 has a significantly larger accumulated short liquidation scale, overall liquidity still leans towards attracting prices upwards, but in the short term, it needs to hold above $59,000 to avoid a bearish-dominated market.

- Spot ETF Net Inflow/Outflow: BTC spot ETF saw a net outflow of $414 million yesterday, with a net outflow of $469 million the day before, totaling a net outflow of $997 million over three consecutive days.

Driving Factors Analysis: Bitcoin fell below the $60,000 mark and hit a recent low, mainly influenced by the US May PCE inflation data exceeding expectations, with the market worried that the Fed may maintain higher rates for a longer time, putting pressure on risk assets. A significant wave of long liquidations occurred in the leveraged market, with the liquidation amount close to $900 million in 24h. ETF funds continue to show a net outflow trend, reflecting institutions' cautious wait-and-see attitude in a high-volatility environment. ETH's performance is relatively weak, showing some divergence from BTC. From a technical perspective, BTC needs to pay attention to the effectiveness of the $58,000 support in the short term; if it fails to hold, it may further test lower ranges; on the upside, it needs to effectively break through $62,000 to open up rebound space. Overall, macro uncertainty dominates short-term trends, and institutional views lean towards considering the current adjustment as a normal correction after high valuations, but caution is needed for further escalation of geopolitical and policy risks.

US Stock Index Performance

- Dow Jones: 51,920.62 (+0.14%)

- S&P 500: 7,357.49 (-0.01%)

- Nasdaq: 25,358.60 (-0.46%)

Tech Giants Dynamics

- NVDA: $200, -1.9%

- AAPL: $275, -6.1%

- MSFT: $357, -3.5%

- GOOGL: $344, -0.5%

- AMZN: $228, -3.0%

- META: $557, -4.5%

- TSLA: $376, -6.1%

- MU: $1,214, +15.7%

- SPCX: $150, +1.3%

Performance Summary and Driving Analysis: US stocks show a clear divergence pattern, with memory and chip stocks related to AI infrastructure significantly leading the gains (Micron, SanDisk, etc. rose over 15%), reflecting the market's optimistic expectations for the sustainability of AI capital expenditures; in contrast, consumer tech giants like Apple, Microsoft, and Amazon faced sell-offs due to product price increases, with Apple experiencing a single-day drop of over 6%, the largest single-day decline since April 2025. The driving factors differ significantly: memory stocks benefit from strong demand for HBM and storage chips from AI data centers, with companies like Micron exceeding earnings expectations, directly boosting the sector; meanwhile, large tech stocks are forced to raise prices due to rapidly rising storage chip costs, raising market concerns about demand elasticity and profit margins. Overall sector trends indicate that the AI theme is still fermenting, but high-valuation consumer tech stocks face cost transmission pressures. Institutional views suggest that this divergence will continue, with funds favoring stocks in the AI supply chain with high earnings visibility.

Overview of Cryptocurrency Stock Derivatives

- 24H Total Trading Volume: $20.199 billion (-4.77%)

- Total Open Interest: $5.571 billion (+1.78%)

- 24H Total Liquidation: $30.948 million

- Trading Volume Proportion: 8.85%

- Open Interest Proportion: 5.37%

- Liquidation Proportion: 3.48%

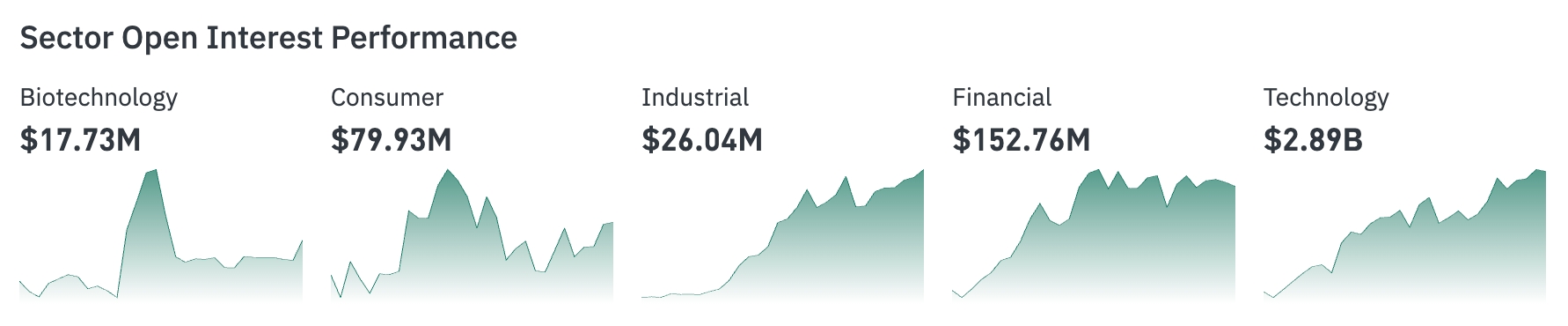

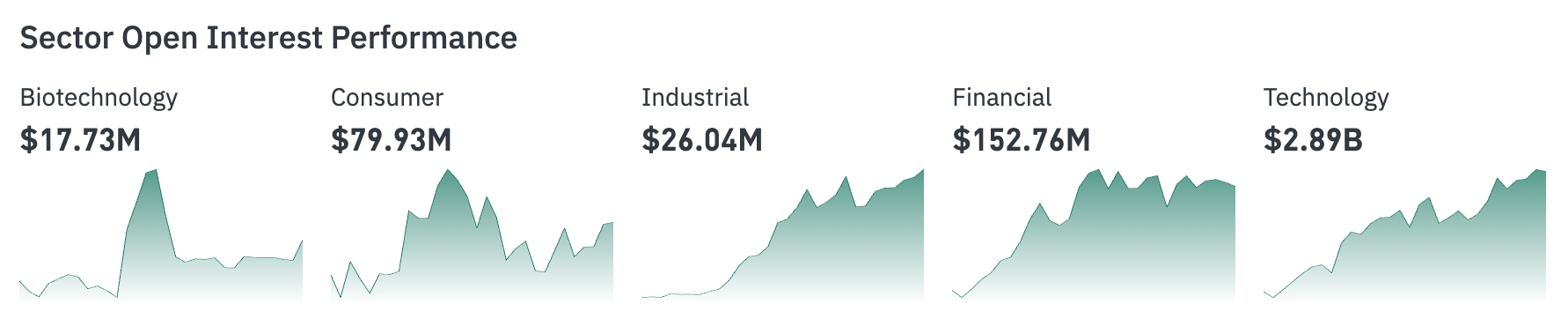

Sector Position Performance

- Biotechnology: $17.7296 million

- Consumer: $79.9109 million

- Industrial: $26.0645 million

- Financial: $153 million

- Technology: $2.893 billion

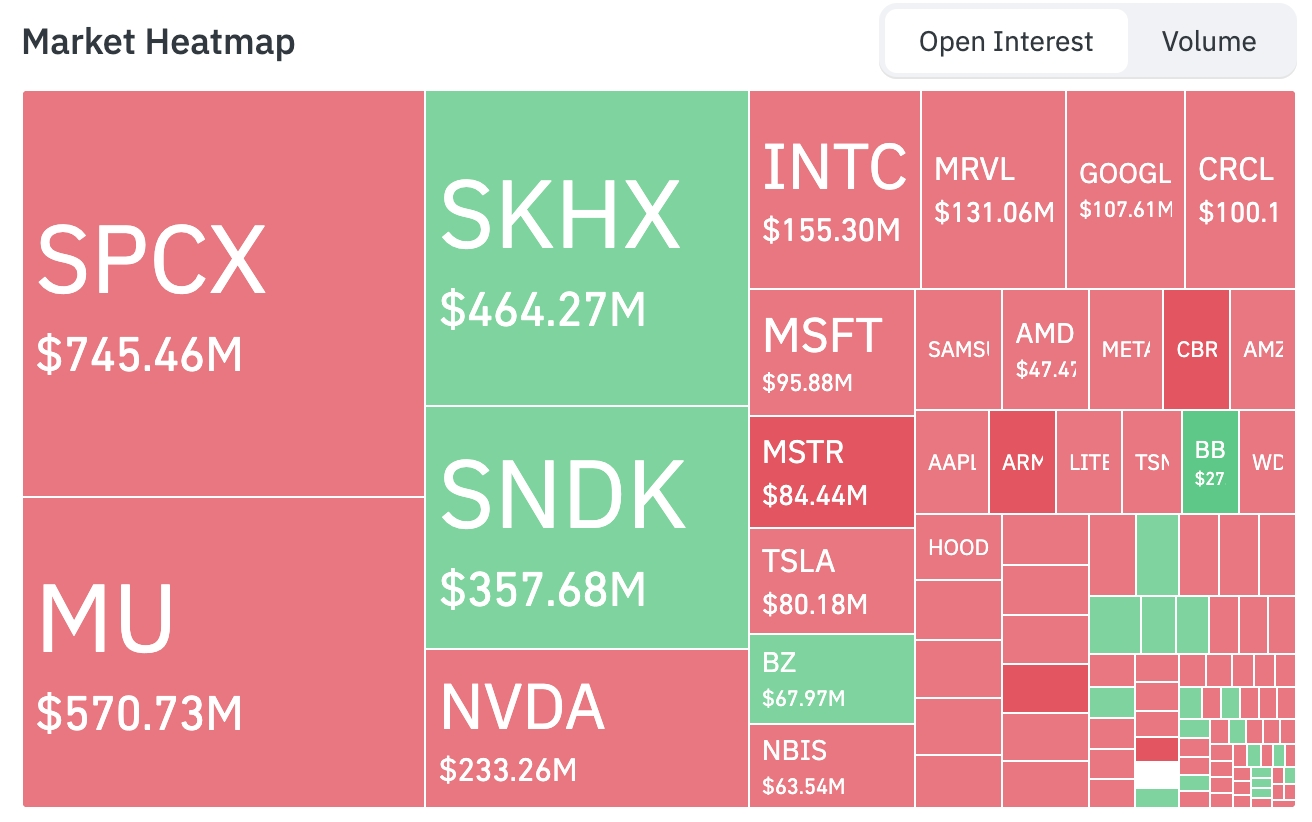

3. Market Heatmap

Largest Positions/Hot Targets:

- SPCX: $745 million

- MU: $571 million

- SKHX: $463 million

- SNDK: $357 million

- NVDA: $233 million

Sector Movement Observation

Memory and AI chip sectors surged over 15%, with the AI infrastructure theme continuing to ferment, forming a stark contrast with consumer tech stocks.

Representative stocks: Micron (MU) +15.74%, SanDisk (WDC-related) +21%+, Applied Materials (AMAT) +13%+

Driving Factors Analysis: Micron's quarterly performance significantly exceeded expectations and raised its full-year guidance, primarily due to explosive growth in demand for high-bandwidth memory (HBM) driven by AI training and inference. Currently, the capacity and bandwidth of HBM3/HBM3E chips have increased several times compared to the previous generation, with new generation GPUs like NVIDIA Blackwell requiring 3-8 times more HBM than previous generations, leading to continued global HBM capacity tightness. As one of the few manufacturers capable of mass production and design of HBM, Micron has significantly improved order visibility and ASP, directly driving margin expansion and earnings exceeding expectations. Semiconductor equipment manufacturers like Applied Materials benefit from capital expenditures brought by advanced packaging, 3D stacking, and memory production line expansions; storage manufacturers like Western Digital also rise due to AI data centers' demand for high-speed NAND flash.

This surge sharply contrasts with large consumer tech stocks (such as Apple and Microsoft, which faced sell-offs due to price increases driven by rising storage costs), highlighting the market's differentiated pricing between "AI capital expenditure with high ROIC certainty" and "weak consumer demand elasticity." Even in the macro environment where May PCE inflation rose to 4.1% and Fed official Williams released signals of "higher rates for longer," AI-related supply chains are still viewed as a non-discretionary growth track, with funds continuously flowing into pure AI enabling segments. Institutional views suggest that if hyperscaler capital expenditure guidance remains strong (historical data shows high visibility of AI ROI), the excess returns of memory and equipment sectors may continue until 2027; however, caution is needed if macro data continues to deteriorate or geopolitical risks escalate, leading to a slowdown in overall tech spending. In the short term, the sector has shown some profit-taking pressure, and it is recommended to pay attention to opportunities for phased allocation during pullbacks and Q3 capacity ramp-up data verification.

# 3. In-Depth Analysis of US Stocks

1. Micron Technology - AI Memory Demand Exceeds Expectations Driving Performance Surge

Event Overview: Micron Technology announced quarterly earnings, with revenue and profit significantly exceeding market expectations, primarily due to strong demand for high-bandwidth memory (HBM) and DRAM from AI data centers. The company's management raised its full-year guidance, significantly alleviating market concerns about the AI capital expenditure cycle. Market Interpretation: Several investment banks raised Micron's target price, believing that AI infrastructure construction is still in the early stages, with a clear upward trend in the memory cycle, and the tight supply situation will support prices and margins. Some institutions pointed out that Micron's capacity ramp-up in the HBM field is ahead of its peers, making it a core beneficiary of the current AI wave. Investment Insight: The memory and storage segments under the AI theme still hold allocation value, and it is recommended to pay attention to earnings visibility and capacity expansion rhythm.

2. Apple - Rising Storage Chip Costs Prompt Product Price Increases Raise Market Concerns

Event Overview: Apple announced price adjustments for product lines such as Mac and iPad, with increases of up to $300, due to "unprecedented" rapid increases in storage and memory chip prices driven by AI data center demand. The company also adjusted its chip strategy, skipping some iterations of the M series and prioritizing AI-optimized architectures. Market Interpretation: The market is concerned that price increases may suppress demand elasticity, especially against the backdrop of an unstable recovery in consumer electronics. Institutional views are divided: some believe this is a necessary measure under cost pressure, benefiting margins in the long term; others point out that high-price strategies may accelerate user migration to the Android camp, with short-term stock price pressure reflecting caution about demand prospects. Investment Insight: Pay attention to the rhythm of Apple's AI hardware rollout and demand feedback after price increases, and look for allocation opportunities during short-term fluctuations.

3. Western Digital - AI Storage Demand Drives Increase in NAND/SSD Market Share

Event Overview: Western Digital (WDC), as a representative of the storage sector, surged significantly following Micron's performance exceeding expectations, with the market recognizing its direct beneficiary position in the expansion of AI data centers. Market Interpretation: Institutions believe that AI training and inference are driving exponential growth in demand for enterprise-grade NAND and SSDs, and Western Digital, with its market share advantage and product portfolio in this field, fully benefits from the expansion of data center storage capacity. The cautious expansion on the supply side provides upward space for profitability. Investment Insight: Pay attention to Western Digital's quarterly inventory levels and ASP trends, as a satellite holding under the AI theme, complementing core memory stocks.

4. Corning - Accelerated Demand for Data Center Interconnect Materials

Event Overview: Corning (GLW) and other data center material suppliers benefit from accelerated AI server deployments, with demand for fiber optic and glass substrate products rising simultaneously. Market Interpretation: The demand for high-speed interconnects from AI data centers is driving growth in orders for Corning's fiber optic solutions, which institutions view as an indispensable supporting element in AI infrastructure construction, with demand continuing to expand as server scales increase. Investment Insight: Corning is suitable as an indirect beneficiary of AI capital expenditures, with a focus on tracking validation signals for data center capital expenditures.

5. BlackBerry - Edge Computing and Security Layout and Collaboration with NVIDIA Attracts AI Market Attention

Event Overview: BlackBerry (BB), leveraging its long-term accumulation in edge computing and security, has gained additional attention in AI discussions, especially as AI deployment expands from the cloud to the edge, with its QNX security operating system and deepening collaboration with NVIDIA further highlighting the applicability of its solutions. Market Interpretation: AI-driven security platforms like Cylance help BlackBerry enter the AI edge device and IoT security market, providing real-time threat detection and protection support for distributed data centers, autonomous driving terminals, and industrial IoT devices. The expansion and integration of the company's QNX security OS with NVIDIA's IGX Thor platform (covering robotics, medical, and industrial systems) builds a security-critical unified platform for edge AI, aligning with the industry trend of AI applications migrating from centralized training to edge inference. Institutions believe that in the context of tightening data privacy regulations and frequent cyberattacks, BlackBerry's end-to-end security capabilities have a differentiated competitive advantage and are expected to occupy a place in the full chain of AI infrastructure. Although the core business transformation still faces challenges, the growth potential brought by the AI security sub-track and collaboration with NVIDIA is recognized by analysts. Investment Insight: BlackBerry can serve as an auxiliary holding in the AI security and edge computing theme, with investors needing to closely track its collaboration progress with NVIDIA, contract landing situations in the IoT/AI security market, partner dynamics, and changes in quarterly revenue contributions; it is suitable to pair with pure AI hardware/storage stocks in the portfolio to diversify single-theme risks while paying attention to the impact of the macro interest rate environment on its valuation recovery.

# 4. Project & Market Dynamics

After not purchasing ETH for 8 months, Ethereum treasury company Sharplink today restarted its accumulation, receiving 5,000 ETH ($7.85 million) from FalconX 6 hours ago. It currently holds 876,000 ETH ($1.37 billion), with an average cost of $3,609, resulting in an unrealized loss of $1.789 billion (-56%).

The 90-day correlation between Strategy perpetual preferred stock STRC and Bitcoin prices has risen to nearly 0.70, the highest level since the product's launch in July 2025. This month, STRC fell 23% to $76, while BTC prices dropped nearly 20% to below $60,000, with both weakening simultaneously.

Once famous for physical keyboard phones, BlackBerry has quietly transformed into a key software layer provider for the "physical AI" and robotics ecosystem, with its QNX software framework known as the "never crash" autonomous machine neural system, providing a safe, reliable, and deterministic real-time operating system for chip manufacturers like Nvidia and AMD for smart cars and warehouse robots.

In response to CoinDesk's report that Kraken's parent company Payward is negotiating to acquire a 15% stake in the Aave protocol at a valuation of $385 million (equivalent to only 30% of AAVE token FDV), Aave founder Stani Kulechov responded on the X platform, stating, "We will never sell AAVE at a 70% discount," and pointed out that CoinDesk's report was inaccurate.

Multicoin released a report stating that the native token HYPE of Hyperliquid is currently severely undervalued at around $63. Multicoin gives a target price of $319 for HYPE in 2028 under the base scenario, expecting Hyperliquid's annual revenue to be around $8 billion, calculated at a 20x price-to-earnings ratio. Multicoin disclosed that it has been actively buying HYPE since February and is now one of its largest positions in its liquidity hedge fund.

TD Cowen analysts stated that if SpaceX cannot reach a network sharing agreement, it may accelerate its wireless business layout through the acquisition of T-Mobile. The existing partnership between T-Mobile and Starlink is strategically aligned. This idea is purely speculative but highlights the growing competitive pressure SpaceX faces in the telecommunications industry.

Based on Bitcoin's current price of $59,600 and a 200-day dollar-cost averaging (C200) of $75,821, the Ahr999 bottom-fishing indicator is approximately 0.287, in the extremely undervalued range; the year's low was 0.27 on February 6, 2026. Statistical data shows that Ahr999 below 0.3 is an extremely rare signal, usually only appearing during systemic panic or bear market bottoms. Historically, this indicator has fallen below 0.3 during early market phases in 2011, the bear market bottom in 2018 (minimum around 0.24), the COVID flash crash in 2020, and during the FTX collapse and ETH liquidation events in 2022.

# 5. Today's Market Calendar

Data Release Schedule

|-------|----|------------------|------| | 08:30 | US | May Advance Goods Trade Balance | ⭐⭐⭐ | | 08:30 | US | May Retail Inventories (excluding autos) MoM Advance | ⭐⭐ | | 08:30 | US | May Wholesale Inventories MoM Advance | ⭐⭐ | | 10:00 | US | June University of Michigan Consumer Sentiment Index Final | ⭐⭐⭐⭐ |

Important Event Preview

- Fed Officials' Speeches: Chicago Fed President Goolsbee and several other officials may speak, with the market paying attention to their latest statements on inflation and policy paths.

Institutional Views:

Based on the performance of US stocks, precious metals, crude oil, forex, and cryptocurrencies over the past 24 hours, mainstream investment banks and strategists are leaning towards cautious optimism. Signals released by Fed officials like Williams, indicating that "the current policy stance is appropriate, and the inflation target may be extended to 2028," are interpreted by the market as suggesting that the number of rate cuts this year may be fewer than previously expected, supporting the dollar and US Treasury yields. Inflation data exceeding expectations (PCE 4.1%) reinforces the narrative of "higher rates for longer," but the strong momentum of AI capital expenditures provides support for structural opportunities in US stocks, with the performance of memory and chip stocks confirming this logic. Precious metals and cryptocurrencies are temporarily pressured by a stronger dollar and fluctuations in risk appetite, but institutions generally believe that the current adjustment magnitude has partially reflected macro uncertainty, and long-term allocation value remains. Some strategy reports indicate that if geopolitical situations further ease and inflation data does not continue to exceed expectations, risk assets may welcome a phase of recovery; conversely, caution is needed regarding the chain reactions brought by further strengthening of the dollar. Overall, the market is transitioning from a "loose expectation" phase to a "data validation" phase, with structural divergence likely to become the main theme for some time to come.

Disclaimer: The above content is compiled by AI search, with human verification for publication, and should not be considered as any investment advice. The data in the text inevitably contains deviations, please refer to real-time market data.

Risk warning

Risk warning

Popular articles